In case you missed it, Jerome Powell announced the end to the rate hike cycle at this week’s FOMC.

No more rate hikes in 2023.

In fact – the market is now pricing in 3 rate cuts by end of 2023.

All while T-Bills yields plunged to 3.65%.

And almost every bank is revising their fixed deposit interest rates down (after the promotion periods).

This raises an interesting question:

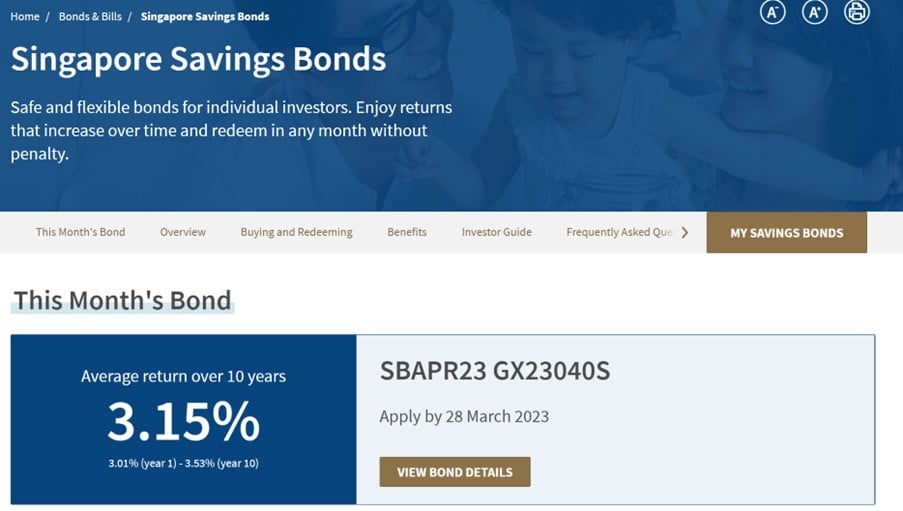

Did the April 2023 Singapore Savings Bonds suddenly become a very attractive buy?

You can lock in 3.15% returns risk free for the next 10 years.

And also have the option of getting your money back (with accrued interest) any time within the 10 years.

Worst case if interest rates stay high, you can always redeem the Singapore Savings Bonds.

Best case if the market is right and interest rates are going to be cut aggressively – you can hold up to 10 years.

A good way to hedge?

No more Interest Rate Hikes in 2023

I extract the key quote from Powell below:

At today’s meeting, the committee raised the target range for the federal-funds rate by a quarter percentage point, bringing the target range to 4.75 to 5 percent, and we are continuing the process of significantly reducing our securities holdings.

Since our previous FOMC meeting, economic indicators have generally come in stronger than expected, demonstrating greater momentum in economic activity and inflation.

We believe, however, that events in the banking system over the past two weeks are likely to result in tighter credit conditions for households and businesses, which would in turn affect economic outcomes.

It is too soon to determine the extent of these effects, and therefore too soon to tell how monetary policy should respond.

As a result, we no longer state that we anticipate that ongoing rate increases will be appropriate to quell inflation; instead, we now anticipate that some additional policy firming may be appropriate.

We will closely monitor incoming data and carefully assess the actual and expected effects of tighter credit conditions on economic activity, the labor market, and inflation, and our policy decisions will reflect that assessment.

Basically, no more rate hikes in 2023.

Until the Feds assess the true impact of the bank failures the past 2 weeks.

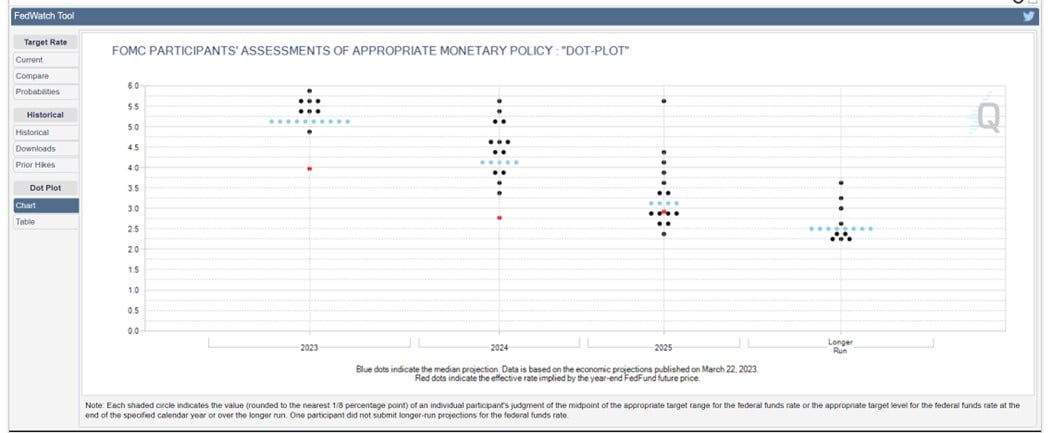

What about interest rate cuts?

On rate cuts though, Powell doesn’t see any rate cuts in 2023.

This is completely contrary to what the market is pricing in.

So you now have a situation where the Feds expect to hold interest rates steady at 4.75% – 5.00% for the whole of 2023.

While the market is pricing in 3 interest rate cuts by end of 2023:

Suffice to say, somebody is going to be very wrong here.

Either the Feds are going to be proven very wrong and be forced to cut interest rates soon.

Or the market is going to be very wrong and force a sharp repricing across the board.

I have my own views on this, but for now let’s just say that there is a fair bit of uncertainty on the path for interest rates going forward.

Because of this, locking in interest rates may not be the worst thing in the world.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Should you buy T-Bills, Fixed Deposits, or Singapore Savings Bonds at this stage of the cycle?

Given that the Feds have said no more interest rate hikes in 2023.

Does it pay to start locking in interest rates longer term?

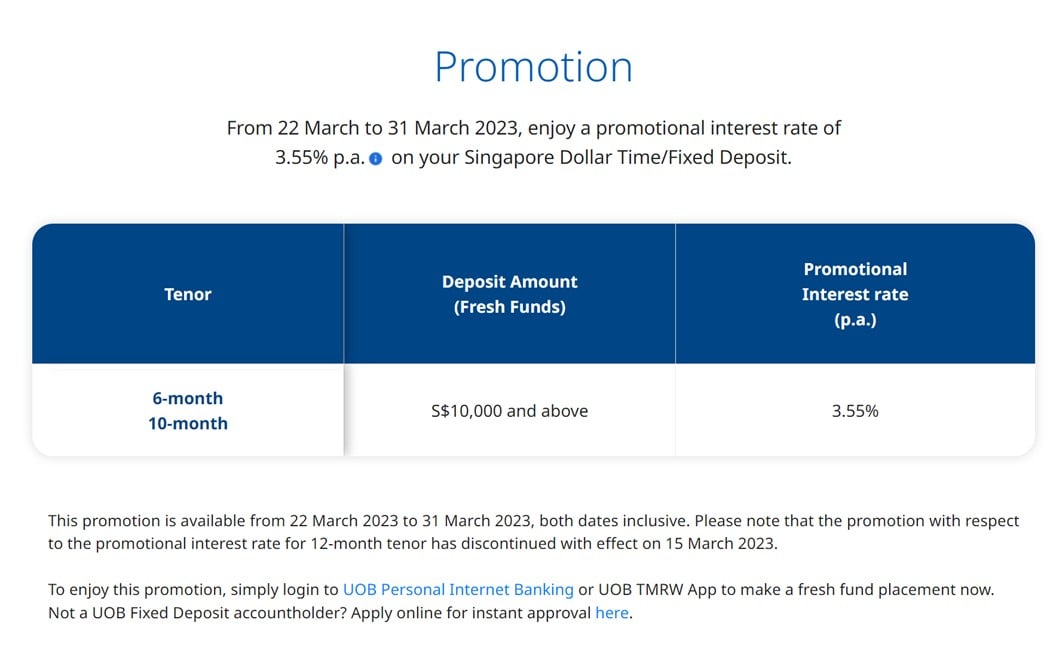

Fixed Deposit Rates keep getting cut…

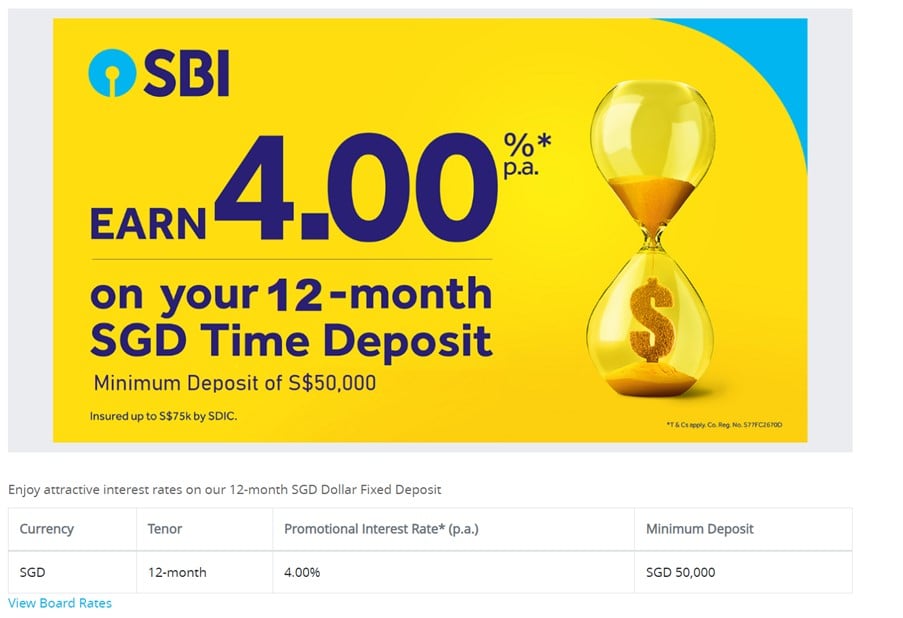

In my recent Fixed Deposit article I shared that the best fixed deposit interest rates are:

- If you are okay with a foreign bank – State Bank of India offers 4.00% for 12 month fixed deposit with minimum of $50,000

- If you want a local bank – UOB offers 3.85% for 6, 10 or 12 month fixed deposit with minimum of $50,000

Unfortunately UOB has slashed their interest rates down to 3.55% now.

This is in line with what’s been happening with most other banks after their Fixed Deposit promotion period.

You can still get 4.00% with State Bank of India though.

Pretty good deal given the drop in T-Bills and Fixed Deposit rates across the board.

Not sure how long it will last though, if this keeps up.

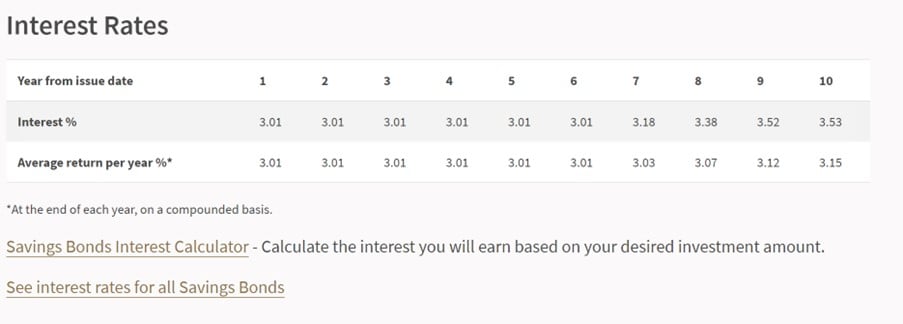

Singapore Savings Bonds Interest Rates are decent, and go up to 10 years

With the events of the past 2 week, I think you might see the April Singapore Savings Bonds become quite popular.

You’re locking in 3.01% for the first 6 years.

Stepping up to 3.15% over 10 years.

For an instrument that is risk free.

And where you can get the principal back with accrued interest any time, without liquidity concerns.

Heads you win, tails you don’t lose much?

Worst case if you are wrong and interest rates stay high, you can always redeem the Singapore Savings Bonds and get your money back.

Best case if the market is right and interest rates are going to be cut aggressively – you can hold up to 10 years.

Not too bad in these uncertain times.

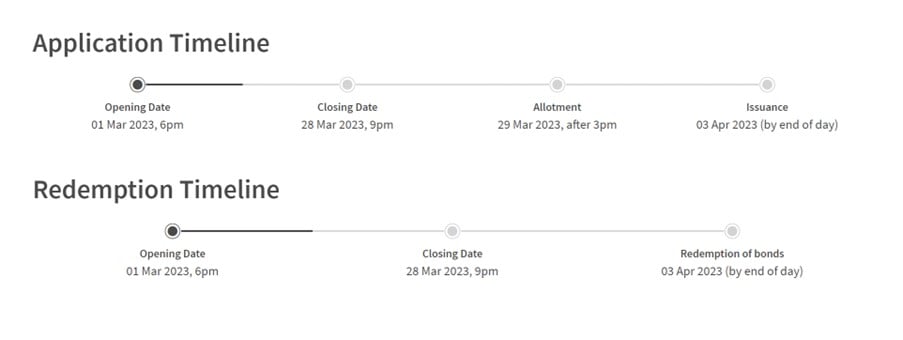

Singapore Savings Bonds Application Timeline

So for those who are keen, you might want to consider putting in an application before the 28 March (9pm) deadline:

Bidding / Allotment strategy for Singapore Savings Bonds

An interesting question I received was on bidding strategy.

The past few Singapore Savings Bonds all saw 100% allotment because T-Bills and Fixed Deposit rates were very high.

Now that T-Bills and Fixed Deposit rates have come down sharply, we might see a meaningful pickup in Singapore Savings Bonds demand.

What kind of allotment will we see for the April Singapore Savings Bonds?

I thought about it for a bit.

And the answer I must admit – is I have no clue.

What I would say is that if you’re submitting something below $40,000, there’s probably a good chance of meaningful allotment.

But if you want to apply for $200,000 at one go, I’m not sure.

For those already maxxed out on Singapore Savings Bonds allotment and looking to refresh their SSB…

So for those of you who already have a full $200,00 allocation and want to refresh your Singapore Savings Bonds.

I would say maybe don’t redeem the full $200,000 at one go, just in case this round of Singapore Savings Bonds prove very hot.

But truth be told, I think your guess is as good as mind here.

Incredibly hard to predict what kind of allotment we’re going to see next week.

What am I doing with my Singapore Savings Bonds?

Personally for me I’m already maxxed out on my Singapore Savings Bonds.

The worst Singapore Savings Bonds I’m holding pay about 2.8 – 2.9% for the first year.

Is it worth swapping them out for these 3.01% yielding Singapore Savings Bonds?

Nah… probably not worth the effort for me.

But it really depends on each investor.

If you’re holding pre-2022 Singapore Savings Bonds that are yielding 2%, it’s probably a no brainer.

As always, this article is written on 24 March 2023 and will not be updated going forward.

If you are keen, my full REIT and stock watchlist (with price targets) is available on Patreon, together with weekly premium macro updates. You can access my full personal portfolio to check out how I am positioned as well.

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

WeBull Account – Get up to USD 500 worth of fractional shares (extended to 31 March)

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 500 free fractional shares (extended to 31 March).

You just need to:

- Sign up here and fund any amount

- Maintain for 30 days

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

Hmm? Fed dot plot shows 5.125% which means one more rate hike in 2023.

Well it means a less than 50% chance of 1 more rate hike in 2023.

Market is even more aggressive – Market prices only a 10% chance at 1 more rate hike in 2023.

Sorry I should have been clearer. The 5.125% is the midpoint of the target range of 5.00-5.25% hence it means one more hike to get to said target range. But yes, market apparently thinks otherwise.

Ok I get what you mean. Thanks for clarifying, appreciated.