Given that today is the last day of 2022…

I figured this would be as good a time as any to review the year.

And to review my 3 biggest investment mistakes in 2022.

So here goes!

Mistake No. 1 – Neglecting Counterparty Risk (FTX)

It’s ironic that in a year where the S&P500 is down 21%, my biggest investment loss comes from having invested in a ponzi scheme.

Although when you put it that way, I suppose it’s not ironic at all.

After all, it’s only when the market goes down that the ponzi schemes are uncovered right?

As a percentage of my overall portfolio the loss is not big because of position sizing.

But dollar value wise, this was probably the biggest investment loss of 2022.

So to say that this loss doesn’t hurt is not accurate too.

A decent chunk of my crypto and USD stablecoins were held on FTX, and realistically the chances of getting it back any time soon is incredibly slim.

What could I have done better?

Hindsight is 20/20.

But realistically, I think the first signs of trouble only started to emerge when CoinDesk reported a leaked balance sheet of Alameda Research on 2 Nov:

From then until 9 November when FTX halted all withdrawals – was almost exactly one week.

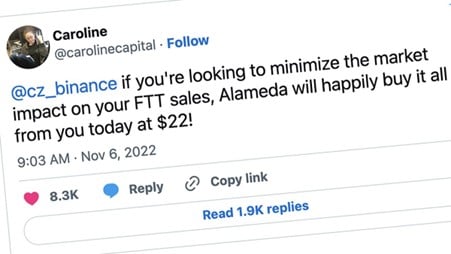

Although that being said, the real red flags only started coming when Binance’s CZ talked about selling down FTT, and when SBF and Caroline responded to him (6 – 7 November).

Remember this tweet from Alameda’s Caroline?

That was the point where your alarm bells should have gone off and you started pulling funds.

Which means realistically there was only a 2 day window to pull funds before it was gated.

Lesson Learned?

In hindsight of course, I should have pulled my funds quicker.

But all the talk about SBF being crypto’s golden boy, and investors that included Sequoia and Temasek, probably affected the timing of my decision.

I only started to pull funds on 9 November, literally right when redemption gates when up.

Lesson learned – in future, when it comes to counterparty risk, you want to panic first, and ask questions later.

Or as the quote from Nassim Taleb goes:

“If you must panic, panic early. Be scared when you can, not when you have to.”

Mistake No 2 – Playing it too cautious… Not having bigger conviction in my own macro thesis…

Long time readers of Financial Horse know that I’ve been bearish on the macro since late 2021 / early 2022.

I wrote many macro posts sharing my concern on inflation, and what the withdrawal of liquidity would do to financial assets.

In hindsight, I probably should have bet bigger on my own thesis.

What I did wrong in 2022?

What I did right in 2022, was to be in heavy cash, so I sat out a big part of the market decline.

What I did less right, was not to have greater conviction in my own thesis, and benefitted better from the macro shifts.

For example there were many trades like shorting long bonds (eg. TLT), put options on FAANG that had asymmetric risk-reward profiles.

Those allowed you to risk a small amount of capital, for potentially a big pay-off if you are right.

Lesson Learned?

As a macro investor – you want to move in size when you have conviction.

Knowing how to size a trade is almost as important as knowing what trades to make.

You want to size it big enough so that if you are right, you have a significant payout.

But you don’t want to size it so big that if you are wrong, you are carted out.

It’s a fine balance, and one that I probably didn’t do well in 2022.

I probably played my cards a bit too cautious this year.

Yes I did well by going heavy cash.

But I probably could have benefitted a lot more from the market decline.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Mistake No. 3 – Sweating the small stuff, neglecting the bigger picture (80-20 rule)

I’m a big believer in the 80-20 rule.

In investing, like in life, you want to focus your efforts on the 20% of the stuff, that drives 80% of the outcomes.

What I did wrong in 2022?

You guys know what I mean.

Sweating over bidding 4.3% on a T-Bill vs 4.25%.

Choosing between FD at 4.2%, or T-Bills at 4.28%.

Stuff like that.

As humans, we only have 24 hours a day.

Take out 8 hours for sleep, and you’re only left with 16 hours a day.

Spend too much time sweating the small stuff, and you don’t leave enough time to focus on the big stuff.

So…

Instead of spending time worrying about what exact yield to bid on the T-Bill.

Worry about how much money you should be holding in T-Bills vs REITs.

Instead of worrying about whether to sell DBS at $33 or $33.5.

Worry about how much DBS you should sell (if at all) and where the money should go instead.

Instead of worrying about where interest rates will go in 2023.

Worry about what you can control – how your portfolio will perform if interest rates stay high, or stay low.

Lesson Learned?

This is tied in some ways to Mistake No. 2 above.

When you identify a big macro trend, you want to move fast.

You don’t want to spend too much time obsessing over the details.

You want to move first, and ask questions later.

As long as the trade is (1) easy to unwind, and (2) does not involve betting the house, you almost always want to move first, and worry later.

I’ve been guilty of moving too slow in the past, and I probably made that mistake in 2022 again.

What I did well in 2022 (as a Singapore Investor)?

In hindsight, the asset classes that did well for me in 2022 are:

- Energy (Oil)

- Singapore Banks

- Residential real estate

- Cash

Energy (Oil)

I accumulated fairly large positions in oil stocks in 2020, and I added to them in 2021 and 2022.

Those have done amazingly well for me, and have grown to a significant part of my portfolio today.

The big question of course, is when to sell (I have not sold any oil positions since 2020).

I like the mid term outlook for oil because of structural demand-supply imbalance.

And yet if we are going into a 2023 recession, oil may not necessarily be a position I want to be holding in size.

You already see that from all the hedge funds whipping out the 2008 playbook and shorting oil.

This will be a tricky one in 2023.

The path of oil going forward will determine the path of inflation, and the path of the rate hikes.

In any case I share weekly updates on my macro views and portfolio moves on Patreon. Do sign up if you are keen.

Singapore Banks

Much like oil, I accumulated these positions in 2020, and many of them have doubled (or close to).

Unlike oil though, I’ve started to take profit in the Singapore bank positions, and to rotate the cash elsewhere.

Risk-reward does not make sense to me at these prices.

Whether this is the right or wrong call, only time will tell.

Residential real estate

Regular readers of FH will know that I bought residential real estate in 2021.

I expected the coming wave of inflation to raise asset prices (especially residential real estate), and locking in a mortgage at zero bound interest rates to buy assets would be a great way to play it.

Back then, I probably didn’t expect the Ukraine war to happen, nor did I expect interest rates to shoot up this much this fast. Nor did I expect such a marked mismatch between supply and demand for residential real estate.

But for now at least, the general thesis of inflation seems to have played out, as the market value of the 2021 property I bought has risen decently.

Whether this will continue (or reverse) in 2023… let’s see.

With new supply coming online and interest rates at 4%+, can residential real estate stay at these prices?

Cash

I increased cash allocations a fair bit in late 2021 and early 2022.

Sure, I’m probably on low single digit returns on cash.

But in a year where the S&P500 is down 21%, not losing money is probably already a win.

Although as shared above, I probably should have done better to bet on the macro trends identified.

Looking forward to 2023?

2023 looks to be an action packed year.

If 2022 is the year of inflation worries and multiples compression (due to rising interest rates).

2023 is going to be the year of recession worries and earnings declines.

You’ll see the conversation shift away from inflation, into recession.

New year, new start

Whatever the case… on 1 January 2023, all performance counters are going to be reset.

So whatever mistake you made in 2022, it’s time to put that behind you, and move on.

Because 2023 is a new year, with new money to be made, and new mistakes to be made.

Ready or not, here we go!

Happy 2023 to all readers!

For regular updates on my portfolio positioning, and my Stock / REIT watchlist, do sign up as a Patreon.

I provide weekly updates on macro commentary, and portfolio movements there.

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

WeBull Account – Free USD150 ($212) cash voucher

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with a free USD 150 (S$212) cash voucher.

You just need to:

- Sign up here and fund S$2000

- Make 1 US Stock or ETF trade (you get USD100)

- Make 1 Options trade (you get USD50)

1080-1080-002-1024x1024.jpg)

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

I misjudged “political risks”. Marc Twan once said, it is not the things you don’t know which kill you, but the things you know which ain’t so.

Invest in Russian stocks? Russians always sticked to the rules and I had no trust worries. It was the US, who stole the stocks right out of my account. The Russians offered something like an C-account, but one needs to travel to Moskow for that because of Russian money laundering laws (are they kidding me?). I have a 100% loss and launder what exactly? To add sunken costs was a no no.

Lesson: I avoid western stocks and will not invest anymore “over orders”. So any REIT should be a pure Singapore one.

Thanks – appreciate the honest sharing very much.

I think this was the year that geopolitical risk really hit home for me as well.

Mistake 1 talks about not pulling out fast enough. The better question is whether it should be there in FTX custody in the first place. There is a reason why DBS can charge 1% crypto trading fees and 0.5% annual crypto custody fees.

Fair point.