After my recent article on how to generate $50,000 dividend income a year.

There were a lot of questions on OCBC, and how it compared to DBS and UOB.

A lot of retail investors also seem to think that OCBC is “cheaper” than DBS and UOB, and therefore a better buy.

So I decided to do a deeper dive into OCBC, and find out if this is indeed true.

Valuations of OCBC vs DBS and UOB (as at 11 October 2023)

First off – High level valuations of OCBC bank vs DBS and UOB below.

You can see how DBS is:

- The biggest of the 3 banks

- Trades at the highest valuation (highest price to book at 1.49x).

Whereas OCBC is in between DBS/UOB in terms of market cap and Price/Book.

|

|

OCBC |

DBS |

UOB |

|

Market Cap ($ billion) |

58.4 |

87.6 |

47.7 |

|

Price/Book |

1.10 |

1.49 |

1.05 |

|

Dividend Yield (annualising latest yields) |

6.15% |

5.68% |

6.01% |

OCBC Bank pays a 6.15% dividend yield – Highest of the 3 local banks

OCBC just raised their dividend this year due to stronger earnings.

If you assume the 40 cents dividend will stay, you’re looking at a 6.15% dividend yield for OCBC.

This is the highest of the 3 local banks.

But… note that banks are cyclical stocks, the dividend can get cut

A note of caution though – bank dividends are never really set in stone because it is tied back to their earnings.

The 3 local banks target to pay out around 50% of their earnings.

So when times are good, like right now, the dividend is very juicy.

When times are not so good, then the dividend drops.

And when things get really bad (like COVID in 2020), the regulators (MAS) may even cap the amount of dividends that can be paid out.

Banks are as cyclical as it gets – you do not want to extrapolate the 6.15% dividend yield into infinity.

So dividend investors in bank stocks should take note of this.

This isn’t like a REIT where they have to pay out 90% of their taxable income.

Operational Metrics of OCBC vs DBS and UOB

Diving deeper into the operational metrics.

DBS has the best performance:

- Return on Equity (ROE) of 17%

- Quarterly revenue growth of 37% year on year

Viewed this way, you can kind of understand why DBS trades at such a premium to book value – it’s just a better company based off these numbers.

|

|

OCBC |

DBS |

UOB |

|

Quarterly revenue growth (yoy) |

27.7% |

37.1% |

23.8% |

|

Return on Equity (ttm) |

12.8% |

17.0% |

12.4% |

|

Non-Performing Loans |

1.1% |

1.1% |

1.6% |

OCBC’s operational metrics are again in the middle of the pack, in line with its valuations (slightly higher than UOB, but much lower than DBS).

OCBC Loan Exposure – A lot of China exposure?

A lot of retail investors choose to stay away from OCBC because they think that OCBC Bank has a lot of exposure to China.

The background here is that OCBC bought over Hong Kong’s Wing Hang bank in 2014 for $6.23 billion.

Taking on Wing Hang’s loan book and business, you would expect a lot of Hong Kong and Mainland China exposure to come with it.

Looking at OCBC’s latest loan book:

- 24.5% of the loan book is Greater China.

- Of that – 49% is Hong Kong, and 46% is Mainland China credit risk.

But… DBS has 29% exposure to Greater China

Interestingly – DBS actually has even higher exposure to Greater China, at 29% of their loan book.

|

Loan Book |

OCBC |

DBS |

UOB |

|

Singapore |

41% |

46% |

48% |

|

Greater China |

25% |

29% |

17% |

|

South East Asia |

14% |

8% |

21% |

|

Rest of World |

20% |

17% |

14% |

But… different quality of China loan book for OCBC?

I know what you’re going to say though.

That DBS’s China exposure is more from Singapore companies (especially Temasek linked) operating in China, so it’s not really “real” China exposure.

While OCBC’s China exposure comes from Wing Hang Bank, which means this is “real” China exposure.

If you look at the FX exposure it does support this theory.

DBS’s Mainland China (China ex Hong Kong) loan book is $52 billion, and yet there is only $18 billion RMB exposure.

Indicates a good part of DBS’s Mainland China exposure is USD / offshore loans.

So… Which bank has the riskiest loan book?

|

Loan Book |

OCBC |

DBS |

UOB |

|

Singapore |

41% |

46% |

48% |

|

Greater China |

25% |

29% |

17% |

|

South East Asia |

14% |

8% |

21% |

|

Rest of World |

20% |

17% |

14% |

Coming back to the table, it’s fairly clear that each of the 3 banks has slightly different exposure.

Both OCBC and DBS have big exposure to Greater China, but it’s probably fair to say that DBS’s China exposure is more tilted towards the Singapore (esp Temasek Linked) companies, and of a higher quality than OCBC’s.

Whereas UOB has the highest exposure to South East Asia.

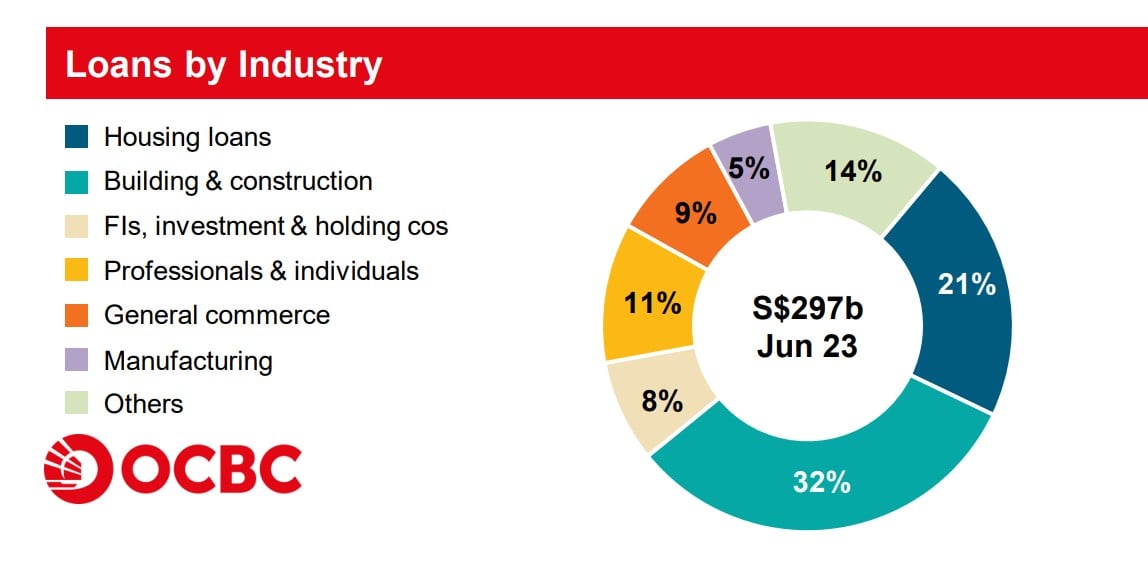

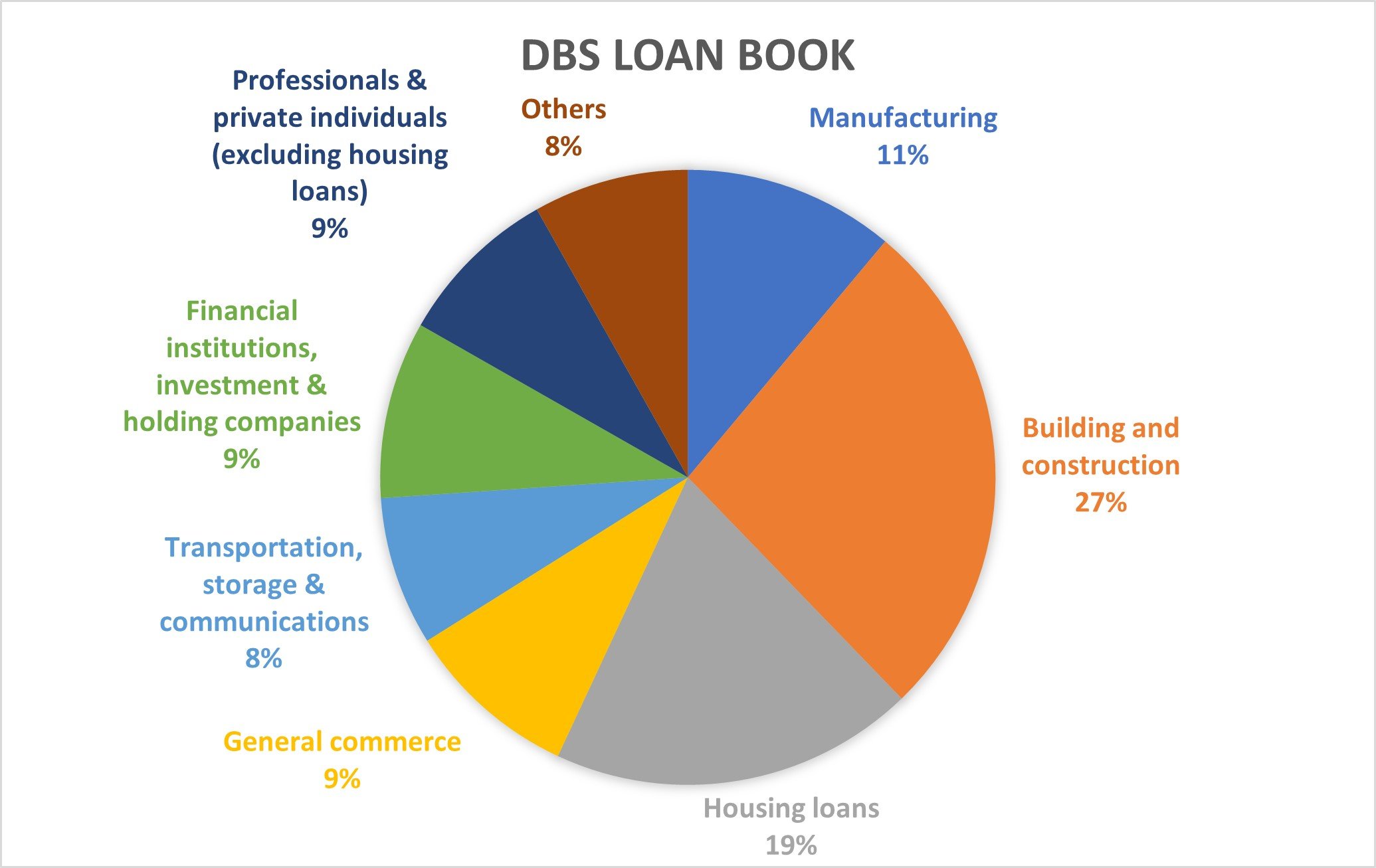

Industry exposure is not all that different, Housing and Construction loans make up close to 50% for both DBS and OCBC:

What about non-interest income of OCBC vs DBS and UOB?

Yes, each of the 3 banks has slightly different flavours – for eg. OCBC with its Great Eastern arm.

But big picture wise.

You can see how each of the 3 banks, non-interest income makes up about 30% of their income.

Very close, and you could argue this is pretty much by design.

When you have an oligopoly dominated by 3 equal players, whatever one player does, the other two will copy.

Which makes it tough for any one player to significantly outperform the others in any new business line (for eg. Wealth management).

As a consumer, I’m sure you’re pretty much aware of this.

Yes, DBS, UOB, OCBC, their offerings may have slightly different flavours.

But by and large you can pick any one of the 3 local banks, and you won’t really be able to find any service where one bank does 10x better than the other banks.

Which of the 3 local banks you use – pretty much just comes down to personal preference rather than anything.

Price Performance – DBS has outperformed OCBC and UOB by a huge margin

Going into the price performance is where things start to get interesting.

This is price performance going all the way back to IPO.

You can see how OCBC and UOB both outperformed DBS in the post 2008 period.

After the 2015 period though, DBS started to catch up with OCBC and UOB.

And since 2020, DBS has significantly outperformed OCBC and UOB.

So the huge outperformance of DBS – it’s quite a recent phenomena actually (past 5 years).

Would I buy OCBC Bank?

Okay, let’s get to the million dollar question.

Would I buy OCBC Bank over DBS Bank or UOB Bank today?

I suppose there are 2 questions here:

- Would I buy banks today?

- Would I buy OCBC Bank (if I were buying banks)?

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great charts & insights on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

Would I buy Singapore banks today?

I think if you’re buying banks today, you really need to understand why you are buying them.

Are you buying them to hold for the next 20 years, while collecting your dividend?

If so that’s perfectly fine.

But if you are buying them to hopefully sell at a higher price the next 2 – 3 years, then it gets a bit tricky.

I don’t know how to put this, but where we are in the debt and interest rate cycle, macro risks are elevated.

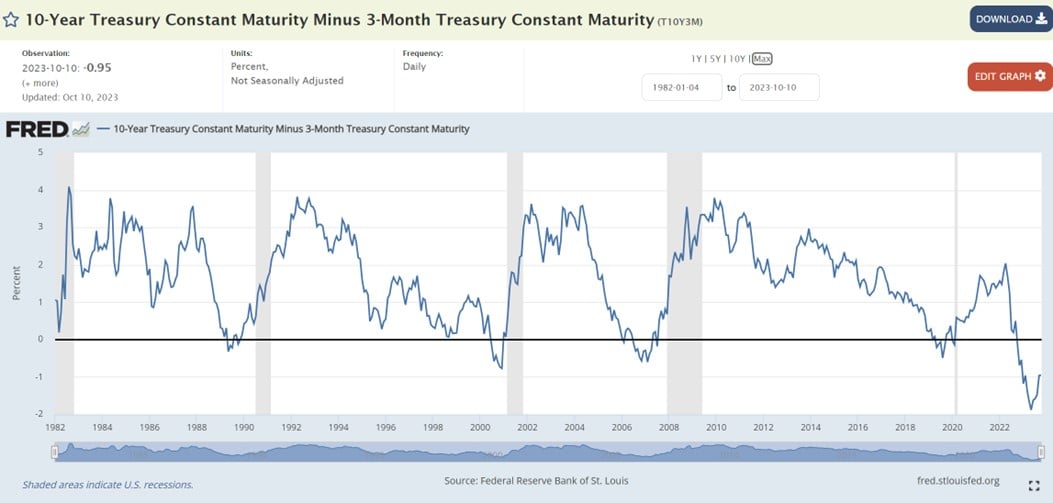

Here’s the US 3s10s yield curve.

Every single recession in the past 40 years, has been preceded by an inversion in the yield curve.

The recession usually hits around 6 – 12 months after the curve beings to resteepen.

This cycle, the inversion in the 3s10s is the deepest it has ever been in 40 years.

And it started to re-steepen in June 2023.

Which would place the danger zone for the US economy in the 1H 2024 range.

FH… why does the US economy matter?

The reason why I keep talking about the US economy.

Is because the US economy determines US interest rates.

And US interest rates, determines interest rates for the whole world, Singapore included.

So if you want to understand how Singapore interest rates may play out the next 2 – 3 years (and the impact on Singapore banks).

You cannot do that without an understanding of how the US economy may play out.

And you have to recognise that there is significant risk over the US economy the next year or two.

So it goes back to the point above.

If you want to buy Singapore banks and hold them for the next 20 years, it’s quite a different question from if you want to maximise capital gains in the short term.

Is the Yield Curve still reliable?

I know many will argue that the yield curve is no longer reliable because this cycle is different.

Because of inflation, because of fiscal stimulus, the traditional signals don’t work anymore.

That’s definitely possible too.

The last time the 3s10s was this inverted was the 1970s inflationary period, and that was not a good time for investors.

And leading indicators are pointing towards trouble in late 2023 / early 2024 for the US economy.

But hey – economic forecasting is not a science, and I could well be wrong on this.

Would I buy OCBC Bank (if I were buying banks)?

Assuming I wanted to buy banks today – would OCBC be my top choice?

Full disclosure that I do not have a position in OCBC (not have I ever, now that I think about it).

I’ve bought DBS and UOB and traded in and out in the past, but never OCBC.

Does that change today?

|

|

OCBC |

DBS |

UOB |

|

Market Cap ($ billion) |

58.4 |

87.6 |

47.7 |

|

Price/Book |

1.10 |

1.49 |

1.05 |

|

Dividend Yield (annualising latest yields) |

6.15% |

5.68% |

6.01% |

I think what does indeed trouble me with OCBC is the China exposure.

If I wanted the China exposure, I would just buy a big 4 China bank like ICBC and collect the 8% dividend yield instead.

No need for additional China exposure from OCBC.

So if I were to buy more exposure today, I’ll probably still go with DBS as the best in class bank, and Temasek links.

And UOB for the other Singapore bank, with strong South East Asia exposure.

And if I really wanted the China exposure, I would just size a position in a big 4 China bank like ICBC to juice the yield.

In fact I do hold positions in China banks ICBC and CCB, and you can see my full portfolio on Patreon. I also share the stocks and REITs I am keen to buy on Patreon.

But that’s just me, and there’s no right or wrong here.

Love to hear what you guys think!

This article was written on 13 Oct 2023 and will not be updated going forward.

For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do sign up as a Patreon.

– Get up to USD 2000 worth of shares

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 2000 free fractional shares.

You just need to:

- Fund any amount

- Hold for 30 days

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Investment Research Tools

I use Trading View for my research and charts. Get $15 off via the FH affiliate link.

I also use Koyfin for fundamental and macro research. Get a 10% discount via the FH affiliate link.

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Best investment books to improve as an investor in 2023?

Check out my personal recommendations for a reading list here.

The content here is for informational purposes only and should NOT be taken as legal, business, tax, or investment advice. It does NOT constitute an offer or solicitation to purchase any investment or a recommendation to buy or sell a security. In fact, the content is not directed to any investor or potential investor and may not be used to evaluate or make any investment. Do note that this is not financial advice. If you are in doubt as to the action you should take, please consult your stock broker or financial advisor.

Hi FH,

I also have a small position in UOB and OCBC, with a similar position in Chinese banks (I got them at dividend yield >9%).

UOB has a less demanding valuation at 1.05x PB while OCBC is at cycle highs 1.11x. UOB should see once-off integration costs with Citi drop off this quarter, so I’m hoping this will give it a boost.

Anyway, if you think a recession is near, the NIM cycle should be turning, and hopefully we can pick up cheaper banks on the other side of the cycle.

Both DBS and OCBC are priced at cycle highs.

While Reits are beaten down.

Cheers

Mrs Pennies

https://pugsandpennies.substack.com

Appreciate the sharing Mrs Pennies!

Personally I think the cycle is going to turn soon. But exact timing, and how hard it turns, remains to be seen.

The overwhelming bullishness over Singapore banks as a stable dividend play makes me wary too. My best investments are usually made when everyone thinks it’s a bad buy, never when everyone agrees it’s a good buy. Singapore banks today feels more like the latter to me.

But let’s see. 😉

Hi FH,

Just asking, are you the one and only male writer of the articles here?

Saw a female co-Founder on CNA

https://youtu.be/vWM_O9dCdmg?t=145

Thanks,

KK.

Hi kk, yes that is our co-founder! 😉

Hi FH,

Great analysis and easy to understand, keep up the good work!

Another 2 differences between the 3 banks is their CEOs and DNA:-

(1) DBS has a great CEO in Piyush, his seed planting since he joined in 2009, had paid off. Can be seen in its share price – pulled away from the other 2 after 2020 (good observation on your analysis)

(2) OCBC and UOB came from conservative Singapore backgrounds and continue to be very prudent till today, hence can be seen in their ROEs

Appreciate the kind words and feedback!

Indeed that looks to be the case. DBS many years ago was like OCBC/UOB, boring and convervative. That seems to have changed of late, and it is reflected in their ROE and consequently share price.

In my opinion, the answer may lie in the IPO of one of the digital assets of DBS Group. On 31 March 2022, DBS Group revealed its plan to list the asset in SGX pretty soon. In this article, I will share my insight on this exciting IPO of DBS’ asset.

https://sgwealthbuilder.com/2023/08/07/dbs-group-share-price-to-rocket-with-10-billion-ipo/

Looks like the article is paywalled – what asset is this of DBS?

Dear FH,

I’m a fan of yours & read all your articles when I come across them. I would like to share with you my real life experience investing in all 3 local banks.

1) I was starting to build my dividend portfolio in 2011, besides buying the Reits, i needed something to hedge their vulnerabilities & the banks seem like a good idea to me.

2) I averaged down aggressively into the 3 banks from 2015 to 2016. How aggressively? Well, almost every other day, I was buying a bank stock. The bank stocks alone became a 6 figure sum. Did i know that it was a good time to buy bank stocks? Honestly, no, I was just trying to build my dividend portfolio, so I did what needed to be done, that’s all. But the process was filled with fear & self doubt, but an inner voice tells me to keep at it.

3) Did i foresee that the bank shares would subsequently take off? No, but that wasn’t my primary objective. Today, my DBS & OCBC shares are freehold. My UOB shares would also be FH if i sell a little, but I don’t need the money, so I will just sit & collect the dividends. The handsome capital gains is the cherry on top of it all..

Amazing stuff – appreciate the sharing very much! And kudos on a successful investment. 🙂