I’ve been thinking a lot about SingTel and the future of Telcos recently.

And my thoughts are best summed up with a story.

The story of Reliance Jio

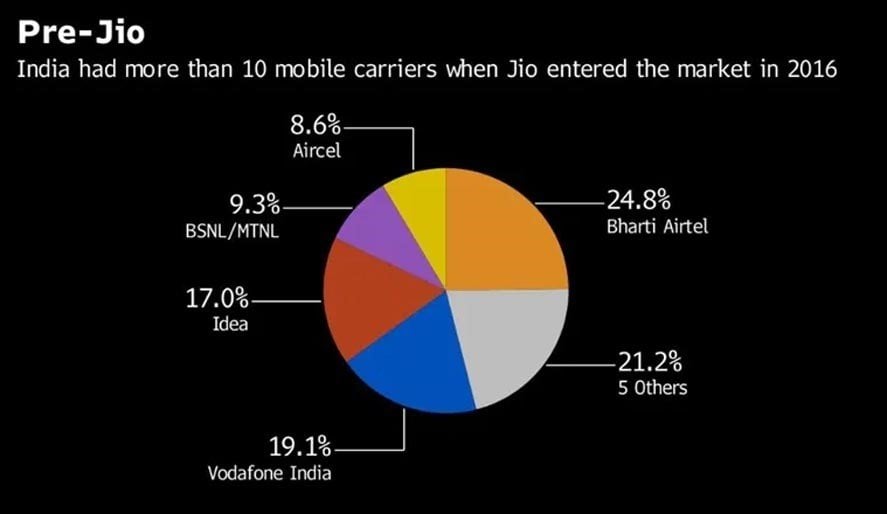

The year is 2016, and India’s telco market is dominated by 5 – 6 main players.

Mukesh Ambani, an Indian billionaire, decides that he wants to go into the Telco space.

The business strategy is to offer free services. Reliance Jio heavily subsidizes the cost of a phone plan, and uses viral marketing and referrals to grow market share aggressively.

Consumers love a free service, and Reliance Jio grows well.

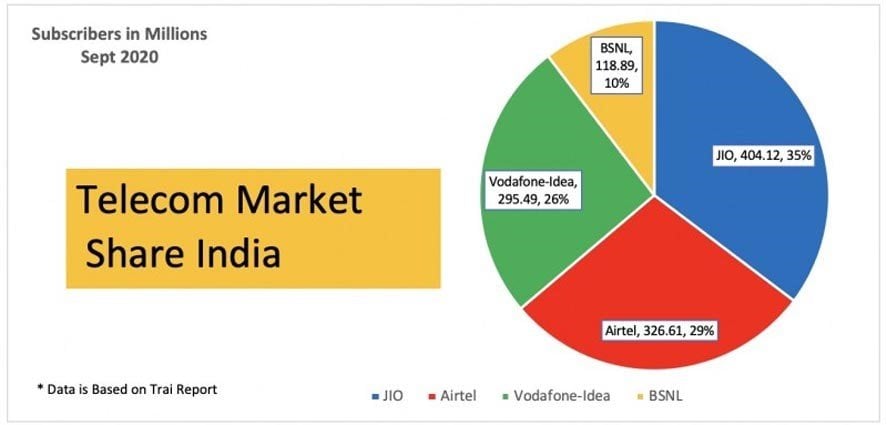

By Sept 2020, the market has consolidated into 4 main players.

Reliance Jio went from 0% market share to 35% in 4 years:

With the market share that Reliance Jio has, they sell value added services to users (or at least they try to).

Entertainment, digital commerce, payment, healthcare, manufacturing etc. They’re trying to become the Tencent or Meituan of India.

And they sell this dream of targeting the Indian consumer to global investors and tech companies.

Who love the story.

Reliance Jio has raised over $15 billion to date, with $4.5 billion alone coming from Google.

You can see the list of investors below, it’s a really impressive list:

- Facebook,

- Alphabet Inc’s Google

- Silver Lake,

- KKR & Co,

- Abu Dhabi Investment Authority,

- TPG

- Public Investment Fund of Saudi Arabia

- Qualcomm

- Intel Corp

What’s the moral of the story?

FYI, Bharti Airtel, the No. 2 player in India, is Singtel owned.

And this, is what Singtel is competing with.

This, to me, is the future of Telcos.

The future of Telcos is not about operating a Telco business and selling phone plans. It is about using the Telco business to achieve a deeper underlying goal – whether it is to build a digital platform (Reliance), or to invest in disrupters (Softbank).

In other words – The Telco business is a means to an end, not an end in itself.

Just look at Softbank.

Investors didn’t invest in Softbank because they were bullish on the Telco business.

They invested in Softbank because they believe in Masayoshi Son’s vision, and they were willing to bet on the man. The Telco profits were used to invest in tomorrow’s Alibaba and Uber.

Singtel’s problem today

Singtel’s business model today, is selling phone/internet services to consumers and businesses across SEA.

Selling a commoditized service, with zero pricing power.

All COVID did was accelerate the decline. The structural factors for the decline have already been here for a while:

- Increased competition from new players squeezing prices

- Commoditized service – no pricing power

- Value add is in the software the runs in the “pipes”, not the pipes themselves

The days of selling phone plans on a 2 year lock in at $60 a month are over.

Singtel needs to find a way to replace those earnings, fast.

Note: The research for this article (and most of the charts) are sourced from ShareInvestor Webpro. The platform offers 10 years of financial data across 7 markets, along with charting tools, screeners, insider trades, consensus estimates and more!

Sign up in the month of July to enjoy an additional $20 off.

Learn more in my review on ShareInvestor Webpro here.

Singtel’s problem… in 1 chart

Okay maybe 2 charts.

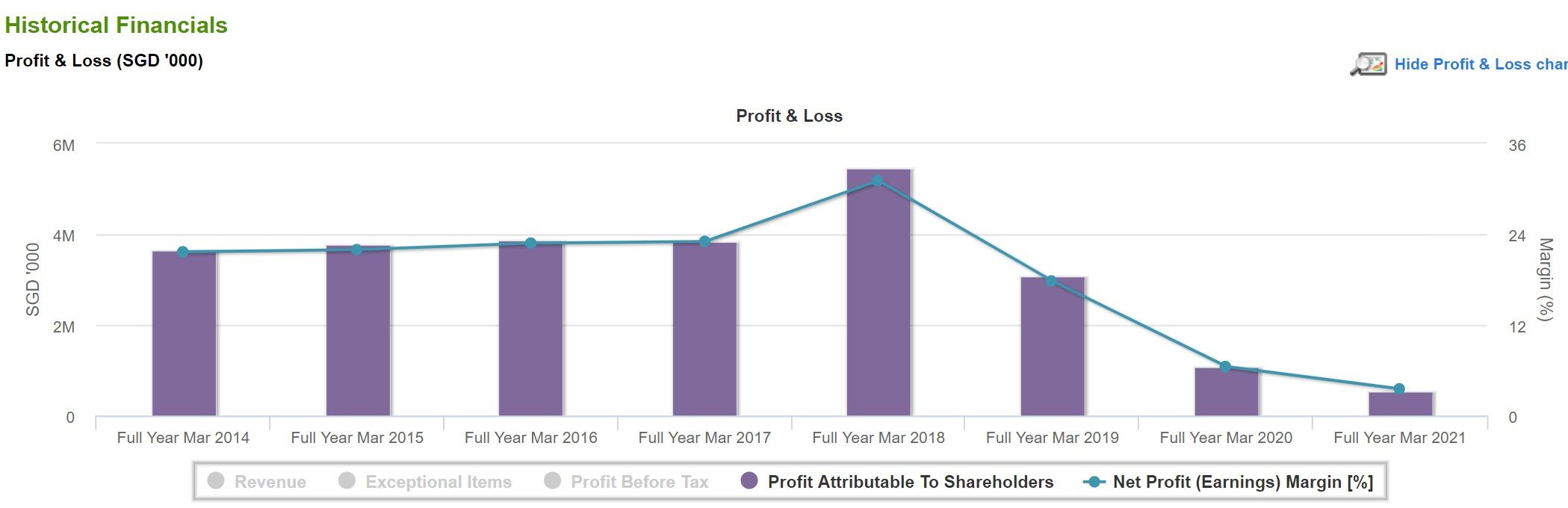

Singtel’s revenue has been flat for 8 years.

Just think about that for a minute.

This is a company that as the entire smartphone revolution was playing out, stayed on the same business model and collected the fat margins, while the world was changing around them.

Singtel’s profit dived after 2018.

As with most things in life, change was slow, then all that once.

Profits were flat from 2014 to 2018.

And then took a nosedive after 2018 as the pace of change accelerated.

New Singtel CEO to shake things up – Strategic Review

The good thing is that Singtel knows this is a problem.

So out went the ex-CEO (Chua Sock Koong, who was CEO from 2007 to 2020 – 14 years).

And in came a new CEO, Yuen Kuan Moon.

Who promptly organised a big “Strategic Review”.

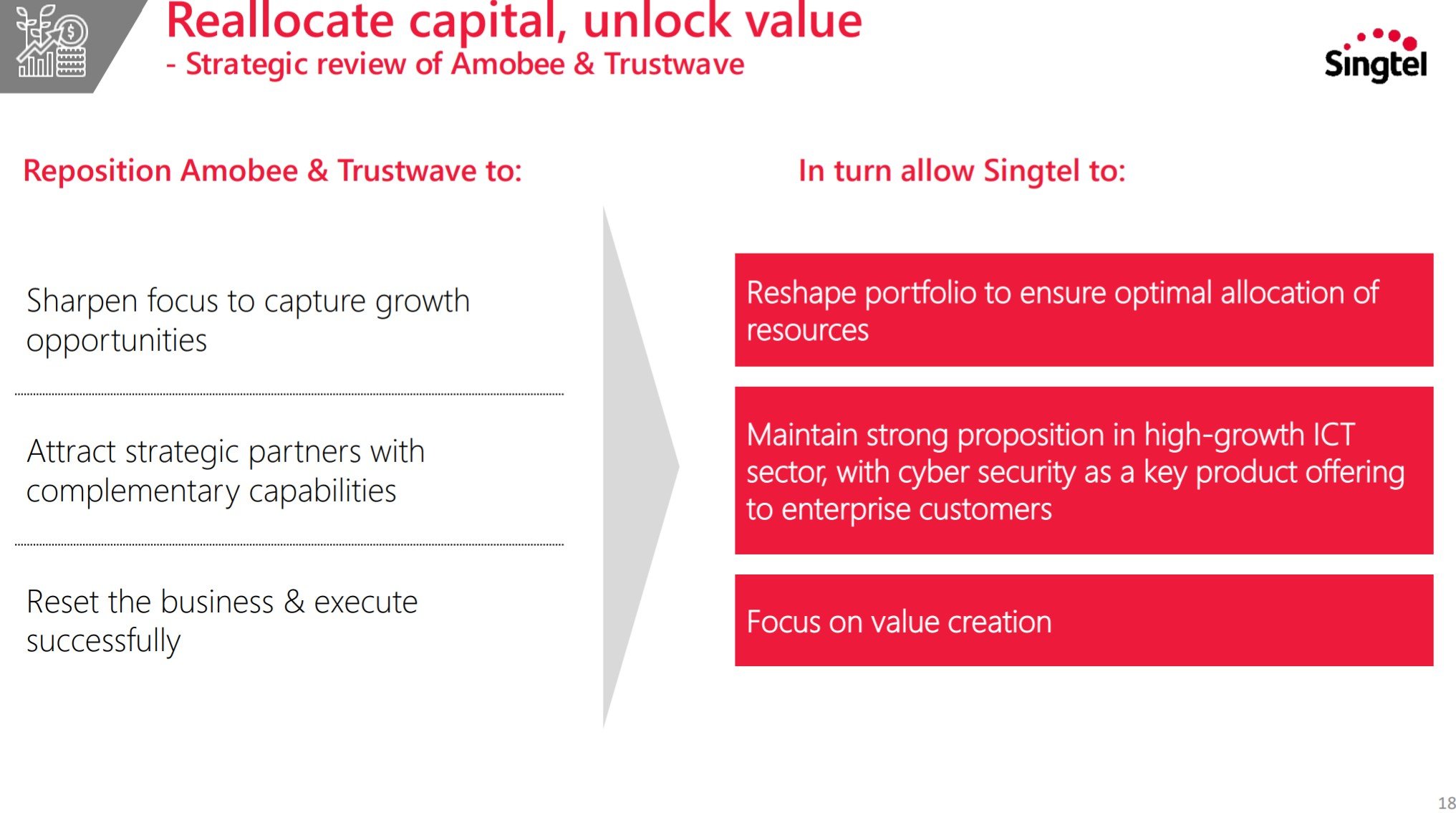

Singtel’s “Strategic Review” Explained

Now I poured over a ton of corporate speak before I finally figured out what the Strategic Review was.

The Strategic Review basically, is similar to what SPH is trying to do.

It is to (1) sell the old world assets to free up cash + Balance sheet (eg. mobile tower and rooftop sites). And (2) use that cash to reinvest into new world businesses.

Why didn’t they just say that?

If you think about it, this is the same strategy across all the Temasek portfolio companies:

- CapitaLand (selling offices/retail and buying data centers, family housing, warehouses)

- Keppel/Sembcorp (selling marine and O&G, focussing on renewables)

- SIA (survive and buy out/outcompete regional airlines with the balance sheet)

(1) Sell old world assets

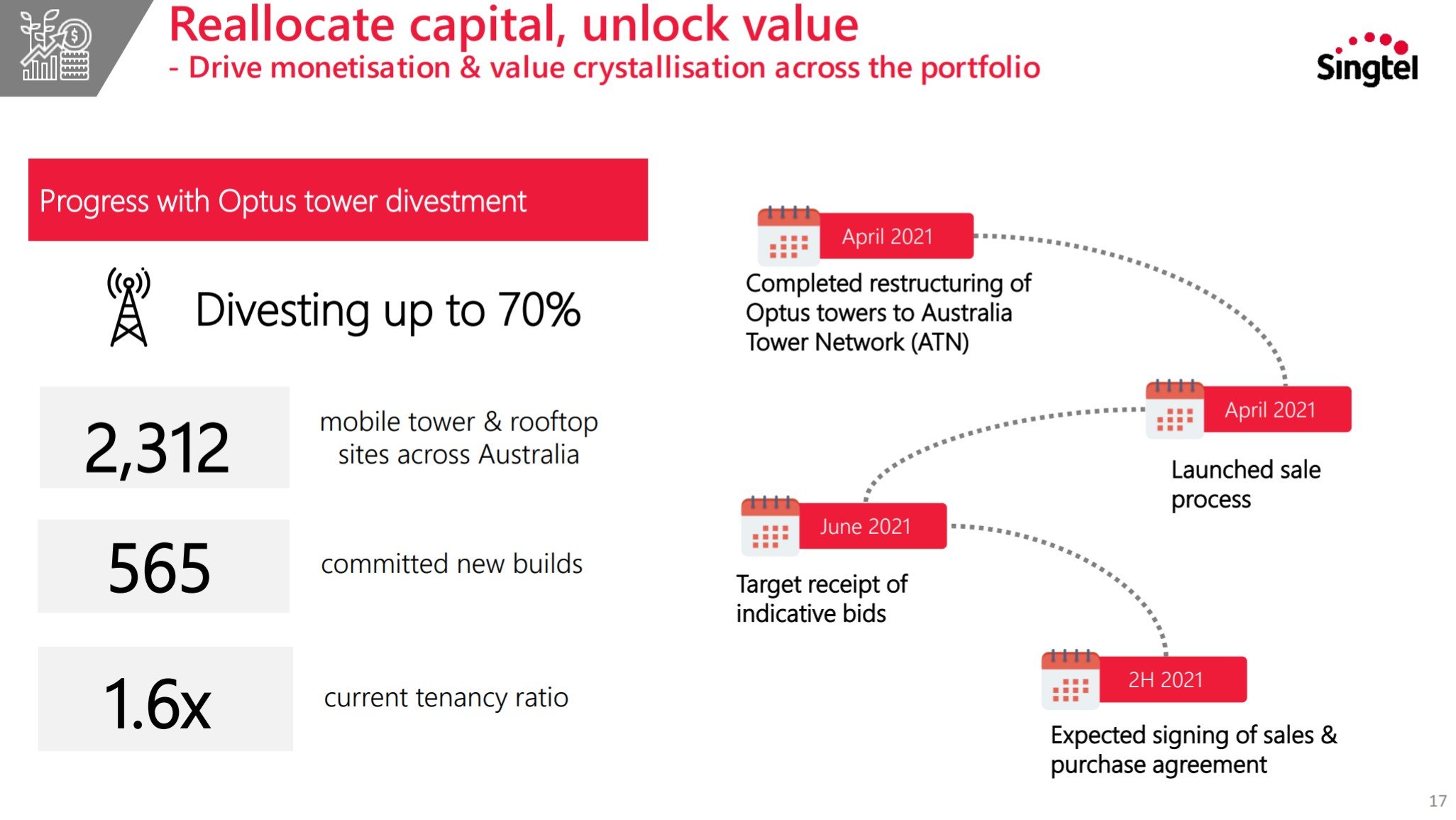

Singtel is selling a 70% stake in the Optus Cell Towers in Australia.

This is basically the Australian version of Netlink (cell towers).

Should free up about $2-3 billion from this sale – with more down the road.

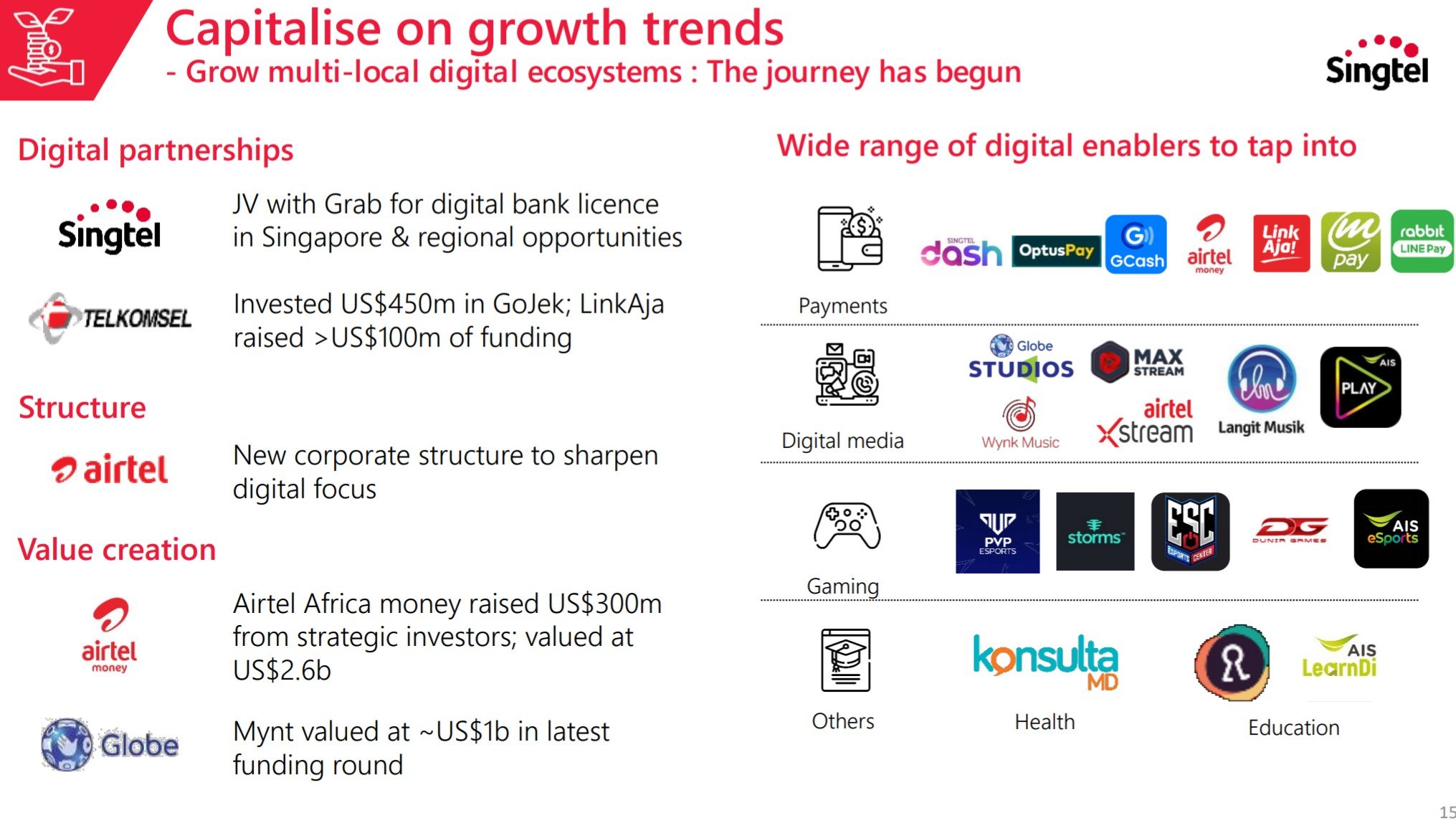

(2) Invest in new world businesses

And with that cash, Singtel will invest in new world businesses.

Like the Singtel-Grab Digital Bank. Or 5G.

And they’re also looking at payments, digital media, and gaming.

My biggest concern – Can Singtel execute the “Strategic Review”?

Now don’t get me wrong, I love the Strategic Review.

I think it’s a very ambitious plan.

They’re trying to become the Tencent / Softbank of South East Asia. Heck even the Reliance Jio of SEA.

The problem though – is that they’re trying to do so with the management structure of an old-world legacy company.

The track record hasn’t exactly been amazing.

Food website Hungrygowhere is an interesting case study – it had so much potential as an online food destination, but nothing came out of it.

Video streaming platform Hooq as well. This Horse is old enough to remember when Hooq was being sold to shareholders as a future Netflix. Only to be liquidated in March 2020.

And now they’re talking about “unlocking value” and “value creation” from Amobee and Trustwave.

I mean I really want to trust Singtel on this, but I do have concerns here.

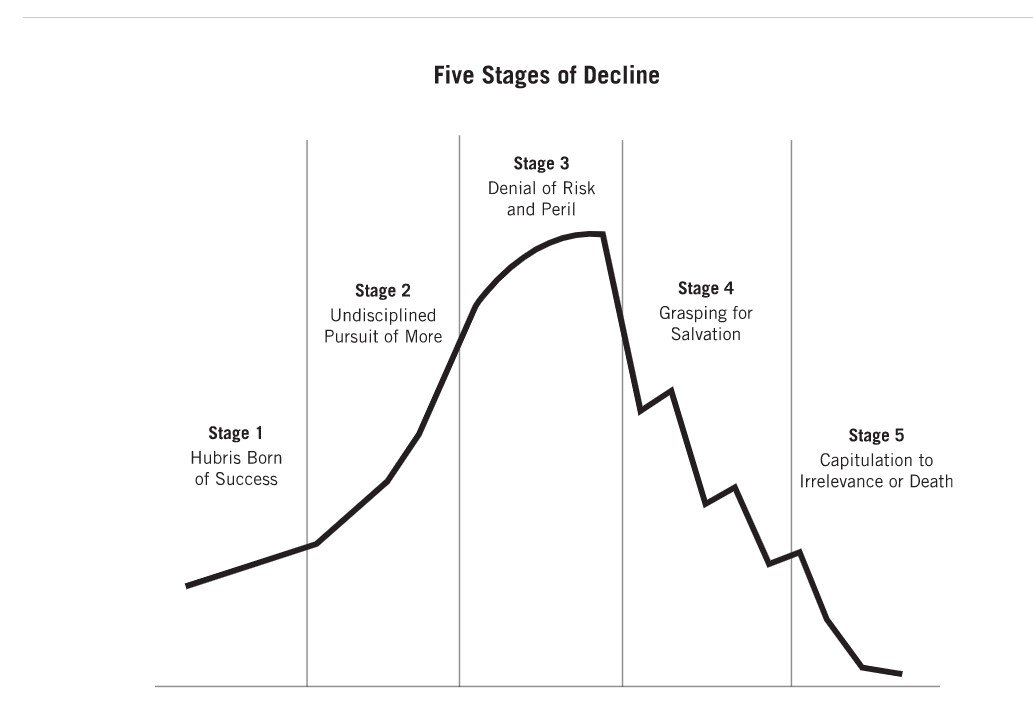

Jim Collin’s Five Stages of Decline

Jim Collins has a great book How the Mighty Fall, where he studies how giant companies fall.

He splits it into 5 stages:

- Hubris born of success – Companies are drunk on success and become arrogant, losing sight of the factors that created the original success

- Undisciplined pursuit of more – They make undisciplined leaps into areas they cannot compete with excellence

- Denial of Risk and Peril – Internal warnings signs mount, but external results are strong enough to explain away the disturbing data

- Grasping for salvation – The decline is now obvious to all. How does leadership respond? By lurching for a quick salvation or by getting back to the disciplines that brought about greatness in the first place?

- Capitulation to Irrelevance or Death – The longer a company remains in Stage 4, repeatedly grasping for silver bullets, the more likely it will spiral downward.

What stage of decline is Singtel in?

If I were to guess, I would probably put Singtel at an early stage 4 (or late Stage 3).

The good news (according to the book), is that hope is not lost yet.

At Stage 4, if the company goes back to its roots, back to the disciplines that made it great in the first place – the company can be turned around to go on to greater heights.

Whether Singtel can do that, is the million dollar question to me.

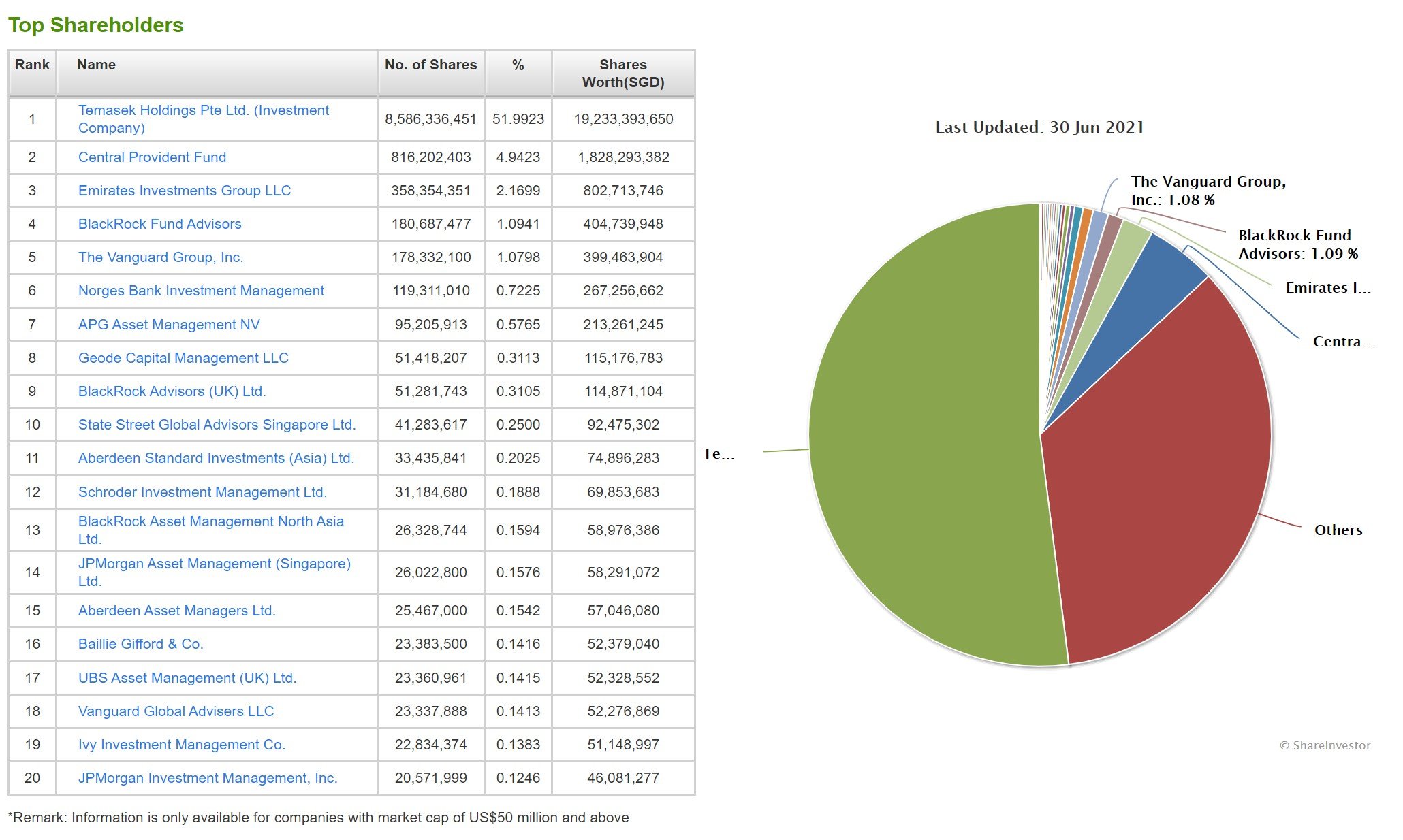

Singtel’s Ownership

Note: ShareInvestor WebPro is a great and very cost-effective way to do analysis like this – beats trawling through the SGX announcements one by one. If you do such analysis regularly, worth checking it out here.

Singtel is 51% owned by Temasek, so that helps.

Push comes to shove, a Temasek led restructuring / fundraising is always an option, just like we’re seeing with Keppel or Sembcorp or SIA or CapitaLand.

I don’t think we’re there yet though.

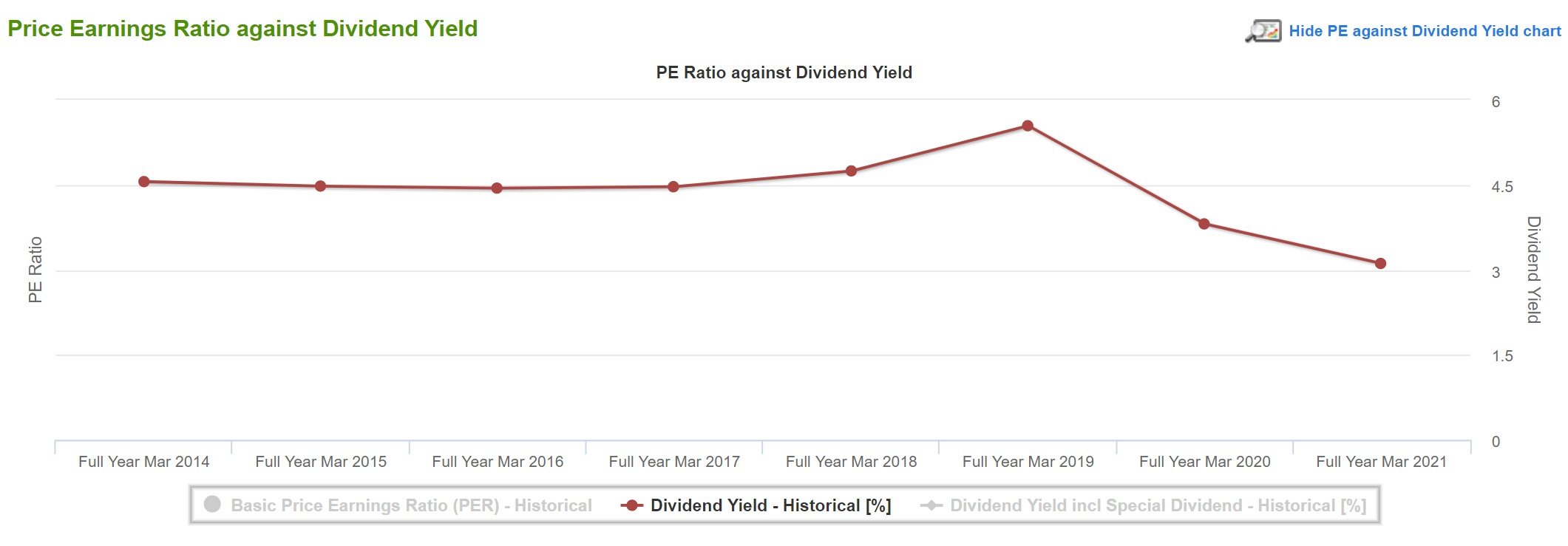

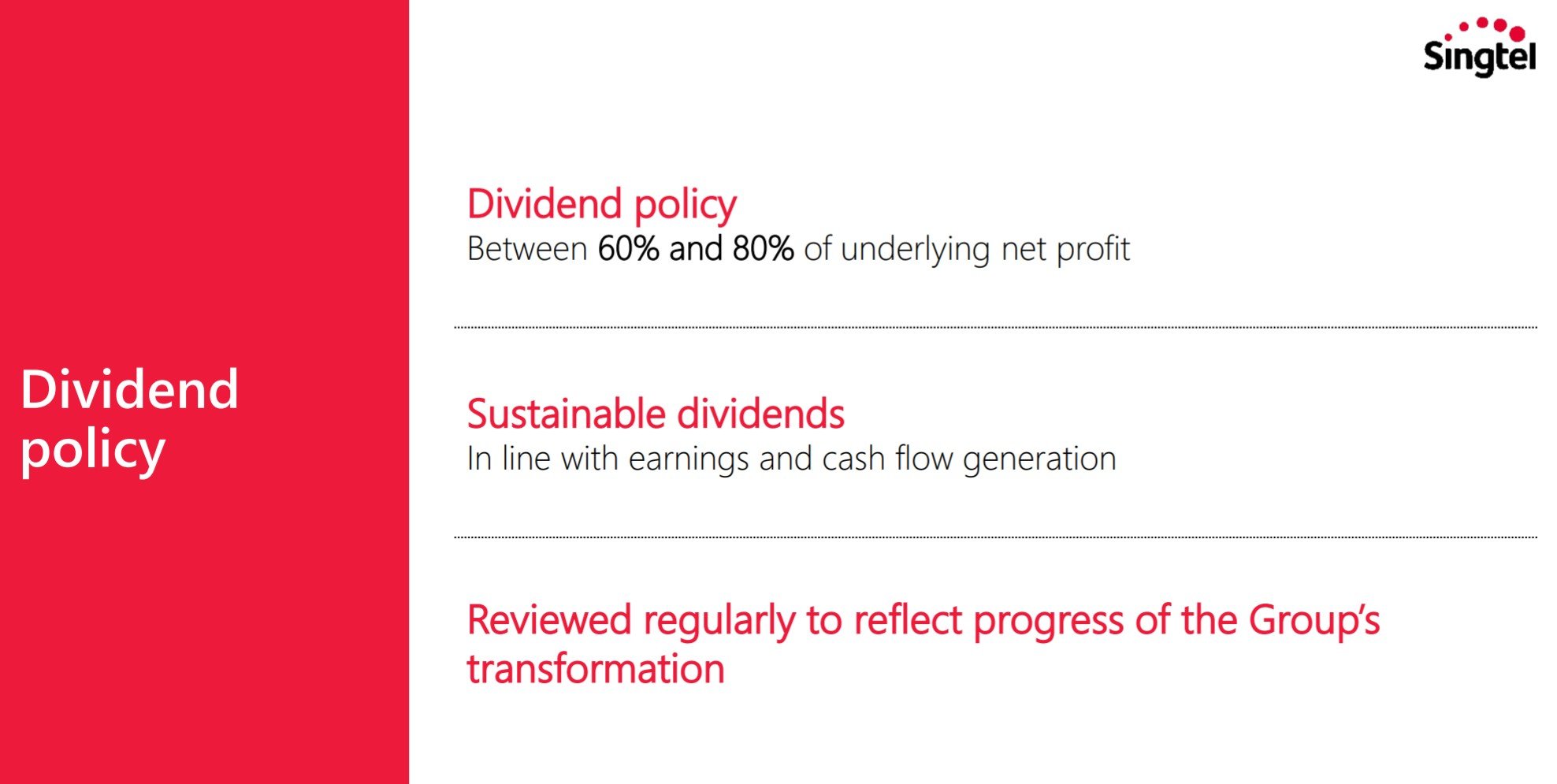

Singtel’s 3.3% Dividend

Trailing twelve month dividend is 3.3%, at a 71% payout ratio

Funnily enough Singtel has committed to pay out 60% – 80% of their profit going forward.

It’s tough to see how Singtel can maintain this dividend, while executing the strategic vision (which is going to require a ton of cash).

Perhaps that’s where the sale of the cell towers comes in. Either way, it’s a tough position to be in, and I don’t envy them.

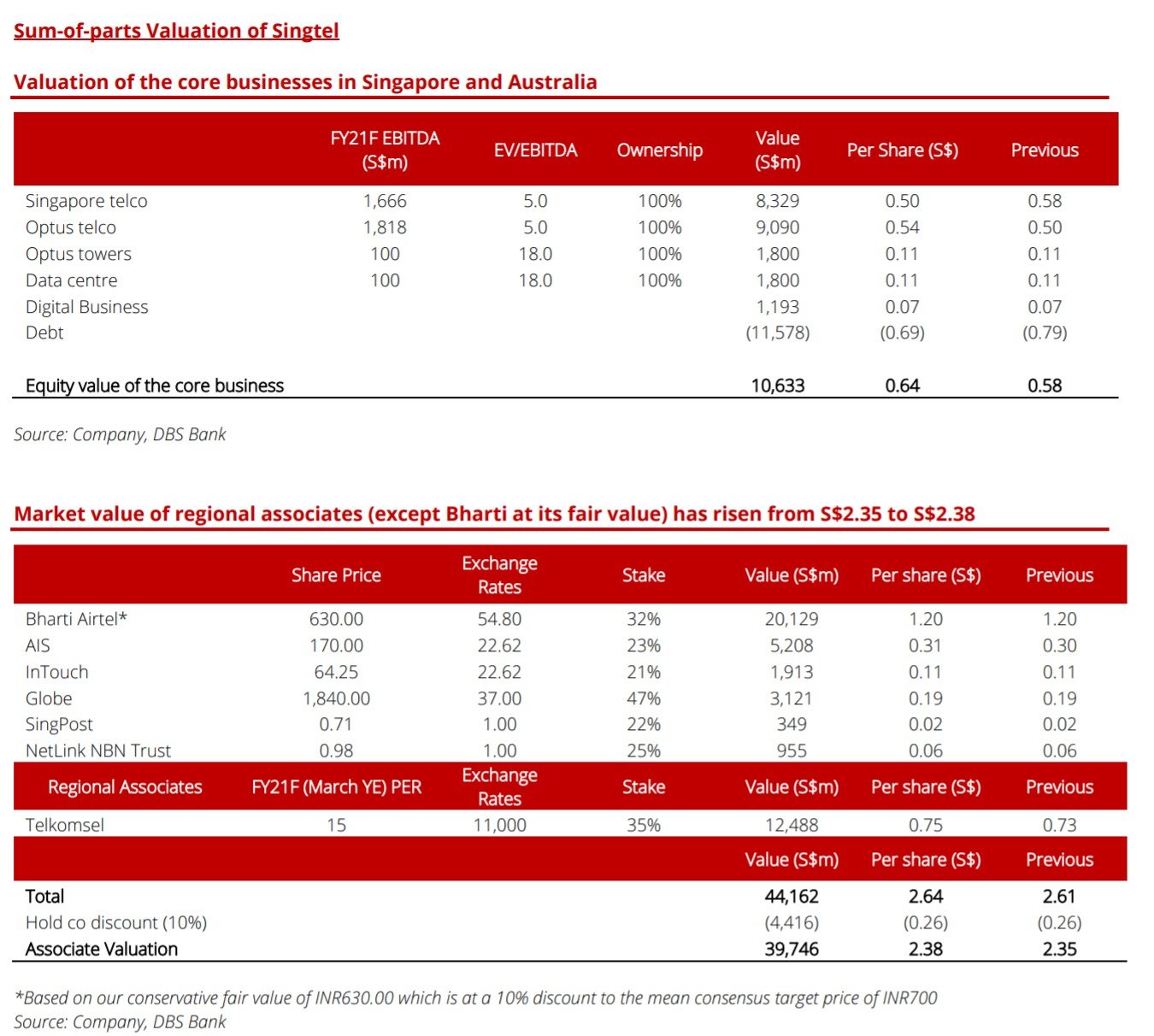

Valuation of SingTel

DBS has a sum of the parts valuation that values Singtel at $3.

I don’t disagree, that’s probably the value if you break up Singtel and sell it for parts today.

The problem though, is that the Telco business will continue to decline, so the value in 2 or 3 years could be significantly lower.

If you buy into Singtel today, you’re buying into their vision on digital transformation.

And not into a sale for parts strategy.

Would I buy Singtel at $2.2?

I exited most of my Singtel position for a small loss last year at the $2.5 range.

So far at least, that’s been the right decision.

And the more I think about it, the more I’m worried about Singtel.

They need to manage the decline of their core legacy business (and sell it to raise cash), while managing investments into new digital transformation.

The skillsets for the two are fundamentally different.

One requires you to move fast and break things, the other requires you to take a measured approach.

Executing on either task is already no mean feat, executing both at the same time is like trying to turn around an oil tanker in the Suez. Not easy.

Closing Thoughts: Do or do not, there is no try

To me at least, Singtel is at a crossroads.

They either go on to become the Softbank / Reliance Jio of South East Asia.

Or they gradually fade away as the core business goes into structural decline.

It’s hard to see Singtel remaining static at where they are now, for the next 3 to 5 years.

As a Singaporean, I love Singtel, and I want to see them succeed. I want to see Singtel go back to its heyday in the 2000s, when they were going around South East Asia buying up regional players.

But as an investor, I want to see some results before I go in (again). I want to see management team execute and deliver on the “Strategic Review”. And if I have to miss some of the initial rally, so be it.

For now at least, I see better places to deploy my capital elsewhere.

Especially with the China tech sell-off, and US cyclicals starting to roll over. I think 2H2021 is going to be volatile (with possibility of a correction), and I’ll share more thoughts on it this weekend.

For now, you can check out my latest thoughts, stock watch, and personal portfolio on Patron.

Let me know what you think of Singtel! Turnaround play or value trap?

Join our Reddit community at r/SingaporeInvestments

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Both are THE best quality investment courses available to Singapore investors out there!

Good insights, thanks. I do agree that viewing it as a turnaround/digital transformation play is a long shot and you likely wont get value there. Where I disagree is the decline of core earnings. Yes, revenue and margins have declined over the past few years, but this is not SPH where you literally have an old core (print) that wont be around in 5 years time. I can see certain parts of the telco revenue stream not being around in the future, say voice, roaming but we will still require data etc… which provides a base of earnings. Telcos are inherently cyclical with the capex/upgrade cycle and competition. We are nearing the end of 4g and countries always continuously move from 3 players to 4 players then back to 3 again and so on. So I do think we are just at trough revenue, trough earnings and not a structural decline of the core business.

However, I would argue that through monetizing Optus towers or other subsidiaries, you will get a right sizing of the business and excess cash for buybacks, dividends or debt reduction. In other words this is essentially an asset play and not an earnings play, if we had to define buckets. And as such is a less volatile holding that is slowly on its way to eliminate its holdco discount. Essentially, a higher returning bond like holding for your portfolio instead of your typical high risk high return equity. Perhaps framing it in the portfolio sense is where we differ.

Hi Ed, that’s a very interesting perspective, and thank you for raising this.

I don’t disagree with you, that’s definitely one way of seeing Singtel. I guess my concern is what would it take for the market to realise this, and what catalyst (if any) is required for that to happen. Or is it just a case of watching management continue to unlock value, until such time as the market comes to value Singtel properly.

Definitely possible though.

Hi

Another great write-up again.

I am not an expert in telco or digital, but what comes to my mind is the question, by pivoting to digital now, is it too late to the party? Especially considering your point that they have an old legacy structure but the areas they are pivoting to are more competitive.

It will very likely come down to execution. Financially, they have the backing of a SWF, so no worries there. With the recent shake-ups and pivoting at the GLCs, there seems to be no shortage of willpower as well (at least on the surface).

That’s a great point Robert – I agree with you on this.

Singtel’s probably slightly late to the party, but like the saying goes – the best time to start was yesterday, the next best time is today. If Singtel executes well, they can still overcome the difficulties.

That said it’s the execution that worries me. The backing and willpower is there, but do they have the flexibility, nimbleness, and management culture to execute and deliver? The skillset it takes to succeed in today’s digital world is quite different from that of the old world infrastructure based world.

Will be monitoring closely, and if I see signs of a turnaround, the current price will look very cheap. 🙂

Good article. Aside from being late to the party does a traditional state controlled business really know how to compete in the digital economy? Chua Sock Koong was CFO for ages before she became CEO. I met her a number of times. She was complacent and arrogant with a not invented here attitude who did much to devalue the brand.

I don’t know Yuen Kuan Moon but he is another SingTel insider who has worked there for years. They need a outsider with real vision and experience in the new digital economy but Singapore Inc. doesn’t seem willing to appoint a foreigner.

Good article. Aside from being late to the party does a traditional state controlled business really know how to compete in the digital economy? Chua Sock Koong was CFO for ages before she became CEO. I met her a number of times. She was complacent and arrogant with a not invented here attitude who did much to devalue the brand.

I don’t know Yuen Kuan Moon but he is another SingTel insider who has worked there for years. They need an outsider with real vision and experience in the new digital economy but Singapore Inc. doesn’t seem willing to appoint a foreigner.

Thanks, great comment. I agree that this is an issue, which is why it will be interesting to watch the execution. Will management be able to deliver results, or is it just talk?

The key word is transformation. Even laid back government agencies were doing it for the past 5 years at least. I agree it’s better late than never but the key is both mindsets and execution. They need to have the people yet to do it well, we should look out if they are hiring the right ones. If you can please do a follow up article on their key personnel. Thanks

Agreed. Saying you want to do something, is not the same as actually doing it. Execution is tough.

Another insightful article from you. Good to bring in Jio and SoftBank as a comparison, makes it so much easier to understand the differences. It’s a disruptor vs defender mindset and culture. When I read and listened about NCS rebranding, behind all the buzzwords, it is still fundamentally the same approach – throw everything on the wall and hope some will stick. It’s still about doubling down on everything you have seen and can see. It’s tough to say no when it’s in your hand.

That’s a fantastic way of putting it – defender vs disruptor mindset. That’s exactly it.

When faced with a changing world, how do you respond? Do you stand and defend your turf, or do you go out and build a new turf?

Speaks a lot about one’s mindset. 🙂