Note: This review is on StashAway Simple (money market fund). For the review on StashAway’s investment product, check out this article instead. There’s also a referral link at the bottom of this article (50% off fees for 6 months – worth $94), so don’t forget to use the link if you’re signing up!

Update (28 Aug 2020) – Do note that StashAway has announced that they will be updating / revising the projected interest rate on StashAway Simple down to 1.4% p.a. starting in September 2020. This makes StashAway Simple significantly less competitive. You can check out Singlife Account instead – pays 2.5% on the first $10,000. Review and Promo Code available here.

Money market funds are a big thing in the US and China. The concept is really simple. You have some spare cash lying around, you pop them in a money market fund, and you earn good interest on them on a daily basis. There are no minimum sums, and there are no lockup periods.

China has their yuerbao (under Alipay), and US, well US has a ton of money market funds.

Unfortunately, this hasn’t been available to Singapore retail investors thus far.

So I was really pleased when I heard about StashAway Simple, which is effectively a money market fund.

Basics: What is StashAway Simple?

Like the name implies, StashAway Simple is actually really simple.

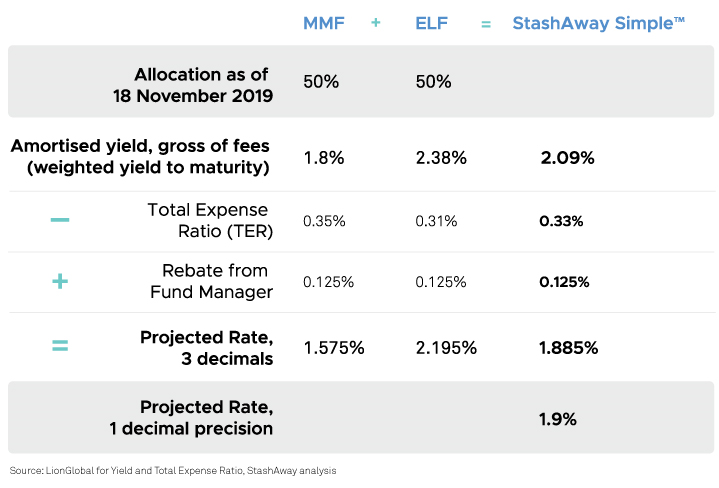

You put money into StashAway Simple. They invest in 2 underlying funds equally (50-50), LionGlobal SGD Money Market Fund, and LionGlobal SGD Enhanced Liquidity Fund SGD Class I Acc.

LionGlobal SGD Money Market Fund and LionGlobal SGD Enhanced Liquidity Fund SGD Class I Acc essentially invest in short term, low risk bonds.

StashAway Simple then pays you interest on a daily basis.

There is no minimum sum, and no lock up period.

So whenever you decide to take the money out, you’re able to take it out, and you earn interest up until the day you take it out.

It’s like a Fixed Deposit or Singapore Savings Bonds, only much much better (in theory).

What’s good about StashAway Simple

Institutional Fund Class

You’re investing in the institutional fund class, which means that you get to enjoy the fees typically paid by institutional clients (lower than those paid by retail investors). The way it works is that you pay the retail class fees upfront, and every quarter the fund manager rebates the difference between the retail class and the institutional class to StashAway, and StashAway rebates that amount to you.

This is actually a great reason to go via StashAway, because if you buy it directly via FSMOne, you’re buying the retail class and paying the higher retail investor fees.

On top of that, StashAway doesn’t charge you any fee for using this service (unlike the usual investment product), so it’s really a great deal. StashAway is probably using this as a way to garner publicity and get cheaper customer acquisition, which is great for customers like you & me.

Great returns, no lockup, no minimum sum – Too good to be true?

StashAway Simple’s projected return is 1.9% per annum.

By contrast, the highest fixed deposit now offers about 1.85%, subject to minimum of S$20,000, with a 12 month lockup.

The Singapore savings bond offers about 1.56% for one year, and you need about 1 month’s notice to redeem the bond.

| Year from issue date | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

| Interest % | 1.56 | 1.56 | 1.56 | 1.66 | 1.72 | 1.72 | 1.76 | 1.82 | 1.87 | 1.91 |

| Average return per year %* | 1.56 | 1.56 | 1.56 | 1.58 | 1.61 | 1.63 | 1.65 | 1.67 | 1.69 | 1.71 |

So for StashAway Simple to offer 1.9%, with no minimum sum, and no lockup, seems like a really great deal actually.

Too good to be true?

There’s a saying here on Financial Horse that goes like this, if something’s too good to be true, it probably is.

StashAway Simple is a great product there’s no doubt about it, but there’s definitely some downsides to it.

Returns are not guaranteed

Update (28 Aug 2020) – Do note that StashAway has announced that they will be updating / revising the projected interest rate on StashAway Simple down to 1.4% p.a. starting in September 2020. This makes StashAway Simple significantly less competitive. You can check out Singlife Account instead – pays 2.5% on the first $10,000. Review and Promo Code available here.

And the first one of course, is that returns are not guaranteed.

According to StashAway: https://www.stashaway.sg/faq/360038638114-how-is-stashaway-simple-projected-rate-calculated

The math on the projected rate of returns is quite straightforward: StashAway Simple™ returns are the sum of the amortised yield from the underlying funds, minus fees charged by the fund managers, plus any rebates.

We’ll review the projected rate weekly, and in the case that there is a variation of the projected rate of 1 decimal point or more, we’ll notify our clients if there is any variation with 1 decimal point precision (i.e., 1.x%)

As of 18 November 2019, the projections are as follows.

The Total Expense Ratio (TER) for each fund includes the Management Fee charged by the Fund Manager, as well as other expenses incurred by the Fund (e.g., custody, marketing, compliance, shareholder services); as the TER includes fixed costs, it may slightly vary depending on the size of the funds.

What this means is that the 1.9% per annum return is based on a forecast, using projected returns using weighted yield to maturity of the underlying bonds. They are not guaranteed, unlike a fixed deposit or Singapore savings bond.

And the tricky thing about using weighted yield to maturity of bonds when the bonds are short term, is that there will be huge volatility in future returns.

As an example, the weighted duration of LionGlobal SGD Money Market Fund is 0.3 years, or about 3 to 4 months. This means that every 3 to 4 months, the entire fund’s worth of bonds will mature, and will be refreshed. This also means that every 3 to 4 months, the future return of the fund will be reset to the prevailing market rate.

This isn’t necessarily a bad thing. In fact, it’s a fundamental limitation of all money market funds and short term bond funds. It’s just something that you need to take note of when investing in StashAway Simple. By contrast, when you’re investing in fixed deposits or Singapore savings bonds, you’re effectively locking in the interest on the day you create them. Not so much for StashAway Simple.

Of course, this works both ways as well. So when interest rates are going up, these things could be great because you get all the upside of the increase in short term interest rates. But when interest rates are going down, your interest rate gradually drops too.

What will future returns be like?

Of course, the next question here is going to be, what will future returns look like? Future returns are always tough, because it requires a prediction of where interest rates will be in the future, which more often than not is a fool’s errand.

To sidestep the issue, we’ll use the historical returns of the 2 underlying funds here, LionGlobal SGD Money Market Fund and LionGlobal SGD Enhanced Liquidity Fund SGD Class I Acc.

And from StashAway’s calculations, they’re projecting 1.8% return for LionGlobal SGD Money Market Fund and 2.38% return for LionGlobal SGD Enhanced Liquidity Fund SGD Class I Acc. But how accurate are these?

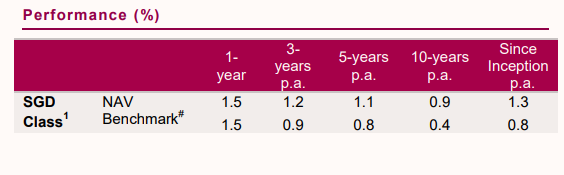

LionGlobal SGD Money Market Fund in particular has been around for quite a while, and I’ve extracted its historical returns below. It’s returns since inception is about 1.3%, it’s 10 year return is 0.9%, and 1 year return is 1.5%. That’s actually a fair bit lower than the 1.8% return StashAway is projecting.

LionGlobal SGD Enhanced Liquidity Fund SGD Class I Acc on the other hand was only incepted in December 2018, so it doesn’t really have a long track record. It’s 6 month return is about 0.8%, which would work out to around 1.6% annualised. Again, it’s a fair bit lower than StashAway’s 2.38% returns.

And if we use both fund’s historical 1 year returns (annualised), it works out to a blended rate of about 1.55%, which after fees, is around 1.38%. So assuming StashAway Simple was around 1 year ago and you bought it then, you’ll probably be sitting on about 1.38% returns, approximately.

That’s a fair bit lower than StashAway’s projected 1.9% returns.

Of course, like every good fund manager will say, past performance is no indicator of future performance. And I do absolutely agree that short term interest rates have gone up since, so the future return could be higher.

But if you take nothing away from this exercise at all, just remember than the projected returns are merely projected returns, and what you actually get in reality, depends on how the future plays out for interest rates. And how the future plays out, is anyone’s guess.

Possibility of Capital Loss

Which brings me to my next point. Money in StashAway Simple is not SDIC guaranteed.

For those who are new to it, SDIC is the Singapore Deposit Insurance Corporation Limited. The way it works is that:

In the event a Deposit Insurance (DI) Scheme member bank or finance company fails, all of your insured deposits with that member are aggregated and insured up to S$75,000 by the Singapore Deposit Insurance Corporation Limited (SDIC). Insured deposits held in trust and client accounts held by non-bank depositors are insured up to S$75,000 per account.

Your monies placed with a Scheme member bank under the CPF Investment Scheme (CPFIS) and CPF Retirement Sum Scheme (CPFRS) are aggregated and separately insured up to S$75,000.

As your insured deposits are covered under the DI Scheme, SDIC will pay you the insured amounts if your bank or finance company fails.

To put it simply, what this means is that when you invest in a fixed deposit with say DBS, and DBS goes bankrupt, the SDIC (government backed) will guarantee all amounts up to S$75,000.

And I know what you’re saying. DBS will never go bankrupt, so this doesn’t matter.

Well yeah, that’s what everyone thought until 2008 too, when banks all around the world were failing, and the government had to come up with SDIC to prevent a run on the bank. SDIC guarantee doesn’t matter most of the time, except when it does, and you’ll really wish you had it.

And likewise, when you’re investing in Singapore Savings Bonds, the money is guaranteed by the Singapore government, so the chance of default is almost zero.

When you invest with StashAway Simple, there is the possibility of capital loss via a default in the underlying bonds owned by either of the Lion Global funds.

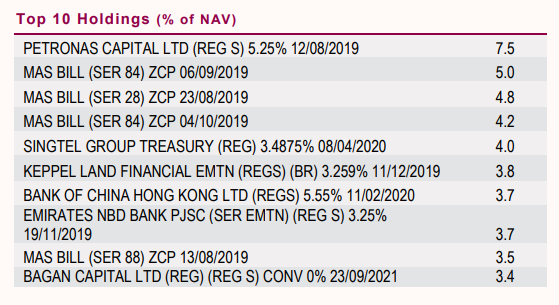

To be fair, I think the risk of this materialising is low because of how safe the underlying investments are. I mean just look at the top 10 holdings of Lion Global Money Market Fund. Petronas, MAS, Singtel, Keppel, BOC HK etc. The chances of a default from one of these players are, objectively, terrifically low.

But of course, there’s no such thing as zero risk in this world, so it’s something to note nonetheless.

How long does it take to withdraw your money from StashAway Simple

*Update December 12*

Just as a quick update – StashAway has confirmed the withdrawal mechanics from StashAway Simple. Essentially, it will take around 3 business days to withdraw your money from StashAway Simple.

So when you decide to pull your money out of StashAway Simple, you just need to notify them, and the money should be withdrawn to your account within 3 business days. That’s a pretty decent timeline actually, so this is a really nice confirmation from them.

Closing Thoughts: Will I invest in StashAway Simple?

Writing this article has made me realise how efficient the market is.

If you want something with zero risk and zero lockup, you need to go with the Singapore Savings Bonds with the lowest interest at 1.56%.

If you want something with zero risk but are okay with a one year lockup, you go with fixed deposit with a 1.85% return.

If you are okay taking on a bit of risk, and don’t want any lockup, you go with StashAway Simple, with a 1.9% projected return.

All 3 are very different products, and cater to different kinds of investors. The market is efficient that way.

Would I invest in StashAway Simple?

To be honest I think it’s a very good product, giving retail investors the chance to invest in institutional class money market funds.

I’m not so sure how the 1.9% will play out going forward, so there’s some uncertainty on that.

But yeah, if I have some money lying and it’s generating zero interest, I just might pop some into StashAway Simple for a while, since any interest I earn is still better than nothing. But longer term though, there’s going to be huge volatility with StashAway Simple’s returns, so I may prefer Singapore Savings Bonds (or fixed deposit) if I can get it at the right interest rate.

StashAway Referral Link

For those are new to StashAway, you can use the referral link below for Financial Horse readers. You get 50% off your fees for the first SGD 50,000 invested for 6 months. That’s about S$94 saved on fees, so it’s well worth your time.

Note: This fee waiver doesn’t apply to StashAway Simple because StashAway Simple has no fees. But this will help if you decide to invest with StashAway down the road, so I do recommend using the link if you decide to check it out.

Will you guys invest in StashAway Simple over a fixed deposit or SSB? Share your comments below!

Looking for a comprehensive guide to investing? Check out the FH Complete Guide to Investing for Singapore investors.

Support the site as a Patron and get market and stock watch updates. Big shoutout to all Patrons for their support!

Like the Financial Horse Facebook Page and join the Facebook Group (Singapore) or Facebook Group (China) to continue the discussion!

Hi FH, what do you think of an equal weighted portfolio Of Stashaway (their flagship investment product) + MoneyOwl (dimensional funds) using srs funds?

Hmm, I think that could be really interesting actually. What risk level would you be setting?

Prolly the second highest risk setting for money owl. 80% equity, 20% short term bonds. Haven’t studied stashaway’s offerings yet so can’t comment on that one.

My rationale is srs funds are limited to investing in sgx listed equities and etf. For the global etfs like s & p 500, liquidity is v poor.

Money owl and stash away helps me to get geographical diversification, helps me to avoid paying tax on my bond income, and helps me get exposure to foreign bonds. Mixing the two gives me exposure to small / large caps as well.

So what I’m saying is, I’m unable to replicate money owl and stash aways offerings with my srs funds. Which makes both compelling options.

Interesting. That’s quite a lot of risk exposure there though. It really depends on what kind of investor you are I guess (and your risk appetite).

For me personally, I’ll probably still do DIY investing because I like to have full control over what goes into my portfolio. So I use SRS as a small component in my overall portfolio, instead of needing to have SRS be a complete asset allocation in itself (which seems like what you’re trying to do).

Cheers!

Hi, thanks for the analysis.

For purposes of the default analysis, I don’t really understand the linkage between the Lion Global Money Market Fund and the underlying Stashaway Simple Money Market Funds (ELF and MMF).

Are the ELF and MMF 100% feeder funds into the Global Money Market Fund?

Hi there! StashAway Simple invests equally in ELF and MMF. So if you put $100 with StashAway simple, $50 goes to ELF, and $50 goes to MMF.

That’s really all there is to it. StashAway Simple merely facilitates the investment.

Hope this helps!

Hi Financial Horse,

What are your thoughts on FSMOne’s new ETF RSP plan? https://secure.fundsupermart.com/fsm/article/view/15709/etf-rsp-with-fsmone-the-investment-world-has-gotten-that-much-easier-to-invest-into

Am a huge fan of your blog and would love to hear your thoughs 🙂

Hmm that’s an interesting question. I’m generally not a fan of RSPs/DCA unless the amounts in play are very small. I prefer just manually investing so I retain full control of when the money goes in, but this may be unique to me. I’ll see if I can do an article to share my thoughts on this soon.

[…] Read financial horse’s review on this produce here. […]

I also conducted sanity check on this portfolio, for the past 1 year, MMF and ELF generates NAV return of ~1.5% and ~1.8% respectively, which appears to be far off the 1.8% and 2.38%.

HOWEVER, kindly correct me if I misunderstood, there is a confusion of NAV and TAV (total asset value) here.

NAV = [TAV-Mgt Expense Ratio(MER)] / Number of Outstanding units.

The 1.8% and 2.38% should be TAV. If they are deducted by MER = 0.35% or 0.31%, we would obtain NAVs more or less in line with the figures in the lion global website.

To me, the attractiveness falls within:

– ELF is not easily accessible to us, from other sources like FSM.

– The rebate is attractive.

Yes, absolutely agree with your 2 points! 🙂