Ask any financial advisor how to begin investing as a young investor today, and chances are the answer will be to “dollar cost average into the STI ETF, hold it until retirement, and let the power of compounding do its work”. The big local banks have even built a Regular Savings Plan around this concept, allowing you to invest a fixed amount of funds every month into the STI (POSB Invest-Saver, OCBC Blue Chip Investment Plan and POEMS Share Builders Plan).

How sound is this strategy? Over the course of 30 years, will this strategy double or triple your money? Will it keep up with the other major global indices?

I am going to set out 3 fundamental reasons why I am not a huge fan of the STI.

Basics: STI ETF

Basics first, the STI ETF (SPDR STI ETF or Nikko AM STI ETF) is an exchange traded fund listed on the Singapore Stock Exchange. It owns a basket of stocks similar to the Straits Times Index.

The Straits Times Index (STI) consists of the top 30 companies listed on the Singapore Stock Exchange (SGX). This index is jointly calculated by SPH, FTSE and SGX.

The STI ETF mirrors the performance of the STI Index very closely, by buying and selling stocks to achieve the same composition as the index. It charges an annual expense fee of 0.3% (SPDR) to 0.35% (Nikko AM), as the management fee.

- Historical Performance

A picture speaks a thousand words, and the chart below plots the performance of the STI (excluding dividends) against the other major global indexes for the past 30 years.

It is evident from this chart that buying and holding an ETF can make you wildly rich. However, the index you pick is of critical importance. You would have achieved a 20 times return for the NASDAQ and 10 times for both the Hang Seng and S&P 500. By contrast, the STI would have returned about 2.5 times your money (CAGR of about 4.8%).

The STI has massively lagged other global indices. And bear in mind that the past 30 years was a period of unprecedented, transformational change, catapulting Singapore from developing country status to a financial capital of South East Asia, the envy of the world. Can we replicate this performance, or better yet, outdo ourselves in the next 30 years?

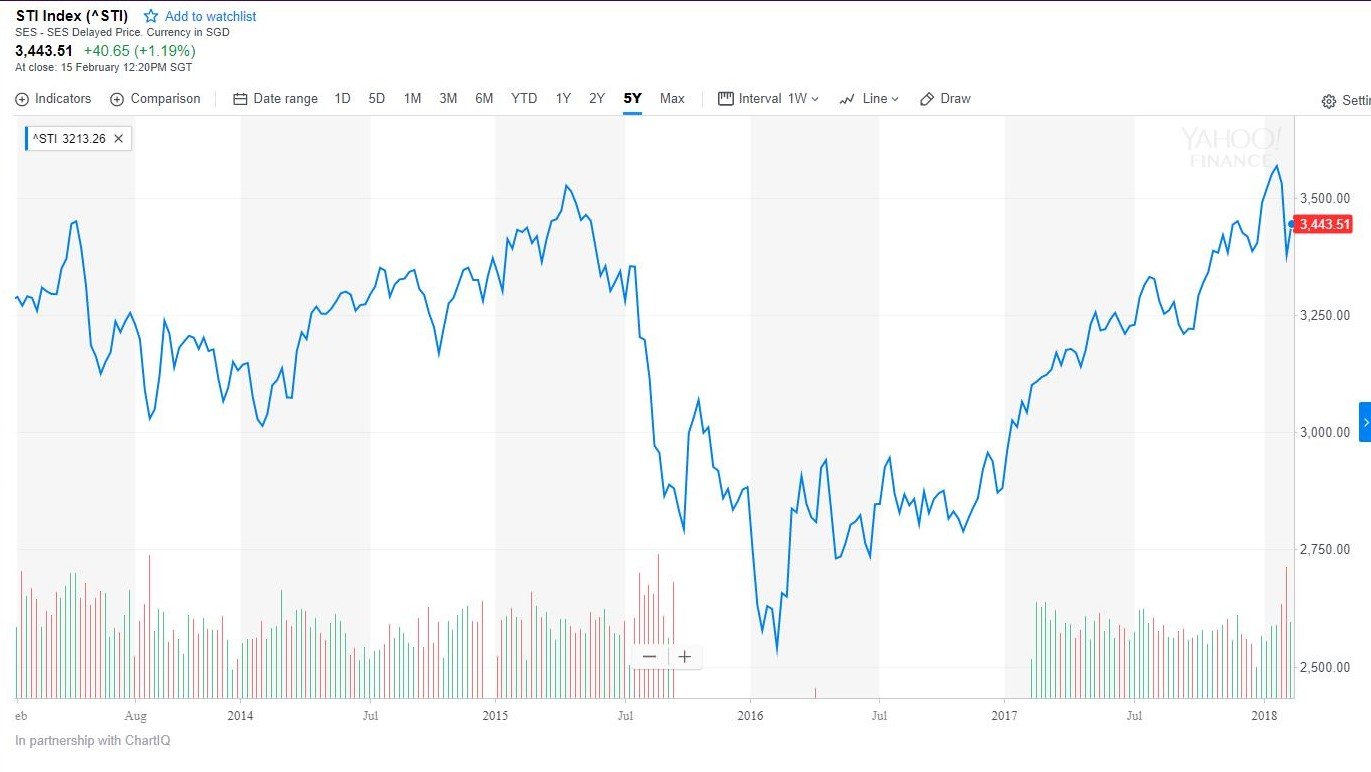

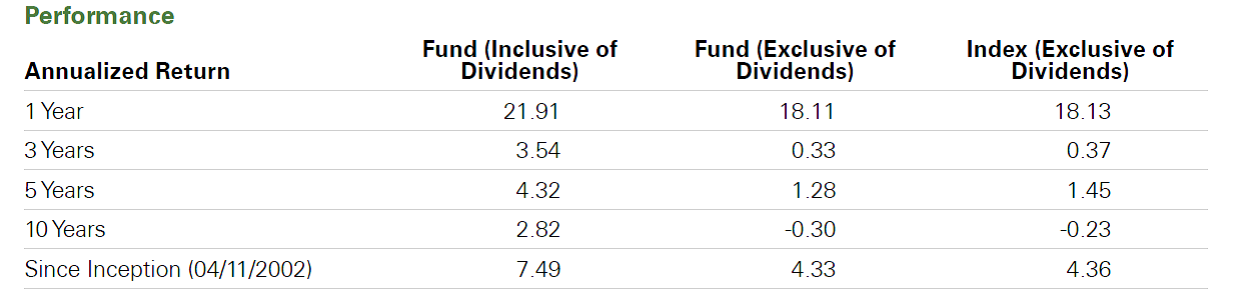

The 5 year chart for the STI yields additional insights. It is evident that the STI has gone nowhere the past 5 years, with an annualised return (excluding dividends) of 0.37% (3 years), 1.45% (5 years), -0.23% (10 years). The numbers are better once you include dividends (4.32% (5 years), 2.82% (10 years)), but still paltry compared to the performance of the other indices (eg. for the S&P 500 12.10% (5 years), 7.42% (10 years). If historical performance is any indicator, there is no guarantee that you will achieve a decent rate of return over periods of 5 to 10 years when investing in the STI.

Stocks are a high risk investment prone to bouts of drawdown of up to 50% in a financial crisis, during which time I as an investor may lose sleep and be unable to touch my investments for extended period. For such risks, I expect to enjoy handsome returns.

Of course, any financial advisor worth their salt will caution that past returns are not an indicator of future returns. As humans however, we cannot predict the future, and have to look to the past for an indicator on which to base our expectations. And based on these charts, the STI ETF does not look very promising.

Source: SPDR STI ETF Fact Sheet

- Diversification

The STI is heavily weighted in favour of financials, which makes up a whopping 59% of the index. The top 3 constituents of the STI, the local heavyweights of DBS, OCBC, UOB, collectively comprise about 40% of the STI.

Source: SPDR STI ETF Fact Sheet

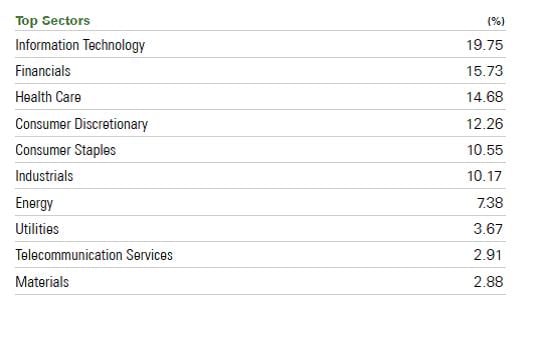

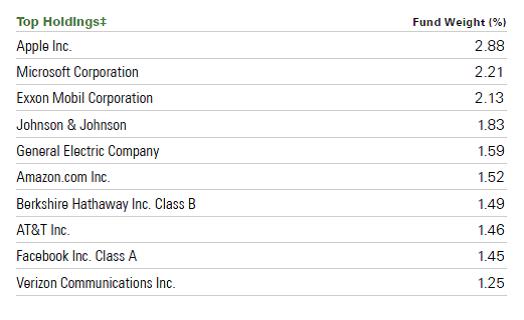

By contrast, the distribution of the S&P 500 is far more balanced, comprising 19% Information Technology, and 15% Financials. The top 3 constituents of the S&P500 (Apple, Microsoft, ExxonMobil), comprise approximately 7% of the S&P500. This broader distribution would offer me a lot more comfort when building a long term portfolio.

Source: SPY ETF Fact Sheet

Given this lack of diversification, an investment into the STI is essentially an investment in a basket of large Singapore companies, with an overweight focus on the local banks.

Investopedia defines diversification as “A risk management technique that mixes a wide variety of investments within a portfolio… Diversification strives to smooth out unsystematic risk events in a portfolio so the positive performance of some investments neutralizes the negative performance of others. Therefore, the benefits of diversification hold only if the securities in the portfolio are not perfectly correlated”.

Looking at the constituents of the STI, I do expect a fairly high correlation between the equities. Take for example, the fact that 59% of the STI are financials, with the 3 local banks forming 40% of the index. In a rising interest rate environment where banks are outperforming, the STI may generate outsized returns. As a corollary however, in a financial crisis such as the 2008 Great Financial Crisis, and the subsequent slew of regulations that destroyed the profit margins of banks, the STI is going to underperform significantly.

From a portfolio allocation point of view, with an eye to diversification of risk, I would therefore be slightly worried if the STI formed my sole investment.

- Competitiveness of Singapore Inc

There are a number of additional problems with this lack of diversification:

Singapore Centric – A number of the large players such as Singtel, SIA, SPH, derive a large portion of their revenue from Singapore. A problem with the Singapore consumer, or a recession in Singapore, will lead to a fall in the STI.

Competitiveness of Singapore Companies – You are betting on the continued competitiveness and relevance of Singapore companies. If the management team for these companies cannot successfully grow cash flow and stave off competition from regional players, the STI is going to underperform.

Correlation with other investments – As a Singapore Citizen with a job earning SGD and all my assets, savings accounts denominated in SGD, I am already making a large bet on the continuing viability of Singapore. To further invest heavily in the STI would mean that all my eggs are in one basket, and if something were to happen to Singapore’s competiveness (eg. due to political problems, poor leadership, competition from regional neighbours etc), my net worth will suffer drastically.

The corollary of these problems is that ultimately, an investment in the STI is a bet on Singapore, the competitiveness of Singapore companies, and the relevance of Singapore as a regional hub.

By contrast, the top 3 constituents for the S&P 500, Apple, Microsoft, Exxon Mobil, are global behemoths with operations in virtually every country around the world. Problems for the US consumer, may not necessarily translate into financial disaster for these companies, given the ability of their international operations to continue to prop up the company.

The lack of diversification further means that the margin of error is low. DBS makes up 15% of the STI, and if DBS were to become uncompetitive for the next 10 years, the STI performance is going to suffer. With the S&P500 however, Apple makes up a tiny 2.88%, and if Tim Cook screws up beyond our wildest imaginations, it still translates into a small impact on the overall index.

On a global level, Singapore is relatively inconsequential. The fact that we have gotten to where we are today is testament to the vision and foresight of our founding fathers. Whether that can be sustained in the coming 30 years, is a question that remains open. An investment into the STI requires an implicit belief in the strength of Singapore and its continued relevance going forward. Otherwise, with the interconnectedness of global financial markets, it is too easy for one to simply convert S$100,000 into USD and invest in the S&P500 and NASDAQ.

Personally, I do think that Singapore will remain relevant going forward, and that Singapore companies will manage to find a way to stay competitive. Singtel may never be able to compete with Apple in terms of innovation and technological foresight, but it does not have to. It merely has to focus on retaining its market share in Singapore, and growing its pie in neighbouring South East Asia. The lack of diversification however, troubles me.

Honourable mention: Forex

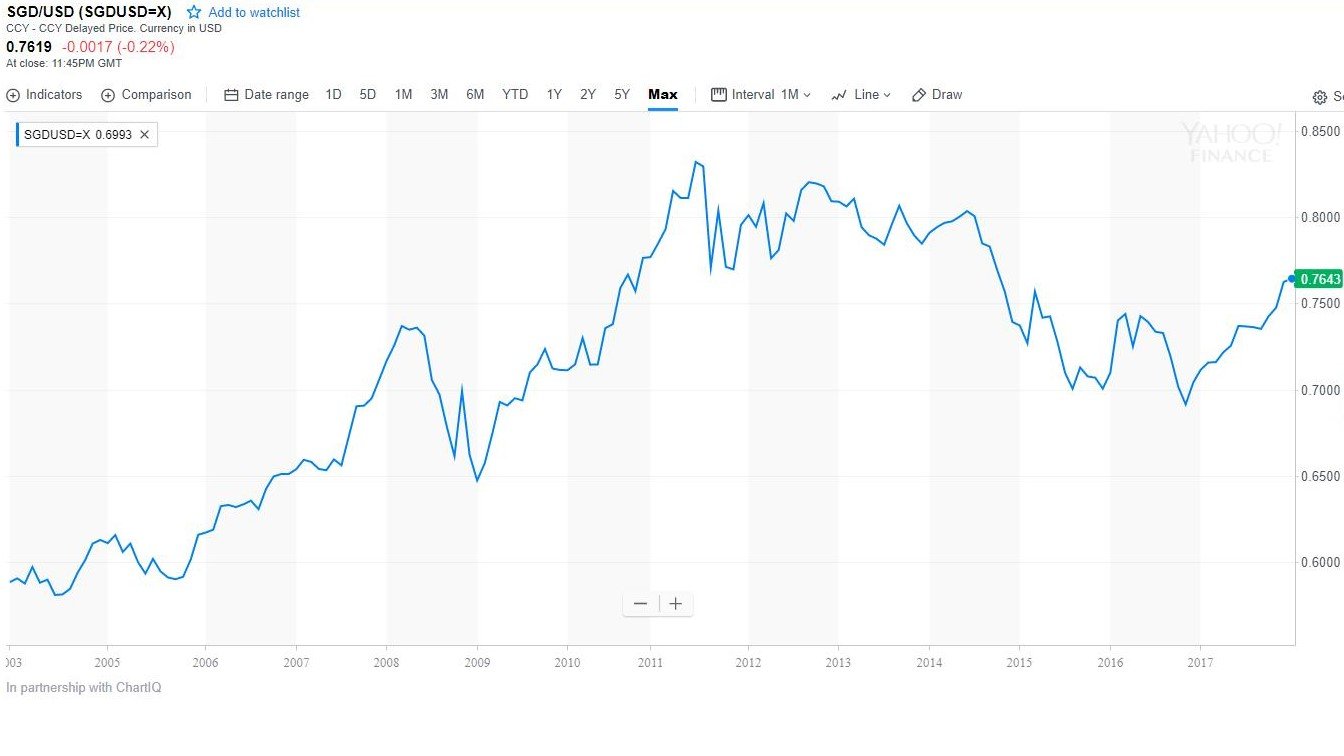

One benefit in the STI, and a major problem with investing in foreign indexes, is the foreign exchange risk. Historically, the MAS maintains a stable and gradual appreciation of the SGD against a basket of foreign currencies. This means that unless your foreign investments are generating a steady return, you are actually losing money due to appreciation of the SGD.

As seen from the chart above, this Forex movement is not something to be trifled with, resulting in almost a 25% movement in the SGD/USD pair over the past 15 years. Given that no one can predict the future, there is little point in worrying about this trend and trying to anticipate its movements going forward. We must however, remain vigilant of this risk and invest with this in mind. For this reason, I do not advise putting too large a portion of your savings into foreign equities, lest a large currency movement wipe out most of your investment returns.

Of course, Forex movements work both ways as well, and holding a portion of your net worth in foreign stocks would provide a hedge if the SGD were to fall dramatically. Diversification is the name of the game here.

Alternatives

What then, are the alternatives to the STI? I am going to assume that you are looking to grow your money for retirement purposes, and not simply to preserve wealth (for wealth preservation, look to Singapore Savings Bonds, Nikko AM Bond ETF, gold etc).

Viable alternatives are:

- Singapore REITs1

- Singapore equities (stock picking)

- Regional Indexes (Hang Seng, ASX, FTSE China etc.)

- Global Indexes (S&P 500, NASDAQ, EURO STOXX 50)

- Foreign equities (stock picking)

1 I do not advise using a REIT ETF due to the 17% corporate income tax payable. Read more here.

Personally, my current portfolio allocation is approximately 30% foreign equities, 20% local equities, 50% REITs. As much as I love Singapore, I remain sceptical on the competitiveness of many Singapore companies. I do not invest in equities unless I see a compelling story, hence the underweight Singapore equities position. I am however, a huge fan of the S-REITs, given the favourable regulatory climate, world class property developers, and the best in class assets held by some of these REITs. My foreign equities, mainly for diversification purposes, are largely in the form of index funds in S&P500 (SPY) and NASDAQ (QQQ), as well as one or two counters that I personally like.

Closing Thoughts

Whether the STI ETF is appropriate ultimately depends on your profile as an investor. Had you bought an STI ETF at the absolute worst time 10 years ago right before the financial crisis, your annualised returns to day (including dividends) would still be a 2.82%, higher than a fixed deposit account. Taking a longer time frame (since 2002), returns are 7.49%, something not to be trifled with.

An individual stock picker could easily have picked a group of poor stocks and ended up with a far worse performance, and with far more effort expended. The STI ETF is a true buy and hold investment, with little to no input required from its investor. You could be selling char kuay teow at your day job, or a hedge fund manager at Temasek, and your returns would be identical. For this reason, I recognise that there will always be a place for the STI ETF. If you do not know the difference between a stock and a bond, and have no idea what level the NASDAQ is trading at, you could do less wrong than invest in the STI.

However, given the lack of diversification and implicit bet on Singapore Inc an investment in the STI entails, I remain wary of putting all my eggs into the STI basket. I would highly recommend that prudent investors consider allocating a portion of their portfolio away from a pure STI ETF, into REITs or foreign indexes, as a hedge against a decline in Singapore Inc.

While we are on the subject of ETFs, find out also what Financial Horse thinks about REIT ETFs following Budget 2018.

Enjoyed this article? Like our Facebook Page for more great articles!

Financial Horse has a set of 7 Commandments for Successful Investing, that I ask myself before making every investment, and that I will never break regardless of the situation. I share this with all my email subscribers at absolutely no cost. Sign up for the newsletter now!

[mc4wp_form id=”173″]

STI ETF good for longer term trades though, to capture those 50% to 100% upside while avoiding the 20% to 60% downsides.

For multi-decade buy & hold or DCA, STI ETF should probably not make up more than 5% of your total portfolio. ETF purists will argue for less than 2% in line with S’pore’s valuation on the world stage.

For no-brain multi-decade investing, easiest will simply be 60:40 or 50:50 allocation between world stock index (encompassing both developed & emerging) and mid-duration world bond index. And just do annual rebalancing.

Hi Sinkie,

That’s a great point. The STI ETF can be used by traders for a mid to long term trade, if they are confident in their ability to time the market. The current market correction comes to mind for one.

As a buy and hold investor myself, I am with you on the need to limit exposure to the STI ETF. However I prefer not to do a 40/50% allocation to bonds given my age, instead I leave a cash buffer in a high interest savings account. My thoughts on portfolio allocation here: https://financialhorse.com/ideal-asset-allocation-by-age/

Cheers.

Hi, what are your opinions on the SPY regarding the fact that it gives dividends that are taxed? If I understand correctly there is a 30% dividend withholding tax, please correct me if I am wrong. Regarding the indices’ performance, when I checked longer term comparing the Hang Seng and the S&P, I noticed that the STI seems to have done quite well, notably better than the Hang Seng for most of 2001-2007 and 2011-2015, based on plotting historical data on FT. I understand that historical performance is no indicatoe of future performance and understand your good points about diversification risk, but for the purposes of diversifying especially across FX, would it be helpful for a not so experienced new investor like myself to split something like 50-50 across STI and something like IWDA? Apologies if anything I have said is incorrect, am looking to learn from the more experienced investors out there.

Hi JY,

You are absolutely right, a foreign investor investing in the SPY will be subject to a 30% withholding tax. However the TTM dividend yield for SPY is approximately 1.7%, vs 2.9% for the STI. If you invest in the NASDAQ (QQQ), the yield is an even lower 0.79%. Foreign investors don’t pay capital gains tax on US stocks, so when investing in the US i generally go for growth stocks over dividend stocks, and my personal portfolio favours the NASDAQ (QQQ) over SPY.

Picking the right index is really important, the Hang Seng is pretty much a proxy for China, and a lot of stocks look really bubbly these days. Something like the IWDA is definitely a great choice as it provides a ton of diversification at a very low expense rate. I presume you chose it also because of its Irish domicile and the tax treaty with US (favourable treatment for US dividends)?

Personally for me, a 50% allocation to the STI is on the high side. If I were to do a true buy and forget portfolio for myself, I would do a 20% STI, 30% REIT, and 50% global equities (through something like IWDA). The REIT portion may be tricky as it used to be that you had to pick REITs individually, due to tax treatment for REIT ETFs. However this has changed with the Budget 2018, and I’ll be writing an article analysing the REIT ETFs as a long term investment. Do check back for that. As a young investor, I wouldn’t touch bonds as my main goal is wealth creation rather than wealth preservation, and my holding period is decades long.

Cheers. Thanks for the great question!

How can one gain exposure to foreign equities and foreign ETFs without incurring exorbitant fees and commissions?

For eg, $100 a month of STIETF, POSB charging $1 which is equivalent to 1%. However, local brokerages will charge something like $2 per counter per month? This is counter intuitive to someone who wants to better returns, at a lower capital.

Hi Jason,

That is a great question. Perhaps I will share what I would do in such a situation, and you can see if it is applies to your case:

(1) I use Standard Chartered online trading. They charge a minimum commission of US$10 on trades (vs US$25 for DBS), and no monthly charge per counter.

(2) I will try to pool my capital such that instead of making monthly purchases, I make quarterly purchases of a larger amount (min of about 2,000 USD is my recommendation). This allows me to reduce the minimum commission on a percentage basis. From a dollar cost averaging perspective, the returns will not be affected significantly over long periods, since I am still buying into the market on a regular basis.

(3) Of course, if I have a huge influx of cash for that month (eg. annual bonus), or if there is a great price (eg. market correction), I can make more frequent reinvestments.

Cheers.

May i know what trading platform you use? Like scb or?

Hi Vincent,

Welcome to Financial Horse, and thanks for the question! I use DBS Vickers Cash Upfront for Singapore shares, and for US shares I use a mix of SCB and Saxo.

You can read more about my choices here: https://financialhorse.com/stock-brokers-i-use-to-replace-standard-chartered-online-trading-s500-referral-bonus/

Cheers.

The lack of diversification aside, I am curious why you would be concerned with the performance of an individual bank over the long term.

If DBS really underperforms, won’t it shrink in market cap and drop out from the STI (and the ETF) and be replaced by some other high performing blue chip stock ? After all STI only tracks the top 30 by market cap , which may or may not include DBS in the future.

You are right, it is primarily a diversification issue, as the index is heavily weighted towards financials.

[…] from https://financialhorse.com/sti-etf/ […]