You know that the IPO market in Singapore is not doing so great when the Lendlease Global REIT IPO becomes the “Biggest” IPO all year. But you know the saying, beggars can’t be choosers.

For those who missed it, in Part I of the Lendlease REIT IPO review I shared my love for Lendlease REIT, and why I thought it’s a pretty good deal (this article assumes you already know the basics of Lendlease REIT, so do check it out if you haven’t already).

But I was pretty surprised by the amount of negative feedback I received on Lendlease REIT.

So in Part II of this article, I’ll be sharing my responses to some of the common criticism, and why I’m still going ahead to subscribe.

Basics: Common Criticism of Lendlease REIT IPO

The criticism can be split into a few key points:

- IPO portfolio is concentrated

- IPO assets are low quality and does not include Parkway Parade

- Likely to be capital raising soon after IPO

1. Portfolio is concentrated

The argument goes like this. The IPO portfolio consists of two assets, 313@Somerset in Singapore, and Sky Complex in Italy. This is a concentrated portfolio that I don’t like, because there is a lack of diversification.

And I have to admit, of the three points above, this is the only argument that I don’t really get.

As a REIT investor, why do we care if the REIT is diversified or not? After all, the REIT only forms 1 component of my broader REIT portfolio.

In fact, the more concentrated the REIT, the happier I am, because it allows me to more easily achieve diversification across my portfolio.

To illustrate, if I think Lendlease Global Commercial REIT is too concentrated in Singapore and Italy, I can just go out there and buy Mapletree Logistics Trust, and get broad exposure to Asian logistics facilities. Or Mapletree North Asia Trust, to get exposure to Hong Kong and Japanese commercial properties. But you get the idea.

The way I see it, the fact that the portfolio is relatively concentrated, is not necessarily a bad point. What matters more is the quality of the properties that I am buying.

2. IPO assets are low quality – Does not include Parkway Parade

Which bring me to the next argument – That the IPO assets are low quality; they’re not a Vivocity or Parkway Parade.

And I actually get this argument.

313@Somerset

313@Somerset is probably not the best shopping mall in the world. In the world of shopping mall rankings, you have Vivocity and Parkway Parade and maybe Plaza Singapura right up there at the top (Tier 1 Malls), and then you have the okay malls like Bedok Mall and Suntec in Tier 2, and finally you have the never touching these malls in Tier 3 that I shall not name out of respect.

313@Somerset probably doesn’t belong in Tier 1, but it’s a very comfortable Tier 2.

Tenants wise, the F&B seems to be doing well (both the food court on the top floor and the shops in the basement) but the retail stores are a bit more of a question mark.

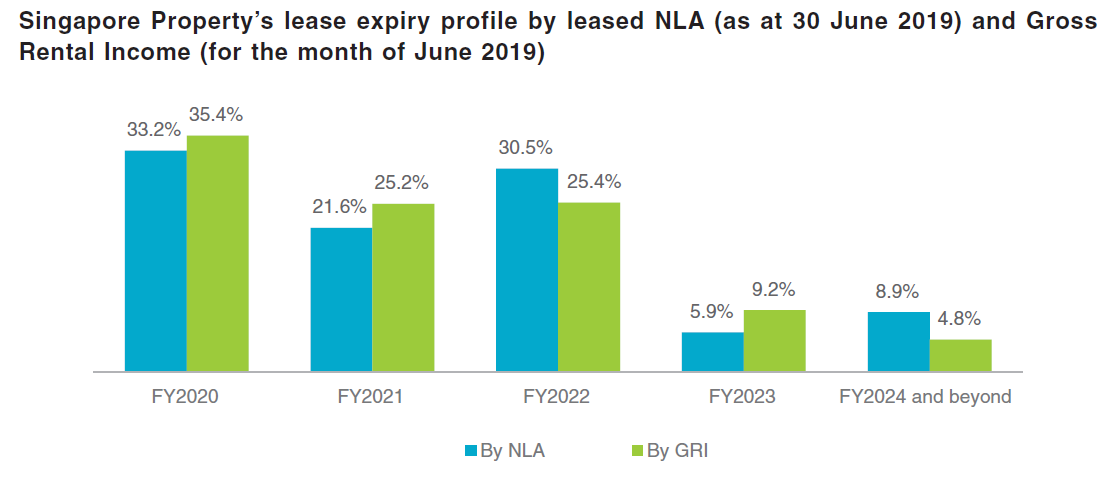

The lease expiry profile shows a huge chunk of leases are up for renewal in FY2020, which exposes Lendlease Global REIT to the retail environment at a time when consumer sentiment is weakening quickly.

But then again, these points hold true for just about every retail REIT out there today. Just about every shopping mall is facing the same challenges from eCommerce, slowing economy, experiential retail etc.

So there’s no denying that 313@Somerset is no Vivocity or Parkway. And if it were, this thing would be IPO-ing at a sub 5% yield. But you can’t have your cake and eat it. With Lendlease Global REIT tou get slightly less awesome properties, but a higher yield in exchange. That’s alright in my books.

Sky Complex

I’m quite puzzled as to where all the negativity over Sky Complex is coming from. It looks like a perfectly good office building located near the airport and transportation networks, and decently near Milan city.

It’s also locked into a 12 + 12 year lease with Sky Italia, which is an Italian Satellite TV provider owned by Sky (itself owned by Comcast). They’re a big player in Europe, so I don’t see any issues with this tenant in the near future. It’s not like the property is master leased to WeWork or anything.

The lease also has a built in rental escalation pegged to the inflation index, which is always nice to have.

The icing on the cake is that the European exposure allows Lendlease REIT to borrow in euros, which is just fantastic given where euro yields are trading at the moment (German yields are negative). Sure, it may be hard to borrow money to fund new acquisitions going forward, but with a REIT of this size, any future acquisition always needs to be funded via equity anyway, so I don’t see this as a big issue.

Valuations

Another blogger did a nice compilation of valuations below. I still think that the closest comparison to Lendlease REIT is SPH REIT and their Paragon property, so in this aspect Lendlease REIT is far superior in many ways, from WALE to weighted debt maturity to P/B and yield.

The Sky Complex property really adds some stability to the REIT, with it’s long term lease helping to smooth out the volatility that comes with a shopping mall.

| Metric | Lendlease | Starhill | SPH | CMT |

| Properties | 2 | 10 | 4 | 16 |

| Port. Value | S$1,403m | S$3,065m | S$3,566m | S$10,263m |

| Occupancy | 99.9% | 99.4% | 99.0% | 98.3% |

| WALE (GRI) | 4.9 yrs | 5.4 yrs | 2+ yrs | 2.2 yrs |

| Gearing | 36.4% | 36.1% | 30.1% | 34.2% |

| WA Debt Maturity | 3.8 yrs | 2.8 yrs | 1.8 yrs | 4.9 yrs |

| Market Cap | S$1,028m | S$1,636m | S$2,855m | S$9,664m |

| P/B | 1.08 | 0.86 | 1.17 | 1.28 |

| Yield | 5.8% | 6.0% | 5.0% | 4.47% |

Likely to be capital raising after Lendlease REIT IPO

The last criticism is the one I agree with the most. And it goes like this. With a REIT of this size, Lendlease REIT will likely do an acquisition post listing. This will need to be funded via equity from unitholders, so I may need to put more money into Lendlease REIT even before I get some back.

I get this. I too, think that there will likely be a big equity fund raising eventually, to acquire a new pipeline asset.

But the key to me, is what asset that will be, and at what price.

I’ve extracted Lendlease REIT’s investment mandate and pipeline below (emphasis mine):

Lendlease Global REIT is a Singapore real estate investment trust (“REIT”), established with the principal investment strategy of investing, directly or indirectly, in a diversified portfolio of stabilised income-producing real estate assets located globally, which are used primarily for retail and/or office purposes, as well as real estate-related assets in connection with the foregoing.

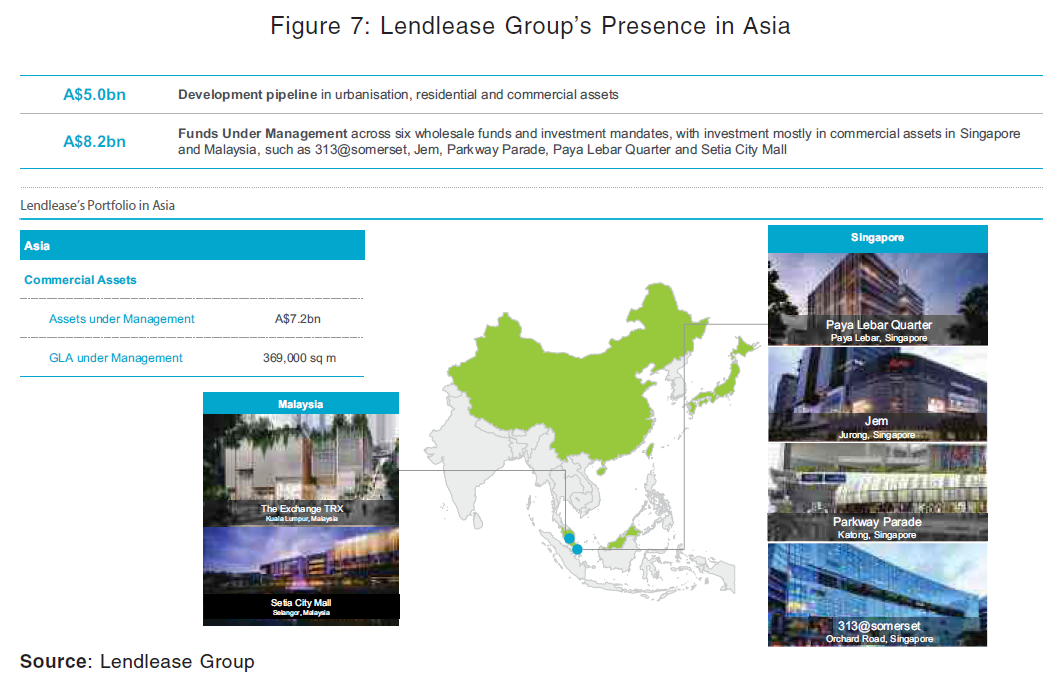

The Lendlease Group has a portfolio of 21 urbanisation projects across 10 Gateway Cities, some of which include: Barangaroo South (Sydney, Australia), Melbourne Quarter (Melbourne, Australia), Paya Lebar Quarter (Singapore), The Exchange TRX (Kuala Lumpur, Malaysia) and Milano Santa Giulia (Milan, Italy). In July 2019, the Lendlease Group secured a project to develop three mixed-use communities in the San Francisco Bay Area in conjunction with Google. The predominantly residential led scheme, with an end value of approximately A$20 billion, will deliver more than 15,000 new homes over a 10-15 year timeframe.

Because this is Lendlease, and because this REIT has a global mandate in retail / office assets, that’s a lot of very interesting assets that can go in. Parkway Parade, Jem, and Paya Lebar Quarter in Singapore are the big ones that I have my eye on.

So in the longer term, what will make or break Lendlease REIT is how Lendlease views this REIT.

Are they in for the long term with unitholders, and plan to slowly divest key assets into the REIT to build this into the next Mapletree Commercial Trust? Or are they going to use Lendlease REIT as an easy way to exit mature asset at premium valuations.

If it’s the former and they inject Parkway Parade or Paya Lebar Quarter at a 4.5% capitalisation rate, hell yeah would I be pleased. But of course, if it’s the latter and they’re injecting lousy assets at expensive prices, I’m out of here the next chance I get.

Unfortunately, because this is Lendlease’s first REIT globally, we actually don’t know the answer to that. But that’s where the fun is in investing right? If we knew everything all the time, what fun would that be?

Personally though, I’m willing to take a chance on this. Worst case if Lendlease turns out to be a bad sponsor, I’ll just take my 5% to 6% yield a year and find an opportunity to exit down the road. If they turn out to be a good sponsor, then there’s a long and fulfilling journey ahead of this REIT, and one that I’m looking forward to be a part of.

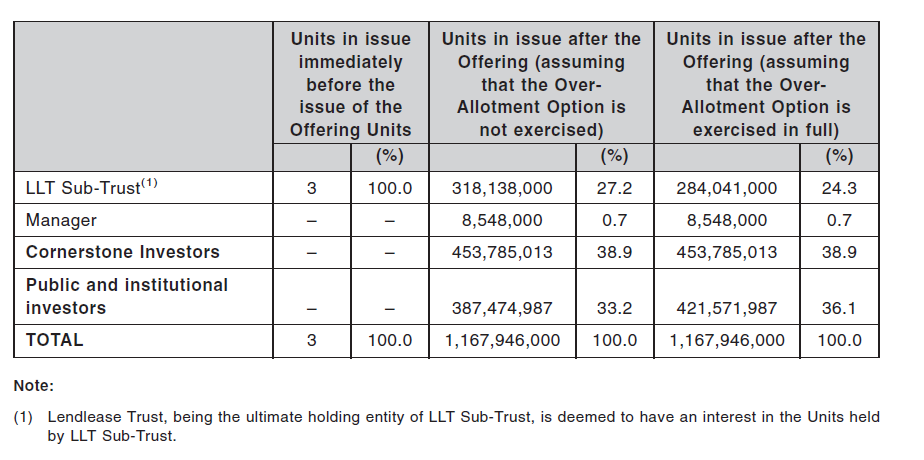

If it’s any help, Lendlease is going to be holding about 24 to 27% of Lendlease Global REIT post listing, similar to the CapitaLand / Mapletree models, so perhaps that’s a nice sign that they’re in for the long term.

Public offer is tiny

I also just wanted to point out how small the public tranche for Lendlease REIT IPO is. The public tranche is 22,727,000 units out of 387,474,987, which works out to about $20 million, or 5.8% of the final offer.

As a rough ballpark, we usually see issuers come to IPO with a public offer of around 10% of the total offer, so this is way below that. Probably the negative sentiment from the past few IPOs (*cough* Eagle Hospitality Trust) has made them particularly nervous.

Because of this, and because the valuations are pretty decent, and because of the ridiculous list of cornerstone investors (Blackrock, Fullerton, Segantii etc), I think that public demand at IPO will probably be quite hot. There’s just not going to be enough units to go around.

In the short term at least, this should provide a support for the price, so it’s unlikely there will be a huge drop in price unlike some other REITs…

Closing Thoughts

I’ve spent the past week mulling over Lendlease Global REIT, and my conclusion is that I actually really like it.

I think the closest equivalent to Lendlease Global REIT today will be SPH REIT, because 313@Somerset is very close to Paragon in terms of location and yields.

And in this aspect, Lendlease Global REIT is far superior. With Lendlease Global REIT, (1) you are buying in at a much higher yield (5.8% vs 5.0%), (2) you also get Sky Complex which is a free cash flow generator and stabilizes the portfolio, and (3) you get access to Lendlease’s global pipeline.

I can’t stress point 3 enough. When you buy SPH REIT you get access to SPH’s pipeline, which doesn’t count for much given that they’re a newspaper company and not a property developer (okay, I know that’s debatable these days). But the point is, with SPH REIT, future growth will come from assets outside the SPH group, stuff like Rail Mall.

With Lendlease Global REIT, given that this is their first REIT globally, and the REIT has a mandate to invest in global retail and commercial assets, that’s actually a massive pipeline for Lendlease REIT to draw on for future growth. And all we need is for Lendlease REIT to acquire one or two quality assets, and this could suddenly become a very attractive REIT. Of course, we won’t know whether Lendlease will be a responsible sponsor along the likes of Mapletree, so there’s some uncertainty there, but that’s a bet I’m willing to take. I’ll be waiting patiently until the next acquisition, for some signs as to the REIT’s strategy going forward.

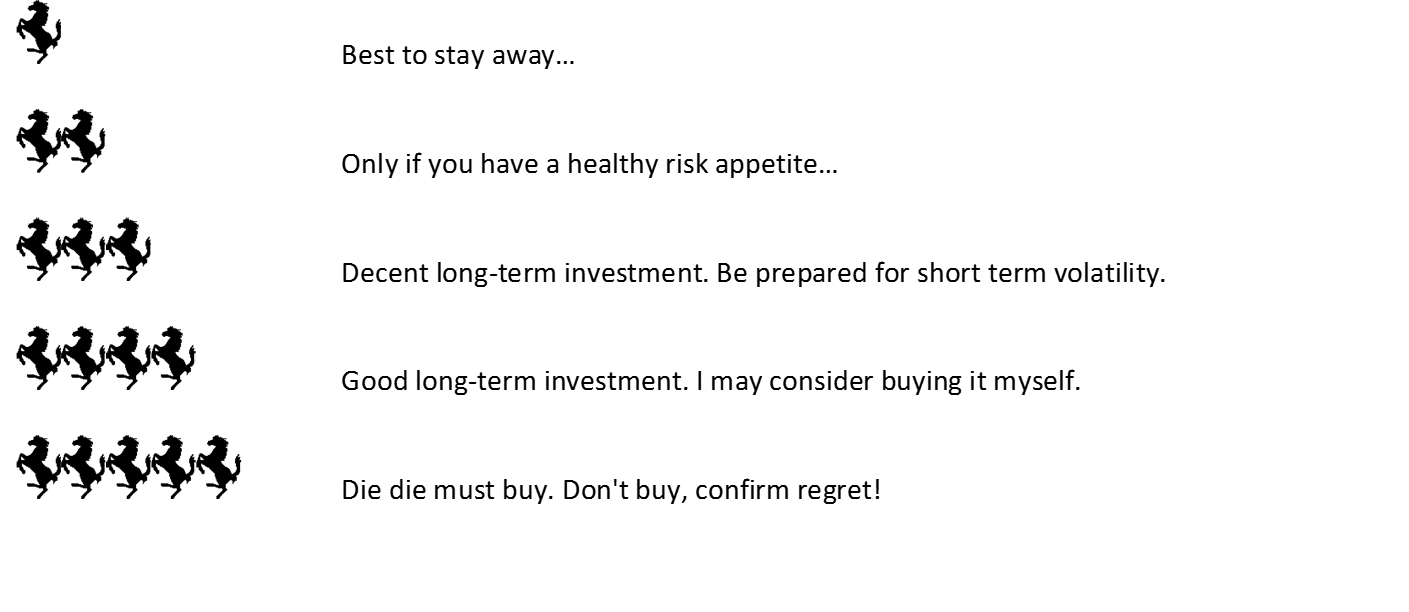

I’m giving Lendlease Global REIT a 4 Financial Horse Rating, and just to show I’m putting my money where my mouth is, I’ll pop $10,000 on this IPO. I think it’s going to be quite hot though, so I expect public allocations to be low, but I do hope to be pleasantly surprised.

Are you guys signing up for the Lendlease REIT IPO? Share your comments below!

Lendlease Global REIT – Financial Horse Rating

Looking for a comprehensive guide to investing? Check out the FH Complete Guide to Investing for Singapore investors.

Support the site as a Patron and get market and stock watch updates. Big shoutout to all Patrons for their support!

Like the Financial Horse Facebook Page and join the Facebook Group (Singapore) or Facebook Group (China) to continue the discussion!

Hello,

IPO price drops usually after listing. What are your thoughts of waiting for awhile to see the actual valuation of the price?

Because the public tranche is so small, I would be surprised if it drops much post-IPO, simply because of the lack of liquidity. If anything, price may go up as those who couldn’t get it at IPO will buy in. I could be wrong though.. we shall see 😉

People are highlighting that kep reit ex ceo and ex cto are in this reit and their past records are horrible where where they dump asset in at premium price while dilute DPU. Any view on this?

I would be more concerned about the Sponsor, rather than the REIT manager. Practically speaking, if the Sponsor wants to be nasty and inject a horrible asset into the REIT, there’s only so much the REIT manager can do.

[…] Lendlease Global REIT IPO – Why I’m subscribing for this IPO from Financial Horse […]