What an absolute bloodbath in tech stocks!

From it’s October 2021 high of $366, literally just 3 months ago – Shopee (Sea Ltd) has plunged 58%.

And it’s not just Shopee though, almost all the high flying tech stocks have been crushed the past 3 months.

A lot of short-term indicators I track are indicating we are very close to a local bottom here.

As long as these support levels hold, we could see a pretty big bounce in risk assets short term (followed by a broader decline as 2022 plays out).

Never thought I would say this – but at $154, is Shopee (Sea Ltd) a great value buy?

Basics: What is Sea Limited / Shopee?

In October 2020, I wrote an article evaluating Sea Ltd at $169.

Funny how life works, because almost 1.5 years later, after a 100% rally from there, Sea Ltd is now back below that price.

Sea Ltd is basically split into 3 parts:

- Digital Entertainment (DE) – Gaming business, Garena Free Fire is the big cash cow

- E-Commerce (EC) – Shopee, basically

- Digital Financial Services (DFS) – Seamoney, the nascent fintech arm

Core markets for Sea Ltd are South East Asia, Taiwan and Brazil.

While management has a strong eye on expansion into Poland, France, Spain and India.

For now, the 2 biggest revenue generators are gaming and eCommerce:

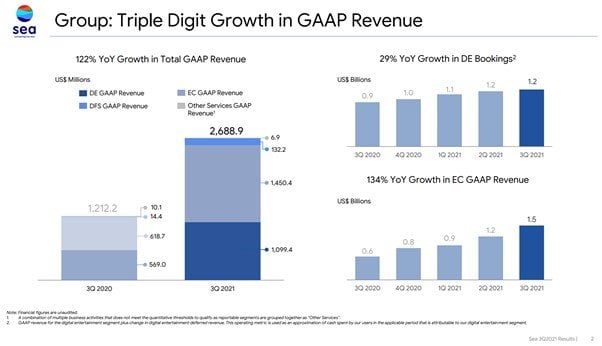

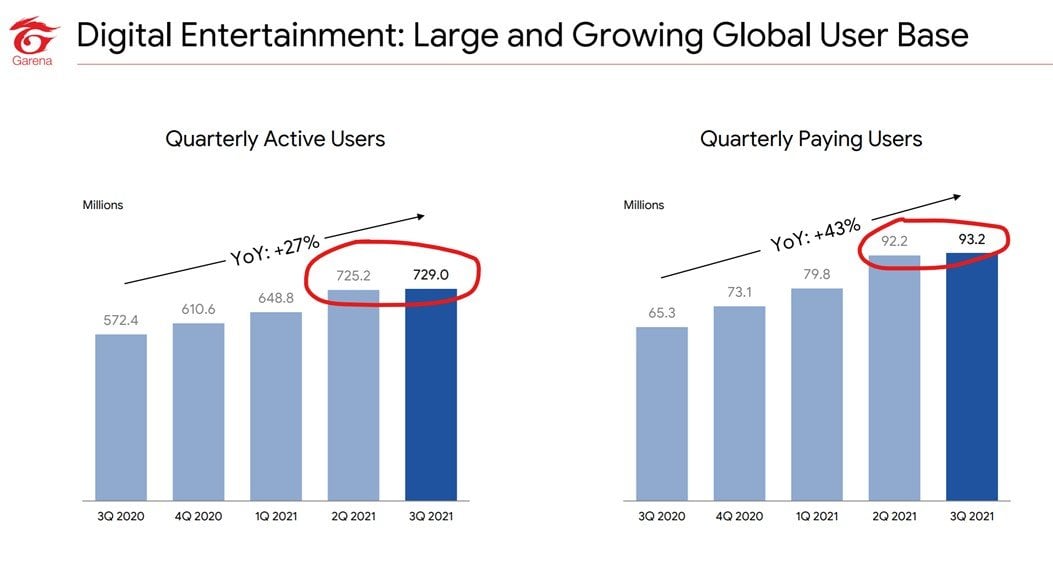

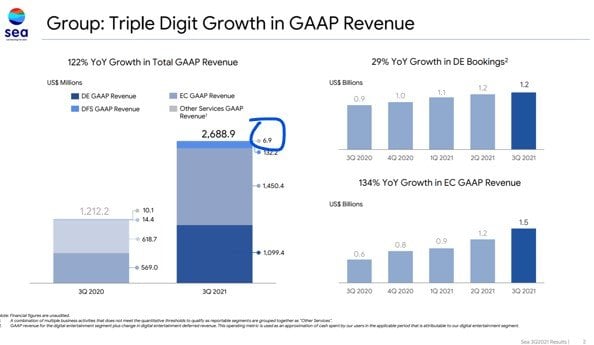

Core Gaming Business is slowing

I’m just going to say it – the big red flag in the latest financials is that the core gaming business is starting to slow.

Now the narrative before this has always been that Shopee and Seamoney will burn massive amounts of cash to grow market share.

While the gaming business, powered by Garena Free Fire, generates a ton of free cash flow to fuel the cash burn.

That narrative is now in question, because the gaming business is starting to slow:

At the same time, expenses are not slowing down:

There was a time when burning money to grab market share was sexy, but this is most definitely not the year.

In a year when the Feds are on track to hike 4 times and start Quantitative Tightening, ballooning losses are not sexy at all.

Tencent sold $3 billion in Sea Shares

When it rains, it pours.

To add to Sea’s misery, their biggest shareholder, Tencent, is mired in problems of their own with the Beijing Government.

Word is that Beijing doesn’t like the China tech giants to have fingers in every pie.

The official version is that this is not good for competition, the cynic’s version is that they don’t like anyone to have that much power.

The past week saw Bytedance close their entire investment division.

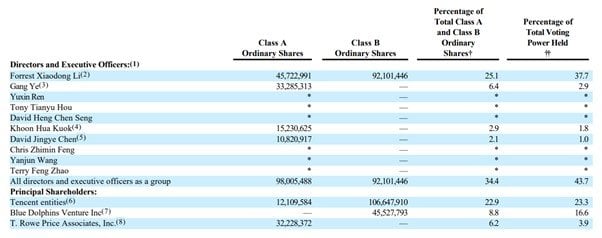

Tencent has also been very obediently selling down stakes in their portfolio companies, which includes JD, and of course Sea Ltd.

Tencent has sold close to $3 billion in Sea Ltd stock at an average price of $208.

But what happens next?

Even after the sale, Tencent holds 18.7% of Sea, which is worth about $17 billion at today’s price

Tencent has committed that they will not further sell their stake for another 6 months, but what happens after that?

Tencent will convert all its stock into Class A stock which holds less votes, which means the founder Forest Li will hold 57% of voting rights going forward.

You can argue that this might satisfy Beijing such that Tencent won’t need to sell more stock after 6 months.

But frankly – it’s tough to call exactly what will please Beijing.

Until this is resolved that could add a lot of near term pressure for Sea stock.

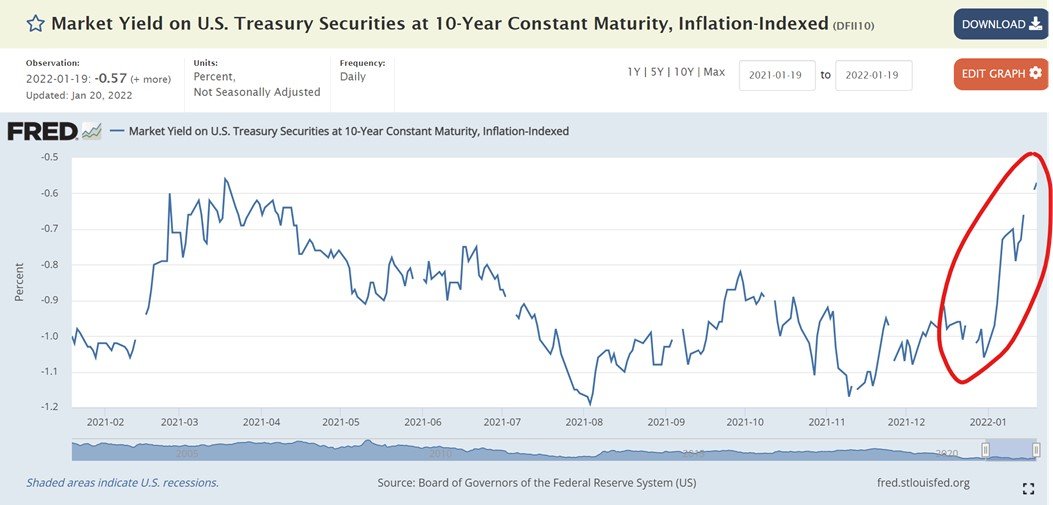

Respect the Macro… Macro Headwinds from Rising Rates

I wrote a detailed article last week sharing my macro views and why I think 2022 is going to be the most adverse macro environment for risk assets since 2018.

I hate to say it, but I don’t think 2022 is the year to try to be too clever on fundamental stock picking.

This is a new regime of higher inflation and rates volatility, very different from the previous.

So I think 2022 is the year to respect the macro, to respect the flows.

When things sell-off, the market will throw the baby out with the bathwater.

Switch into fundamental stock picking mode only when the dust settles.

And short term bounce aside, I think the broader move for risk assets is downwards, until such point when Powell changes his mind on rate hikes.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Just created a Discord server where I collate analyst reports and investing resources that I come across in my research. Hit us up here if you’re keen.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

What I like about Sea?

Okay, so everything above was the bad stuff.

Now let’s talk about what there is to like about Sea:

- Impeccable Execution

- Sea Digital Bank

- A lot cheaper than 3 months ago

Impeccable Execution

You almost never see me say this about any company, especially not the ahem *ah gong* companies.

But I think Sea’s management team has impeccable execution.

Seriously, everything they touch turns into gold.

From Garena Free Fire, to Shopee taking on Lazada in SEA, to their recent expansion into Latam and Europe. Even their execution of Seamoney in Indonesia looks very promising.

I don’t know how they do it, but this horse is truly impressed by their execution.

Tech is maturing very quickly, and at this point in the cycle it’s sometimes less about how good your tech is, and how well you can execute in the real world.

And in that sense, I’m really impressed by Sea.

If they continue executing like this, there’s a lot of potential to grow in their core markets of SEA, Brazil and Taiwan, And their new markets of Poland, France, Spain and India.

Sea Digital Bank

Take a management team with a strong track record of execution, and given them a digital banking licence – and watch what they can do.

I have very high hopes for the Sea Digital Bank.

The Fintech part of the business is tiny now, but if they play their cards right this could in time become Sea’s version of AWS (Amazon Web Services – the cash cow for Amazon).

Fintech is big money for any player who can build a dominant position, which is why we see so many players trying to do it.

There will be fierce competition from the Grab-Singtel consortium, but I think the market is big enough to accommodate a few players.

That said, short term, Seamoney is not going to contribute meaningfully to the bottom line, and will burn lots of cash.

Valuations – A lot cheaper than 3 months ago

If you liked Sea Ltd at $366, you should be loving it at $154, no?

From a fundamental perspective, nothing much has changed over the past 3 months.

And yet the price is 58% cheaper.

What is a fair valuation for Sea?

Price to Sales still sits at a lofty 16 times though.

Which begs the question – what is a fair valuation for Sea?

With high growth companies like this (revenue growth in excess of 100%), it really doesn’t make sense to run anything fancy like discounted cash flow.

I’m just going to stay very big picture here.

Sea’s core markets of SEA, Brazil and Taiwan have a combined GDP of $4.2 billion.

Tencent at their prime was valued at US$660 billion, and China’s GDP is $14.7 billion.

If we assume that Sea one day grows to become as dominant as Tencent in its core markets, and the market values it as such, then the fair valuation for Sea would be:

4.2 / 14.7 * 660 = $188 billion

Which is almost 120% upside to current market cap of $85b.

Of course, this analysis doesn’t count their growth markets of Europe and India, so that’s just pure upside.

But you could also argue that the market may never value Sea like it does Tencent, or that Sea would never become as dominant.

But that misses the point of this tabletop analysis.

Big picture – is that if you think Sea can become as dominant as Tencent one day, and you think the market will value it like Tencent, there’s potentially 100%+ upside from here.

Shopee vs Grab?

I suppose the most natural comparison to Shopee would be to Grab.

Both are South East Asia platform plays, both have an upcoming Fintech arm.

Grab’s market cap is significantly lower at $20 billion, a mere 23% of Sea Ltd.

That said – both have the same problems where they’re still not profitable and cash flow positive.

In 2022’s macro environment, the market is likely to punish such stocks, and Grab themselves have also collapsed 45% from their IPO price.

That said – if I were bullish on South East Asia, I would not want to get sucked into a discussion of which will prevail longer term.

I’ll probably just buy both, together with Gojek-Toko when it lists, and be done with it. Assuming I’m bullish on SEA tech of course.

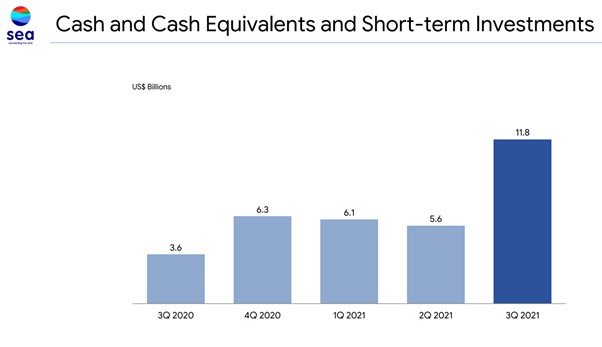

Balance Sheet is ok

Couple more points to look at then I’ll share holistic views.

Balance sheet is very strong with $11.8 billion cash on hand, so even though Sea is burning through a lot of cash it’s not a major cause of concern.

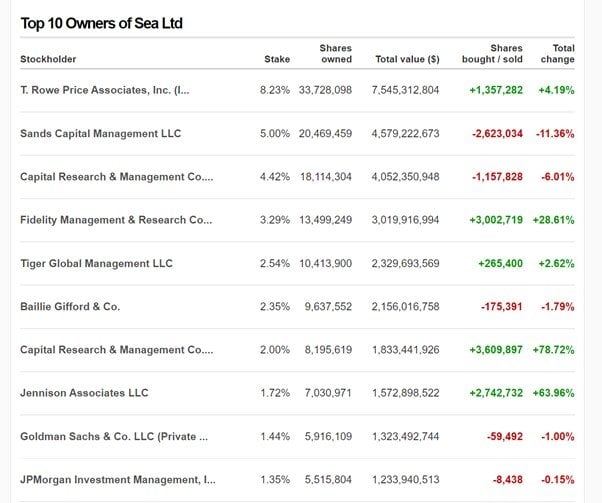

Institutional Shareholders are very strong

List of Institutional Shareholders are very strong too.

Some really big names on there, including T.Rowe (8.2%) and Tiger Global (2.5%).

This is a good sign.

Will I buy Shopee / Sea at $154?

On to the million dollar question – Will I buy Shopee (Sea Ltd) at $154?

Full Disclosure – I don’t have any existing position in Sea Ltd, so read into that what you will.

I like the impeccable execution from the management team.

I like the growth potential, from their growing core South East Asia, Taiwan and Brazil markets, and from new markets in Europe and India.

Valuations wise – I think if you can take a longer-term perspective, the valuations are reasonable. There’s a lot of growth baked in, but the company is also growing very quickly.

What I don’t like, is actually completely beyond Sea’s control.

It’s the macro headwinds, and potential unwind of COVID trades.

The past week saw pandemic winners Peloton and Netflix crater 20%. It looks like the post-COVID normalisation is happening faster than expected, and I would be curious to see how that would impact Sea’s numbers going forward.

If people go out more, that could translate into slowing growth in eCommerce and gaming.

And from a macro perspective, I just think this year will be tough on high beta stocks like Sea.

Sure, the stock is very oversold now, and I wouldn’t be surprised to see a strong rally until late Q1 / early Q2.

But then the Feds are going to hike 4 times, and start on Quantitative Tightening.

I mean how much can stocks go up, until the Feds change their mind and ease policy again?

Short Term or Long term position?

So to answer this question, I think it depends on whether I see this as a short or long term position.

Short term, 3 – 6 months, I think it may make sense to buy now and try to flip it into any strength in Q1. Subject of course, to proper position sizing and stop losses.

Longer term, say 3 – 5 years, I don’t see a big hurry to add.

Fed hikes will take some time to play out, and as shared in last week’s article, I don’t see them changing their mind for as long as inflation stays sticky.

And until they change their mind, I think the upside for risk assets generally will be muted.

You can check out my full portfolio and how I am positioned on Patreon.

But like I said, I know not everyone is a fan of market timing. For those who are into Dollar Cost Averaging (DCA) you might want to just ignore the entire discussion on timing.

Closing Thoughts – I’m tempted to flip Sea Stock

I’m actually pretty tempted to buy Sea and just flip it short term (2 – 3 months).

Market looks close to capitulation here, at least in the near term.

Buy it, set a stop loss, and look to sell by late Q1/early Q2.

And buy it back as 2022 plays out.

But truth be told, I haven’t made up my mind just yet.

For those who are keen, you can check out my full portfolio, and weekly updates on my buy and sells (and my stock watch) on Patreon.

I would love to hear what you think about Sea though. At $154, is it a screaming buy? Or still a falling knife?

As always, this article is written on 22 Jan 2022 and will not be updated going forward. Latest thoughts (and my stock watch and personal portfolio) are available on Patron.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Looking for a low cost broker to buy US, China or Singapore stocks?

Get 1 free Apple share (worth $230) you’re new to and fund $2700.

Get a Free Apple stock (worth S$230) when you open a new account with and fund $2000.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

Hi FH, just 2 comments.

1. I don’t think the chinese government is concerned with Tencent being a ‘monopoly’ overseas, it dosen’t go in line with their policies for companies to invest more in RnD and expand overseas markets. (The stars and the sea, if you know what I mean). So what’s the explanation for the Sea divestment? I don’t know. Also, I’m actually more concerned about future US government actions against Chinese tech. Feels like BAT are being sandwiched. They won’t collapse, but it’s hard to get a high rate of topline growth moving forward. If Baidu develops the worlds first self driving software, the US hammer will come down. If Baidu buys over lets say Weibo, the Chinese hammer will come down.

Also, the big question for FAANG and BAT, all the tech companies, is that are current earnings growth rates sustainable? If we take Apple and Tencent as examples, their earnings growth stagnated in 2018-2019, and even went negative. So it is possible that earnings growth rates start to decline in 2022, and that 31 Dec 21 valuations were simply too high.

2. The yield curve, as always. It’s kind of worrying how fast the spread is tightening. We might get a year of rate hikes + balance sheet taper, which is like 2014 – 2018 ? PLUS declining earnings growth rates like in 2018 – 2019. Double whammy for big tech, which is like 30% of the SNP500.

So what should we do? Like yourself, I have some picks in mind, but can’t decide whether to enter or not. Maybe I’ll just play it safe and wait for the next easing cycle, or when the spread gets close to forecasting the easing cycle.

Thanks once again for great content.

A lot of China tech don’t derive significant revenues from the land of Stars and Stripes (for obvious reasons), except for TikTok I think. I think if the Stars take too many actions against china tech, then CCP may be forced to retaliate in some ways (remember many foreign corps are deriving significant revenues 20-40% from china). Look at Walmart , Nike, Tesla, Intel incidents. Though china has to position itself as biz-friendly, so they have to tread carefully. They can also push aggressively into friendly countries in Africa, Mid East, SEA and even some EU. Look at Xiaomi which is enjoying high growth rates from emerging economies.

Plus china itself is a huge market, still lots of runway to grow. Projected to be largest economy around 2030 and double GDP by 2050. If china population shrink to 1bn by 2050 due to falling birth rates, and GDP is 40trillion, then GDP per cap could be 40,000 which is respectable. The population there also invests most of their wealth in real estate (hence contributing to the bubble), once the mindset shifts towards stocks , we could see higher valuations coming, although that is no guarantee. But bear in mind that any actions taken by the Stars, also hurt themselves . It’s mostly lose-lose. Look at the tariffs, they want to remove some tariffs to reduce inflation. They are still selling chips to china. Many of these actions are wayang shows.

Hi LME,

That’s a great comment. My thoughts:

1. True, you could be right on this. I naturally made the connection between the two, but you are right that it may be finding connection where there is none. If so the Sea divestment is interesting, and we may need to monitor to see more clues as to their true intentions.

Actually the China tech break was instructive. It’s basically a repeat of 2000 in some ways. Once the bubble burst, companies spend less on advertising, so even companies not directly hit by the regulations were impacted by the lower spending across the sector generally. I wonder if the same will play out with US tech this year.

2. Agreed. The pace of change is astounding. Like you said, it is the entire 2014 – 2018 monpol tightening, compressed into 12 months. Even if the economy is strong enough to take it, the upside for risk assets should be limited.

Personally I’m holding cash at this moment, looking for an opportunity to deploy it this year. Actually all my cyclicals like banks, REITs, oil etc are holding up very well. So I might cash out and rotate into other sectors as the year plays out.

Just to add – really good point on the situation China BAT is in. I suppose the natural answer is that going forward, China tech giants will be a shadow of their former self. I dont think they will ever evolve to become as big as the FAANG, and that is by design in some ways because CCP does not want any person (or entity) to have that kind of power to rival them.

what do you think, whether they can continue to grow in tandem with china GDP growth? I think Baidu’s core business in search is not looking good, with new rivals like Bytedance stealing ads money. Its cloud also fighting with giants like Huawei, baba and tencent cloud. Baba and Tencent are getting ‘old’/matured, but I think they should be able to grow in their existing buisineses quite well. I’d be interested in bytedance’s IPO, if they can copy some elements of FB, Wechat, instagram, etc. I think they have a very huge runway. Politics wise, having an alternative to Wechat is a good thing for CCP , and also good for EU since they probably don’t like FB dominating (judging from the fines they have handed out to FANG).

Some of the recent moves from Beijing, especially shutting down the VC/Investment arms (Bytedance) are quite worrying. Looks like China tech will never be allowed to grow into a FAANG like monopoly.

If so – they may never hit the kind of valuations that FAANG has.

But if the target is just to grow in tandem with GDP growth, that’s a significantly lower bar that would be easier to achieve.

But does faang have any vc/investment arms? I know goog does but their venture companies don’t contribute much to revenue. Yet they are able to grow so big in their core biz. But i think their valuations and revenue are partly owned to the massive money printinng effect. If we withdrew QE since 2008, doubt they will be able to grow so big til now. Xiaomi on the other hand is able to keep their investment arm in hardware startups, so i think ccp just want to increase oversight over internet giants as somehow it is easier to form monopolies in internet due to the winner takes all phenomena.

Yes, really agree with this. With the FAANG a big part of their growth is also due to favourable macro and passive index flows. That could easily reverse this year.

Regarding execution:

– Gaming: did Tencent (king of gaming) help the mgmt to suceed?

– Seamoney: is it only ShopeePay and used only in their games and Shopee? Is there growth outside the ecosystem?

– Shopee: this is pure burn cash with lots of promotions, of course can grab market share easily. Logistics per package only costs $1 in most cases, how is this sustainable?

Overall, very risky in depending on 1 game. FinTech is also unproven and very very competitive (GrabPAy, Apple, Samsung,Google, Alipay, WeChatPay, Stripe, PayPal, etc.) . Fintech sucks, nobody wins.

Shopee will face more competition with Lazada as Baba is forced to expand overseas. Also fighting with GrabMart, Amazon Fresh, etc.

Overall bearish on this stock. Very risky play.

I’d argue execution is actually easy because Shopee outsourced their logistics to 3rd parties and probably subsidised heavily. They just provide a website with lots of ads and promotions and localisations, sure succeed, especially when Lazada is facing management issues and retreating. Gaming probably boosted by cooperating closely with Tencent who taught them the secrets of creating successful games. But gaming itself also very very competitive.

Give me $10 bn and I can also recreate Shopee.

also what if the next few Quarter earnings are disappointment , due to them wanting to tighten loss, and competition with Lazada, and maybe consumers tightening wallets? will it prompt the price to drop like Netflix?

massive competitions on ALL fronts, and yet loss-making deeply. No moat whatsoever. At least e-commerce like baba , jd and amazon they have logistics as a huge moat. Their logistics network is something that is difficult and takes billions and years to develop. Going forward, SEA will find it diffcult to raise more cash to burn, so they may be forced to tighten which likely hurts growth. If a recession happens, it will likely spill over globally, consumers may tighten wallets. Plus digital banks require massive cash burn as well… So it’s only a downward spiral from here.

Thanks! Appreciate the sharing.

I wouldn;t buy any dips until a clearer picture appears. Yes there may be a rebound , yes I may miss out some gains, but the stakes and risks/uncertainties are very high now. It is looking like a repeat of 2000 + 2008 TOGETHER. Mother of all bubbles is bursting in front of our very own eyes. Stock valuations still very high. Inflation caused by many factors (tariffs, labour shortage, covid, money supply, supply shortage). Crypto lending platforms give you high yield of10% as they lend money to gamblers at 20% interests. This is certainly a house of cards. They are almost certain to screw up big time.

one government has tight control over everything so they can manuevuer any crisis carefully. the other has almost no control over anything besides monetary policies…

Everyone should read this https://www.gmo.com/asia/research-library/let-the-wild-rumpus-begin/

Agree with this in some ways. This new regime of higher volatility in rates/inflation is very different from the previous regime. It will take time to play out.

Just within 2 yrs, shopee has already overtaken Mercado libre, Latin America biggest e-commerce player.

Like u said, everything shopee touches, it turns into gold.

Short term it’s going to be volatile, no point trying to time a bottom, just do DCA at this price range. I bot in at $170 and will just buy in at intervals of every 10-15% drop.

5yrs down the road, I believe we will SEA will be few folds above current prices.

https://blog.apptopia.com/shopee-overtakes-mercado-libre-top-shopping-app-latam

it’s called ‘cash burn effect’ boosted by the pandemic. Most of its competitors in Latin Am are trying to be profitable. Even amazon doesn’t burn cash to such an extent — it always tries to be near breakeven, and it burns cash to build long-term moats, unlike shopee which burns to capture market share which can be easily stolen. And itself may be disrupted by new comers such as the PDD-clone mentioned in the article.

if some VC can give me a few billions, I can guarantee 200% y-o-y growth in revenue (just don’t look at the bottomline). Then I can also guarantee the share price will rocket to the moon. Then I will cash out at the peak, and hehe bye bye. Good luck to all holders.

ya.. agreed.. haha.. sounds like a ponzi disguised as a business….

Hmm, more like become a penny stock in 5 years when investors realised the ‘beautiful growth story’ is just an unsustainable sham. They think Shopee may eventually become Free Fire (highly popular cash cow). But bear in mind games are different: the player has stakes in the game i.e. the character they built up and the network effect due to friends playing with them — high switching cost. On the other hand, Ecommerce has no customer loyalty. Shopee is literally paying people to download their app and to buy their stuff. It’s suicidal for existing profitable companies to compete head-on with this unprofitable company which is ‘spoiling the market’ so to speak. Every market it enters, it needs to burn massively to grab market share. It’s a money-sucking black hole.

That is true. But the case of Amazon shows that it is possible to generate moats in eCommerce. And the case of Taobao also shows the flipside, and competitive threats.

Whether Shopee evolves to become Amazon or Taobao is the big question.

after so much discussion above , I think you’re still missing the point.

amazon has logistics network that even walmart /shopify can’t rival that guarantees fast and fuss-free delivery . So best case shopee becomes a shopify? unless shopee wants to build logistics itself that it owns. otherwise other players can also tap on 3rd logistics to provide same kind of delivery service, thus shopify has no moat, and itself will always be disrupted. used to remember it was qoo10 => lazada => shopee … highly likely another player will come along .

Sorry yes I meant that Shopee can go down the Amazon route of building its own logistics arm. Althought that said, Taobao has Cainiao, and JD has their own JD logistics, and it didn’t help all that much when PDD/Bytedance came along.

Maybe disruption is just inevitable then…

Also games are usually like fashion. Like all content-based businesses, they may eventualyl fade away. Who still remembers Angry Birds, and those once-popular iPhone 4 games? Pokemon Go, Candy crush anyone? The growth of FreeFire is slowing — quite a dangerous sign. Very few games become legend like Warcraft, Starcraft with people still playing. Who knows whether metaverse and NFT game will be the next big thing, stealing market shares from existing games? If SEA’s cash cow does fade away, and it cannot quickly replace it… then good luck. Have yet to see it coming up with new games so far. And with less help from Tencent, wonder if it can continue to produce hit games. SEA and Tencent will be considered as rivals moving on. The picture is not looking pretty.

Yes agree that this is the bull case. Of course, whether it actually plays out is a different question.

it’s called ‘cash burn effect’ boosted by the pandemic. Most of its competitors in Latin Am are trying to be profitable. Even amazon doesn’t burn cash to such an extent — it always tries to be near breakeven, and it burns cash to build long-term moats, unlike shopee which burns to capture market share which can be easily stolen. And itself may be disrupted by new comers such as the PDD-clone mentioned in the article. It’s a get-rich-quick scheme for the founder, Forest Li. Hopefully he has cashed out before the crash. It never baffles me why founders & investors think they have a competitive advantage in this kind of ecommerce. Price-sensitive consumers have no loyalty. Sellers have no loyalty. Barrier to entry is low. Seems like anyone can just create an ecommerce website nowadays.

There’s still a long, long way for unprofitable tech stocks to fall. The correction in ARKK is probably only halfway through. Millennial investors are going to learn the same lesson many of us did twenty odd years ago.

yes agreed. After SO MUCH discussion, I have yet to see a CONVINCING bull thesis for all these stocks. I just trade them in and out, never dare to hold long-term. But I think it’s safer to trade when the bearish momentum reverses. They are only good for trading and punting. Gen Z traders / investors don’t know how the REAL world works. Cathy wood , like analysts and many others, are SALESMEN, selling you the toxic junk. To think many of them are holding the stocks long-term. What a joke. It’s also difficult to analyse the tech behind, esp for biotech, whether they are truly game-changing or some airy fairy crap.

Yes, agree with this. This will be a rough year from a macro perspective.

I have never bought online stuff on Shopee as If find the gui and searches are hard, I bought most of my stuffs on Lazada if not Qoo10. In this article context, if I die die must invest big ecommerce Tech, Baba is better bet for me, not SEA, not Tencent, not JD or PDD, simply because the downward risk is lower and the potential upside is greater, besides most of its segment are already profitable 🙂

Interesting – appreciate the sharing. 🙂

I happened to travel the United States during the Grab IPO. The tenor of American CNBC window that evening was something along the line of “The next company from South East Asia which has yet to prove any business model to work and which is here for stupid American money”.

What goes for Grab does for Shopee as well. The marketing portion in their P&L is insane and it’s lesson 101 for the South East Asian founder to just “buy” GMV by heavily subsidizing sales to attract additional investments. I really struggle to see how they plan to turn this around now that investors have been rattled and Baba is having deep pockets to sit this out in SEA.

Hard pass for me unfortunately.

Really interesting comment, thanks for sharing.