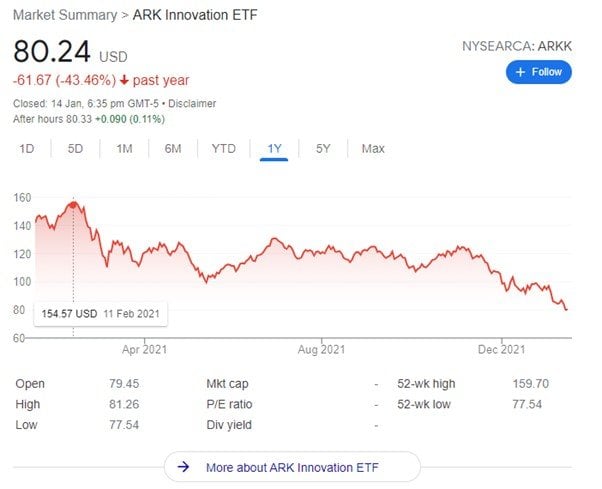

About a year ago, I wrote a macro article where I suggested that Cathie Wood’s ARKK would become a big problem on the way down.

I got a lot of hate for it back then.

But fast forward a year, and ARK is now down 50% from highs.

So here’s another macro prediction for 2022.

I think 2022 is going to be the most adverse macro environment for stocks since 2018. And I think risk assets generally are going to be in a world of pain this year.

For the record, this was what 2018 looked like for the S&P500. It basically went nowhere for a year, and finished it off with a massive decline.

What is my (or everyone’s) base case?

My base case for 2022, is that:

Q1 2022

By and large, things should still remain orderly in Q1. Growth is decent, inflation is rising, and Quantitative Easing (QE) is still in play.

Q2 and Q3 2022

Where things start to get rocky.

I think Q2 onwards growth will start to slow, inflation will start to slow.

Right as the Feds switch into rate hikes and Quantitative Tightening (QT).

Which is going to be a very dangerous mix for risk assets as we head into the middle of the year.

In 2018 terms, I think we’re somewhere in mid-2018. Things can still go okay for a while more, but a big move (to the downside) lies somewhere in the future.

Let me explain why I think this way, and where I could be wrong.

Inflation is a political issue – Powell was renominated to fight Inflation

Now inflation hits the poor harder than the rich.

When you spend 80% of your income on food, rent and gas, you’ll notice when prices go up.

So inflation is deeply unpopular, and Biden’s latest approval rating has plunged to 33% in the latest poll.

With the midterm elections coming up in Nov 2020, this is a big problem.

It’s quite clear now that Powell was renominated to fight inflation – he literally said inflation is no longer “transitory” a week after his renomination.

To recap what he’s done since:

- QE to end by March 2022

- Market pricing in 3.5 rate hikes by Dec 2022

- Quantitative Tightening to start shortly after first hike – at a much faster pace than before (2018 max was $50 billion a month)

The USD is the reserve currency of the world.

If the US needs to raise interest rates to keep the US voter happy, it’s going to have implications on global asset prices whether you like it or not.

What would stop rate hikes?

The way I see it, there’s only 3 scenarios where Powell will stop the rate hikes:

- Inflation goes away

- Voters stop caring about inflation

- Markets break

Inflation goes away

The problem with inflation is that much of it is supply driven.

Omicron is causing supply chain disruptions around the world, which will not go away just because you tighten monetary policy.

All the Feds can do is to raise rates and hope that demand for goods will drop.

And the problem then is that it takes some time for monetary policy to kick in, about 6 – 12 months on average.

So if the Feds hike today, we only see the impact on demand in Q3 – Q4.

Because of that, it’s hard to see inflation (as measured by core PCE that the Fed tracks) going down significantly before the later parts of this year.

Which means Powell will keep on hiking.

Voters stop caring about inflation (or elections are over)

I don’t think the voters are going to stop caring about inflation any time soon.

You can argue this will no longer be an issue after the midterm elections in Nov 2022.

Maybe, but that still leaves us from now till Nov 2022, which is a long way to go.

Markets break

Either:

- S&P500 drops 20 – 30%, or

- Treasury markets stop functioning properly (like late 2019 or March 2020)

Every time the Feds take the markets off QE, something usually breaks.

The markets are like a drug addict these days, no longer able to function properly without monetary stimulus.

In 2019 it was the repo crisis, in March 2020 the treasury markets stopped functioning.

If something breaks again, I think the Feds will be forced to reverse course, just like they did in Dec 2018.

In fact I think this is the most likely outcome of the rate hikes.

So FH… you’re telling me the Feds are going to hike until the markets break

Pretty much, essentially.

The Feds will tighten monetary policy until (1) inflation goes away or (2) markets break.

Inflation (measured via core PCE which the Feds look at) is unlikely to budge in the short term.

Which means that the Feds are basically going to hike until the markets break.

What is the opportunity cost if I am wrong?

There are 2 ways a stock price can go up: (1) earnings growth, (2) multiples expansion.

For those familiar with Price to Earnings, (1) is the E going up, (2) is the P/E going up.

In a year when the Feds are tightening monetary policy, it’s hard to see multiples expansion, so (2) is out.

Which leaves earnings growth.

And my personal view is that earnings growth will peak in Q1 2022 because:

- Rising inflation is hitting profit margins due to higher costs

- 2021 is a strong year for earnings which makes the year on year comparisons hard to beat

- Fiscal stimulus and credit growth peaked in 2021, which will hit the economy in 2022

So even if I am wrong and the economy is strong enough to take the rate hikes, I frankly don’t see stocks going up all that much this year because of (1) limited multiples expansion and (2) muted earnings growth.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Just created a Discord server where I collate analyst reports and investing resources that I come across in my research. Hit us up here if you’re keen.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Could I be wrong?

Let’s stress test with some counterarguments:

- Feds will chicken out before they hike

- Same thing happened in early 2021, but nothing happened

- Already priced in – market is now anticipating rate cuts

- Economy is strong enough to absorb the hikes

Feds will chicken out before they hike

This one I plain disagree.

If you read Powell’s latest speeches, it’s quite clear that he is serious about fighting inflation this year. A lot of Fed members have come out to say the same as well.

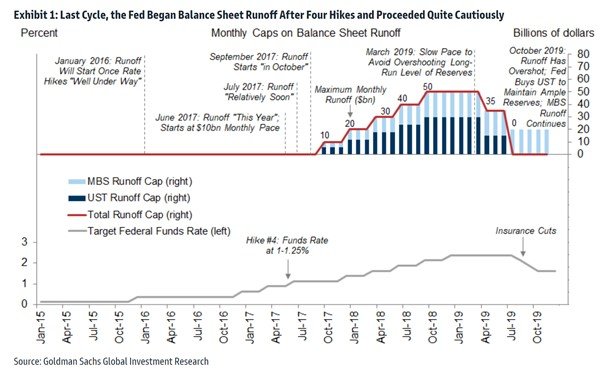

In fact the latest minutes suggest that the Feds are looking at quantitative tightening (balance sheet run off) quite soon after the first rate hike, and at a significantly higher pace than in 2018.

Quantitative tightening is big news because it’s literally the opposite of Quantitative easing. With QE you’re pumping money into the system. With QT you’re taking money out of the system. It’s a deflationary event.

In 2018 the highest pace we ever got was $50 billion of QT each month. Bigger than that is quite a scary thought.

So I actually think that investors may be surprised by how quick QT could run this year.

It makes sense too – if the Feds are going to hike 4 times this year, they need to implement QT to bring the long end up, to prevent yield curve inversion.

Same thing happened in early 2021, but nothing happened

Remember when the market was freaking out over rising rates in 2021?

And then absolutely nothing happened after that?

Well, I think the key difference this year is that (1) the Feds are actually going to hike, and (2) corporate earnings are starting to peak.

Whereas in 2021 you had very strong earnings growth, and a very supportive Fed.

So yeah… I think this year is different.

Economy is strong enough to absorb the hikes / Already priced in – market is now anticipating rate cuts

This is probably the most convincing argument.

That after the huge plunge in growth stocks the past 2 months, rate hikes are already priced in at this point. And that the economy is strong enough to absorb the rate hikes.

And I agree this is possible.

What I would say though, is that in this scenario, where is the upside going to come from?

If the market never crashes, the Feds have no reason to stop hiking.

And if the Feds don’t stop hiking, how are stocks going to go up materially from here?

Without multiple expansion, it’s just earnings growth.

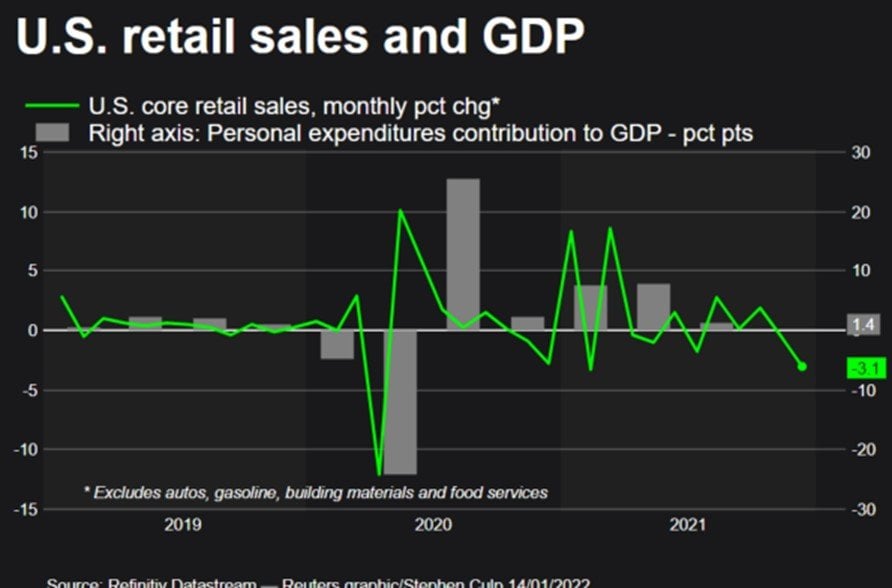

How much can earnings grow in a climate with inflation pressuring costs, and the Feds hiking 4 times in a year?

High frequency indicators are already starting to show weakness, here’s US retail sales:

So I definitely could be wrong here. But at least if I am wrong, the opportunity cost should not be massive.

How am I positioning?

For my personal portfolio, I’ve already started taking profits in some positions late last year.

Those I continue to hold today are mostly positions I want to hold long term.

That said if we get any strong rallies into late Q1 or early Q2 I may use the opportunity to derisk further.

I’ve also significantly dialled back on my rate of purchases since Q3 2021 (as shared here).

This has increased my dry powder quite significantly, that I will likely deploy in 2022.

What will I buy in 2022?

Like I shared in a previous article, I plan to be buying REITs heavily this year on any interest rate sell-off.

Long term secular growth tech positions will be a good buy at some point too.

At some point in 2022, I will also take profit in my DBS and UOB positions.

I’m up 60-70% on them, and I don’t think high interest rates will last forever.

For those who are keen, you can view my full personal portfolio and stock watch, with weekly updates on my trades on Patreon.

When to buy? Better late than early?

The key event to me is when Powell decides to pivot away from hawkish monetary policy.

That’s probably the time I buy interest rate sensitive stocks like REITs and tech, and sell my banks.

And this time around, I would much rather be late than early.

Sure I may not buy the bottom, but at least I don’t catch a falling knife.

Because of how big markets are, if Powell changes his mind it’s not like the S&P500 will jump 20% overnight anyway.

Remember – stocks take the stairs up, and the elevator down.

There will be time to buy on the way up.

Do support FH on Patreon for more in depth and timely positioning updates.

Closing Thoughts: Everyone has a plan… until they get punched in the mouth

So there you have it. My high level game plan for 2022.

But much as we can plan and theorycraft, it would be wise not to forget the eternal words of Mike Tyson:

I think this is going to be one of those years.

While we still need to plan, it will also be wise to keep a close eye on how the markets play out, and how Powell responds.

Flexibility, and being quick to respond, might just be the name of the game this year.

I know not everybody wants to run such an active portfolio.

If you’re one of those, I would say tilt towards value stocks / FAANG style stocks, which should be less volatile in 2022. And watch your risk exposure to ensure that you can sit through a 20% drawdown.

I do want to caveat that this discussion above is looking at the indexes broadly.

Some sectors like banks or oil or FAANG could still continue to do well despite a declining broader environment.

Individual stocks can still continue to outperform too if the company executes well.

Love to hear what you think though! How are you positioning for 2022?

As always, this article is written on 15 Jan 2022 and will not be updated going forward. Latest thoughts (and my stock watch and personal portfolio) are available on Patron.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Looking for a low cost broker to buy US, China or Singapore stocks?

Get 1 free Apple share (worth $230) you’re new to MooMoo and fund $2700.

Get a Free Apple stock (worth S$230) when you open a new account with Tiger Brokers and fund $2000.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

Hello,

I like the way short and concise way you present the macro view and the plan.

By the way, do you mean FED tracks inflation via core PCE and not CPE (typo here?)

Thanks for the kind words! Yes typo sorry I meant PCE. 🙂

what about a bullish scenario of the market finally looking past covid with omicron leading to an endemic situation? That might provide a boost to market sentiment and consumer spending overall? love to hear your thoughts

Actually my base case is Omicron leading to an endemic situation, at least in the west.

However I see that as a bearish scenario because it will boost demand short term, at a time when supply cannot keep up, worsening inflation. That would hasten the need for tighter monetary policy to combat inflation.

This is just short term, 6 – 12 months timeframe though. If you zoom out and take a longer term perspective, it will all flow back to demographics and secular trends, which are disinflationary.

Nicely put, its also my roadmap for next year. Quick thoughts:

– I get a bit worried when everyone starts saying the same thing:

https://www.youtube.com/watch?v=Ffth8bSweIs

https://twitter.com/Hedgeye_Staples/status/1482028468896505856?cxt=HHwWgIC9ucrCnJEpAAAA

– Long term (3-5 years), cash is a melting ice-cube. Its tricky, waiting for a correction.

– Paper gold helps hedge a market correction, but not a liquidity event (“something breaks”).

– I think there’s a lot of leverage to be unwound, a correction can become a crash.

– Think we get a wild and inflationary boom after the 2Q correction, thinking abt what to buy for it during the correction.

Yes actually I agree with your points.

It troubles me that everyone is calling for a crash when the hikes start, and make me wonder whether the contrarian sign is to buy now.

Agree that long term, cash is probably the worst asset to be holding because of fiat depreciation, which frankly is likely to be the only way out of this debt crisis. I dont think markets can be allowed to go down for long, so if there is indeed a correction, I would be deploying cash heavily into all kinds of risk assets, from REITs to stocks to commodity plays etc.

Yep, maybe we get a melt up in the indexes to kill the bears, before the correction.

Can’t predict the markets too much, can just position ourselves so we are comfortable no matter what happens. 🙂

Yep agreed. Which is why despite what I think, I am still somewhat fully invested at this point.

Hi FH,

I noticed for the past three years, you have been making prediction that stock market would crash like no tomorrow. But now US stock markets are now at record high. To be frank, nobody can predict the future. Nowadays, there are too many smart monies around.

Regards,

Gerald

https://sgwealthbuilder.com

Haha I understand where you’re coming from.

To clarify, these macro pieces are intended as a short term (6 – 12 month) timing tool. So in Jan 2020 we called the COVID crash, and in 2021 (okay we were a bit early) we called the high beta stock / ARKK crash.

From portfolio positioning perspective, if you can avoid a drawdown, and buy back in near the bottom, that can really supercharge returns. I know not everyone wants to (or believes) this is possible, and if you’re one of those then just DCA in every month.

If you look under the surface, a lot of US stocks are more than 50% below all time highs. Using the indexes only tells half the picture because of how heavily FAANG features in there.

That said, if you take a longer term perspective, then I absolutely agree that crash is trash. Longer term the markets cannot be allowed to go down because it will break the western financial system as we know it, so the only way is to engineer markets to go up, at the cost of depreciating fiat.

TLDR – Stonks only go up (in the longer term).

Why not just overweight your portfolio heavily into banks (the regular NIM ones), and rotate back into tech only when the Fed turns dovish again? Sure banks are definitely pricey now, but there’s still a long way to go with rate hikes expected for 2022 and continuing into 2023.

If you go back and look at the charts from 2018, you’ll find that DBS and UOB peaked in May 2018, a whole 6 – 7 months before Powell finally reversed course in Dec 2018.

My fear is that something similar happens here, where the long end of the curve peaks way before the Powell pivot.

Even if I am wrong, the possibility of this would probably hold me back from adding heavily into banks at this point in the cycle. If anything, I would be looking to take profit in bank positions going forward.

Could be wrong though, but with DBS at 1.6x book value, how much upside is left on the table? 10-20% move from here, tops?

Fair points, but I just can’t find anything other than financials to add to right now, even with limited upside. The alternative is to risk making losses or just going ssideways with other sectors.

The blue chip REITs look good at this price frankly, for long term holdings. The only question is whether to buy now or to be greedy and try to wait for a better price. The choice kinda goes back to risk appetite and existing positioning.

The counter intuitive thing to do would be to buy bank stocks on pending interest rate hikes.

Because when the hike comes, bank stocks, like every other stock, will drop.

With banks gaining >50% since 2020, it makes a lot of sense to take profit.

You mean sell right? And yes, I am inclined to agree. Will be looking to sell banks sooner rather than later.

Stagflation could be coming. Inflation is partly due to supply chain issues, not only too much money. A lot of labor shortages… rate hike wont solve inflation and may even lead to recession if not carefully handled. I have no confidence in the govt as they are grossly incompetent. I am selling out of my stocks and holding 50% cash and overweight china. Valuations still very high after recent crash. The indexes no longer represents the real economy. Main street is detached from Wall st. There are 2 extreme sides : one represented by the faang and elites and the other by the poor and jobless. Long-term wise not looking good. There is also great resignation. If recession really comes, they gonna print more money again which drives up debt. Although china might be affected as exports to Us could be affected as well. Dont know why people so optimistic about us and so pessimistic about china. I’m the other way round lol. It’s very obvious who does a better job at running the economy

https://www.nbcnews.com/business/business-news/why-store-shelves-are-empty-omicron-bad-weather-hurt-supply-chain-rcna11859

Stagflation could be coming. Inflation is partly due to supply chain issues, not only too much money. A lot of labor shortages… rate hike wont solve inflation and may even lead to recession if not carefully handled. I have no confidence in the govt as they are grossly incompetent. I am selling out of my stocks and holding 50% cash and overweight china. Valuations still very high after recent crash. The indexes no longer represents the real economy. Main street is detached from Wall st. There are 2 extreme sides : one represented by the faang and elites and the other by the poor and jobless. Long-term wise not looking good. There is also great resignation. If recession really comes, they gonna print more money again which drives up debt. Although china might be affected as exports to Us could be affected as well. Dont know why people so optimistic about us and so pessimistic about china. I’m the other way round lol. It’s very obvious who does a better job at running the economy

https://www.nbcnews.com/business/business-news/why-store-shelves-are-empty-omicron-bad-weather-hurt-supply-chain-rcna11859

I suppose the counterargument is that governments cannot allow stocks to fall for an extended period, because the entire western financial system will collapse. So holding cash is ok from a tactical positioning perspective, but at a certain point that cash will still have to be deployed.

Can you expand on the point that “if stocks fall for an extended period, the entire western financial system will collapse”? Is it because the money for retirement is invested in stock market?

Well it’s because of how much wealth is tied up in financial assets, and how western investors (or rather the world) is so leveraged long that a collapse in financial assets/rise in interest rates will bankrupt many corporations or even countries. Politicians are motivated to stay in power, so if the choice comes to having a Great Depression 2.0 or printing money to solve the problem, they will pick the latter. The inevitable result is that financial assets will need to be kept elevated, and that is likely to come at the cost of inflation/fiat depreciation.

Well to save the markets, they have to print more money or reverse rate hike. No other way out? If print more $ then it worsens the inflation which defeats rate hike. If reverse rate hike then inflation wont go away. Either way they are doomed? I really dont see a solution here. If a new covid variant comes after omicron then labor shortage will persist. No end to it. Inflation may persist for a very long time. If they risk a recession then market surely crash. Therefore i think holding a large warchest is better at this point rather than risking it in the stocks market. I am fairly confident the situation is getting very tricky now. And the market has not priced in yet. Just like the unexpected mar 2020 crash. Investors are still complacent thinking rate hike will just solve inflation magically. Problem is the govt only has 2 tools: print money and adjust rates. And they are out of other options. Wonder if china market can still go lower

Every and any move they make will certainly make their financial health worse. Like seriously. Think about it. Esp now with all sorts of bubbles in place: crypto, stock, inflation, housing, etc. A major crash will burst all bubbles which will be very ugly. The end is nigh…

Well, if the crash is bad enough, it will feed back into lower demand, and solve the inflation problem. And then the Feds will be forced to respond with easy monetary policy again. 😉

Yes broadly agree with this, in terms of the choices available to the Fed right now. They are boxed in, and it’s about picking the least bad outcome.

Wait , how does a crash lead to lower demand of basic goods which are the concerns of inflation? People still need to consume basic goods even in recession? So you are saying they will print more money or reduce rates in the event of recession or market crash? Wouldnt that lead to more inflation which they are trying to solve in the first place?? Dont understand what you are trying to say. My conclusion is they are doomed , is right?

In a crash the discretionary demand should taper off because of perceived wealth effects (people feel poorer because of their wealth in stocks), which should help the inflation problem. 🙂

It will not be even though, so different sectors may be impacted differently.

Oh my oh my, so they will keep printing more $ to keep the financial system afloat?? And let the bubble get bigger and more insane… . Lets hope this system wont collapse in our lifetimes… I fear for our future generations….

Yes, pretty much! Ie. Cash is trash (in the longer term, and outside of short term tactical positioning)!

Dear FH

Thanks once again for your insight

I agree with you but I think the fed will be cautious with their hikes and pause to see impact each time. The market has priced in mostly the three hikes but not the fourth one or the unlikely possibility of a ‘shock and awe’ 50 basis point hike at one go.

You are right regarding our banks . DBS at 38/40, UOB at 32/34 will get over stretched and possibly are a partial sell to book profits

OCBC is still not taking off despite their high CET ratio- the market is not happy with the lower payouts but more importantly apprehensive of new acquisitions, especially in greater China, following the new CEO takeover

The SG REITS are good buys at each dip and my strategy would be to gently add good names but slowly and steadily at prices offering at least some margin of safety

Although tech might get hit, I will still use the sectoral ETF route in the US to add on to mega cap techs, financials and energy

Finally, if interest rates go higher and utilities pullback, as they will do, I will be adding selectively in the UK and US as well. The downside is the dividend withholding tax though- do prefer the UK utilities like NG UU SSE SVT PNN

Finally, I am fairly certain that the upside to the sg market is capped and the index might struggle at 3400. I will exit ES3 and redeploy in the well run REITS, those proceeds

Regards

Garudadri

Pretty sure 3 or 4 hikes wont be enough as this inflation is not purely caused by money supply. So he may even need to hike more which will shock the markets. Of course the elites wont want him to hike so much as they dont care about inflation. But who really knows what will happen? Things often spiral out of control very quickly. For some reason i feel more comfortable with china dealing with property bubble vs the fed dealing with inflation. One is competent while the other is not. Stonks go up only holds true when the fundamental economy is well and there are massive stimulus, we may be at a time when we can no longer blindly believe in this folklore. From dotcom bubble burst in 2000 to 2008, the SnP index didnt break previous high. From 2008 til now, it broke all highs due to QE infinity. So stonks go up doesnt hold true in all time periods. Take care. I feel like people have too much faith in the govt saving the markets but truth is they are running out of options … things dont look good beneath the surface

HI Garudadri,

Thanks again for the great sharing.

Agree that the market has priced in 3.5 hikes at this point, with the 2 year treasury at 0.9+. That said, while the Feds will be cautious, they are responding to inflation this time around. So if the S&P500 falls 10% but inflation is still running hot, I don’t really see them holding off on the next hike. Quite a different paradigm from the past few rounds of QE.

Agree on REITs + ETFs investment. Similar strategy for me.

Utilities I dont follow the western utilities closely, but Netlink is one that I’ve traded in and out of the past few years. If we get a decent enough pullback I will add to it.

On STI, I have been doing the same myself. Taking profit in a couple of the blue chips and redeploying into the blue chip REITs. 🙂

Cheers,

FH

Since inflation is caused by supply disruptions due to covid and labor shortage “great resignation” ( you left this out), rate hike may not solve this problem. So he will keep hiking til market breaks, and then what happens? Will he reverse or continue hiking? Why did Michael Blurry sold all his stocks? Do you sense something amiss? There are also reports that insiders at faang are cashing out. I think there is a great deal of uncertainty and risks going forward. Stagflation could be possible. The real economy is not doing so well despite the media saying so. Only the financial and big tech are well.

Hi FH,

I agree that a significant correction will come, either this year or next.

One question for you. If you have a significant war chest which you don’t want to risk, where would you keep it for 1-2 years?

Thanks

Hi CMC,

Good question. Personally mine is a mix of SSB/CPF-OA. But for new funds, I am having the exact same problem. Tried some money market funds but performance is really poor.

I am mostly just keeping them in cash in high yield savings account, yielding no more than 1% on average.

That said, I think we will see volatility this year that will allow me to deploy some of the warchest.

Nice analysis! Keep the good work up!

Thanks! Glad it’s useful!

“With the midterm elections coming up in Nov 2020, this is a big problem.”

I think you meant Nov 2022.

Similar sentiments here, I hold all three banks and see them gain new highs every other day. I’m not too sure when to sell them though. Otherwise I’m bullish on China Tech this year. Hopefully we see some upward movements.

Yes sorry I meant 2022.

Similar views on the banks. China it’s hard to say whether this is the year they will recover, but definitely they’re ahead of the curve as compared to US growth tech.

Hi FH, good post. All eyes on the curve 😉

Yes! Indeed! We might get a short pullback in rates, but rest of 2022 will be very interesting.

Very timely piece. Now with the negative wealth effect, the chance of demand for goods falling may have increased.

Yes, the whole point of tighter monetary policy is to hit the demand side, and bring down inflation long enough for supply side to catch up.

That’s the theory at least. Trying to get the balance right is going to be devilishly hard.

Perhaps time for another ‘where I’d invest 100k now’ article? Would you this time consider just holding much of it in cash for the short term and buy later in the year on a dip?

Good idea – will look into doing one. 🙂