So… SIA is back for more cash.

After raising $7.7 billion in 2020, they’re now trying to raise another $6.2 billion.

SIA’s 2021 Rights Issue

The 2021 SIA rights issue is 209 MCBs for every 100 shares in SIA.

At the current price of $4.96, this means that for every $496 held in SIA shares, shareholders are being asked to cough up $209.

That’s a 42% capital call, which is really big.

How does SIA’s Mandatory Convertible Bonds (MCBs) work?

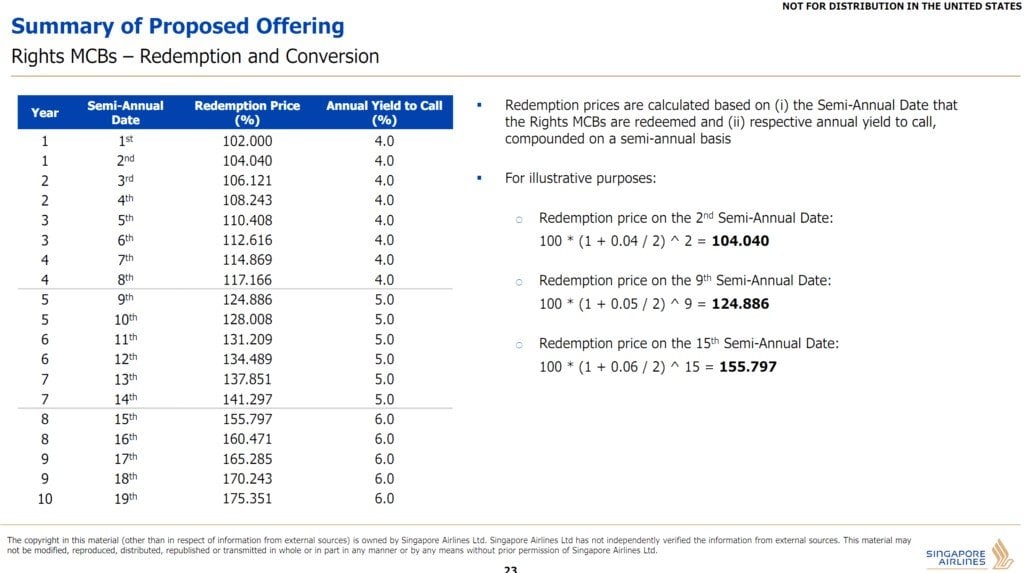

The MCBs are pretty complex stuff, so let’s recap how they work.

Zero Coupon

You do not get paid any interest (or coupon) each year.

MCBs can be redeemed by SIA any time

These MCBs can be redeemed by SIA any time within 10 years.

Let’s say you buy $1000 of MCBs.

On redemption date, SIA will pay you $1000 (being the principal) + an extra amount equivalent to the interest on the bonds for the duration held:

- 4% p.a. for the first 4 years,

- 5% p.a. for year 5 to year 7, and

- 6% p.a. for year 8 to year 10.

So if SIA redeemed the bonds in year 4, you will get no interest payments for the first 4 years, but on redemption date you get a lump sum payment of $1117.166.

This is the $1000 you put in originally, and $117.166 which is 4 years interest at 4% a year.

10 year duration of MCB

What if SIA doesn’t have the cash to redeem the MCBs?

Then you get paid in SIA shares.

In year 10, you’ll get paid a lump sum of $1,806.11, which is the $1000 principal and 10 years’ worth of interest – (in SIA shares).

Temasek will mop up the rest

Temasek will take its pro-rata entitlement and any remaining balance.

The previous round of MCBs from SIA was very poorly received.

Almost 96% was taken up by Temasek, despite holding only 55% shareholding in SIA.

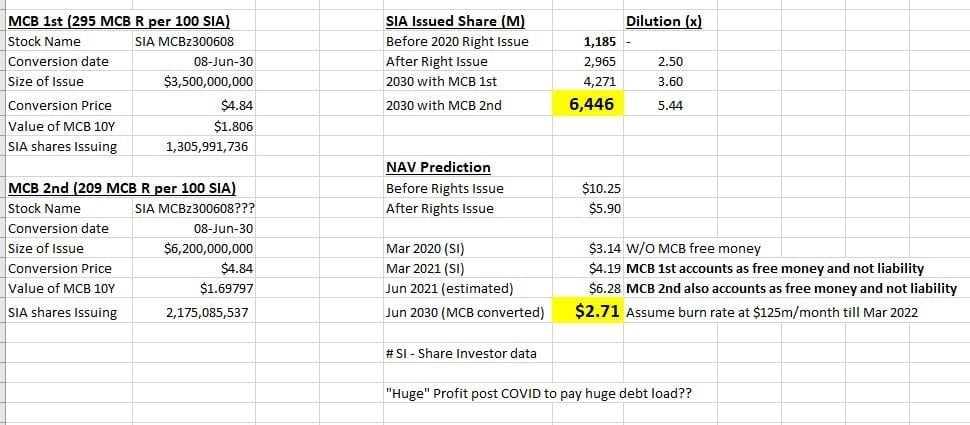

Dilution impact of the MCBs

A FH Reader shared this in our Facebook Group.

Long story short, what SIA has done since COVID struck, has been massively dilutive.

After the 2020 rights issue, SIA’s share count has increased by 2.5 times.

If you assume MCBs 2020 and 2021 all vest in full, the dilution is up to 5.5 times.

With an original price of SIA at $10 pre-COVID, after all the dilution with MCBs fully vested, price will work out to $2.71 just from dilution alone.

There are a lot of assumptions that go into the number above of course, and 10 years is a long time, but it gives you an illustration of how many new SIA shares that can potentially be.

MCBs are accounted for as equity

The interesting thing though – is that these MCBs are treated not as debt, but as equity.

So this wouldn’t show up on the balance sheet or in debt ratios, and it doesn’t dilute the share base until 10 years later.

Pretty crafty solution now that I think about it.

As kicking the can down the road goes, the MCB offers great optionality.

Follow Financial Horse:

[mc4wp_form id=”173″]

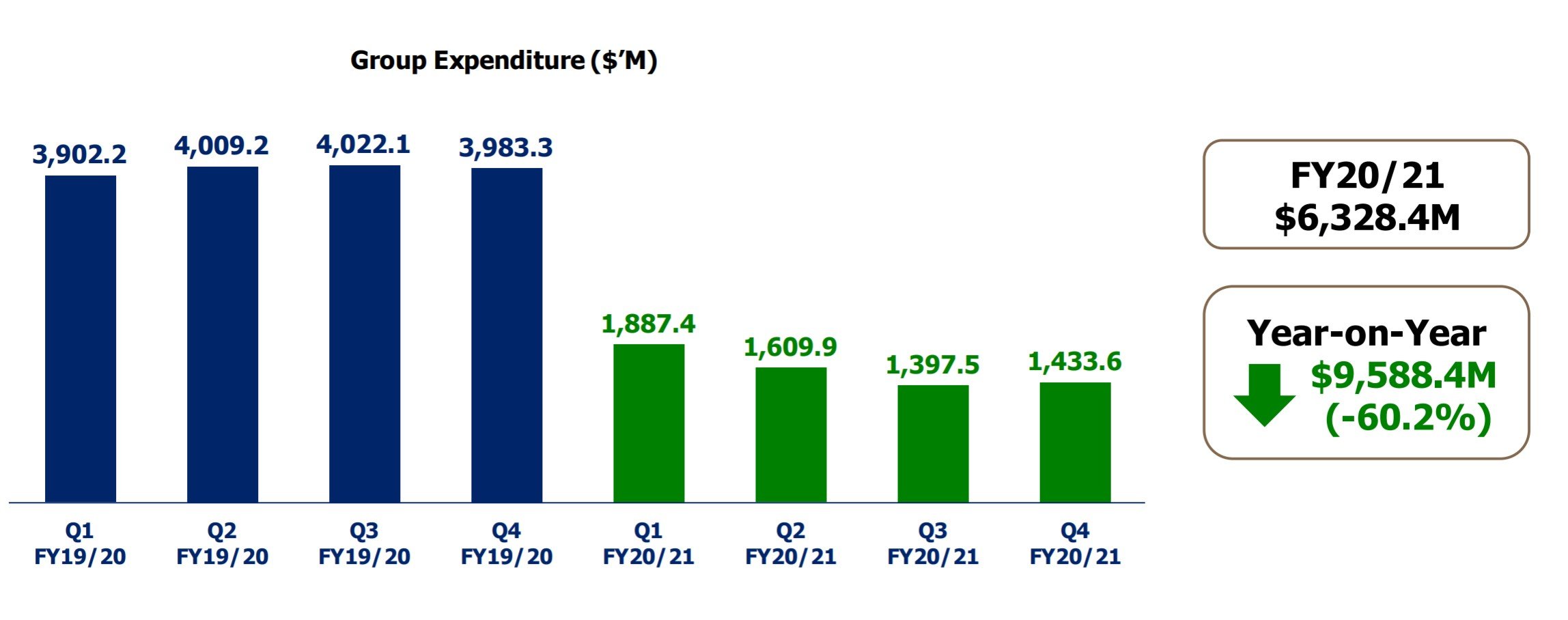

SIA’s FY2020/2021 results

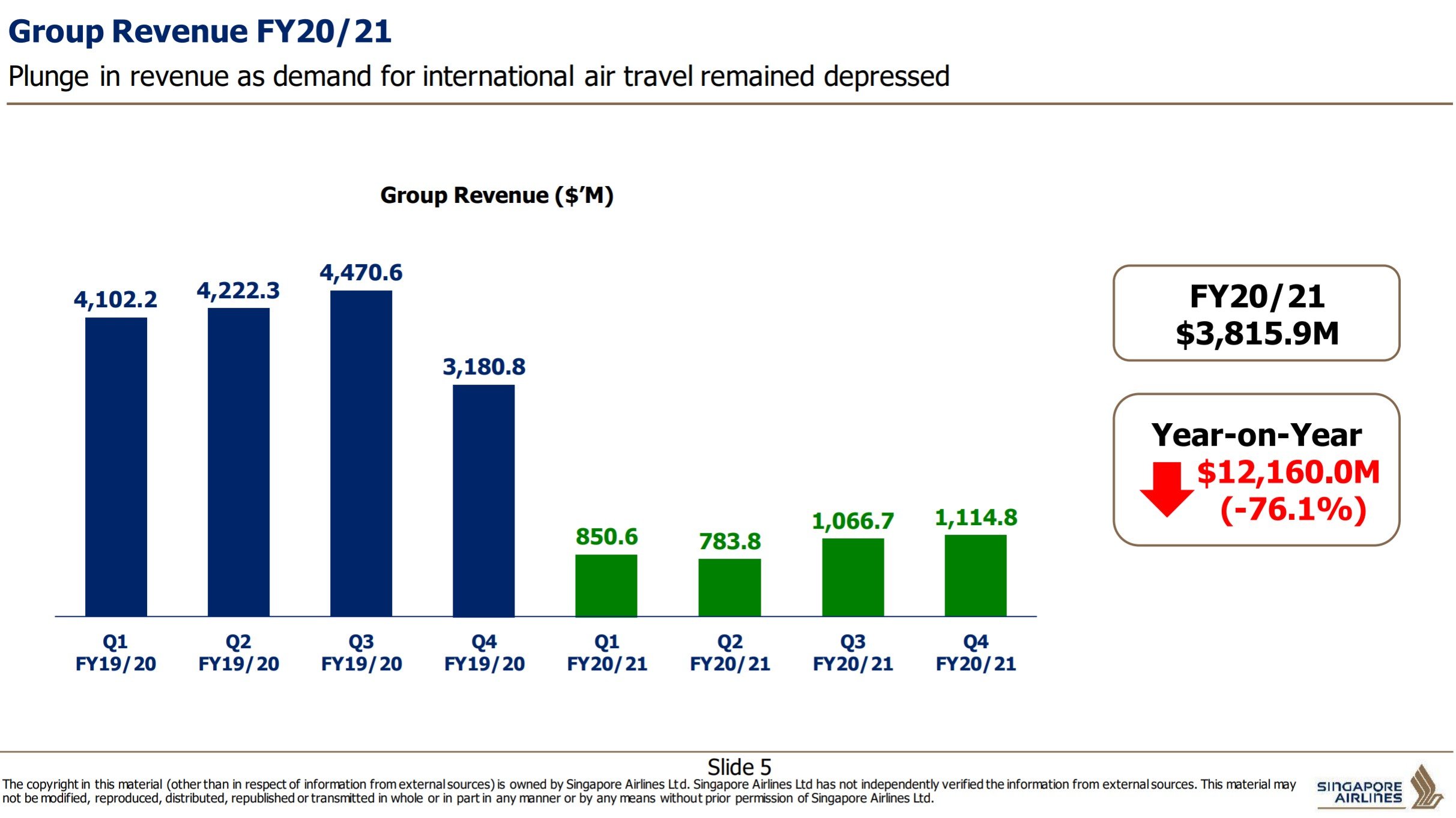

SIA’s Full Year results are out, and to no surprise to anyone, they’re an absolute disaster.

Year on year revenue is down a massive 76%:

Revenue is definitely recovering though, and will continue to pick up pace going forward.

What is SIA’s cash burn?

Using Q4 numbers – SIA pulls in $1.1 billion in revenue, on $1.4 billion expenses.

That’s a cash burn of $100 million a month.

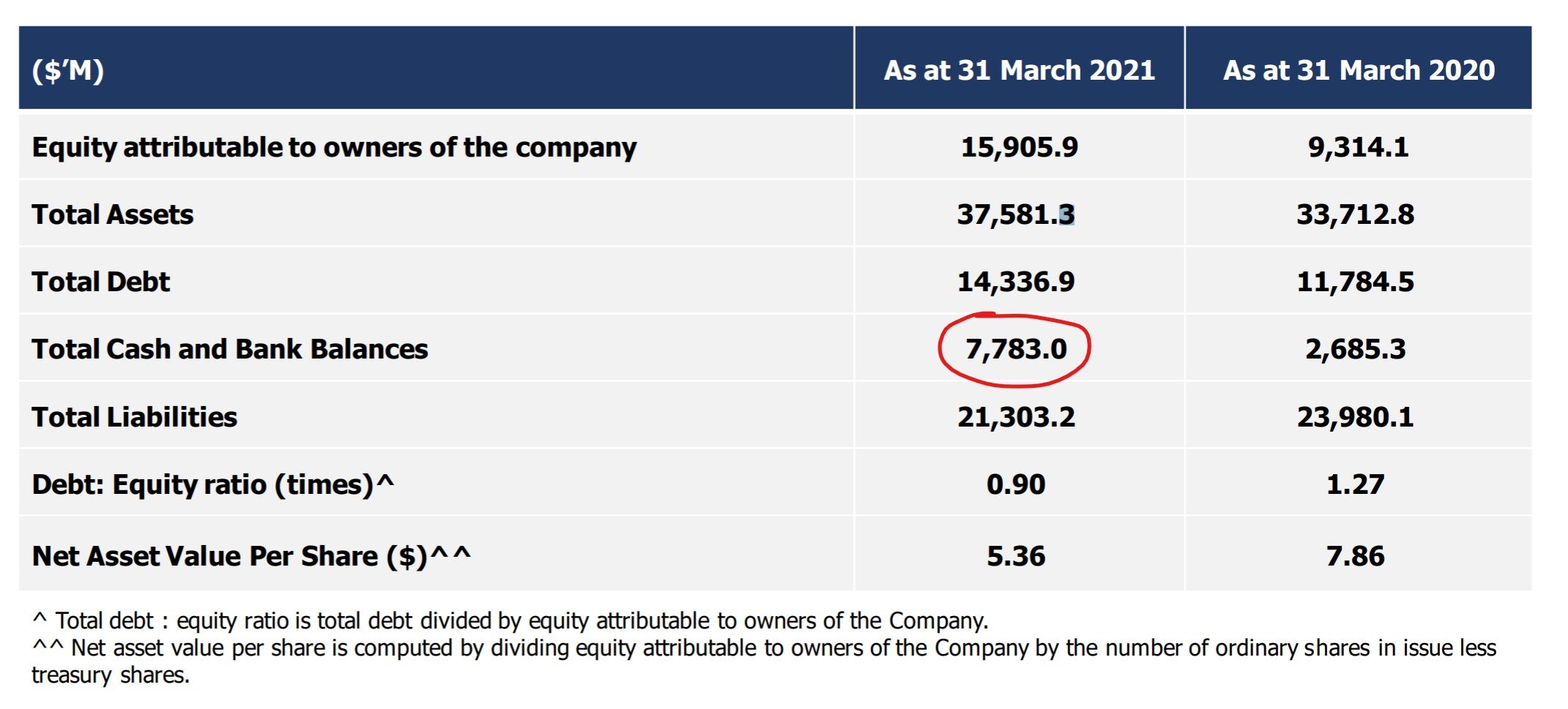

SIA holds $7.7 billion of cash?!

So imagine my shock when I found out that SIA holds $7.7 billion in cash on their balance sheet.

That’s billion, with a B.

This means that at the current rate of $100 million a month cash burn, they can last another 6 years.

Even if you use the full year 2020 loss of $2.5 billion, the current cash will last another 3 years. That’s another full 3 years of COVID, with Fuel Hedging losses.

With the new $6.2 billion SIA is raising, and the existing $2.1 billion untapped credit lines, SIA will have almost $16 billion in cash.

Even if we assume a more aggressive $150 million a month cash burn, that will last almost 9 years.

Why are they raising so much money?

So why does SIA need all this money?

Use of proceeds is set out below.

The 2 big ones are Capex and debt repayments. So I suppose you can argue that this money is being used to fund new aircrafts and invest in digital capabilities, and to pay off debt.

But that still leaves a lot of money on the balance sheet though.

Singapore Airlines Chairman Peter Seah said: “Since 1 April 2020, we have raised S$15.4 billion in fresh liquidity that has given us a strong foundation as we navigated the challenges posed by the Covid-19 pandemic with the support of our stakeholders.

“However, this crisis is not over. While the growing pace of vaccinations has given us hope, new waves of infections around the world mean that restrictions on international travel largely remain in place. The SIA Group has grown its passenger capacity and resumed selected services in a safe and calibrated manner, but industry bodies forecast that air traffic is not expected to recover to pre-Covid-19 levels until 2024.

“The liquidity that we will raise through the MCBs will further strengthen our financial position during these uncertain times, while providing the resources to position the SIA Group for growth and leadership. We have worked hard to retain and prepare our talented people to continue delivering the world-class service that SIA is renowned for. We will also continue to modernise our fleet with new generation aircraft that allow us to deliver greater comfort and innovative products to customers, and help to drive operating efficiency and lower carbon emissions.”

So basically – To get as much liquidity as they can, to protect against how COVID may evolve going forward.

Sure, I get that, but that’s a lot of money to be holding on the balance sheet.

That money isn’t cheap mind you, it costs 4% – 6% a year. Even if you kick the can down the road and pay it all in equity after 10 years, that’s still going to be massively dilutive to shareholders in 10 years.

So why does SIA need all that cash now? With Temasek’s backing, they can easily raise it 12 months later and Temasek would still mop up whatever retail doesn’t want.

Not sure what I’m missing here, so if anyone has any insights please let me know in the comments below.

FH views on airlines?

My views on airlines are no secret – I’m not a fan.

I’m with Warren Buffet on this one, the industry dynamics are really poor.

As the saying goes, “When a management with a reputation for brilliance tackles a business with a reputation for bad economics, it is the reputation of the business that remains intact.”

Airline industry dynamics are a disaster – commoditized product, with no cartel pricing power (no OPEC).

What is SIA’s competitive advantage?

This is how SIA wants to position themselves going forward: (1) Singapore as a travel hub, (2) Modern fleet with new and premium planes, (3) Delivering a world class service.

The problem though:

Singapore as a travel hub – other carriers can fly to Singapore too

Modern fleet – Emirates, Qatar and the China airlines all have a very new fleet, and tons of state backed cash to spend

Good service – Sure, SIA’s service is good, but is it 10x better than say Emirates?

So yes, there is some branding advantage. There are people who love SIA, or who love the miles game, who will only fly SIA.

But by and large, the industry is quite price conscious. If you give me a 50% cheaper ticket with a 10% poorer service, I’ll probably go with the cheaper one.

It’s a really tough business to be in, with limited pricing power.

How to play the travel recovery?

There are a lot of investors who use SIA as a proxy to play the travel recovery.

I get that, but I still think the better ways to play this are via oil, or the online travel agents (OTA).

The advantage with oil is that there is OPEC to manipulate prices, and there is a massive underinvestment into oil now with the whole green push – setting up the potential for undersupply.

The advantage with online travel agents is network effects – once the OTAs get big enough, they have massive network effects and become ridiculously hard to displace, which means a lot of pricing and market power.

For the record – I absolutely think that travel will come roaring back.

I think that once restrictions are lifted, travel is going to explode.

I mean even I myself am dying to travel again.

But as an investor, I am playing the travel recovery via oil and the OTAs, instead of via airlines (you can see my full portfolio on Patron if you’re keen).

If I were a SIA shareholder, would I take up the 2021 Rights Issue MCBs?

Full disclosure – I am not a SIA shareholder, so I have no skin in the game here.

If I were though, I’ll probably skip this 2021 rights issue MCB.

There’s just too much uncertainty over when the MCBs will be redeemed for me.

If SIA is going to hold $13 billion of cash on its balance sheet now, it doesn’t really make sense for them to start paying off these MCBs when the travel recovery plays out in 4 or 5 years right?

Especially if 96% is held by Temasek and not retail investors, even less incentive to pay it off early.

So I could be stuck with the MCBs for a long time, without clarity on when I get my money back. In a market where there could be much better uses for the money.

All for a 4% – 6% a year return. And a chance that I get paid in shares after 10 years.

Risk-reward is not compelling.

Should SIA be privatised?

SIAS wrote a very interesting open letter to SIA.

It raises some good questions, and I suggest having a read if you’re a shareholder.

One big question:

Some shareholders have asked whether SIA is considering privatisation and/or delisting (e.g. SMRT)? Has SIA any such plan?

I would be quite keen to hear SIA’s response on this.

With Temasek holding 55%, and taking up almost all the MCBs, they already have a lot of money invested in SIA. Privatisation could be a logical next step?

Closing Thoughts: Are GLCs losing their edge?

One thought that struck me this week when I read about Singtel’s earnings and restructuring – are GLCs are losing their edge?

There was a time when SIA, Singtel, Keppel were the pride and envy of the region. Every investor had them in their portfolio.

But today, with the rise of technology, the playing field has changed.

The names that garner excitement are names like SEA, Grab, Gojek-Toko.

The world is changing quickly, and the GLCs will need to adapt quickly to keep up.

Take me for example – my Singapore portfolio is mostly banks and REITs. The rest is tech in US / HK. I just see more growth coming from here.

From the Singtel restructuring plan announced, it’s clear that management is aware of the issue, and working to address it.

Let’s hope the GLCs manage to turn it around. As a Singaporean, I’m definitely rooting for them.

Love to hear your thoughts!

*LAST 3 DAYS*

May promotion for both investing courses ends this month!

2021 will be a volatile year – with lots of opportunities for investors. Learn to invest here!

Dbs is very kind with $3.60. Last year when price was below there, I asked myself if I would buy if it drops to $3. Nope, sorry, there are better places to park.

One problem I am foreseeing is the reduction of business travel which is lucrative and profit cash cow. Used to be a jetsetter myself. With Zoom and whatnot and the safety concerns from the virus even with full vaccination, I won’t get on the plane so frequently. If I really need to, I’ll take a cheaper option like LCC due to uncertainty of businesses going forward. Many businesses had already been quite badly wounded, so don’t expect to fly 1st or Biz Class.

Airlines is also likely to mandate that passengers be fully vaccinated and it is not possible for everyone. Else you get quarantine upon arrival and incur more biz costs, does it make sense?

That’s a good point you raised. It remains to be seen if all that business travel will make a comeback, and that’s the big earner for these airlines.

It seems that after every recession, business cuts back on travel expenses. We saw this after 08, and we may see this after COVID again. Either way, airlines may need to focus more on the leisure/travel crowd, which is a more price conscious segment.

The quarantine/vaccine logistics are going to be a nightmare. I suspect at some point the world will have to accept that the virus is endemic, and focus shifts to mitigation rather than absolute prevention (also manages the economic impact). Already some hints of that over the past week.

Thanks FH, always find pleasure in reading your insights. My views in particular:

1. There is still lingering “hopes” on the future of the airline industry..perhaps SIA/Temasek view is to strike while the Hope iron is still hot, before it cools down, so that the takeup rate, while tepid, can still allow for external equity instead of 100% Temasek.

2. Noted the exciting names mentioned are the companies that sell shares for cash, rather than sell a economical service (i.e. don’t generate profits or sufficient cashflows). For instance, SEA sells shares almost as a ritual. If interest rate environment goes up (and a yield curve control doesn’t happen), I believe this excitement fades quickly as it came.

3. IMHO, I find SIAS very edgy and honestly asking questions mainly to serve the happiness of its “constituency”. Asking openly if Temasek (who else) might consider privatisating SIA is just pandering to constituents who are likely stuck with SIA (I assume not much homework done here) and just hoping for a quick buyout of their shares. Isn’t this just yet another hope for Privatizing Profits And Socializing Losses, since Temasek’s money is Singaporean’s money.

Great comment Charlito, my views:

1. That’s definitely possible. Maybe it’s a sentiment thing, they thing it would be easier to raise now rather than later. It’s a scary thought though – what’s going to come next?

2. Agree – rising interest rates will crush the growth trade very quickly. But I don’t expect interest rates to stay high for long, exactly because of that reason – it will crush the long duration trade, and take much of the economy with it. So I think interest rates will stay low for quite a while, which could be supportive of such plays.

3. Agree again haha. But leaving aside the agenda of SIAS, it’s good that at least someone is asking the hard questions. I get that SIA can’t reply to all of them because some could be price sensitive / affect commercial strategy, but at least the questions are asked and SIA is given a chance to response.

Good article! They might be expecting interest rate to rise when they actually need the money (due to inflation?) hence hedging by borrowing more now.

Correct me if I’m wrong – But the MCB terms are fixed? So even if they raise it next year, they are still using the same 4-6% interest rates, and they will have Temasek to mop up any excess?

Technically the coupon rate would be a function of the rfr (cost of debt formula). When they set MCBs IR a year ago,it was based on historically low IRs. Now that rfr is on the way up, the only was coupon rate can stay low is if SQ is in a more secure position that it once was. I don’t think that is the case for many reasons (e.g. delayed recovery). So therefore, I believe the only way they can get away with this issuance is to do it as soon as possible.if RFR inches up,they won’t be able to justify not increasing coupons.

You’re right in any case. Since Temasek has offered to mop up, then why not just let them do so. I guess it’s also about signalling that they are Keen for nonstate sponsored investment or for it tomorrow appear like handout. If not, they could, provide a coupon rate equivalent to rfr and do away with all illusions – thereby reducing dilution.

Sucks to be an SQ investor right now. Great companies aren’t always Good investments.

Oh that’s a fantastic comment SK. I think you’ve just hit the nail on the head right there.

Makes a lot of sense when you put it that way – rising interest rate scenario, but SIA wants to lock in the low rates, and yet send a signal to the market (that this is not a bailout).

If that’s the case, then these MCBs with their massive takeup by Temasek could be viewed as a psuedo government support, while also avoiding a case of socialising the losses – Temasek mops up all the MCBs, which don’t count as debt, and won’t be dilutive until 10 years away, and Temasek earns a decent return on the cash.

Pretty neat solution when you look at it that way, instead of doing a direct cash injection / bailout like the US Airlines.

Hi FH, thank you for your insights! I have been offered the rights issue and I am still considering about it. You mentioned in your article “There’s just too much uncertainty over when the MCBs will be redeemed for me.” But there is a maturity date. Wouldn’t that eliminate the uncertainty you mentioned above,

Yes but the maturity date is 10 years! So if they don’t redeem before that, one would be holding on for 10 years only to get a blended 5% return over 10 years, payable in SIA shares.

Risk-reward doesn’t look amazing to me.

Hi FH

The trajectory of international travel in 10 yrs time is dependent on many variables. Assuming things normalize, SIA starts to make profit. On top of the blended yield, there’s still a possibility that the share price would be higher than the conversion price? Am vested, still deliberating whether to subscribe.

Yes definitely. In fact I would be surprised if SIA’s share price is not higher than $4.84 in 10 years.

But the question is one of opportunity cost. The same money in the MCBs, vs the same money in say the S&P500 / DBS / MCT – which delivers the higher return.

That to me is the key question, and I’m not so sure about SIA. Could be wrong though.

Thanks for your perspective. Forgot about opportunity cost. Some sectors and markets do look a bit expensive now

Hi FH,

Thanks much for the effort and time you put into the article, appreciated! Enjoyed reading the insightful comments from the other readers.

My first time and will come back for more. Keep well and safe!

Thanks for the support KW! Glad that this has been helpful for you. 🙂

Hi FH,

I am vested in SIA with a small profit. I do not intend to subscribe to the rights. Can you advise the steps to sell off the rights? Thanks!

I think the rights are trading for like 0.01 now so you won’t get much for them. You can check with your stock broker for the detailed steps, it’s usually just submitting a sell order for the rights ticker (and choosing the price).

Thank you for the insight.. Was wondering if I am offered the rights and decided not to buy, i do not actually hold the rights am I (based on allocation)? Bcos my SGX statement is showing this rights right now..

The rights give you an option to buy the MCB. So if you decide not to take them up, you do not get the MCBs. Of course, you can sell your rights on the open market, but they’re not trading for much right now.

Hi, after reading this review, I will see if I can sell away the allocated rights. May I know your views on whether to hold on to existing SIA share? I can make a small profit now, sell and go. channel the money to those who offer more lucrative returns. buy SIA when covid is over?

Can’t advise for your situation specifically. Whether to sell will depend on your views on SIA, and your risk appetite + investment objectives.

For me personally, I’m not a fan of the airline business. I’m with Buffet – I think the long term industry dynamics are genuinely poor, so it’s hard to see what management can do to turn it around. Singapore will still need an airline for strategic reasons, but as a profit making entity I’m not so sure. If I had a position, would probably wait for a short term bounce to exit, and move the money into higher conviction long term plays.

if i am not subscribing it, will my holding be diluted?( currently i am holding position for SIA) or any impact to stock price right after the right can be traded in market?

Technically you won’t be diluted because the MCBs are not shares. You only get diluted if the MCBs expire after 10 years and they convert into shares.

But practically speaking – there’s no such thing as a free lunch. So it’s hard to say that SIA issues 6b worth of equity-debt hybrids and shareholders are not “diluted” out. There definitely is some impact, it’s just not the traditional form of dilution where share count goes up and your % ownership of the company drops. 🙂