I’ve been getting a lot of questions about whether to sell stocks / REITs recently.

And I get it.

The media is going on about how rising interest rates will trigger a global recession.

Markets are collapsing day after day.

What’s an investor to do in times like that.

Do you sell your stocks and hope to buy back later?

Or do you keep holding even though a global recession is likely coming?

Now I don’t profess to be right about this. But I wanted to share some of my views – and hopefully it would help you in your decision making process.

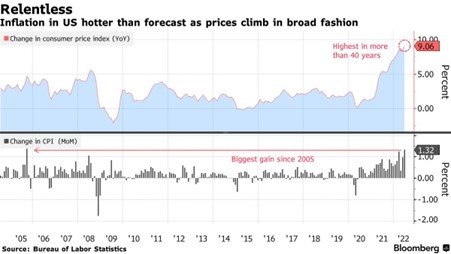

US Inflation is very hot

US inflation numbers for June just came out – and they are very hot.

We’re talking about the highest inflation in 40 years, that shows no signs of slowing down.

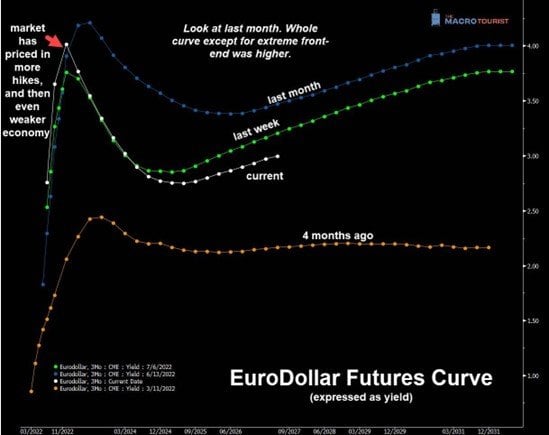

Market Pricing in Faster Rate Hikes… And Faster Cuts

The market thinks that because inflation is so sticky, the Feds will have to hike faster in response… which will crash the economy.

The market now sees a very fast hiking cycle that takes us to 3.75% – 4.0% by end of 2022.

With rate cuts to begin in early 2023.

What if the market is wrong?

Let me put it out there that I’m not the biggest fan of Bill Ackman.

But I was reading one of his tweets recently, and I must say it was a good one.

![]()

The long and short – is that Bill thinks the market is wrong.

The market sees a fast and furious hike, followed by cuts in early 2023.

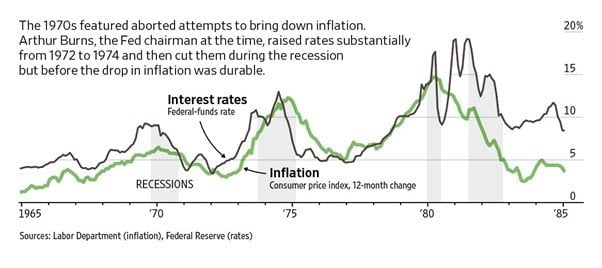

Bill on the other hand – thinks that interest rates will go up, and they will stay up for most of 2023.

He thinks that the Feds will have to do this to avoid the mistake of the 1970s when they cut interest rates too early and created a decade of inflation.

A mistake the Feds are well aware of.

Why does this matter?

Let me explain why this matters.

If you think the market is right and interest rate cuts are coming in early 2023 – then we are probably nearing the later stages of the market decline.

In which case it may not make sense to sell, and you might want to consider looking to buy soon.

If you think Bill is right and interest rates are staying high for 2023 – then well, a lot more pain lies ahead.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great nuggets of wisdom on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

What is my view?

For the record, I actually agree with Bill on this one.

I think the economy may prove surprisingly strong, and be able to withstand the higher interest rate longer than the market is pricing in.

Because of that, I think the market may be mispricing recession risk here.

For 2 reasons:

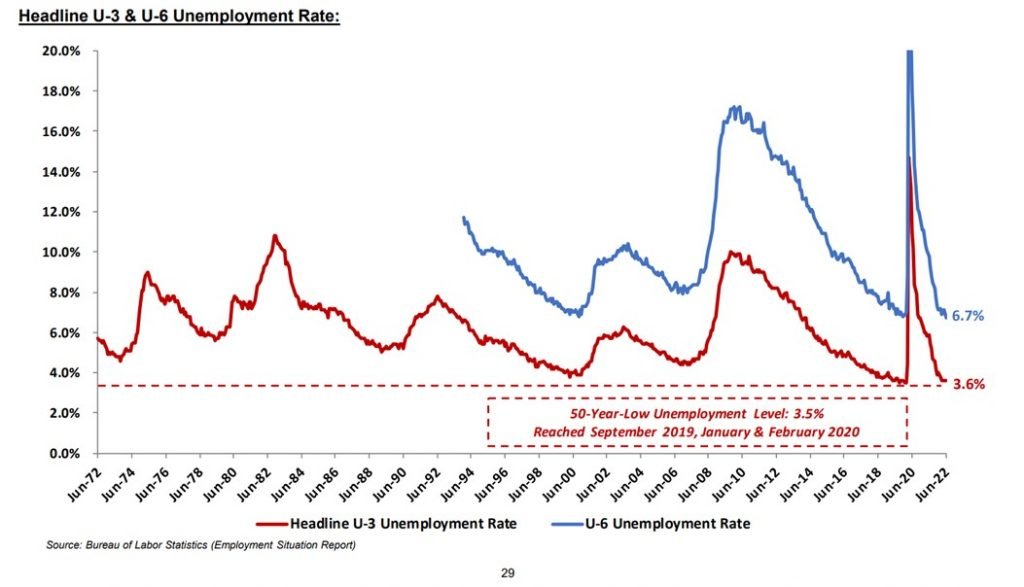

- Labour market is still very strong

- Household savings are very strong

Labour market is still very strong

For some reason, global labour is incredibly tight.

Ask any business owner out there, and they’ll share with you how hard it is to hire workers these days.

It kind of puzzles me where all the workers went after COVID.

But as things stand, the labour market is incredibly tight.

And wage growth is very strong.

Until wage growth numbers start to tick down and labour starts to weaken – I frankly do not see a recession.

It will come though, because that’s exactly what the Feds want to achieve.

But the question is one of timing.

Household savings are very strong

At the same time – household savings are very strong.

Households are sitting on a lot of cash, and this will allow them to withstand the higher interest rates.

So FH… I just want to know whether to sell stocks…

To answer this question, I think a bit of nuance is required.

What type of stocks?

We need to differentiate between different kinds of stocks, because they will respond differently to the macro climate:

- Real Economy Stocks (Inflation Hedges / Cyclicals) – Oil, Commodities, Gold, Industrials etc

- Tech Dream Stocks (Interest Rate Sensitive Stocks) – Non-profitable tech, Crypto, Treasuries etc

Real Economy Stocks

Real Economy Stocks have been crushed of late.

The market has started to price in a full recession.

Here’s the performance of commodities.

Crude oil is back to prices from before the Ukraine war, which is pretty crazy when you think about it.

Which opens up interesting opportunities.

If you think the economy will be stronger than expected.

Then it doesn’t make sense to sell here, and there could even be an opportunity to add.

But if you think the economy will roll over like what the market is pricing in, then yeah prices are probably going to collapse.

Tech Dream Stocks

With Tech Dream Stocks the analysis is more straightforward.

These guys respond to interest rates.

When interest rates go up, they perform poorly.

And interest rates are going up a lot in the next 6 months.

Simple right?

But… rate cuts?

You can argue that if we are going to get interest rate cuts in early 2023, then you’ll probably want to start adding in the next 3 – 6 months.

Sure that’s possible, but like I said, my personal view is that interest rates will not be cut as fast as the market is expecting.

The only reason why it will be cut so fast is if (a) stocks collapse or (b) financial conditions tighten dramatically.

And in both scenarios – that implies further downside for stocks.

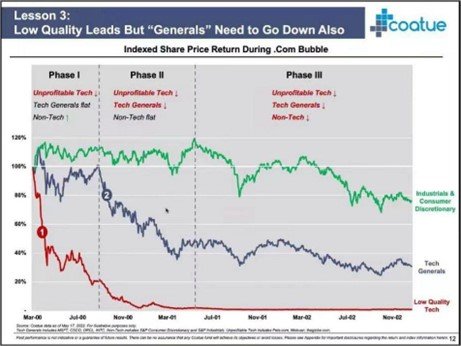

Dot Com Bubble

Here’s how the Dot Com bubble played out.

First unprofitable tech got crushed.

Then Tech Generals (which would be today’s FAANG).

Then the broader market.

I leave you to decide where we are now in the cycle.

How do I see the next 12 – 18 months playing out?

I wrote a Patreon article this week where I shared my framework for the next 12 – 18 months.

Without giving too much away, I think the mid term outlook (2 years out) will be inflationary.

Which means that at some point in time, you will need the exposure to risk assets to hedge inflation.

I’ve been banging on and on about this point for ages.

Here’s an excerpt from the article:

The End Game for the Fed (1 – 2 years)

The short term dilemma for the Federal Reserve can be summed up as follows.

If they cut interest rates too early, inflation comes roaring back.

If they cut interest rates too late, economic growth will be devastated (recession).

My personal view – is that the Feds are going to try to achieve both outcomes – low inflation with strong economic growth.

But at some point in the next 6 – 12 months, it will become clear that will not be possible.

And I think at that point, the Feds will switch to a middle ground approach.

They will give up on their goal of bringing inflation back to their 2% target.

But they will also give up on their goal on real GDP growth.

In other words – they will accept higher inflation, with slower growth.

A stagflationary style outcome if you like.

Short Term Outlook

For the record though – I agree that at some point in 2022/2023 a recession will come.

Because that is what the Feds are gunning for.

They will hike interest rates until they achieve their goal – which is to crush demand.

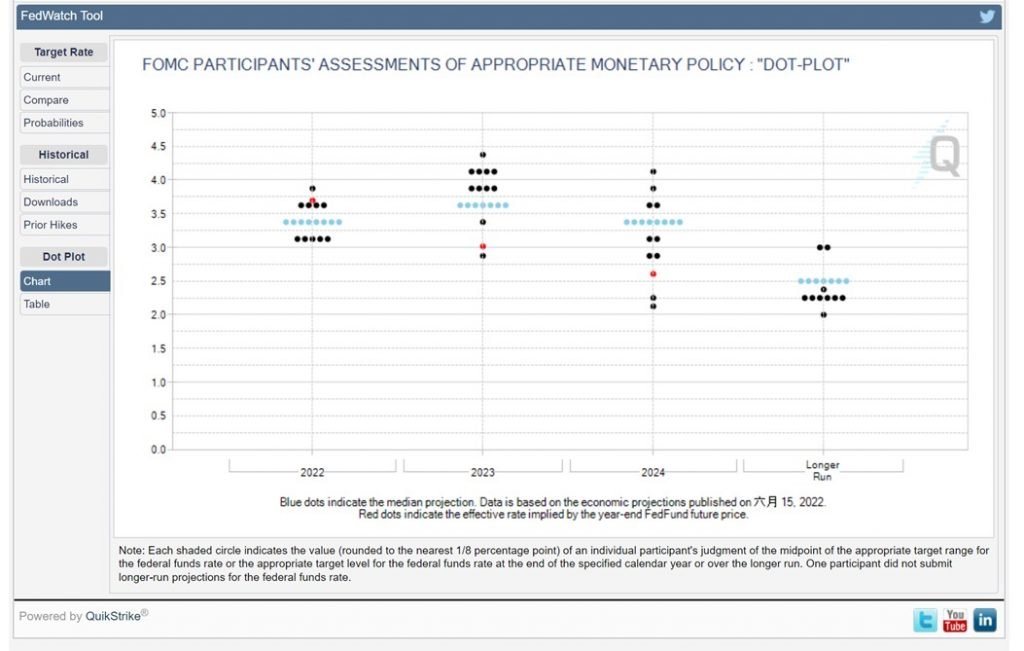

For the record – Fed Dot Plot lines up with Bill’s thesis. Interest rates peak at about 4%, and stay there for 2023:

Am I selling my stocks?

For me the decision is simple.

As shared in late 2021 and early 2022 – I made my portfolio adjustments back then.

Most of the positions I wanted to sell, or which I am not comfortable holding long term, I had exited by early 2022.

The positions that I have left, are core positions I am comfortable to hold long term.

Even through the recession.

What if I am wrong?

My cash allocations are at record highs.

I don’t think I’ve ever held this much cash as a % of my net worth ever, even in Jan 2020.

So I have plenty of dry powder to buy into markets.

I think that’s what cash does for you in this market.

It gives you optionality, in case you are wrong.

Opportunities have started to emerge…

But – and I think this is key, I will want to deploy that cash.

Play it too cautious and stay in cash too long, and you get eroded away by inflation in the mid term.

I think opportunities have emerged in this market.

The bearish sentiment out there is pretty unbelievable.

I get retail investors asking me about a recession like it’s a sure thing. That usually brings opportunity.

There are opportunities on the short side, and opportunities on the long side.

It’s one of the target richest environments in a while. The market is literally throwing opportunities at you.

I will refreshing my personal stock / REIT watchlist this weekend with this in mind. You can sign up for Patreon to have a look once it’s out.

I also update what I’m buying or selling, and my full portfolio on Patreon.

Should you Sell Stocks / REITs before the 2023 Recession? (as a Singapore investor)

But every investor is different.

The decision whether to sell has to be made on individual risk appetite.

It really goes back to whether you can stomach the risk.

Think about how you would feel if your stocks dropped another 30% from here.

If that makes you sick to the stomach, then you probably took on too much risk and need to close some positions.

Whereas if you don’t mind keeping the money locked up for the next few years, then maybe you can continue to hold.

Easy days of investing are over?

Now I know that this article doesn’t have an easy answer.

And in some ways I think that is by design.

The days of easy liquidity and cheap money are quite clearly over.

We lived in a 40 year period where the solution to every economic problem was to cut interest rates.

Well, going forward, you can no longer cut interest rates without implications for inflation (and FX).

A story about the French…

After the horrors of WWI – the French built the Maginot line to defend against a future German invasion.

It was designed for trench warfare.

A real beauty it was, a great line of fortifications.

If there were a repeat of WWI, the German army would never be able to cross the Maginot line.

Well as history would have it, the Germans came up with the Blitzkrieg – fast moving tanks with air support that relegated trench warfare to the annals of history.

That they deployed to devastating effect in WWII.

As for the Maginot line?

The German war machine drove around it – via Belgium.

Don’t invest like it’s 2012 – Be careful with fighting yesterday’s wars

What I’m trying to say here is – be careful fighting yesterday’s wars.

The investing paradigm for this decade, is going to be very different from last decade.

It’s no longer about just buying a broad index to capture Fed fuelled liquidity returns.

Volatility and performance across asset classes may differ quite a bit.

Which requires a very different approach to investing.

Will the FAANG perform as well this decade? Does tech outperform vs Energy/Financials?

As to whether to sell stocks – It really depends on what stock it is. What is your holding period. And what is your risk appetite. And how good you are at reading macro signals (so that you know when to buy back).

There are no easy answers here.

Closing Thoughts: What about REITs or Real Estate?

A couple of you have also asked whether real estate / REITs will do well in a higher interest rate / higher inflation climate.

It’s a tricky question.

Rising interest rates are really bad for REITs and real estate. Financing cost goes up, and cap rates get compressed.

But on the other hand – if inflation is due to depreciation of fiat currency, real estate as a hard asset can hedge against inflation.

How did real estate perform in the 1970s?

To answer this question, I took a look at how real estate performed in the US in the 1970s, the most recent period where inflation was a problem.

And the answer – is that performance was very uneven.

By and large the real estate asset class tracked inflation.

But – it was heavily affected by local demand / supply dynamics.

Real estate in some places did very well. Horrendously in others.

That offers valuable lessons for real estate / REITs this decade.

If you’re expecting the broad returns we saw the past decade, I say keep dreaming. Without the tailwind of zero interest rates, it’s hard to see similar performance for this asset class.

But on the other hand, I think that if you’re careful about picking the right real estate in the right locations, and you’re realistic about the inflation adjusted returns – then real estate can still hold its own against inflation very well.

Refinancing your mortgage

With rapidly rising interest rates – it might pay off to look into refinancing if your loan is coming due.

I know a lot of you have been writing in for my views on fixed vs floating loans, and I plan to write a full article for this.

But in this market – I think you’re pretty much forced into taking floating. The banks themselves know interest rates are going up quick, so the fixed rate loans are priced in such a way that they aren’t sufficiently attractive (in my view).

In the meantime, there’s a fantastic tool by Property Guru.

Do give it a try if you’re close to refinancing.

It’s completely free – you just input your mortgage details, and the tool lets you know whether you’ll save money by refinancing.

If the answer is yes, they’ll give you recommendations on what loan to take.

If the answer is no, you can set up a reminder for the tool to remind you when its time to refinance.

I set up the reminders for my own properties just this week and it’s pretty neat.

Do give it a try here.

As always, this article is written on 15 July 2022 and will not be updated going forward.

If you are keen, my full REIT and stock watchlist (with price targets) is available on Patreon. You can access my full personal portfolio to check out how I am positioned for the coming downturn too.

Looking for a low cost broker to buy US, China or Singapore stocks?

My recommendations on Stock Brokers here.

Get 120 USD in Microsoft Shares with Webull, a zero commission broker.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

FYI – We just launched the FH Property Series. Everything you need to know to buy a property in Singapore, completely free of charge.

Hi FH,

Would you consider DCA-ing BRK.B over an S&P 500 ETF going forward in view of it’s greater value leaning?

Thanks!

That’s an interesting question. Personally I dont DCA as I am a bit more active in my timings.

If I were to DCA though, I think I would not get too cute – I would just go pure passive. So probably S&P500 or an all world index.

I think one either tries to active invest (and go all out), or one just goes pure passive and does not try to outperform the index.

Hello FH,

How do u think semiconductor companies( like TSMC and AMD) will perform in 2022 and 2023?

Yeah that’s a really tricky question, and I will be writing a Patron article on this.

On one hand you have the dynamics I described in this article – where the economy may prove more resilient than what the market is pricing in.

On the other hand, the Feds are almost bound to hike us into a recession.

So the question will have to go back to what is priced into the individual stock + what is your timeframe. Because if you are looking to hold for 6 months vs 1-2 years, answer could be very different.

Good and comprehensive article.

I agree with you on the high household savings and strong employment. Not going to be easy to bring inflation down quickly in this scenario. I feel that this is going to be a long draw one.

Cut rates in early, I don’t think so.

We may end up with a situation like after the dot.com bubble completely burst, with 3 to 4 years of stock market going nowhere. Whether the bubble has completely burst, I don’t think so.

Thanks for the kind words.

Yes, agree that this is a possible scenario. Could be a prolonged period of the market going nowhere.

Economy may be more resilient than what markets are pricing in, and higher rates for longer could be really bad for certain kinds of financial assets…

In time of inflation, wouldn’t cash on hand depreciating further? Your $100 already buying less thing compared to last year. If you put it in stocks, at least it gives u the cushion, e.g. if you put it in DBS at today’s price, it gave of 4.5% in return and hedging against the raising interest too :p

Well the path forward in the short term matters too. Investors who bought DBS at 37 earlier this year are down 20% despite the inflation.

If interest rates are going to go up aggressively to combat inflation, there could be a lot of pain for financial assets in store.

What about people who bought 29 last week?