You may recall that there are only 4 1-year T-Bills issued each year.

And it just so happens that the next 1-year T-Bills will be up for auction next week – Thursday, 19 October 2023.

Given the rise in T-Bills yields of late, you might be able to lock in pretty decent yields, which could be especially attractive for CPF-OA buyers.

3 questions I wanted to discuss:

- What is the estimated yield of the next 1-year T-Bills auction?

- 1-year T-Bills a must buy for CPF-OA buyers?

- What about for cash buyers?

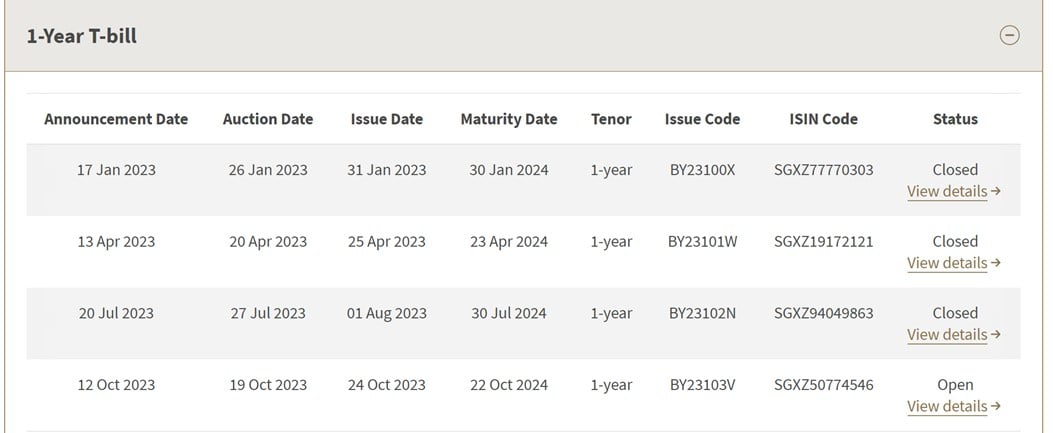

Last 1-year T-Bills auction for 2023 (BY23103V 1-Year T-bill)

First off – this is the final 1-year T-Bills auction for 2023.

CPF-OA buyers should submit your bid by 17 October.

Cash buyers should submit your bid by 9pm on 18 October.

What is the estimated yield of the 1-year T-Bills? (BY23103V 1-Year T-bill)

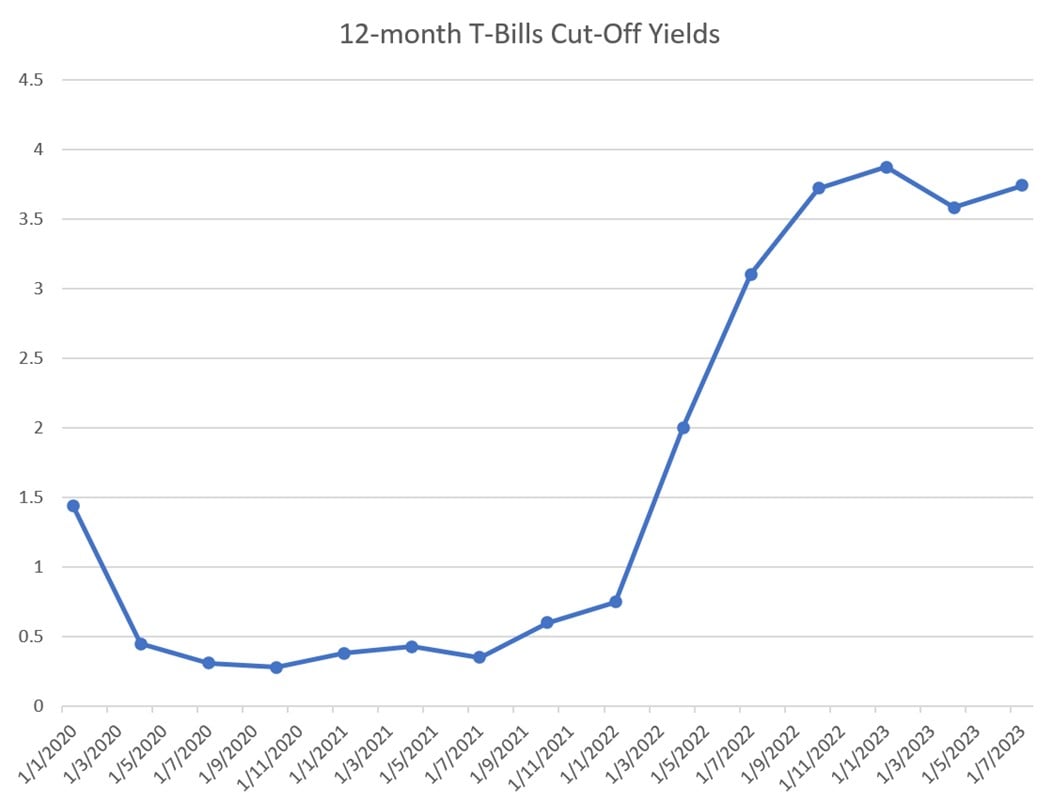

1-year T-Bills trade at 3.83% on the open market

After the recent jump in 6-month T-Bills interest rates.

The same has happened for the 1-year T-Bills.

Which trades at 3.83% today.

US Interest Rate trend is flat

Here’s the trend for the US 1-year T-Bills.

Pretty much flat for the past few months since July.

Market is not pricing in any big changes in US interest rates, which indicates the Singapore 1-year T-Bills should be relatively stable as well.

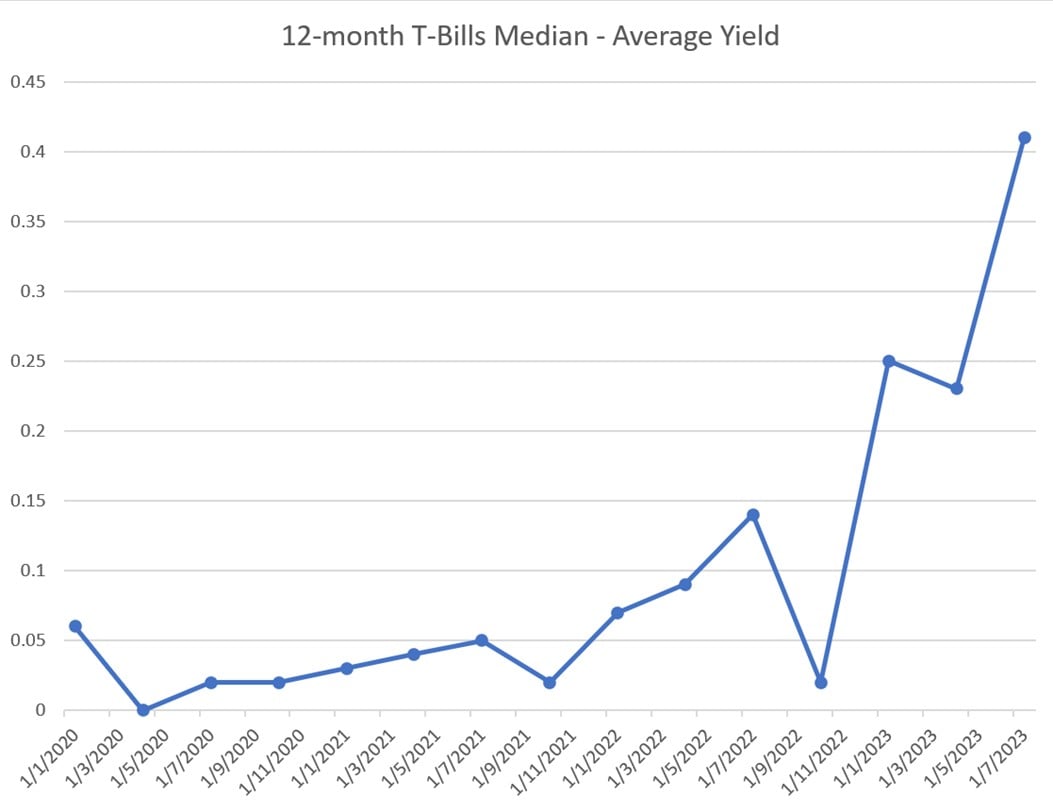

1-year T-Bills usually come in slightly below market yields (because of CPF-OA demand)?

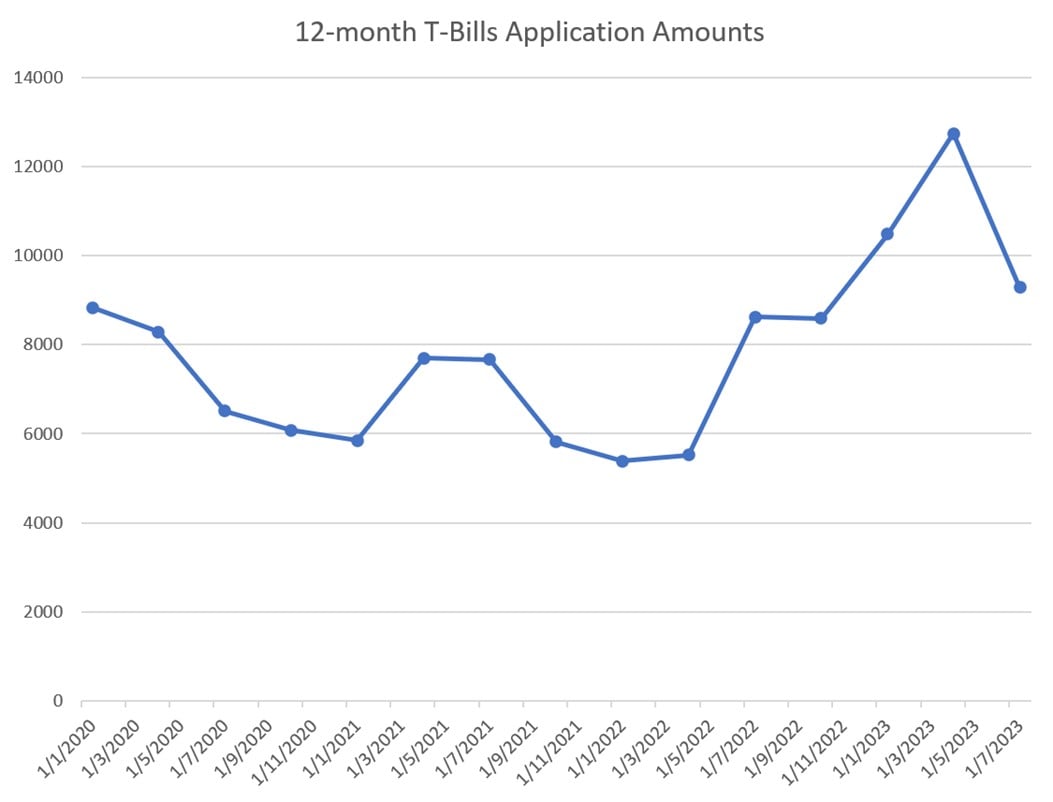

The wildcard here is T-Bills demand.

For the past 5 auctions, the 1-year T-Bills yields have come in below market yields because of higher demand.

You can see the demand picture reflected below.

Since T-Bills yield started going up in late 2022, demand for the 1-year T-Bills have gone up significantly compared to where it was previously.

This demand is likely driven largely by retail investors.

You can see the spread between Median and Average yields blowing out for the past few auctions.

This indicates a lot of low-baller bids.

Which I suppose makes sense if you’re using CPF-OA funds to apply (anything above 2.9% is already higher than CPF-OA even after factoring in lost interest).

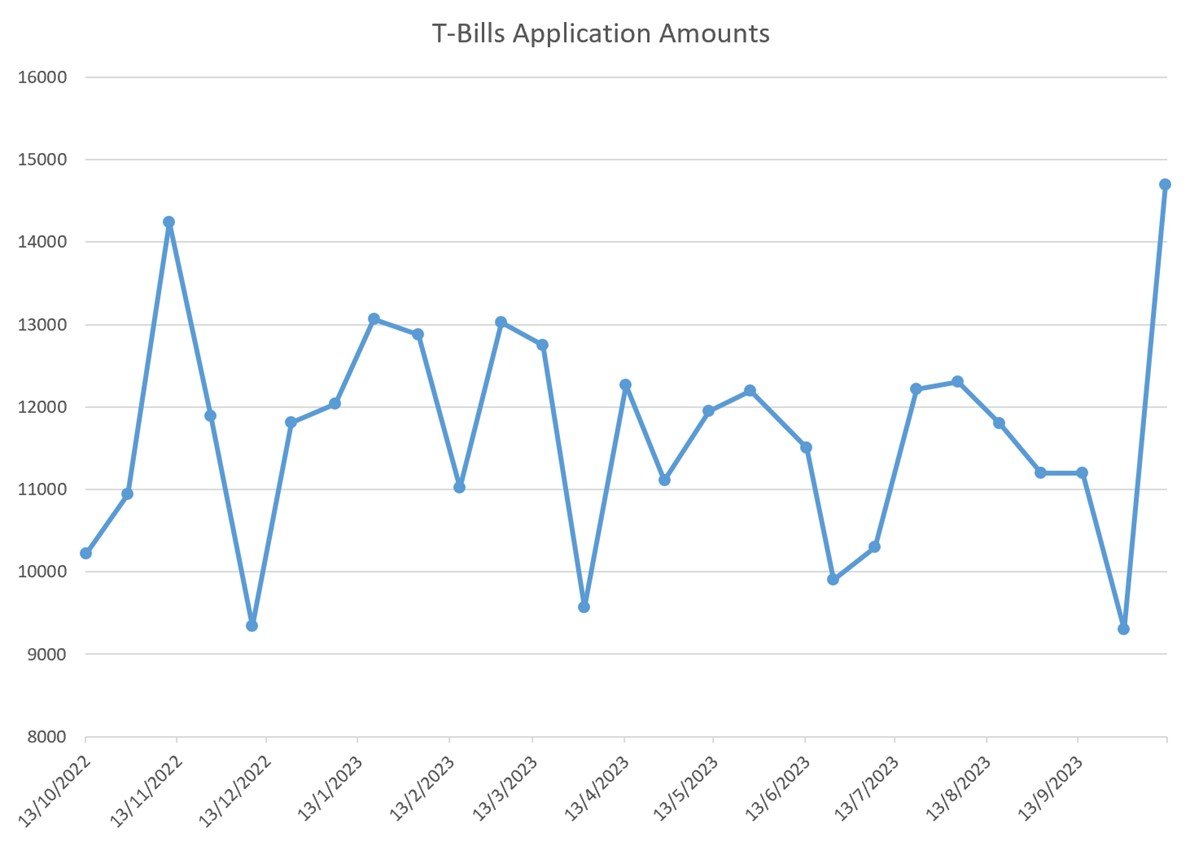

Will demand for 1-year T-Bills remain high?

So the million dollar question is whether investor demand for the next 1-year T-Bills will remain high.

Demand for the latest 6-month T-Bills auction jumped massively, to the point where non-competitive applications don’t get full allotments:

I think there is a chance you may see some of that demand spill over to this round of T-Bills.

And coupled with CPF-OA buyers, you may see demand come in strong.

Estimated Yield of 3.6 – 3.8% for the 1-year T-Bills Auction?

Because of that, I’m going to be slightly conservative in my estimates here.

I think you’ll see the cut-off yields come in below the market yields of 3.83%.

I’ll go with an indicative range of 3.6% – 3.8% estimated yield for the next 1-year T-Bills auction on 19 October 2023.

As always though, I encourage investors to submit a competitive bid.

Just in case there is a freak result and yields plunge.

Risk of Interest Rate cuts going forward?

Where we are in the interest rate hike cycle.

I think there is a good chance the Feds may start cutting interest rates in 2024.

The only question is when, and how fast.

Market is pricing in 3 rate cuts in the second half of 2024, but frankly at this point in the cycle I think the risk is tilted to the downside here (for faster and harder rate cuts than priced in).

Given that the yields on the 6-month and 12-month T-Bills are quite close (ie. You are not penalised for taking the longer duration, like you were earlier this year).

It may not be a bad idea to start locking in interest rates for longer durations at current levels.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great charts & insights on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

1-year T-Bills a must buy for CPF-OA Buyers?

This is especially the case for CPF-OA buyers (especially if you know that you will not use the CPF-OA money for the next 1-year).

This is because with the 1-year T-Bills you:

- Don’t need to roll over until 1-year later (minimises lost CPF-OA interest, and time and hassle)

- Lock in interest rates for 1-year (just in case they drop).

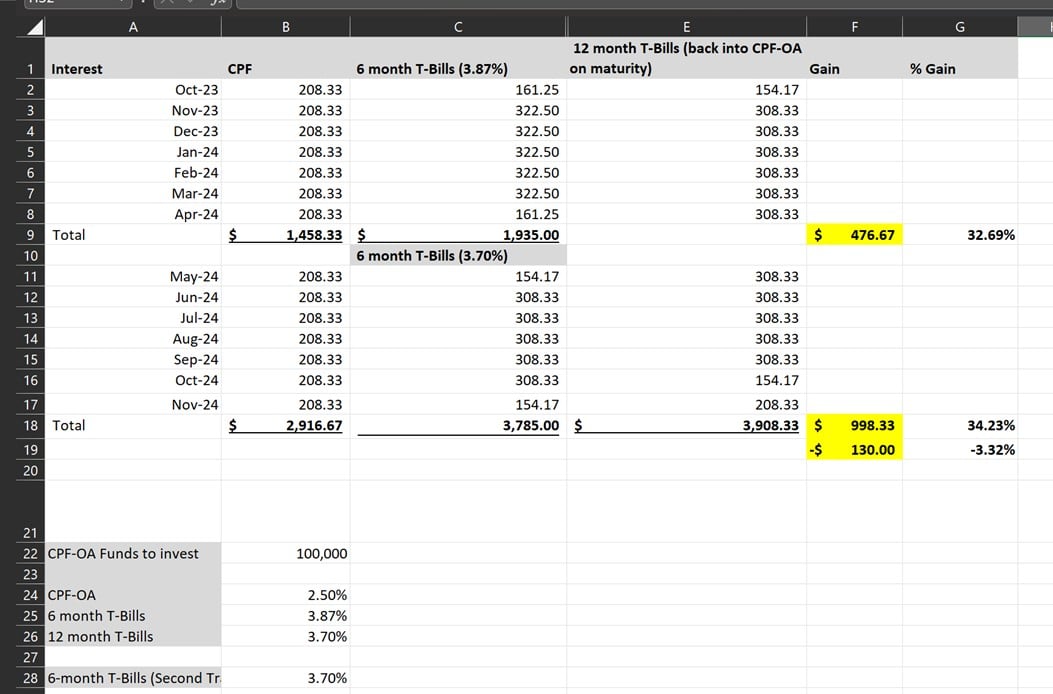

I’ve run the numbers below, assuming that:

- 1-year T-Bills are issued at 3.70%

- 6-month T-Bills are issued at 3.87%, and rolled over at 3.70% in May 2024

You can see that the 1-year T-Bills actually come out ahead here, although the numbers are very close.

What are the risks for CPF-OA buyers?

The big question mark here of course, is:

- Where will 6-month T-Bills yields be in 6-months?

- How quickly can you roll over the maturing T-Bills into new T-Bills (to minimise lost interest)

Whatever the case, I think the numbers are incredibly close here.

To the point that for CPF-OA buyers, it might not be a bad thing to just go with the 1-year T-Bills, and save the time and hassle for the next 1-year.

You don’t need to bother refinancing in 6 months, and whatever happens with interest rates from here you’re covered for the next 12 months.

Just make sure you don’t need to touch those CPF-OA funds for the next 12 months though.

What about cash buyers?

For cash buyers though – it gets interesting.

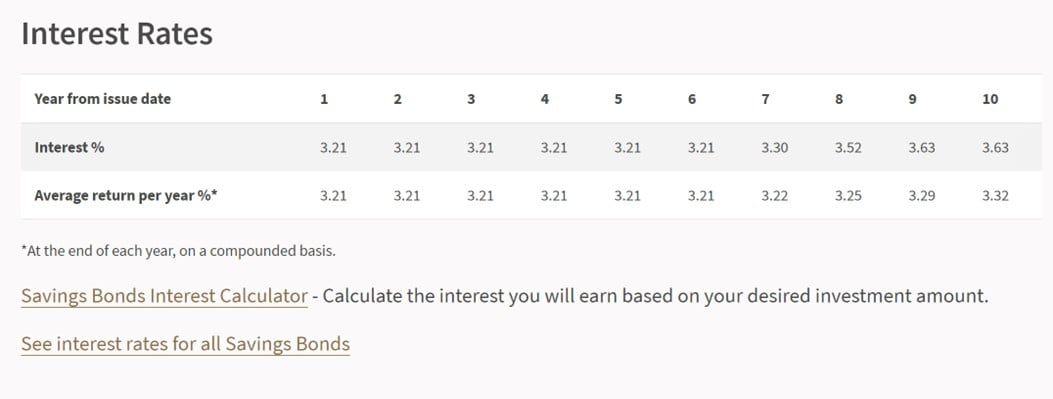

Latest Singapore Savings Bonds are offering 3.21% for the first 6 years.

This is going to get even better next month, due to the rise in SG 10 year yields.

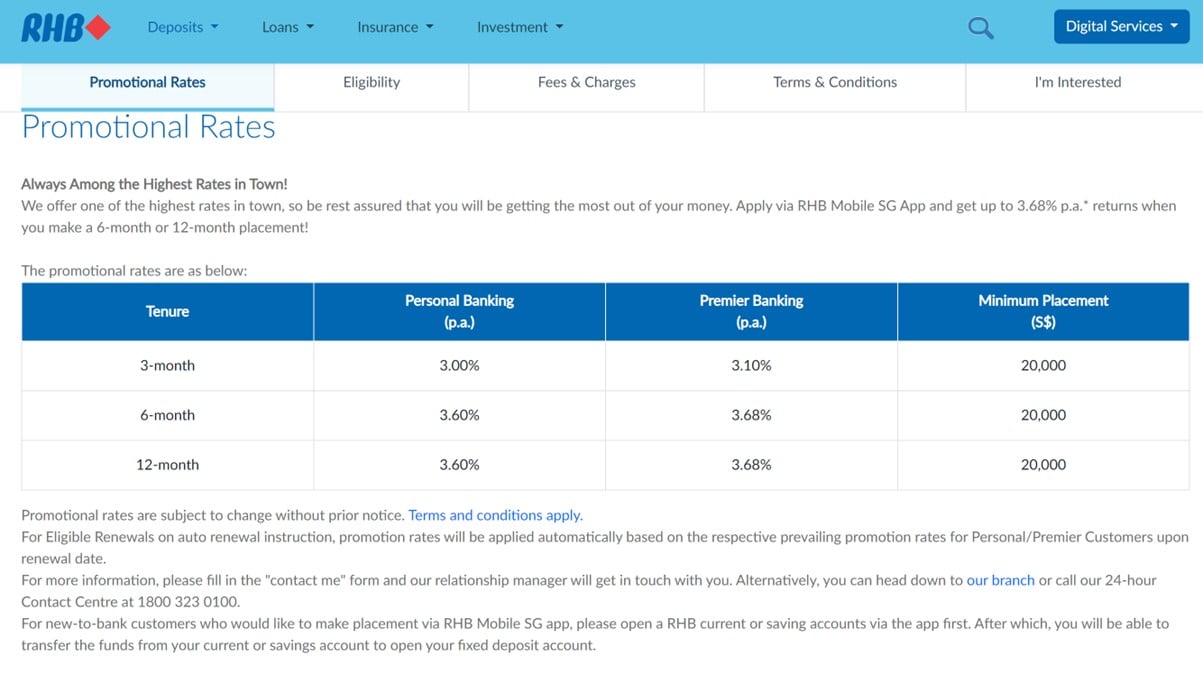

Whereas the best fixed deposit option will be 3.60% with RHB Bank.

Would I buy 1-year T-Bills with cash?

So yes, 1-year T-Bills will still offer higher yields at 3.60% – 3.80%.

But you do have to sacrifice the liquidity for 1-year, as you can easily exit T-Bills before maturity.

Is it worth it?

Personally for me I don’t think it’s worth it, and I would stick with 6-month T-Bills for my own cash.

Given the sharp rise in Singapore 10 year yields, I think there are going to be great opportunities to lock in longer duration yield in the months ahead.

Whether it’s Singapore Savings Bonds, REITs, or Fixed income.

But in any case, there’s no right or wrong here.

I leave individual investors to decide for themselves the right course of action.

This article was written on 13 Oct 2023 and will not be updated going forward.

For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do sign up as a Patreon.

– Get up to USD 2000 worth of shares

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 2000 free fractional shares.

You just need to:

- Fund any amount

- Hold for 30 days

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Investment Research Tools

I use Trading View for my research and charts. Get $15 off via the FH affiliate link.

I also use Koyfin for fundamental and macro research. Get a 10% discount via the FH affiliate link.

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Best investment books to improve as an investor in 2023?

Check out my personal recommendations for a reading list here.

The content here is for informational purposes only and should NOT be taken as legal, business, tax, or investment advice. It does NOT constitute an offer or solicitation to purchase any investment or a recommendation to buy or sell a security. In fact, the content is not directed to any investor or potential investor and may not be used to evaluate or make any investment. Do note that this is not financial advice. If you are in doubt as to the action you should take, please consult your stock broker or financial advisor.

Can you share your view on buying US T-Bills via IBKR at 5.4% interest while taking the FX risk?

I presume you mean the 2 year T-Bills?

I shared some thoughts on it here: https://financialhorse.com/singapore-savings-bonds-pay-3-32-yield-buy-now-or-wait-for-higher-yields/

Long story short is that it works, but because of the short duration its primarily a yield play (unless you leverage up but as retail investor you wont have access to that kind of leverage that hedge funds use then they long the 2Y vs short the 20Y). As a SG investor you need to note the FX risk as well.

I’ve just realised the downside of the competitive bid for the 1 year bills. At the cut-off price, the competitive bids were only 64% allotted in this round. I consider that loss to be much worse than the risk of a freak cut-off yield using a non-competitive bid, which have been 100% allotted in all past 1 year bill auctions.

True, there are pros and cons with each approach.

This point might be more unique for the 1 year T-Bills – as certain 6-month T-Bills don’t see full allotment for non-competitive if particularly hot.