It’s that time of the year again!

For those of you who are keen to top up your Supplementary Retirement Scheme (SRS) – don’t forget to top up by 31 December 2022 if you want to enjoy the tax relief.

I’ve also been getting quite a few questions on when does it make sense to top up an SRS account.

And what to buy with SRS money.

So I wanted to share views in this article.

Basics: What is Supplementary Retirement Scheme (SRS)?

From the IRAS website, emphasis mine:

The Supplementary Retirement Scheme (SRS) is a voluntary scheme to encourage individuals to save for retirement, over and above their CPF savings.

Contributions to SRS are eligible for tax relief.

Investment returns are tax-free before withdrawal and only 50% of the withdrawals from SRS are taxable at retirement.

What is the benefit of Supplementary Retirement Scheme (SRS)?

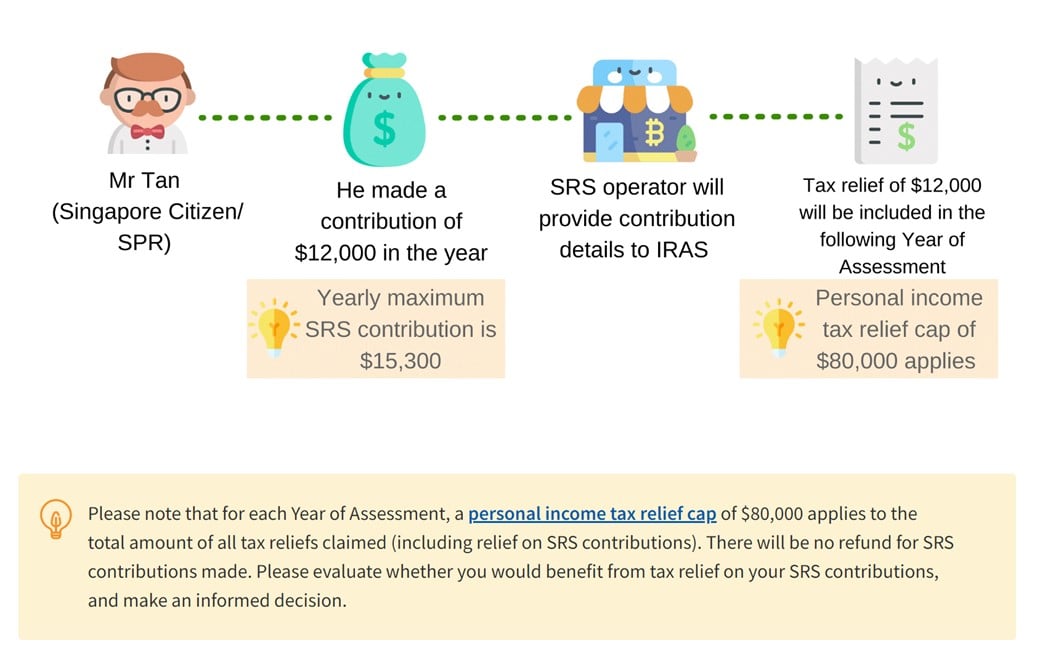

The main benefit of SRS – Income Tax Relief.

Basically, Singapore Citizens / PRs can top up $15,300 a year into SRS, and the amount topped up is fully exempt from income tax.

Yes – you pay absolutely no income tax on the amount that goes into your SRS account that year.

However, do note that for each Year of Assessment, a personal income tax relief cap of $80,000 applies to the total amount of all tax reliefs claimed (including relief on SRS contributions).

Also note that the $15,300 cap is for Singapore Citizens or Permanent Residents, while Foreigners can top up $35,700.

Is it worth it to top up your Supplementary Retirement Scheme (SRS) account?

The short answer, is that it depends very much on your income tax bracket.

The higher your income, the more income tax you pay, and the more it makes sense to top up SRS.

But if done well, SRS can lead to very efficient tax treatment.

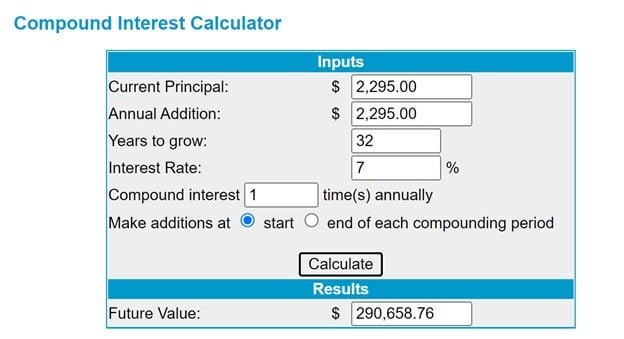

How Supplementary Retirement Scheme (SRS) can save you $290,000 in taxes

Just to give a very simple example.

Imagine you’re a 30 year old, in the $120,000 and above income bracket

You’re feeling very pleased with yourself with your income, and you’re paying an effective 15% tax rate on all income above $120,000.

Now let’s say you top up the max $15,300 every year starting from age 30.

That means you save $2,295 in income tax every year, that you get to invest and compound until retirement.

And let’s say you make 7% a year on the amount in your SRS account.

The amount you save on income tax, will compound at 7% a year – totalling $290,000 in 32 years.

And this is just the amount you save from income tax.

So long story short – yes, SRS can be very worth it, if you know how to use it right.

What is the drawback to using Supplementary Retirement Scheme (SRS) Account?

SRS is not without its drawbacks though.

The main limitation – is liquidity.

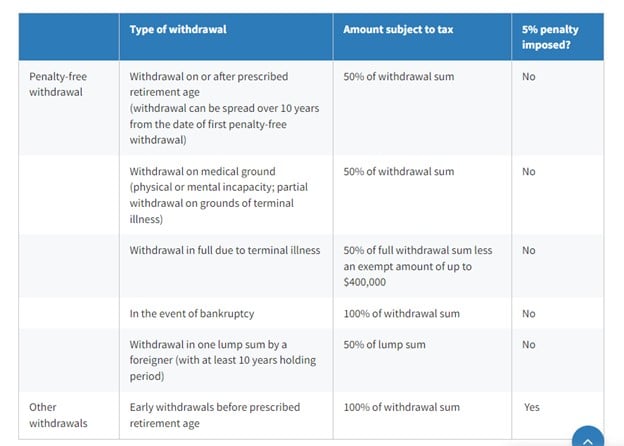

If you withdraw before statutory retirement age (63), you need to pay tax on 100% of the amount withdrawn + 5% penalty

If you want to withdraw any amount from your SRS Account before statutory retirement age, you need to pay:

- Income Tax on 100% of the amount withdrawn (based on your income tax bracket)

- An additional 5% penalty on the amount withdrawn

To give an example, let’s say you’re in the $120,000 tax bracket.

And you’re a bit tight on cash, so you withdraw $10,000 from your SRS account that year.

You need to pay:

- Income Tax on 100% of the amount withdrawn – 15%

- An additional 5% penalty on the amount withdrawn – 5%

So in total, you pay a 20% tax, or $2,000, on the $10,000 withdrawn.

In a way you can think of SRS as a liquidity tax.

You’re not banned from using the money, you just need to pay a penalty if you want to use it before statutory retirement age.

If you withdraw after statutory retirement age, you only pay tax on 50% of the withdrawal amount (spread over 10 years)

If you do withdraw from your SRS account after statutory retirement age though, then there is no penalty fee.

In that case, you only pay income tax on 50% of the withdrawal amount.

At this point though, you should not be earning significant income anymore, so the income tax is very low.

Or at least that’s how it should work in theory.

So to give an example.

Imagine you retire at 63, and your income drops to zero.

Then you withdraw $40,000 from SRS that year.

You only pay income tax on 50% of that – which is $20,000.

And the first $20,000 of income pays 0% tax, so you pay absolutely no tax on the withdrawal from your Supplementary Retirement Scheme (SRS) account.

There are other situations where you can withdraw the money, for example on medical grounds, or terminal illness.

I set out the screenshot below for your reference.

Who should top up their Supplementary Retirement Scheme (SRS) Account?

Okay, now comes the very interesting part.

Who should top up their SRS Account?

My view, is that SRS Account makes sense if:

- You have a high income

- You are close to statutory retirement age (63)

You have a high income

If you have a high income, SRS becomes quite tax efficient.

Whatever you top up into your SRS account, you don’t need to pay tax on.

What is the income threshold where Supplementary Retirement Scheme (SRS) makes sense?

Now of course everybody can use SRS to save on their tax bill.

But as we discussed above, you’re sacrificing liquidity, and the ability to use your cash, when you top up SRS.

So it only makes sense if you’re saving a decent amount on tax, to make this worth it.

There is no right or wrong amount where it makes sense to use SRS, and the exact threshold will depend on each individual.

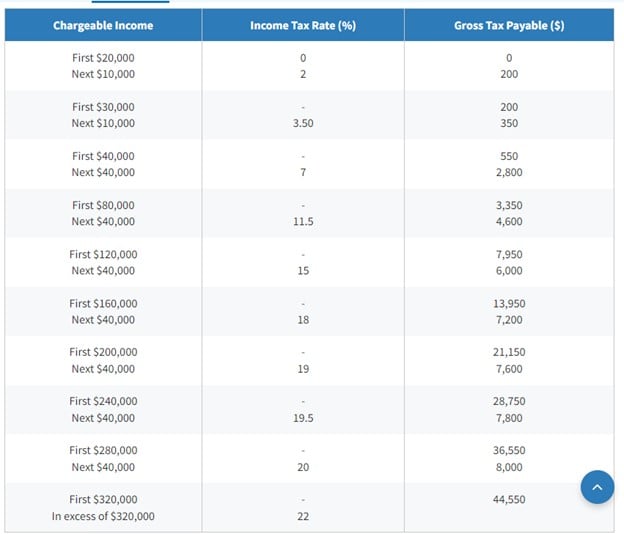

But I would say generally it only makes sense if you’re earning at least $80,000 chargeable income (11.5% income tax bracket). In which case you save $1759.5 on $15,300.

But ideally you should be earning at least $120,000 chargeable income (15% income tax bracket), and save $2,295 on $15,300

But really – there’s no right or wrong here.

It’s your call.

You are close to statutory retirement age

If you are close to statutory retirement age (63), then it becomes a no brainer as well.

You can top up the money to get tax relief.

Then when you retire and your income drops drastically, you take the money out and only pay income tax on 50% of that.

And because your income should drop a lot after retirement (I’m leaving aside those who have rental income from 10 properties…), you’ll be paying income tax on a much lower tax bracket.

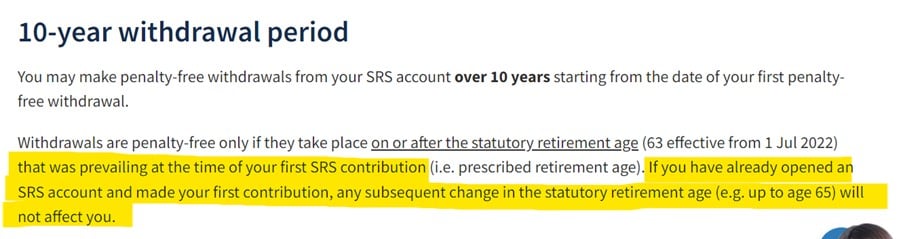

Note: Statutory Retirement Age prevailing when you topped up the SRS Account

Just a sidenote that the Statutory Retirement Age for purposes of SRS withdrawal, is the Statutory Retirement Age that was prevailing at the time of your first SRS contribution.

In plain English, this means when you first top up your SRS account, you lock in the Statutory Retirement Age on that date.

Before 1 July 2022, it was 62.

After 1 July 2022, it went up to 63, and who knows it may go up in future.

So even if you don’t plan to use the SRS account, you really should just open one and top up $1 into it today.

This helps you lock in the Statutory Retirement Age for your SRS account, just in case you want to use it in future.

SRS Accounts can be opened online in just a few minutes, so there’s really no reason to be lazy about this.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Who should NOT top up their Supplementary Retirement Scheme (SRS) Account?

Now you should NOT top up your SRS Account if:

- You need the money before retirement

- Your income is low

You need the money before retirement

If you even think there is a chance you need the money, I would say just be safe rather than sorry, and not top up your SRS Account.

So if you’re saving up for a big ticket purchase like a house, a car, a wedding etc, and you think you might need the liquidity, then don’t bother with SRS.

Just pay the income tax and enjoy the freedom to use your cash as you deem fit.

Your income is low

As discussed above, SRS sacrifices liquidity for lower tax.

It only makes sense if your income is of a certain level, and you can refer to the discussion above on what amount makes sense.

What should you buy with Supplementary Retirement Scheme (SRS) money?

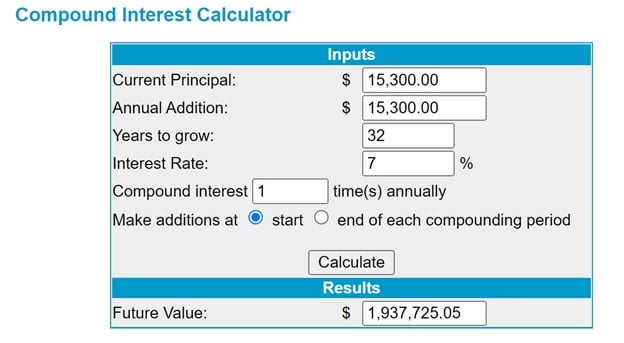

An equally important question – is what should you buy with your SRS money?

If you top up $15,300 a year into SRS, from age 30 until retirement at 62.

And if you grow that money at 7% a year, you’re left with close to $2 million after 32 years.

So yes, it probably makes some time to think seriously about how to properly invest your SRS money.

What can you buy with Supplementary Retirement Scheme (SRS) money?

The kind of investments you can buy with your SRS moneys are set out below, classified by risk:

Low Risk

- Fixed deposits

- Singapore Government Securities, including T-Bills and Singapore Savings Bonds (SSBs)

Moderate to High Risk

- Stocks / REITs (but only SGX listed stocks / REITs)

- Exchange traded funds (but only SGX listed ETFs)

- Roboadvisors (Endowus, Stashaway, MoneOwl etc)

- Unit Trusts

- Single premium insurance products, including endowment plans. The products’ life coverage (including total and permanent disability benefits) is capped at three times of the premiums.

What should you buy with Supplementary Retirement Scheme (SRS) money?

The way I see it, there are 2 types of investments you can make with your SRS.

You can buy short term, risk free investments (eg. T-Bills, Singapore Savings Bonds) to park the cash somewhere until an investment opportunity opens up (or until you hit retirement age).

Or you can buy long term equities for higher long term returns.

Which one to pick depends on:

- The number of years left until statutory retirement age – the closer to retirement you are, the more you’ll favour short term, low risk investments

- Market volatility – if you think markets are looking expensive and may crash in the short term, then you would favour short term, low risk investments

Short term, low risk investments

This one is easy.

Just buy T-Bills, Fixed Deposit, or Singapore Savings Bonds.

T-Bills have the highest yield, but you won’t be able to get the money back before maturity.

So if the market crashes in January 2023, you still need to wait until maturity before you can deploy your SRS Funds.

So if you want the option to get your SRS money back to deploy into stocks / REITs, Singapore Savings Bonds or Fixed Deposit might be a better option.

Long Term Holdings

That being said, if you’re a 30+ year old, and your investment horizon is 30 years or more.

I don’t think you should be putting your SRS money into the low risk investments above for anything longer than a few years.

If you’re investing for a 30 year horizon, you really want to go into equities for the higher long term returns.

There are 4 main options here:

- SGX listed Stocks

- SGX listed REITs

- SGX listed ETFs

- Roboadvisors (but they do tack on fees)

I know a lot of people like to go for (4).

They use a roboadvisor to buy US listed ETFs, and just let it compound.

Personally I’m not a big fan because the roboadvisor charges fees on top of the ETFs fees, and over a 30 year period that can really kill returns.

But hey, it’s your money, your call.

Personally for me I would go with either (1) SGX listed Stocks or (2) SGX listed REITs.

I know that REITs are a bit annoying because of frequent rights issues which require you to have money in SRS in order to take up the rights.

Investors who don’t like this could just stick with stocks I suppose.

What would I do with my Supplementary Retirement Scheme (SRS) money?

What would I do today?

I’ll probably just chuck whatever liquid cash I have in my SRS account into T-Bills or Fixed Deposit.

I’ll ride out the storm, and start buying in 2023/2024 (exact timing will depend on how the macro plays out).

That said, this is definitely market timing.

If market timing is not your cup of tea, just go ahead and buy now.

If you’re holding for 30 years, frankly anything that happens in the next 3 – 5 years is just noise and an opportunity to buy cheaper.

Supplementary Retirement Scheme (SRS) Account – How to open an SRS Account, Who is eligible to open etc.

Couple of administrative details.

Who is eligible to open an SRS account?

Singapore Citizens, Singapore Permanent Residents (SPRs) and foreigners who derive any form of income may make SRS contributions in the current year.

How to open an SRS account?

Only the 3 local banks can open an SRS account:

- DBS Group Holdings Ltd

- Overseas-Chinese Banking Corporation (OCBC) Ltd

- United Overseas Bank (UOB) Ltd

Closing Thoughts: Supplementary Retirement Scheme (SRS) Account

And there you have it!

The Financial Horse Guide to Supplementary Retirement Scheme (SRS) Account.

I hope this was useful for you in deciding whether or not to top up your SRS Account, and what to buy with your SRS moneys.

Any other comments – feel free to share below!

For those of you who are keen to top up your Supplementary Retirement Scheme (SRS) – don’t forget to top up by 31 December 2022 if you want to enjoy the tax relief.

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

– Free USD150 ($212) cash voucher

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with a free USD 150 (S$212) cash voucher.

You just need to:

- and fund S$2000

- Make 1 US Stock or ETF trade (you get USD100)

- Make 1 Options trade (you get USD50)

1080-1080-002-1024x1024.jpg)

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

I have SRS account with OCBC bank. July 22 when I asked the bank officer to transfer 71K to FD, but it end up in saving account without going to FD as I signed blinding the withdrawal form, thinking that it will transfer to FD later. After appeal to various authorities MP, IRA, MAS and OCBC. OCBC finally gave me a good will payment of about 1.8K. I have all the documents approved for my case. IRA will never reversed on the oversight of SRS account holder and the bank. Not in the case of money transfer to wrong account holder where it can be reversed by law. If you are interested to publish my case for the lesson learned, I am willing to provide more details including documents.

Oh dear, that is terrible to hear. So did you lose the 71k? Or only the interest?

Hypothetically if I lose my job for a year (0 income), can I withdraw everything in SRS and pay 5% penalty tax only?

Yes, that is right.

When you mentioned $80K or $120K chargeable income, do you refer to the chargeable income after all other tax reliefs (e.g. CPF, NSman etc)?

Yes that is exactly right 🙂