I’ve had some time over the long weekend to collect my macro thoughts.

So I wanted to share my latest thinking on how things might play out over the next 12 – 18 months.

How I think the next 12 – 18 months might play out

Now for obvious reasons, this is just a general idea of how things might play out.

Much will depend on (a) how quickly inflation falls away, and (b) how quickly the economy slows.

A change to either will affect the forecast below.

But at a high level, this is how I see things playing out:

- Feds will hike interest rates aggressively to combat inflation (We are here)

2. Tightening monetary policy will trigger a US recession in 2022/2023

3. This recession will build its own momentum that will not slow until monetary policy is eased

4. To counter the recession, the Feds will need to cut interest rates by a lot (typical recession requires 5% of cuts or the equivalent amount of QE)

5. However the ability of the Fed to cut will depend on (a) how bad the recession is, vs (b) how bad inflation is.

For Eg. If the recession is mild, but inflation is still sticky at 5%, they may not be able to ease in a big way.

Vs let’s say a terrible recession with inflation at 3%, in which case they ease in a big way.

So there is significant uncertainty in the short term path because it is not easy to forecast where exactly inflation/growth numbers will be 3 – 6 months from now.

6. At some point, the recession will be so bad, and inflation will start to come down, that the Feds will ease.

7. And because of how much pain is required to really bring inflation down, eventually the Feds will accept a middle ground of higher inflation than they expected, and slower growth than they expected.

The End Game for the Fed (1 – 2 years)

The short term dilemma for the Federal Reserve can be summed up as follows.

If they cut interest rates too early, inflation comes roaring back.

If they cut interest rates too late, economic growth will be devastated (recession).

My personal view – is that the Feds are going to try to achieve both outcomes – low inflation with strong economic growth.

But at some point in the next 6 – 12 months, it will become clear that will not be possible.

And I think at that point, the Feds will switch to a middle ground approach.

They will give up on their goal of bringing inflation back to their 2% target.

But they will also give up on their goal on real GDP growth.

In other words – they will accept higher inflation, with slower growth.

A stagflationary style outcome if you like.

How does Oil (or commodities) perform in a climate like that?

If we do get a US recession, demand for oil will drop.

But China emerging from their COVID lockdowns could drive a lot of consumption for oil

At the same time, underinvestment into oil supply is a well known factor. There’s just insufficient capex because of how the oil futures curve looks like, with oil 3-5 years out still at the $60 range making it hard to justify new investments into oil.

All while you have Russian supply falling off due to a lack of Western technology for drilling, and a possibility that Western sanctions actually have some bite.

So with oil, there could be a bit of upside in the mid term after we get through the recession.

And in the short term, there’s a bit of a tail risk where oil jumps to $200 because of some kind of supply shock in the market.

The analysis above can apply to any other commodity, but each commodity has slightly different supply side issues.

How to invest in a climate like that?

So if the picture I set out above plays out, this means that where we are currently:

1. Too early for long bonds / long duration trade – The Feds are still going to raise interest rates aggressively to combat inflation in the short term.

Which means that it is probably too early to go into interest rate sensitive style plays. That means bonds, REITs, growth tech etc.

2. Oil could have a role as a hedge – The worst case outcome for equities here, is for commodities to go up. Because that would drive inflation up, and limit the ability of the Feds to cut rates into the recession.

So if you are long equities now, oil could be a useful diversifier / hedge. Worst case oil does nothing or goes down, in which case your equities go up. Best case oil goes through the roof and equities plunge, but at least your oil positions go up (although this might not necessarily be “Best Case” for your portfolio).

In a world where bonds / Treasuries are no longer a good hedge because of rising interest rates, oil (or commodities) could replace that role.

3. Recession fears are overblown? – This last one is a bit controversial, and I would caution against trading on this unless you know what you’re doing. But my thinking, is that recession fears are a bit too early, and a bit too overblown, for where we are in the cycle.

When even less savvy investors are asking me whether they should sell their stocks because a recession is coming, I start getting concerned about this recession call.

If you look at the analysis above, I too think that a recession is coming. But I think a recession is more of a 2023 kind of story.

In markets, you don’t want to be too early, and you don’t want to be too late.

Nominal growth is still very strong, and there’s a bit of headroom here before we see a US recession.

So there could be a tradeable opportunity here for oil stocks, cyclicals, commodities etc.

How does this decade play out?

Regular readers will know my view is that this decade might be an inflationary one.

The picture I set out above ties into this view.

At some point, the pain of trying to crush inflation will be too much for the US to bear.

And they will start to ease monetary policy, while accepting a higher level of inflation.

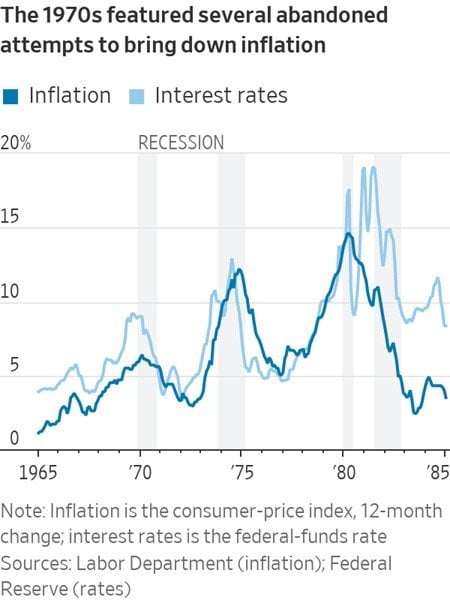

Coupled with supply side issues, this sets us up for the potential for a decade of stop-go inflation like we saw in the 1970s, where inflation goes away, comes back, and goes again.

And having discovered the power of fiscal policy – in the next recession you can expect more to come.

Governments will give handouts direct to the population to offset the impact of inflation / recession.

Think NS55 vouchers, applied on a global scale for the countries that can afford it.

California has already started implementing gas rebates. Actions like this will contribute to higher inflation by distorting market pricing mechanisms, impairing the Fed’s ability to bring inflation down.

Closing Thoughts: How will last decade’s winners perform in this new paradigm?

The outstanding performer of the last decade was undisputedly Tech.

And within tech, the FAANG stocks.

The question then – how will last decade’s winners perform in a new paradigm of higher interest rates, higher inflation, and slower growth.

Frankly I don’t know the answer to this one.

The last time inflation was a real problem was the 1970s, and we didn’t have Big Tech / Cloud back then.

But if your portfolio is very long tech, it’s at least a question to think about in the months ahead.