I know Singapore Savings Bonds are no longer that exciting when:

- T-Bills are paying 3.75%

- GXS Bank is paying 3.48% for a bank account

- Fixed Deposits are paying 3.5%ish

But do note that all 3 of the above do not lock in interest rates for a long period.

It’s always human nature to extrapolate the current state of events.

When interest rates are low, like they were 2 years ago, everyone expects interest rates to stay low forever.

When interest rates are high, like right now, everyone expects interest rates to stay high forever.

But if there’s anything I’ve learnt from markets – it’s that everything is cyclical.

Things go up, and then they go down.

A big benefit with Singapore Savings Bonds is that you get to lock in the interest rates for up to 10 years.

Which in the event that interest rates get cut, is a massive benefit.

Let’s discuss a couple of key questions:

- What is the chance of interest rate cuts going forward?

- Are Singapore Savings Bonds a good buy?

- Singapore Savings Bonds compared vs other cash options like T-Bills, GXS, Fixed Deposits

What is the chance of interest rate cuts going forward?

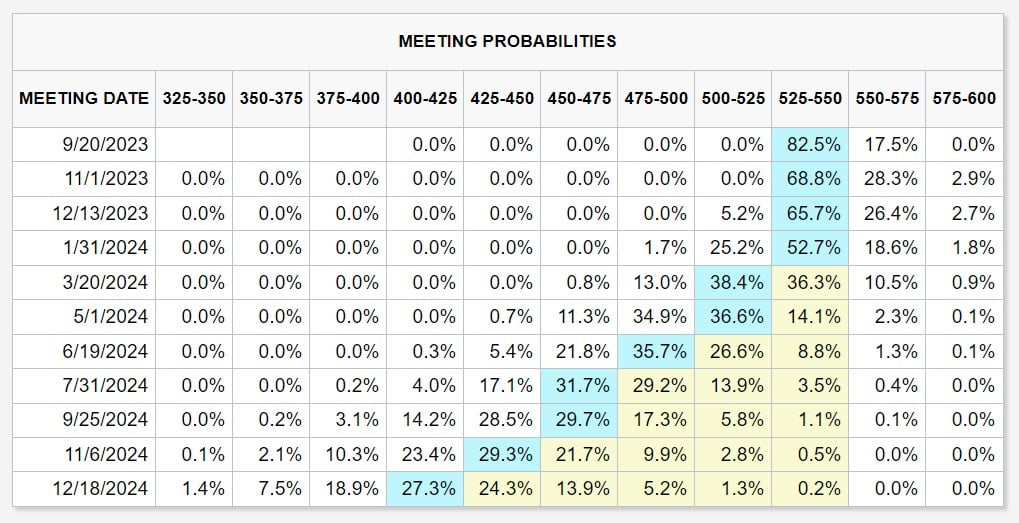

This is what is priced into the interest rate curve today.

Interest rates to stay flat until Jan 2024.

With 5 interest rate cuts throughout the course of 2024.

This means that the market is already saying we are at (or close to) peak interest rates today.

If you believe the market pricing to be accurate, then this is about as high as it gets for short term interest rates.

If true – this means that any new T-Bills or Fixed Deposits or Money Market Funds you buy in 2024 are going to see lower interest rates (if you believe market pricing is right).

What do I think?

Personally, I agree that we are close to peak interest rates here.

I think there is a good chance that the July Fed rate hike was the last hike this cyclee.

And what follows after rate hikes, is usually a period of extended pause, before rate cuts.

The million dollar question now is how long does the Feds pause before they start to cut.

Is it going to be 6 months like the market is pricing in, or longer?

And that’s an incredibly tough call, because it’s not just about inflation and economic weakness.

It’s also about how Jerome Powell’s Fed reacts to slowing inflation and slowing economic growth – and what they determine to be the right path.

All in an election year.

In other words, you’re second guessing Jerome Powell in an election year, and that’s not going to be an easy call.

So… pays to start locking in interest rates?

Because of that, I think that for patient investors who can afford to hold through the short term volatility.

It pays to start thinking about how to play the reversal in interest rates.

From a macro point of view there are many potential plays.

From long duration stocks like REITs / tech, to buying call options on the TLT (20 year+ treasury ETF).

I cover those in greater detail on Patreon, but in today’s article I wanted to discuss implications on cash management.

And whether it makes sense to start adding allocations to Singapore Savings Bonds.

You know, just in case interest rates start to get slashed in 2024.

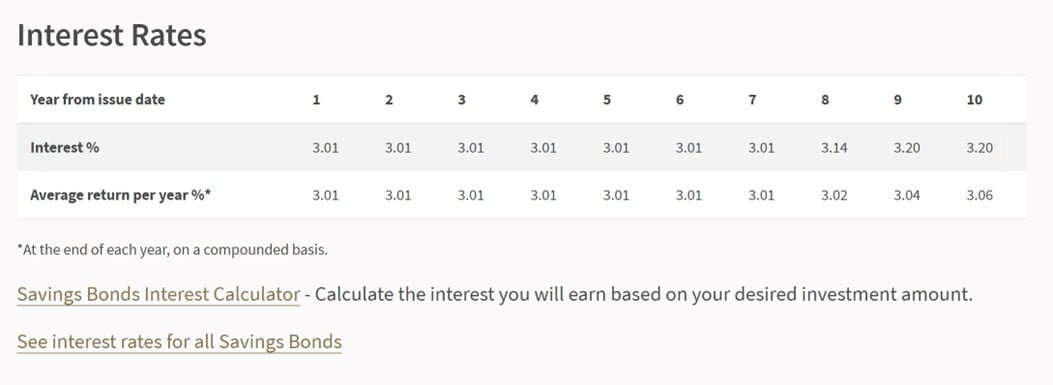

Are Singapore Savings Bonds a good buy? 3.06% over 10 years

You can see the latest interest rates in the Singapore Savings Bonds below.

3.01% for the first 7 years.

And 3.06% over 10 years.

Main benefit of Singapore Savings Bonds is the optionality

For those who are newer to Singapore Savings Bonds, the key features of Singapore Savings Bonds are:

- Locks in interest rates up to 10 years

- Can be redeemed any time at par with accrued interest (get your money back the 1st business day of the following month)

Heads you win, tails you win?

In my view – the main advantage of Singapore Savings Bonds in this climate is that it gives you optionality.

Think about it this way.

If interest rates get slashed in 2024.

You just sit tight and collect the great interest rates for the next few years until interest rates go up again. At which time you redeem and buy whatever is best at that point in time.

If interest rates stay high in 2024.

You can redeem any time and rotate the cash into whatever high yielding cash options are available.

Heads you win, tails you win?

What is the drawback with Singapore Savings Bonds?

The way I see it, there’s 2 notable drawbacks to Singapore Savings Bonds

- Lower short term interest

- No capital gains potential

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

Lower short term interest vs T-Bills / GXS / Fixed Deposit

You’re getting 3.75% on a T-Bill, and 3.48% on a GXS bank account (or fixed deposit).

That’s a spread of 0.74% and 0.47% respectively vs Singapore Savings Bonds.

On $100,000, that works out to $740 and $470 a year.

That’s basically the “opportunity cost” you are paying, to lock in interest rates for 10 years.

Is that worth it?

You tell me.

Personal views?

Personal views – I generally agree with market pricing that you probably don’t see interest rate cuts in 2023.

So locking in rates now, maybe early by a few months.

But sometimes you also don’t want to time these things to perfection – just in case you’re wrong.

Will Singapore Savings Bonds go up the next few months?

US long term interest rates jumped the past week after the Fitch downgrade, and I think you may see a similar trend in the Singapore 10 year.

Singapore Savings Bonds are pegged to Singapore 10 year interest rates, which means there is a chance that the Singapore Savings Bonds for the next few months might get even better.

Which means that if you want to get greedy you can probably wait for a month or two before starting to buy Singapore Savings Bonds.

Of course, the risk is that you’re wrong on this.

And interest rates just keep going down the next few months.

What would I do?

Personally I think I might wait though.

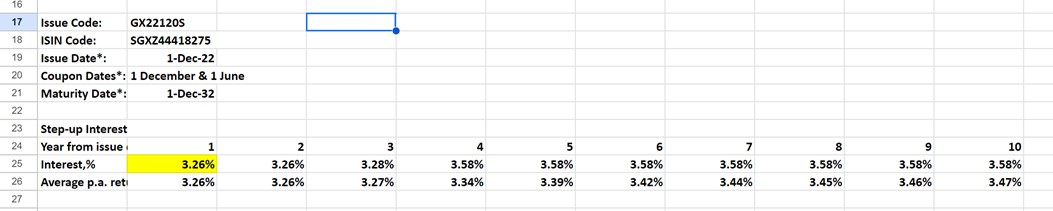

I already have Singapore Savings Bonds from 2022 that are yielding interest rates like this.

So it’s not the end of the world for me if interest rates go down, as I already own Singapore Savings Bonds.

But if you have zero exposure to Singapore Savings Bonds today, and all your exposure is short term debt like T-Bills.

Maybe the answer is different.

Main drawback is no capital gains potential

The other big drawback of Singapore Savings Bonds is no capital gains potential.

This happened to me in 2019 when I was holding quite a lot of Singapore Savings Bonds (given we were late in the business cycle).

In 2020 the markets crashed and interest rates went to zero.

But my Singapore Savings Bonds did not increase in value one bit.

Whereas if I were holding long term US Treasuries, I would probably be looking at 20% capital gains.

So that’s the other drawback with Singapore Savings Bonds.

This is a cash management solution.

There is no upside potential even if you are right on interest rates.

For the upside you’ll want to buy long term US Treasuries, or something like the TLT ETF which I discuss further on Patreon.

Singapore Savings Bonds compared vs other cash options like T-Bills, GXS, Fixed Deposits

What are the other options if you don’t want to buy Singapore Savings Bonds?

Note that most of these alternatives are short term debt, so you cannot lock in interest rates for a long period of time.

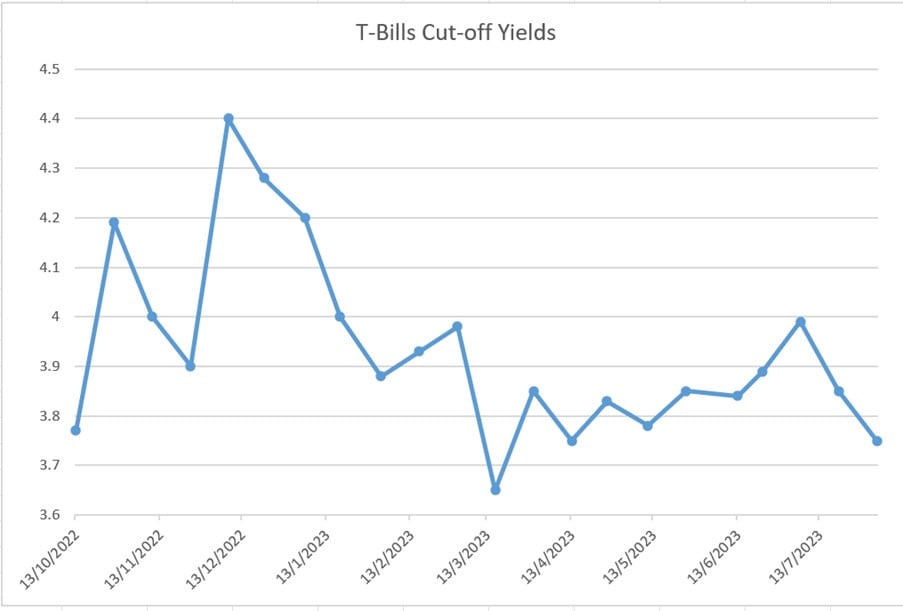

T-Bills – 3.75% for 6 months

Latest T-Bills yields below, you’re looking at 3.75% for 6 months.

Frankly I was quite surprised at this result too (read more on my debrief).

I think there is a chance you may see T-Bills yields recover the next couple of auctions (in line with global interest rates).

GXS Bank – 3.48% on cash

I just wrote about GXS Bank which I think is very attractive.

You’re getting paid 3.48% on cash, on up to $75,000.

With no minimum deposit, and no lockup period.

And no hoops to jump through.

You just put money in, it earns 3.48% pa accrued daily.

And you can take it out anytime.

I think it’s a fantastic deal, and a very strong alternative to T-Bills or Fixed Deposits or Singapore Savings Bonds.

Yes yields are not as high, and GXS may decide to cut interest rates down the road.

But as long as it lasts, it’s a very good deal.

Unfortunately signups have closed due to the overwhelming response, and you can only get on a waitlist now.

For those who managed to get an account though, it’s a very good place to park liquid cash.

If you don’t have an account, it’s probably joining the waitlist for when they open to sign ups again.

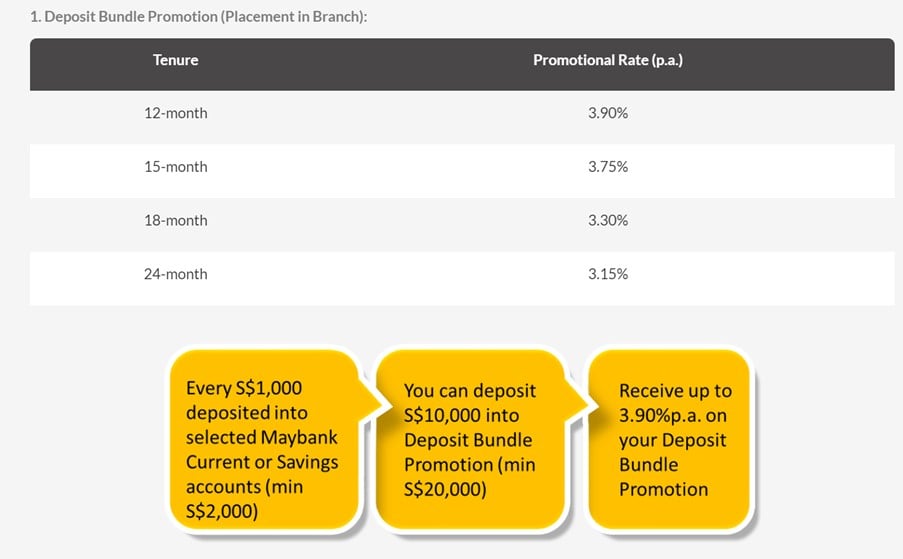

Maybank Fixed Deposit – 3.5%ish blended

Alternatively you can use the Maybank Fixed Deposit which pays 3.90% for a 12 month deposit.

Do note that you do need to deposit $1,000 for every $10,000 in fixed deposit.

This brings the blended yield down to about 3.5%-ish, which is in line with other banks like ICBC or BOC.

This makes T-Bills quite an attractive alternative to Fixed Deposits, simply because of the higher interest rates.

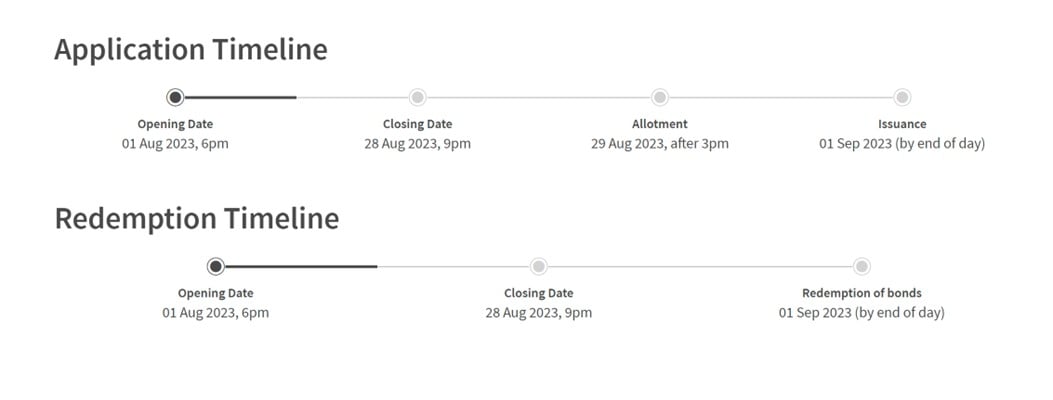

Application (or Redemption) timeline for Singapore Savings Bonds

If you’re keen to apply for (or redeem) Singapore Savings Bonds.

Deadline is 28 August, 9pm.

That’s plenty of time away, and I suggest you only put in your application as close to the deadline as you can.

The moneys are deducted on application so you lose the use of the funds, and you usually want to wait just in case you change your mind due to market conditions.

This article was written on 4 August 2023 and will not be updated going forward. For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do sign up as a Patreon.

– Get up to USD 580 worth of shares

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 580 free fractional shares.

You just need to:

- and fund $300 SGD

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Best investment books to improve as an investor in 2023?

Check out my personal recommendations for a reading list here.

GXS just announced it is cutting interest rates to 2.68% 🙁

I am equally devastated. Just when I had moved 75k in… 🙁

Ouch. I was put on the waiting list.

Saw their nonsensical email statement (“To make your money work just as hard for you”); couldn’t even sustain the 3.48% interest rate for a full month & they’re giving customers a 10-day notice period regarding the rate “revision”. Makes me wonder just how reliable/trustworthy GXS is as a bank.

Hi FH love your posts, could I check where you get the image of the interest rate curve from? Much thanks!

Thanks for the support!

Which interest rate curve do you mean?

The interest rate pricing is from: https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html?redirect=/trading/interest-rates/countdown-to-fomc.html

Whereas the US 10Y and 20Y yield chart is from https://www.koyfin.com/ (I have a paid account, but the free account should still give you limited access).

Hope this helps! 🙂