As shared in previous articles, I recently opened a position in Sea Ltd in Jan/Feb this year.

My average buy in price is around high 30s.

Based on latest closing price of $58.4, I’m up about 50% since my buy in price.

Given the rapid move in share price (and latest earnings) – I wanted to take a closer look at Sea to discuss whether I would:

- Buy more Sea stock

- Take profit in my Sea Stock

- Hold

Quite a few of you have been asking me about Sea Ltd (Shopee) recently.

So I decided to release this FH Premium post to everyone.

This was written in early March when the share price was around $58.

Share price has since dropped below the key $56 support, so the technical analysis portion of this article is no longer be relevant – and my views have changed since.

However the fundamental analysis for Sea, and general thought process, remains very much relevant.

Q4 2023 Earnings Results for Sea Ltd

Personally I was not impressed by the Q4 2023 earnings results, despite the market reaction.

I thought that under the surface it suggested some fundamental weakness in the e-commerce business.

But let’s go through it step by step.

Management Guidance for 2024 is very bullish

Management guidance for 2024 is very strong – I do not deny this.

Key highlights are:

- Expect 2024 to be profitable again

- *Key* Expect Shopee GMV growth in high teens and adjusted EBITDA to breakeven in H2 2024

- Sees “significant upside” in Seamoney

- Garena – “In 2023, Free Fire was the most downloaded mobile game globally according to Sensor Tower. We are pleased that these positive trends are continuing into 2024. In February, Free Fire achieved more than 100 million peak daily active users. It remains one of the largest mobile games in the world. With this positive momentum, we currently expect Free Fire to grow double-digits year-on-year for both user base and bookings in 2024”

- Overall business – “We are pleased to see positive trends in both growth and profitability for all three of our businesses. Looking ahead, we will continue to invest for the future with discipline and focus.”

That’s a very bullish outlook from CEO Forrest Li.

A big reason for the jump in share price post-earnings.

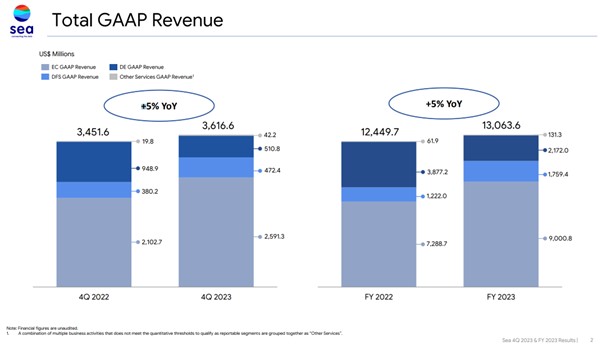

4Q 2023 earnings report for Sea Ltd

4Q 2023 revenue is up 5% year on year.

Looking at the breakdown, and you’ll find that eCommerce revenue and Fintech revenue grew well, while Gaming revenue went down.

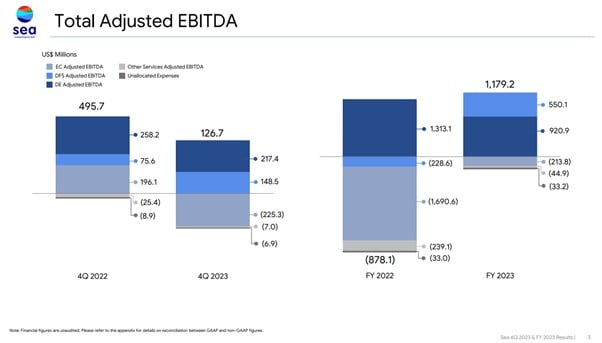

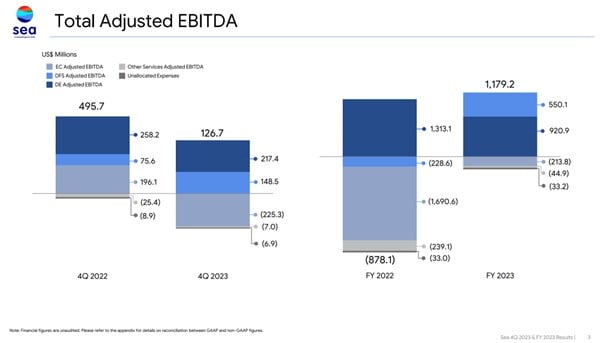

Adjusted EBITDA tells a story of:

- Earnings from gaming is down 16% from last year

- Earnings from Fintech has almost doubled

- In 4Q 2022 Shopee was focussed on profitability so the eCommerce arm was profitable, but in 4Q 2023 Shopee has refocussed on growth and has swung back into loss making

Let’s discuss further on each of the 3 arms:

- Ecommerce (Shopee)

- Fintech (Seamoney)

- Gaming (Garena/Free Fire)

Ecommerce (Shopee)

The e-Commerce earnings can be summed up as follows:

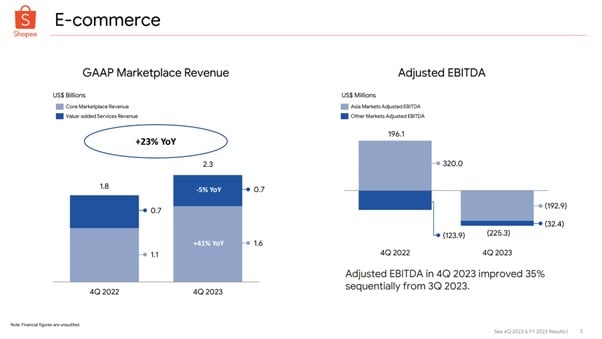

Back to revenue growth, at the expense of massive marketing spend.

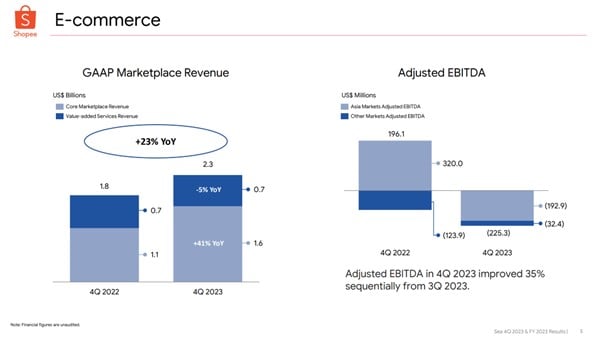

Revenue growth has recovered to 23% year on year.

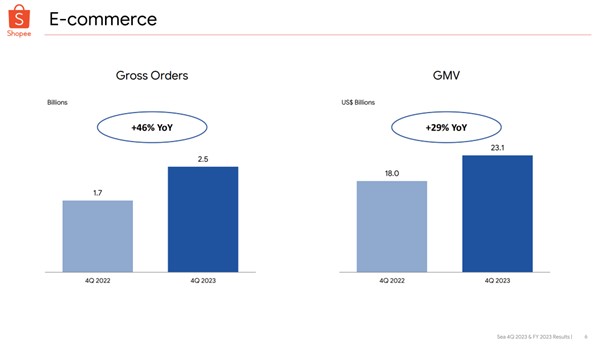

Both gross orders, and gross merchandise volume are up nicely.

The problem – is that growth has come at the expense of a massive marketing budget.

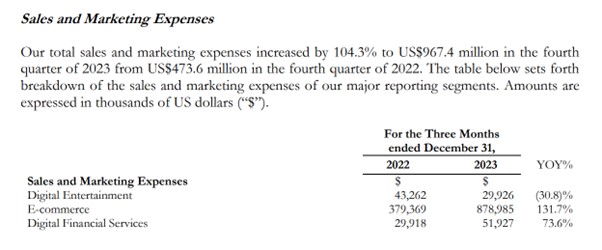

Shopee spend a whopping $878 million in sales and marketing in 4Q 2023.

That’s flat vs 3Q 2023, but up a whopping 131% year on year.

Because of this adjusted EBITDA went back into the red – a $225 million loss.

Basically – Shopee had to spend $878 million, a 131% increase in marketing budget, for a 23% increase in revenue.

The immediate question that comes to mind – is Shopee / E-Commerce even a sustainable business?

If you need to spend $800 million each quarter on marketing promotions for 23% revenue growth.

And the moment you dial back marketing revenue growth goes flat.

It raises the question of what truly is the economic moat of this business?

If a competitor like Tik Tok comes along and throws the same amount of marketing spend, is that going to draw all of Shopee’s customers away?

Is this business like ride hailing in the sense that customers just use whatever app gives them the best price, and there is zero moat and little chance of sustainable long term profits?

The market seems content to overlook this point for now and focus on the positive FY24 guidance, but when I look at the earnings this is the biggest question that jumps out at me.

Fintech (Seamoney)

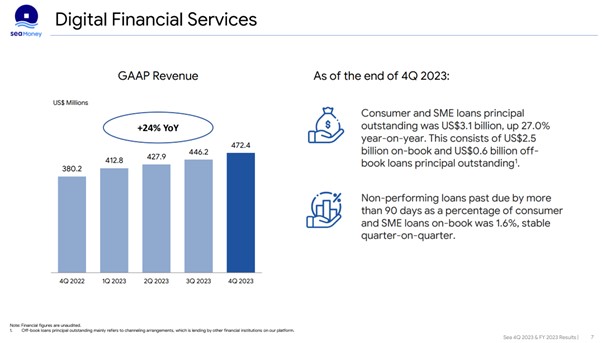

Fintech is doing well though.

GAAP revenue is up 24% year on year.

Adjusted EBITDA has almost doubled year on year.

When queried on the call management suggested that most of the earnings are coming from their lending to merchants.

But the fact that management has been generally quite tight lipped on this segment of the business, coupled with the fact that the numbers show very strong performance – suggests that whatever they are doing is working, and management doesn’t want to beat the drum about this else they invite more competition.

So I’m actually quite upbeat on the fintech business.

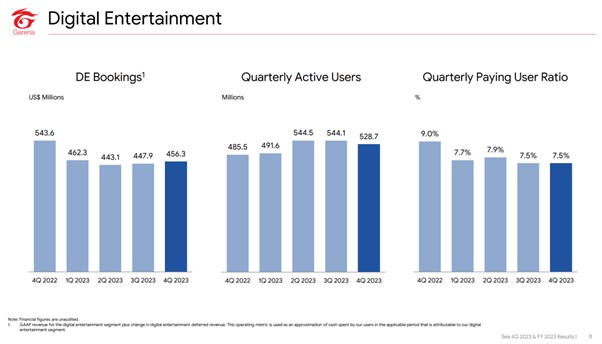

Gaming (Garena/Free Fire)

On gaming – the numbers generally show that the decline has stabilised for now.

The number of active users is still going down, but revenue is flat / no longer going down.

That said the fundamental problem with the gaming business for Sea is that it remains to be seen if Sea can replicate the success of Free Fire.

This isn’t an Activision Blizzard that has a track record of churning out hit games year after year.

Sea only has 1 hit game Free Fire.

And for now they seem content mainly to milk the game for what it’s worth, and take the profits generated and plow into their eCommerce / Fintech business.

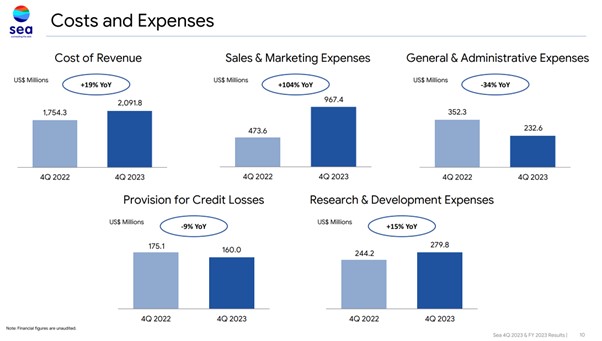

Sales & Marketing expenses have increased tremendously

Generally speaking, management has been quite good on managing costs.

Remember 4Q 2022 was the quarter in which they were focussed solely on profitability, so it would have been a very challenging quarter to compare against.

And yet the expenses fare quite well on a year on year basis.

The only exception is sales and marketing expenses – up 104% year on year.

As we discussed above – Shopee has massively increasing marketing spend to refocus on growth.

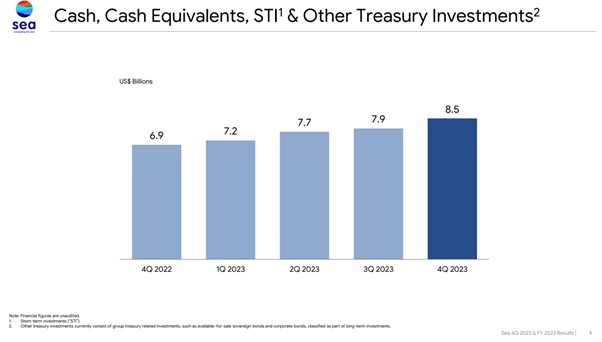

Balance Sheet is rock solid

Balance sheet is rock solid for what it’s worth.

There’s $8.5 billion in cash on the balance sheet, even higher than in 3Q 2023.

So there shouldn’t be any urgent need for Sea to tap capital markets / raise financing, and that $8.5 billion cash buys them a ton of runway even in a higher interest rate climate.

I really like this point.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share thoughts on Twitter regularly.

Don’t forget to sign up for our free weekly newsletter too – with weekly roundups every Sunday!

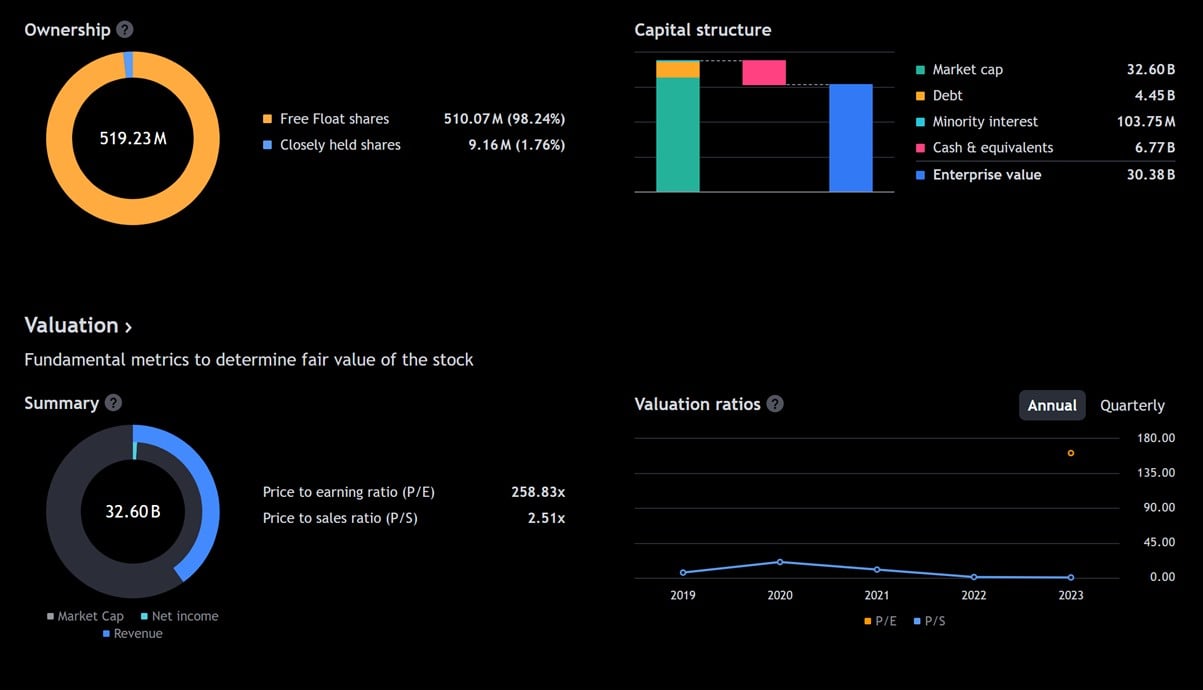

Valuations of Sea

At current price Sea trades at a $32.6 billion market cap (less the cash and debt gives us an enterprise value of $30 billion).

That’s a 2.51x price to sales ratio.

Trying to run a detailed valuation for Sea is fool’s errand, given how quickly the business is evolving.

But off the top of my head, if management can execute on their FY24 guidance – I could see fair value for the business settling anywhere from $30 – $50 billion.

That translates into a share price of about $53 – $90, very much in line with the technical analysis above ($56 – $88 range if the $56 support holds):

Sea’s share price – Technical Analysis

Technical Analysis for Sea is below, but since then the key $56 support has broken quite conclusively.

So much of this is no longer relevant, and do update your thinking accordingly.

My latest views on Sea is shared on FH Premium.

Key Support levels for Sea

The (E) below shows the day Sea earnings came out.

The price action was very interesting – after going as high as 58 in the first hour of trading.

It then dropped all the way back down to low 50s.

Before closing the day around 56.

You can see the massive selling volume in the first hour – which suggests that there was a very big seller looking to sell in size into the earnings report.

Share price has been doing well of late though.

After the 35 support level held in Jan, the share price has gone to 40ish before the earnings, and after earnings it has gone to 58 where it sits today.

Here’s the longer term chart.

The gap down in Sep 2023 has now been filled, and the new support level is 56.

Technical Analysis for Sea is bullish

So generally speaking the charts for Sea are bullish.

As long as the 56 support holds, we may potentially see Sea setting into a new trading range from 56 – 88.

Would I buy more Sea stocks?

As an investor, there are always 3 things you can do with a stock.

If you think the stock is expensive, you can sell it.

If you think the stock is cheap, you can buy it.

If you think the stock is fairly valued, or if you think the stock is cheap but you have no more cash to buy more, you can hold it.

Based on technical analysis above – the uptrend is still intact, and 56 is the new support level to watch for.

Unless 56 breaks, I can still let the stock run for now given the uptrend.

Fundamentals wise it’s a bit mixed.

Yes the management guidance for FY24 is very strong.

But the actual operational performance is a bit mixed.

The way Sea is structured today, the biggest business by far is eCommerce.

And yet eCommerce is still bleeding cash, and it’s unclear whether it will ever turn profitable.

Management has guided for breakeven by H2 2024, so it will be crucial to see if they can deliver on this promise, while maintaining / growing market share.

So… what would I do with my Sea stock?

All things considered, I’ll probably hold onto the stock for now.

For as long as the 56 support holds, I can afford to let the stock play out (Note: $56 support has since broken, so my views on this have changed).

If management delivers on the guidance, I can see the stock going to the high end of the 80+ range.

I’m not sure if I want to buy more Sea stock right now though.

At $30 – $40, market cap was in the $20b range which I thought offered good risk-reward.

At the $30b range today, it looks a lot more fairly valued, and much will come down to management’s ability to execute.

Note that this FH Premium article was written in early March when the share price was around $58.

Share price has since broken the key $56 support, so I have changed my position on Sea.

However, the fundamental analysis and thought process above remains very much relevant.

Given the amount of investment opportunities available out there, I can afford to be picky, and only buy stocks where both the fundamental and technical analysis lines up – and you can see my full stock watchlist on FH Premium.

As always – for my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do subscribe for FH Premium.

Buy Bitcoin, Ethereum, and crypto on Coinhako – 10% off trading fees

I use Coinhako to purchase Bitcoin, Ethereum and crypto.

Enjoy 10% off trading fees using:

Invitation Code: CwHdSgU

Or sign up link: https://www.coinhako.com/affiliations/sign_up/CwHdSgU

Check out my full review on how to buy Bitcoin / Ethereum.

– Get up to USD 2500 worth of shares

I did a review on WeBull and I really like this brokerage – Cheap US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now.

You can get up to USD 2500 free shares.

You just need to:

- Fund USD 500

- Execute 5 trades

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.