As most of you are aware, last week’s Temasek T2023 2.7% 5 year Retail Bonds sold like Bread Talk’s pork floss buns when they first came out (am I getting too old?).

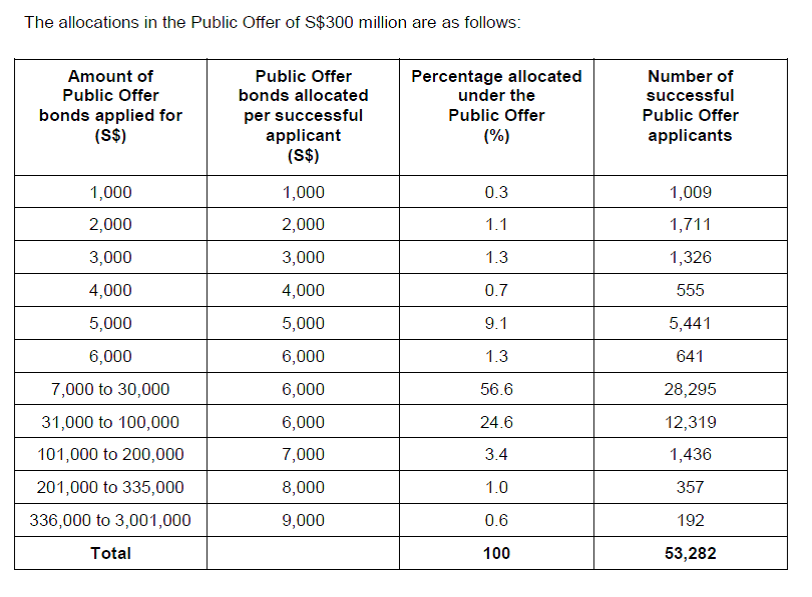

Or in more technical jargon, the retail tranche was over 8 times oversubscribed, with over S$1.6 billion of applications received, and the retail tranche was upsized from S$200 million to S$300 million. I’ve set out the allocation table below, and most investors should have received S$6,000.

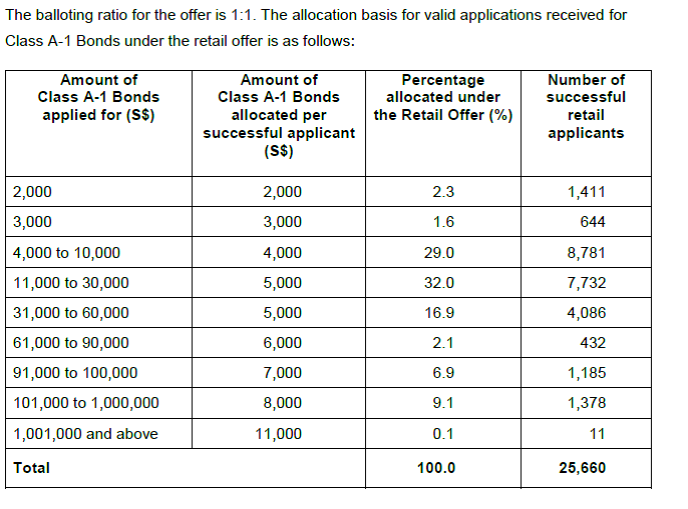

As a rough comparison, the Astrea IV Bond allocation was 7.4 times oversubscribed, with S$890 million applications received on S$121 million of bonds. Astrea’s allocation is set out below, where most people would have received S$4000.

My immediate takeaway, is that Astrea, which offers a 4.25% coupon, attracted only S$890 million in orders, while these Temasek Retail bonds, which offer a 2.7% coupon, attracted over S$1.6 billion in orders. Why are the Temasek Retail bonds so much more attractive to retail investors, when personally I felt that the Astrea bonds offered a more compelling risk-reward profile?

I have a couple of theories set out below:

- We “get it” – The Astrea IV Bonds are complex stuff. It took me a couple of hours of reading the offer documents to fully understand their structure, and even then I didn’t really know what was in the underlying security backing the bonds. By contrast, these Temasek Retail bonds are about as textbook as a bond can get. You buy the bonds, you get yearly interest, and after 5 years you get your money back, all guaranteed by Temasek. Many people have criticised Singapore retail investors for being unsophisticated, but if this theory is right, it seems that the public is actually far more sophisticated than we give them credit for.

- Risk free, duh – Despite all the talk about risk-reward, I cannot rule out the possibility that some investors just want to park their money somewhere that is completely risk free, with a return that beats inflation. There are many investors out there who would fit such a profile and be very cash rich, such as older investors, or those who need to be extra safe with their investments. For these investors, a 2.7% risk free yield is better than just about any other product available out there. The fact that you can use CPFIS for this, and the yield is higher than CPFOA’s 2.5%, is pure icing on the cake.

- Game theory – This last one is a bit of a wild card. It goes like this. Astrea has a retail tranche of only S$121 million, and the 4.25% yield is so good that every Singaporean out there is going to apply for this. Accordingly, there’s no point in me applying for too much, otherwise I’m just wasting my S$2 application fee and opportunity cost of the funds. The Temasek Retail bonds have a S$200 million tranche with a possible upsize to S$300 million. The yield is 2.7%, which is not fantastic, so perhaps not many Singaporeans will apply for it. Since I really like these things, I should apply for more, in the off chance that I actually do get more. And when every investor thinks this way, you have a massive oversubscription.

Do you agree with any of the above? Leave your thoughts below!

Reader Comments

A huge shoutout to all readers who commented on my Temasek Retail bond article, because the quality of comments was truly amazing.

Unfortunately I was on the road the past week, so I didn’t get a chance to respond to you guys personally, huge apologies for that. In any case, the comments were really insightful and warrant a proper response, so I wanted to address them in this article.

Reader: Hi, I know this is not a fair comparison, but comparing the GE270 endowment (which has already closed a few months back) and the Temasek bonds, which do you think is a better option?

Financial Horse says: I didn’t follow the GE270 endowment closely, so I did a quick read up (there’s a nice summary on Seedly):

- They are 5-year single premium – consumers will invest a lump sum into the policy which lasts for 5 years.

- The policy pays out an interest of 2.70% every year. This is guaranteed by Great Eastern.

- One can choose to either withdraw the 2.70% interest earned every year or reinvest it into the policy.

- Minimum investment of S$10,000

- Slight penalty if you want to exit before 5 years

There are 2 key differences between these Temasek Retail bonds and GE270:

- Credit Risk – With the GE270, you’re taking on the credit risk of Great Eastern. With the Temasek Retail bonds, you’re taking on the credit risk of Temasek. The risk of a default by either of them is incredibly low, but the credit risk of Temasek is much lower. If I were to rate the risk of default of GE270 from a scale of 0 to 10, it would be 0.1. Temasek would be a 0.01.

- Exit Strategy – With the GE270, there’s no easy way to exit the investment before 5 years, without paying a break fee (I couldn’t locate the exact amount, please let me know if you do). The Temasek Retail bonds are listed on the SGX, so you can always try to sell them on the SGX like you would a stock. The liquidity is poor, but if you queue long enough, or price at a discount to market, you should still be able to exit your position.

If I had to pick, I would say these Temasek Retail bonds are by far superior to GE270, for the 2 reasons mentioned above.

Reader: I’m taking the opposite view. While i totally agree with all the risk rating analysis etc but as to the part where you are comparing to fixed deposits i do not agree. Today SCB esaver and Maybank isavvy (and for priority) we are getting 1.8-2% by December 2018 and probably 2.5-3% as we expect FED to increase rates by another 75-100 basis points by December 2019. Its better to put in savings above and let interest rates roll up.

That’s actually a really interesting point you brought up.

For discussion’s sake, I’m going to share my personal view. My personal view is that some time in 2019, due to the trade war and political pressure from Trump, the Feds are going to find it harder and harder to raise interest rates in line with their current dot plot. If they do continue hiking, there is a real risk they tighten the US economy into a recession, and are forced to cut rates. In other words, either situation results in the pace of interest rate increase slowing after 2019.

The tricky part with this analysis, is knowing at what level do rates hit, before this happens. Does it go to 3% and beyond as you mention, or does it stop at 2.5%? For reference, the US Federal Fund Reserve rate is at 2.25% now, and expectations are for 1 hike in December 2018 (taking it to 2.5%), and 2 to 3 hikes in 2019 (taking it to 3.0% – 3.25%).

If you’re confident that the rate hike is going to continue unimpeded and hit 3% plus in 2019, then don’t buy these bonds, because we’re going to be seeing a much higher interest rate environment.

Personally, I’m not convinced that will be the case, and I do think 2.7% in the current climate is attractive. There’s no need to bet your house on these bonds, but they’re a useful portfolio diversifier, because sometimes our predictions about the markets just don’t pan out.

Reader: Isn’t it cheaper to buy in the secondary market when fed hikes later this year

As at Friday’s close (26 October), The Temasek Retail bonds are trading on the secondary market at 1.022, which implies a 2.23% yield to maturity, down from the 2.7% it was priced at.

However, BT sums it up well in the extract below:

“At 99.7 cents to the dollar over the counter, the HDB 2.42 per cent bonds due 2023 offer a yield to maturity of 2.48 per cent, he said. Meanwhile, at 102.10 cents to the dollar, the 2.75 per cent Singapore government bond due 2023 offers a yield to maturity of 2.27 per cent.

…

However, Mr Zhan said he was surprised when the bonds opened above 102 cents: “I believe retail investors priced the bonds too high. The yield (for the Temasek retail bonds) should not trade below those of Singapore Government Securities (SGS) or HDB.”

For reference, the Astrea bonds which were offered at a 4.25% coupon are now trading at 1.051, which implies a yield to maturity of 3.13%.

In other words, because the liquidity on the secondary markets is so poor, it calls into question whether there is efficient price discovery. So yes, I agree with you that theoretically speaking, when the Feds hike interest rates, the price of these bonds will fall. However, when that happens, most investors may choose to just hold their bonds to maturity, so you have poor liquidity and poor price discovery, so in reality the price may not budge much, as we have seen with the current pricing of these bonds on the open market.

Reader: Okay, I must first put the disclaimer that I do not have any substantial grounds to make the points I am going to make here; are there any chance that the money raised will be used to fund the purchases of “distressed” assets from HNA in the very near future? One can google “Temasek” and “HNA” together and you will get a picture of the possible upcoming deals with the troubled Chinese conglomerate.

I think the question here is this: Why would it trouble you if the money raised is used to buy “distressed” assets from HNA? Unlike equity instruments (like stocks), debt investors (like a buyer of these bonds) are not entitled to any additional upside beyond the coupon they are entitled to. As a debt investor, the only thing I care about is the credit worthiness of the guarantor, being Temasek. If they decide to buy a couple billion of distressed assets and lose money on it, I’m still okay because Temasek, being Temasek, is unlikely to default because of such losses.

Unless of course, your concern is a moral one. In which case the use of proceeds of these bonds is:

“The net proceeds will be provided by the Issuer to Temasek and its Investment Holding Companies to fund their ordinary course of business.”

So yes, they can theoretically use it to buy assets from HNA if they want to. Although from a pure, investment perspective, it doesn’t really matter all that much what they do with the money.

Reader: I test sell SGS on Sgx for 6 months in queue. Yes its was very very difficult to sell without taking a loss. Even if i was willing to take a small loss, still no buyer. The market makers are all the banks and boy they are much smarter than all of us. So FH is right to be cautious about liquidity risk.

From the past 1 year trend, I am guessing that in 2 years’ time or maybe even shorter, the 5Y yield may touch 2.7%, which means the market price will be below $1. It is just 0.3%+ away. So buy with the mindset of a 5 years lockup is safe approach.

Thanks for the great share! I’ve mentioned many times that liquidity on the SGX is a real issue (just try placing a buy/sell order for a low liquidity counter), and this is fantastic evidence of that.

Reader: In the last PE bond, those who applied for > $1M only get $11K. They must be cursing, thinking WTF waste my time, only got 0.1% allocation. The problem again is the $200M issue size is too small. Just take a few UHNWI (with net worth more than US$50M which SG has plenty) to dump in some money and it will be hugely oversubscribed.

I didn’t apply the last round but for average joe, not too happy too if I did apply. Those who apply for $60K only got $5K. Again I think they will probably think “waste my time” since the annual coupon of $200 is so little.

Since the media blew this up, don’t expect to get more than $5K even if you throw in a lot. So was wondering is it worth the effort and my $2 this time?

The way I will play these bonds is this:

- Ultra High Net Worth Individual – If I am a UHNWI, I will be going via the placement tranche to institutional and accredited investors. No point fighting with the mom and pop for a measly S$6000 in bonds.

- Retail Investor – If I am a retail investor, the lesson from Astrea and these Temasek Retail Bonds is clear. They tend to be heavily oversubscribed, and Temasek’s method of allocation is similar to how they allocate SSBs: everybody who applied will get some. So for future offering, I will just apply about S$11,000 max, that seems to be the sweet spot to ensure you get the largest allocation while not incurring ridiculous opportunity cost on the subscription funds.

Till next time, Financial Horse, signing out!

Financial Horse has a set of 7 Commandments for Successful Investing, that I ask myself before making every investment, and that I will never break regardless of the situation. Enter your email below to receive a copy in your inbox!

[mc4wp_form id=”173″]

Enjoyed this article? Like our Facebook Page for more great articles, or join the Facebook Group to continue the discussion!

[…] put it in perspective, the Temasek 5 year 2.7% Retail bonds had S$1.6 billion of applications on a S$300 million public tranche (5.3 times oversubscribed). The […]