If you are in your 20s and 30s, mastering the Central Provident Fund (CPF) is one of the most important steps you can take to secure a comfortable retirement. A crucial pillar is the Supplementary Retirement Scheme (SRS).

Despite what the name suggests, it’s not just for those nearing retirement. It’s designed to provide an additional retirement safety net beyond CPF savings — with tax relief as the main incentive to save up.

Well, it’s working. The latest data shows an increase in contributions, especially among young people.

The Ministry of Finance (MOF) reported 387,377 SRS account holders in 2022, a 34% increase from the previous year.

Almost one in three account holders were between 18 to 35 years old.

If you are in the earlier phase of your career and haven’t gotten started, here is a primer on SRS and essential tips for making the most out of it.

This article was written by a Financial Horse Contributor.

What is the Supplementary Retirement Scheme?

We already wrote an in-depth guide to the SRS. But in a nutshell, the IRAS website provides a good definition:

The Supplementary Retirement Scheme (SRS) is a voluntary scheme to encourage individuals to save for retirement, over and above their CPF savings.

Contributions to SRS are eligible for tax relief.

Investment returns are tax-free before withdrawal and only 50% of the withdrawals from SRS are taxable at retirement.

The main benefit: you’ll get a dollar-for-dollar tax discount for the amount added to your SRS account.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

How does the Supplementary Retirement Scheme work?

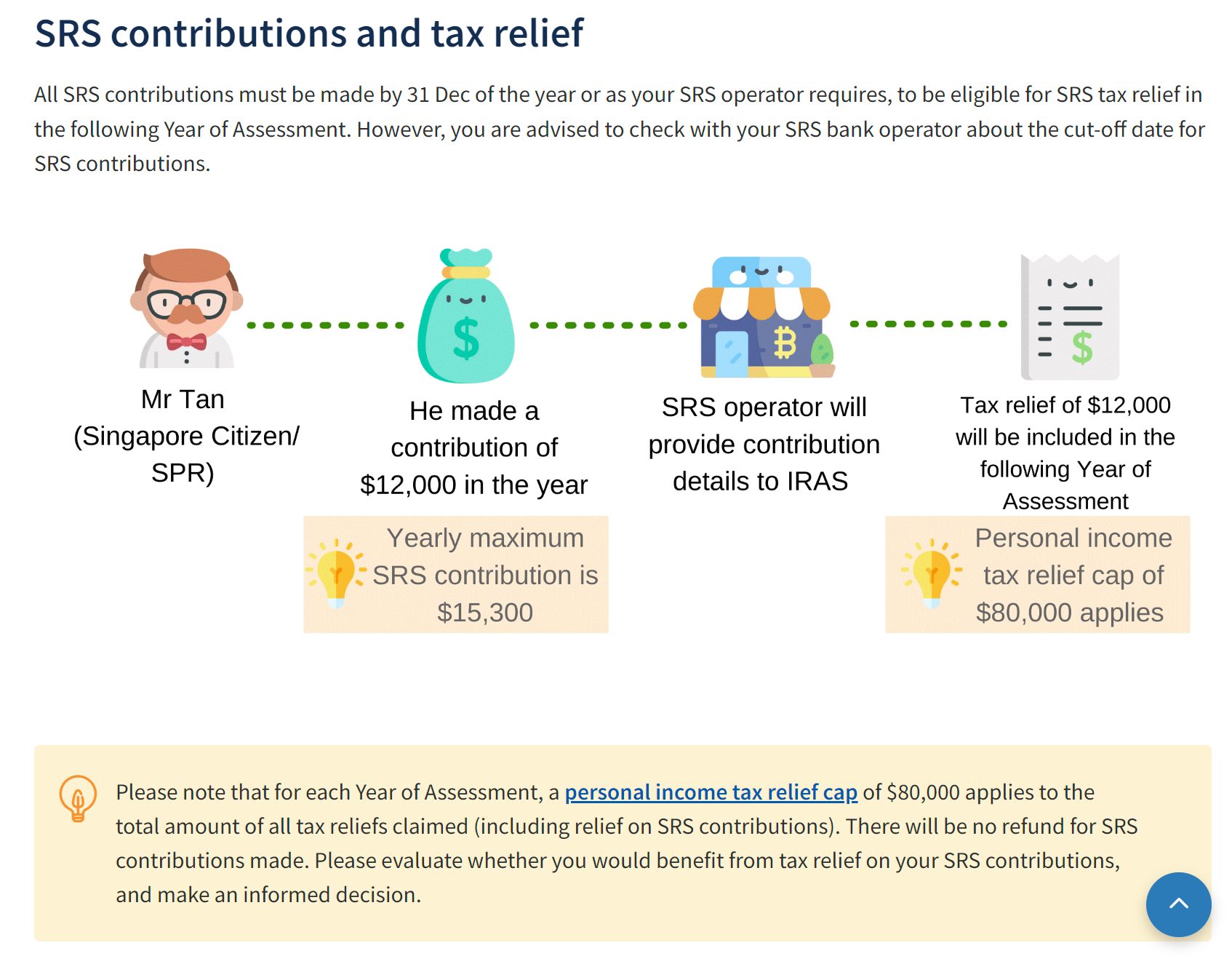

You can set up an SRS account at any of the three local banks — DBS, OCBC and UOB.

Singaporeans are allowed to deposit up to $15,300 into the account each year.

This can be used to invest in products including unit trusts, robo-advisors, SGX-listed stocks, REITs, and ETFs. You can also invest in lower-risk products like Endowment Insurance Plans, fixed deposits, and Singapore Government Securities.

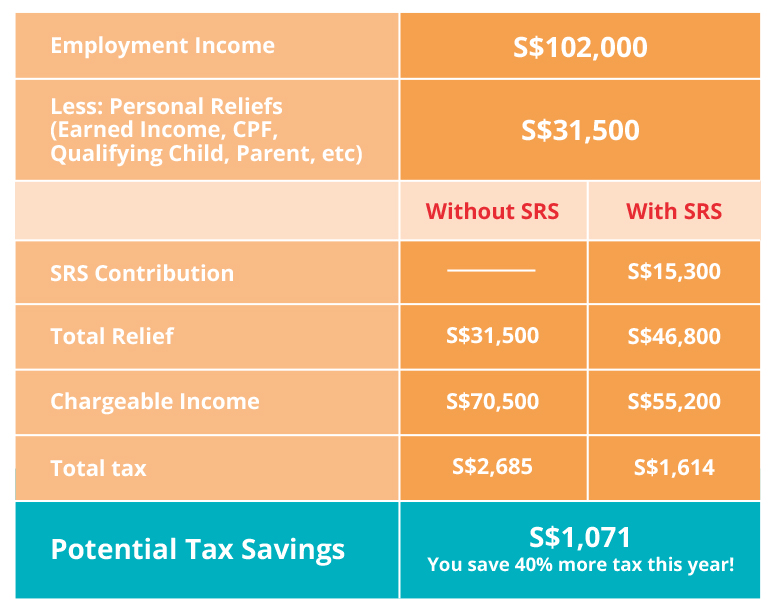

Here is an illustration of the tax savings at work.

Source: DBS

And just like that, you’ve slashed a hefty portion of your tax bill.

Topping up your SRS is generally only recommended if you’re above the 7% tax bracket when the tax savings are more substantial relative to the amount you top up. They become more tax efficient the higher up the tax bracket, as illustrated below.

But deciding whether to put money into your account is a personal decision and varies based on your circumstance.

|

Income tax bracket |

Tax savings on $15,3000 |

|

3.5% |

$535.5 |

|

7% |

$1,071 |

|

11.5% |

$1,759.5 |

|

15% |

$2,295 |

Consideration for SRS top-ups

Ability to commit for the long term.

SRS’s biggest drawback is liquidity. Once that money is in, withdrawing any amount before reaching the statutory retirement age will incur penalties. You’ll need to pay income tax on 100% of the amount withdrawn (based on your income tax bracket) — plus an additional 5% penalty on the amount withdrawn.

As such, make sure this is money you can set aside for the long term and is not essential funds. Treat it as buying an endowment or Investment-Linked Plan (ILP). This is money that you are willing to part ways with for a long time.

This is an especially difficult balance to strike in your 20s and 30s. This is a period full of big financial commitments like paying for a wedding and buying a house. Make sure your cash flow doesn’t suffer in pursuit of tax savings.

Should you top up your CPF or SRS?

Deciding between topping up your SRS or CPF Medisave Account (MA) or Special Account (SA) is a common dilemma. Both are great ways to build savings and enjoy tax relief. Choosing between the two boils down to your risk appetite.

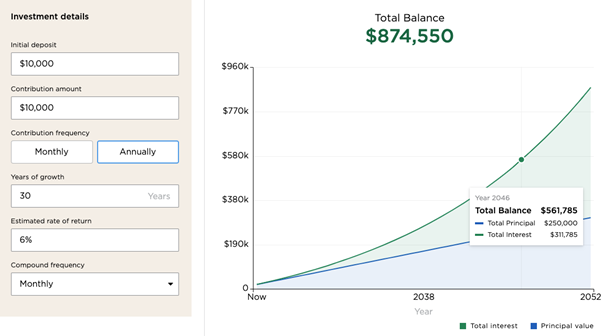

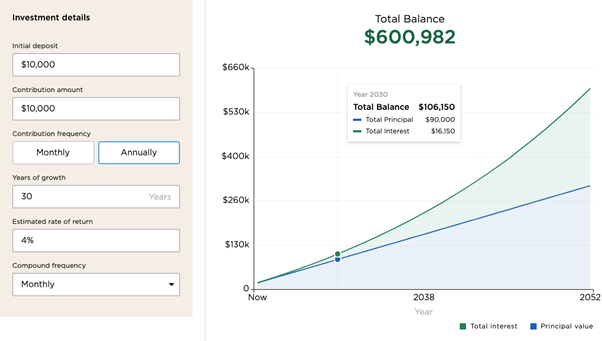

In your 20s and 30s, time is on your side to invest your SRS funds more aggressively. If you can stomach the volatility, you can afford to take risks for higher expected returns over the long term.

Investing in equities will give you a better probability of generating 6 to 7% annually, compared to around 4% if you keep it in your CPF MA/SA.

A 2% higher return makes a huge difference when compounded over 30 years.

But if you are more comfortable with the guaranteed returns of CPF MA/SA — a 4% interest is nothing to sneeze at either.

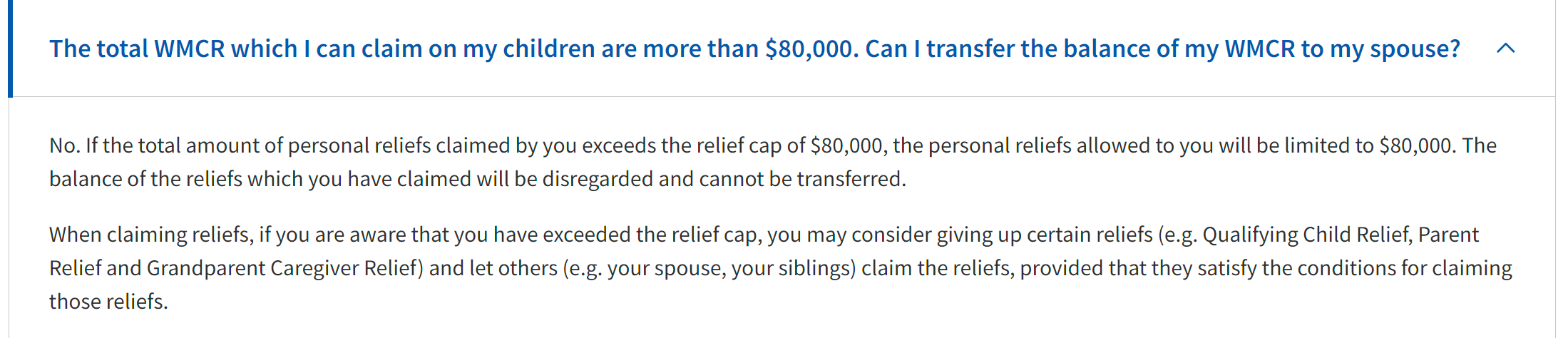

Personal income tax relief cap

Take note that the cap on personal income tax relief is $80,000. This applies across all tax relief claimed for each year of assessment, which includes Earned Income Relief and CPF Cash Top-Up Relief.

The personal income tax relief cap was introduced in Budget 2016.

Working mothers for instance should be mindful of these caps.

Make sure you check the previous year’s notice of assessment, take the amount of tax relief you’re expecting, and factor that into the amount to top up for SRS.

Make sure to deploy your cash

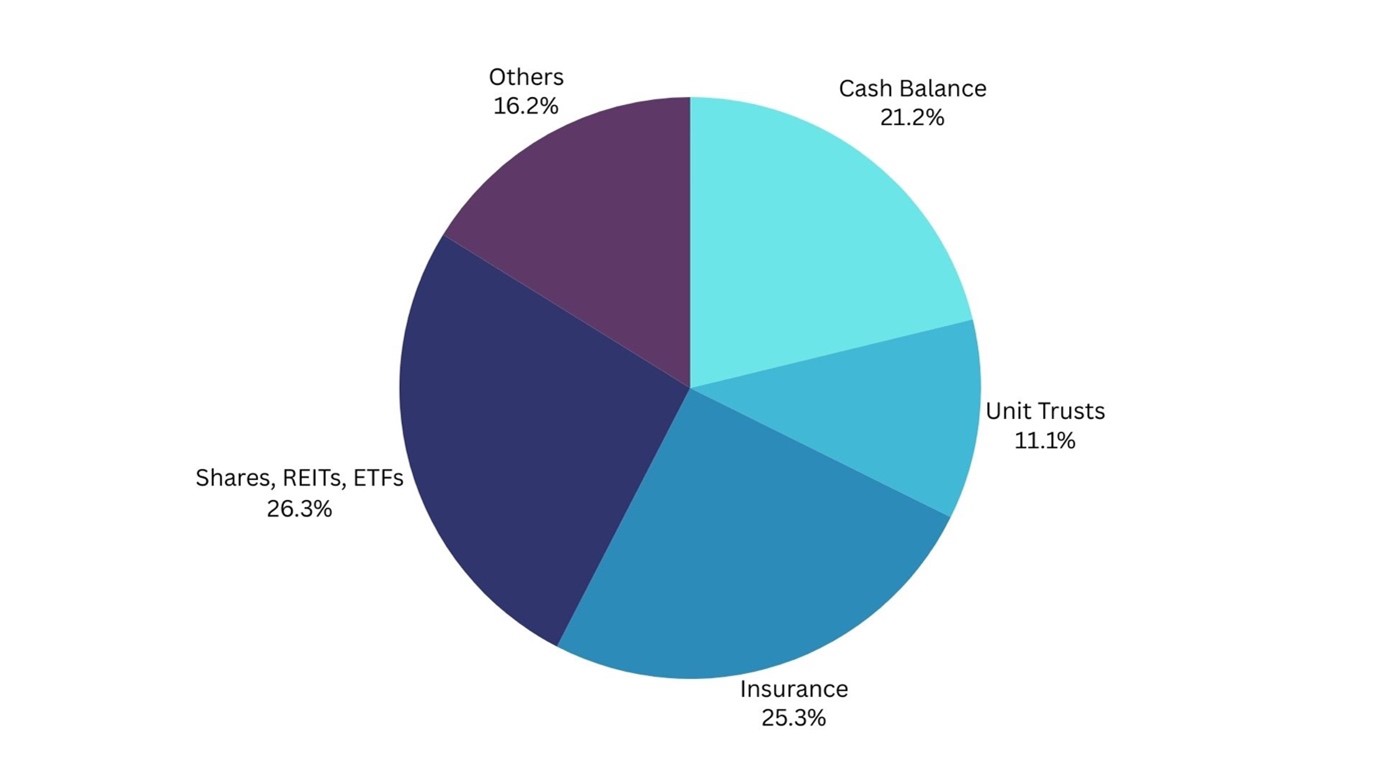

While the tax relief of SRS is the main draw, remember that cash in your SRS account only earns 0.05%. If you’re not investing your SRS savings, you’re losing money to inflation!

According to MOF, 21% of SRS monies are sitting idle in cash, so this is not as uncommon as you’d think.

Why you should top up $1 into your SRS account today

Even if you don’t plan on using your SRS, you should still open one and top up $1 into your account.

This allows you to lock in your Statutory Retirement Age at 63 today before it goes up to 65 in 2030. In other words, opening an SRS account now will protect you from any subsequent changes in the statutory retirement age.

Top up by 31 December!

With the end of the year approaching, now is a great time to top up your SRS.

Don’t forget to top up by 31 December if you want to enjoy the tax relief.

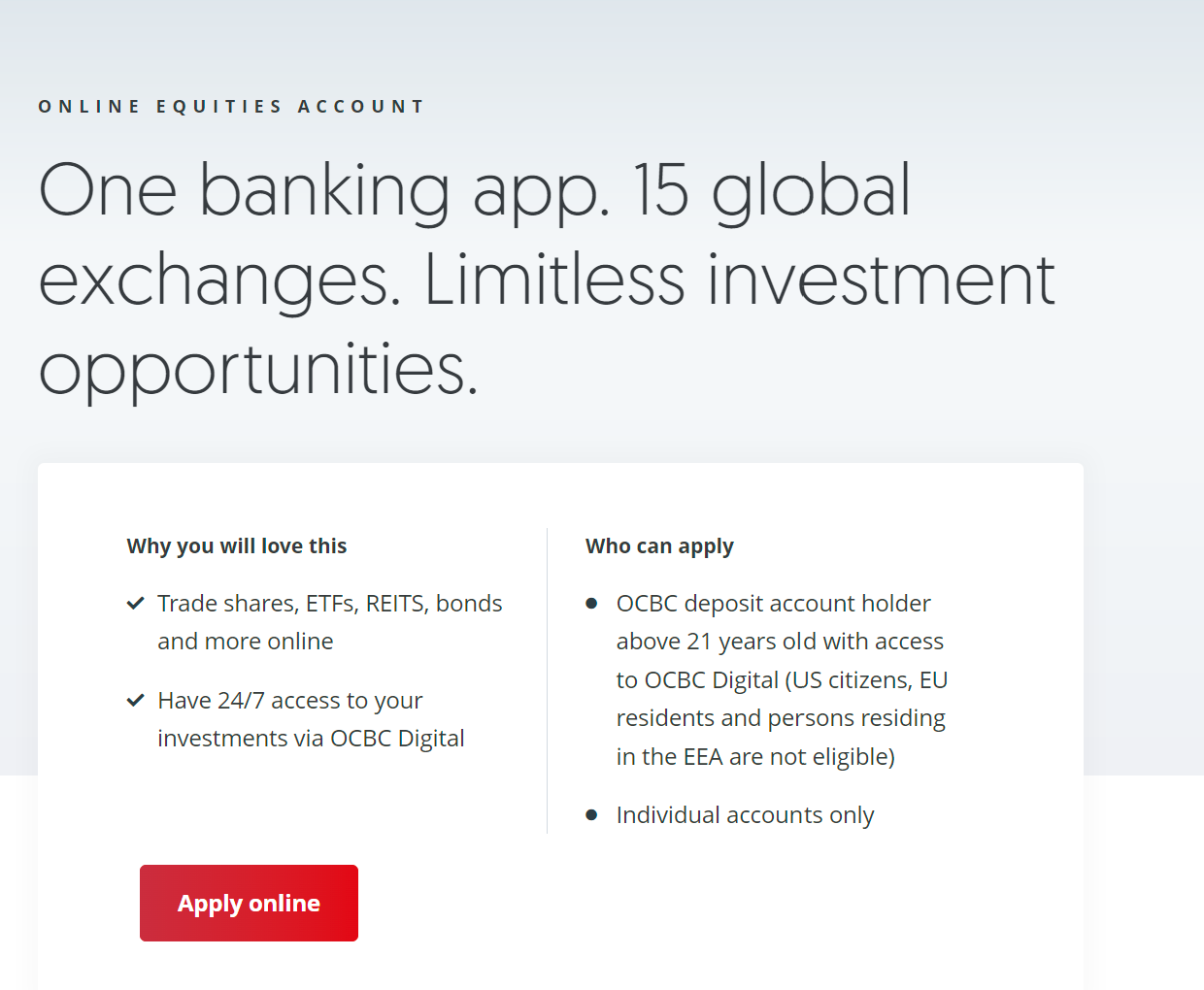

OCBC Online Equities Account – Trade on 15 global exchanges, all via the OCBC Digital Banking App!

Did you know that can you trade shares on your OCBC Digital Banking App?

With an OCBC online equities account, you can buy stocks, local ETFs, REITs, bonds and more directly through your banking app.

Even better? Enjoy reduced commission rates of just 0.05% for buy trades on SG, US and HK market until 31 December 2023.

Everything on one app! Fuss-free funding, with access to 15 global exchanges

For SGD trades, you can fund and settle automatically via your OCBC account.

And for FX trades, you can settle using the foreign currency held in your OCBC Global Savings Account.

This means fuss-free trade settlement and minimising forex costs – saving you time and money.

Start trading with your OCBC Online Equities Account here!

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Investment Research Tools

I use Trading View for my research and charts. Get $15 off via the FH affiliate link.

I also use Koyfin for fundamental and macro research. Get a 10% discount via the FH affiliate link.

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Best investment books to improve as an investor?

Check out my personal recommendations for a reading list here.