After Lendlease REIT, the most requested REIT from you guys has been Mapletree Pan Asia Commercial Trust.

I’ve done a couple of pieces on MPACT for Patrons on this past.

But given the recent plunge in price I figured let’s do an updated deep dive.

Mapletree Pan Asia Commercial Trust’s share price has collapsed

Whatever way you cut it – the charts are not pretty.

This is the 10 year chart of Mapletree Pan Asia Commercial Trust.

At current price of $1.36, this Mapletree REIT is down:

- 38% from the post-COVID high of $2.2

- 44% from pre-COVID high of $2.45

Pretty unbelievable numbers, for what was once the premier Singapore commercial REIT.

The last time Mapletree Pan Asia Commercial Trust was this low?

It was back in 2017 during the previous rate hike cycle (still remember that?).

Before the merger with Mapletree Greater China Commercial Trust that changed everything.

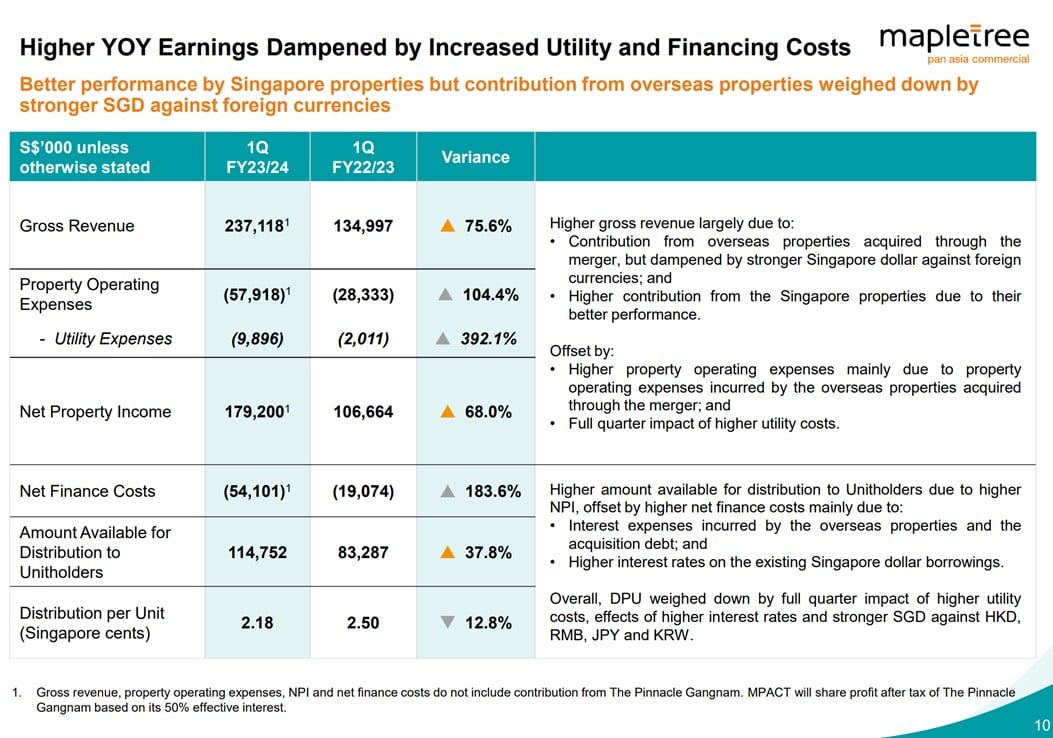

Dividend Yield of Mapletree Pan Asia Commercial Trust

Latest DPU is down a whopping 12.8% from a year ago.

Official reason is due to:

- Higher utility costs (inflation)

- Higher interest expenses

- Strong SGD impacting foreign earnings (HKD, RMB, JPY, KRW)

For what it’s worth, points 1 – 3 should impact other REITs like Ascendas REIT and CICT equally.

But you see flattish DPU in those REIT.

So the 12.8% drop in DPU for Mapletree Pan Asia Commercial Trust is big – greater even than Lendlease REIT.

Annualising the 2.18 cents quarterly dividend.

Works out to a 6.4% dividend yield at current price.

Price to Book of Mapletree Pan Asia Commercial Trust

NAV is $1.75.

So at current price this REIT trades at 0.77x book value.

So why does Mapletree Pan Asia Commercial Trust keep dropping?

Let’s deal with the elephant in the room.

Why does Mapletree Pan Asia Commercial Trust keep dropping?

The way I see it, it comes down to 2 reasons:

- Hong Kong/China Exposure

- Soaring long term interest rates

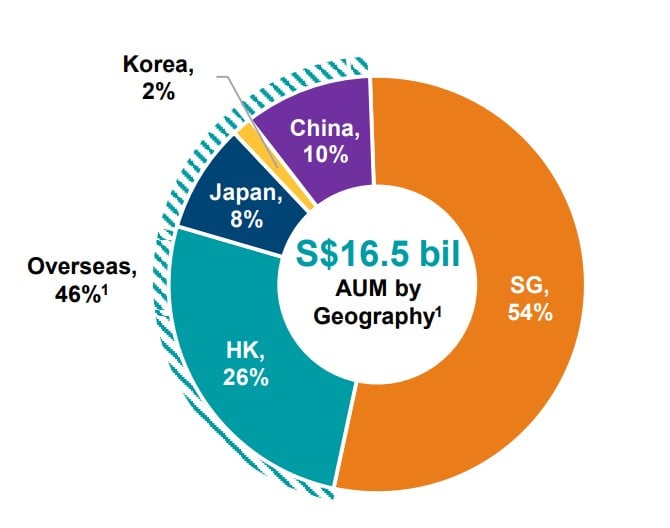

Hong Kong/China Exposure

After the merger with Mapletree Greater China Commercial Trust.

26% of this REIT is now Hong Kong properties, and another 10% is China.

That means 36% exposure to China/Hong Kong.

And in case you missed the memo, the market doesn’t want to touch anything China/Hong Kong related these days.

Here’s link REIT – the largest REIT in Asia.

Down an unbelievable 62% from its high pre-COVID.

If even a behemoth like Link REIT is in trouble, you wouldn’t expect Mapletree Pan Asia Commercial Trust to fare much better.

You can see the relative performance of MPACT vs CICT.

Since the start of 2021, CICT (orange) is only down 21%, while MPACT (candles) is down 36%.

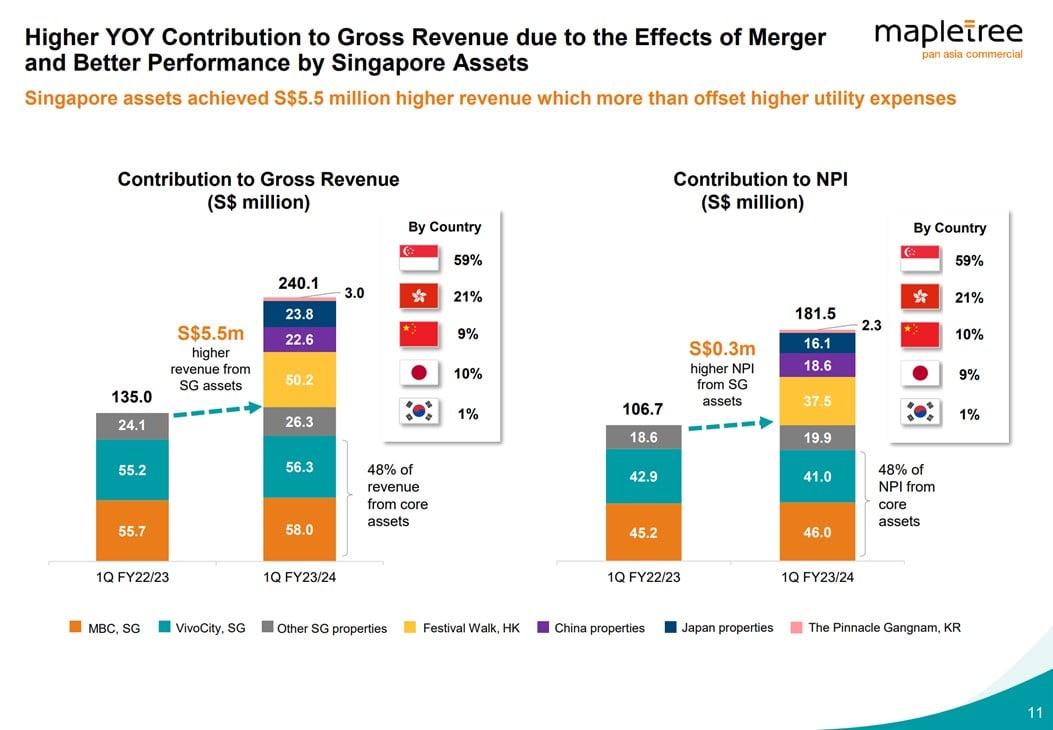

Mapletree Pan Asia Commercial Trust’s Earnings confirms this narrative

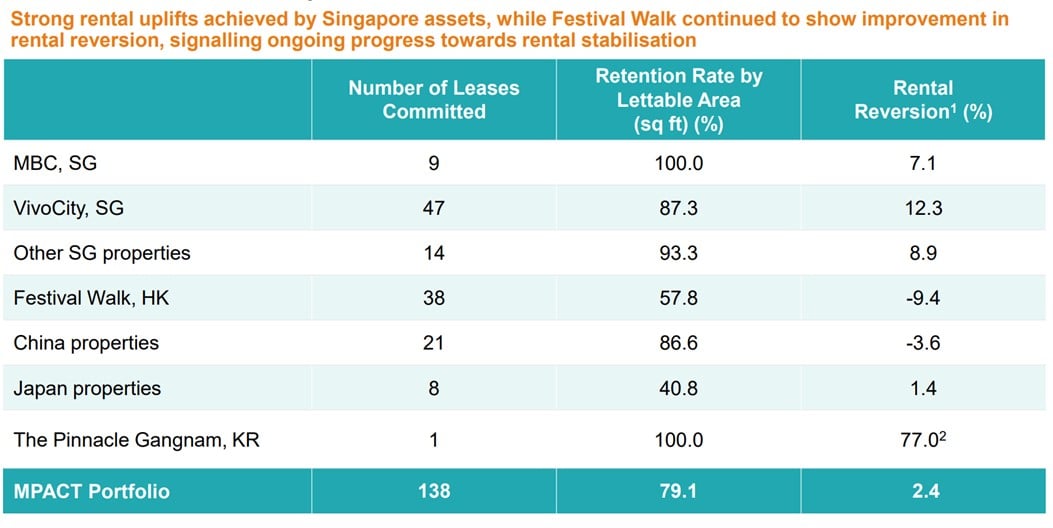

The rental reversions provide further colour.

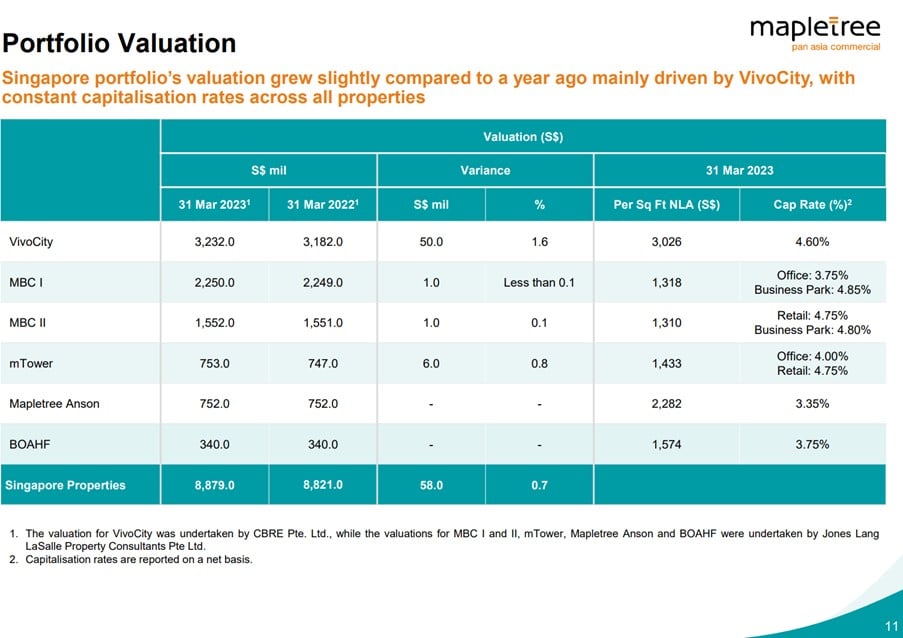

We see pretty strong performance across the board for the Singapore properties.

7% rental reversion for Mapletree Business City, 12.3% rental reversion for Vivocity.

Very solid numbers.

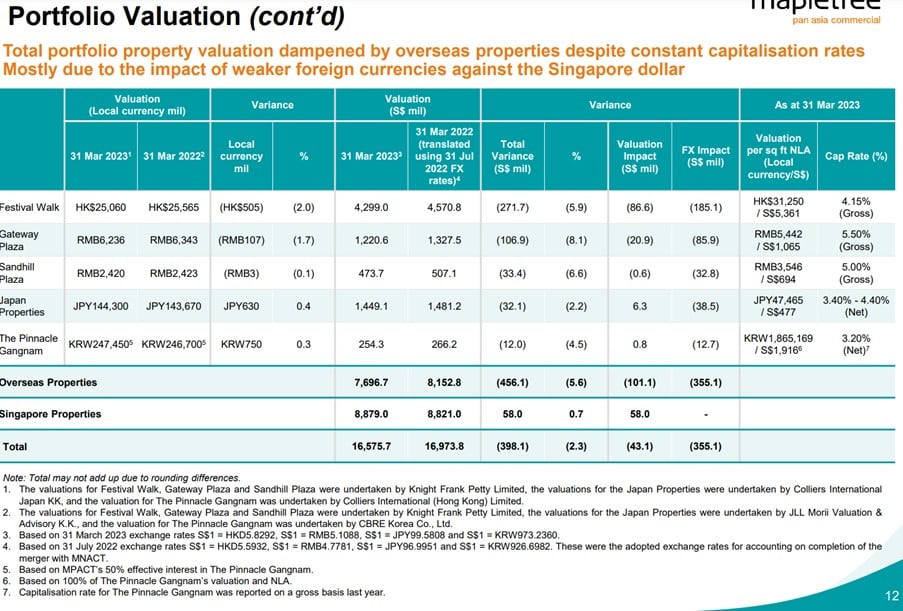

But the Hong Kong Festival Walk is pulling -9.4%, and China is doing -3.6%.

Given that this is 36% of Mapletree Pan Asia Commercial Trust’s asset base – that is a huge drag.

The Singapore portfolio is doing very well, but being dragged down by the Hong Kong/China portfolio.

Where is the bottom for China/Hong Kong?

I’ve shared my views on the China real estate situation generally in a previous article.

The problems that Xi faces go back decades – years of excessive leverage and reliance on real estate growth.

These problems were in place even during (and arguably perpetrated by) predecessors Jiang Zemin and Hu Jintao.

Now there’s only 2 ways to solve a real estate bubble – quickly, or slowly.

Quickly…

A lot of western commentators are seeing this like 2008.

They expect a singular big bang moment for China where it all comes crumbling down – followed by massive stimulus (basically what the US did in 2008).

But I think that misunderstands the centrally planned nature of China – where nothing happens unless it’s allowed to happen.

Or slowly…

So I don’t see a Lehman moment for China.

But the underlying problems from misallocation of resources and reliance on real estate remain.

Rather, I would expect China to go through a few years of slow economic growth + deleveraging + pain for the real estate sector as they manage this transition to non-real estate growth.

Even if we have a short term bottom for China here, I think more pain will come the next few years.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great charts & insights on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

Interest rate march upwards – bad for REITs

The second point of course, has been discussed to death.

Higher interest rates.

MPACT was kind of unlucky too.

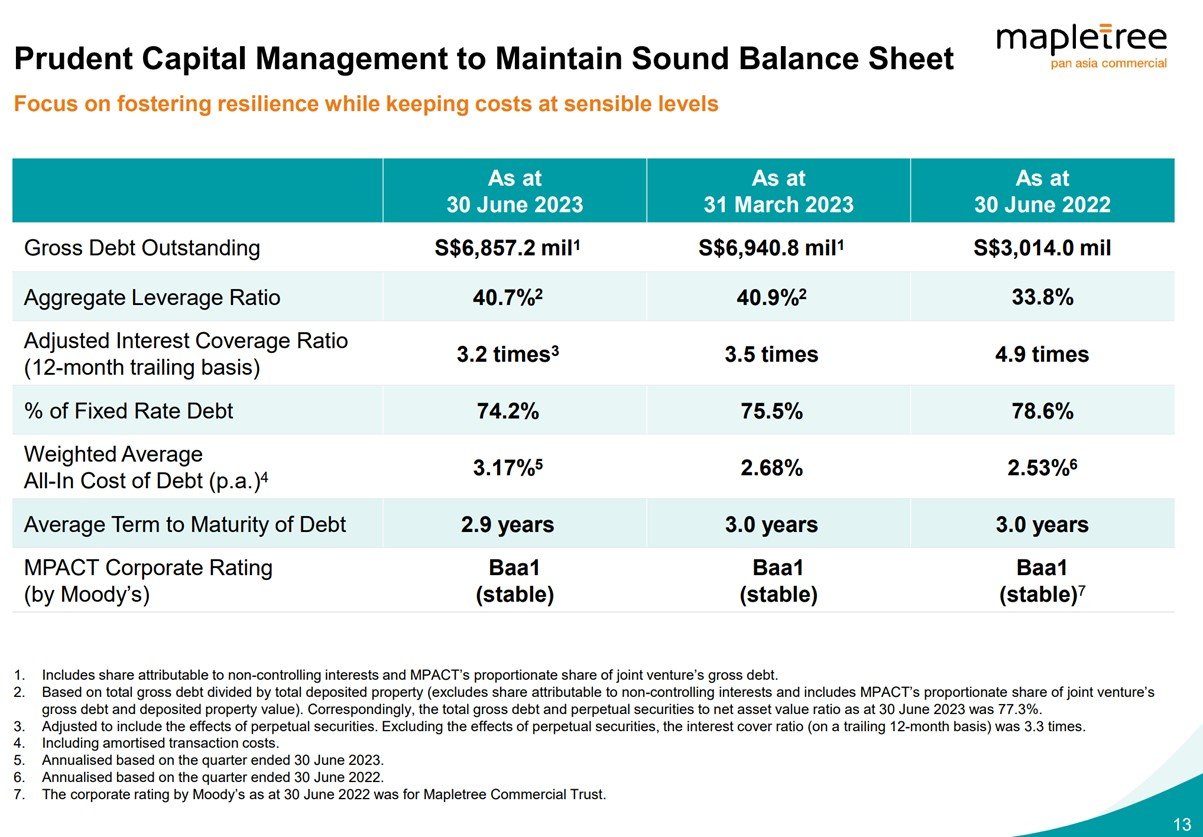

You can see how the REIT was running a very conservative 33.8% gearing ratio in June 2022.

Then they geared up to 40.9% gearing ratio by March 2023 to fund the acquisition of Mapletree Greater China Commercial Trust – right smack into soaring interest rates.

Life is funny like that.

Long Term interest rates are breaking out of cycle highs

I don’t know who needs to hear this – but long term interest rates have made a huge move the past few months.

The Singapore 10 year yield at 3.5% is at cycle high, and at levels last hit in 2008!

Whereas the US 10 year yield has broken out beyond cycle highs – to levels last hit in 2007!

US 10 Year Treasuries are regarded as pristine collateral around the world – and the US 10-year yield sets the benchmark for global asset pricing and lending rates.

A move like that – it’s almost guaranteed to break things.

And we will see the full impacts in the months/quarters to come.

That’s a big reason for the sell-off in REITs generally of late, although to be fair this point will impact all REITs equally and not just Mapletree Pan Asia Commercial Trust.

What is a fair valuation of Mapletree Pan Asia Commercial Trust?

Doom and gloom aside.

Let’s try to determine the fair valuation for Mapletree Pan Asia Commercial Trust.

Given the drop in DPU, dividend growth valuation is not so appropriate, so we’ll do a sum of the parts analysis.

MPACT is basically made up of 3 parts:

- 26% Hong Kong

- 54% Singapore

- 20% China/Japan

Let’s try to assign a fair value to each portion.

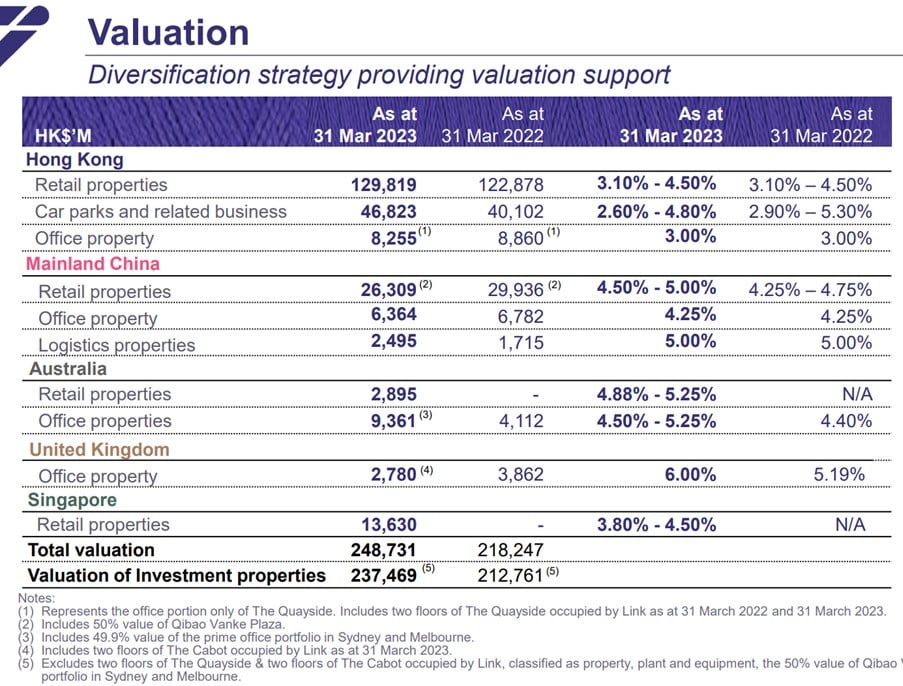

Hong Kong Properties (26% AUM)

If you compare with Link REIT, which is the Hong Kong retail REIT behemoth ($20 billion market cap).

You’ll find that Link REIT trades at a 0.5x book value.

Festival Walk is valued by MPACT using a 4.15% cap rate, which is in line with Link REIT.

So let’s use a 0.5x book value for the Hong Kong portion.

Singapore Properties (54% AUM)

CICT is the retail and office behemoth which trades at 0.86x book value.

While Frasers Centrepoint Trust trades at 0.93x book value (suburban retail).

If you ask me, I think MPACT’s Singapore portfolio (Vivo and Mapletree Business City) are stronger than FCT or CICT’s portfolio.

But let’s be very conservative here, and apply a 0.9x book value for the Singapore properties.

After all, you’re looking at a cap rate of:

- 4.60% for Vivo

- 4.80% for MBC

- 3.5% for Office

Dock about 10% off that and it’s probably fair value range, especially given that MPACT’s Singapore portfolio is best in class.

China/Japan Properties (20% of AUM)

And the rest of the China/Japan properties, let’s use 0.56x for China (in line with CapitaLand China Trust), and 1.0x for Japan.

This gives us roughly 0.78x blended book value for this portion.

Sum of the parts fair valuation of Mapletree Pan Asia Commercial Trust?

Blend all of the above, and that gives us a fair value of 0.77x book value.

With a NAV of 1.75, that implies a fair value of $1.35.

My numbers above are quite conservative, and it shows MPACT at fair value today (1.36).

That is interesting.

But of course, valuations don’t provide a clue on timing, and cheap can get cheaper.

For more clues on timing, let’s look at technical analysis.

Is Mapletree Pan Asia Commercial Trust a falling knife? Technical Analysis?

Technical analysis doesn’t look pretty.

$1.5 was a key support level that has broken recently, after which prices quickly plunged.

The next support is at $1.35, which ties in with my fair valuation above.

So it will be key to watch if $1.35 holds.

If it breaks, the next level is 1.2, that those are levels last hit a decade ago.

Like I said – unbelievable stuff.

Will I buy Mapletree Pan Asia Commercial Trust?

Much like Lendlease REIT.

I think Mapletree Pan Asia Commercial Trust here, is very close to fair value range for the underlying real estate – even if you assume interest rates stay high for a while.

The problem of course, is trying to call the bottom.

A REIT that is cheap can continue to get cheaper, and you don’t make timing decisions based off of valuation.

Where is the bottom for this REIT?

Trying to call a bottom for MPACT is doubly hard because of the (a) China/HK exposure, and (b) soaring long term interest rates.

China/HK

The way I see it – China/HK’s real estate troubles will not bottom out for years, so that will be a big drag on share price going forward.

But that said, in my analysis above I’m already valuing the China/HK portion at 0.5x book value today.

Let’s say cycle bottom is 0.3x book – which implies a 70%+ peak to trough decline for China/HK real estate and is unbelievable numbers.

That implies a fair value of MPACT of $1.22.

So even a very horrendous valuation for China/HK isn’t that bad for MPACT.

Soaring Long Term Interest Rates

Where and when exactly interest rates top out – your guess is as good as mine.

But the fact that guys like Jamie Dimon are calling for 7% long term interest rates.

Suggests to me that we may be far more advanced in the cycle that you expect.

After all, when market participants expect that interest rates can only go up further – that’s probably close to the top right there.

So… Will I buy Mapletree Pan Asia Commercial Trust?

Full disclosure that I hold a position in Mapletree Pan Asia Commercial Trust.

Would I buy more here to average in?

Probably not yet.

At the very least, I would want to see the $1.35 level hold from a technical perspective, and some improvement on the long term interest rates before I buy, otherwise it’s just a falling knife.

That said, I absolutely do not deny that this is in fair value range, from a fundamentals perspective.

For investors who don’t use leverage and have holding power, I think these are attractive prices for a long term pick up.

And because of that, I can easily change my mind on a dime here and buy a position – if the technical and macro picture starts to stabilise in the coming days/weeks.

Sometimes, trying to time the bottom exactly is a fool’s errand, as long as you have holding power and the cash to buy in further if things head south.

That said, I think there are a lot of very interesting buys out there for individual REIT pickers, and we’re shaping up for a very interesting next few months in the macro world (just look at the moves in long term interest rates, FX and credit).

As always, Patreons will get updates as and when I buy (or sell) MPACT, or any other REIT generally.

The full list of REITs I am keen to buy, with approximate price targets, is also available on Patreon.

This article was written on 6 Oct 2023 and will not be updated going forward.

For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do sign up as a Patreon.

– Get up to USD 2000 worth of shares

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 2000 free fractional shares.

You just need to:

- Fund any amount

- Hold for 30 days

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Investment Research Tools

I use Trading View for my research and charts. Get $15 off via the FH affiliate link.

I also use Koyfin for fundamental and macro research. Get a 10% discount via the FH affiliate link.

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Best investment books to improve as an investor in 2023?

Check out my personal recommendations for a reading list here.

The content here is for informational purposes only and should NOT be taken as legal, business, tax, or investment advice. It does NOT constitute an offer or solicitation to purchase any investment or a recommendation to buy or sell a security. In fact, the content is not directed to any investor or potential investor and may not be used to evaluate or make any investment. Do note that this is not financial advice. If you are in doubt as to the action you should take, please consult your stock broker or financial advisor.

Hi FH,

Awesome analysis! Love this piece

Cheers

Thanks Mrs Pennies – appreciate the kind words!