Hot on the tails of the recent Astrea IV private equity bonds, comes the latest Temasek T2023 5 year Retail Bonds with a 2.7% coupon. In my recent Astrea article, I advanced the argument that Temasek (and Ho Ching) are trying to open up the retail bond scene, and I hate to say I told you so, but you know… I did write it a few months back. But let’s not take anything away from them, huge kudos to them for taking this upon themself.

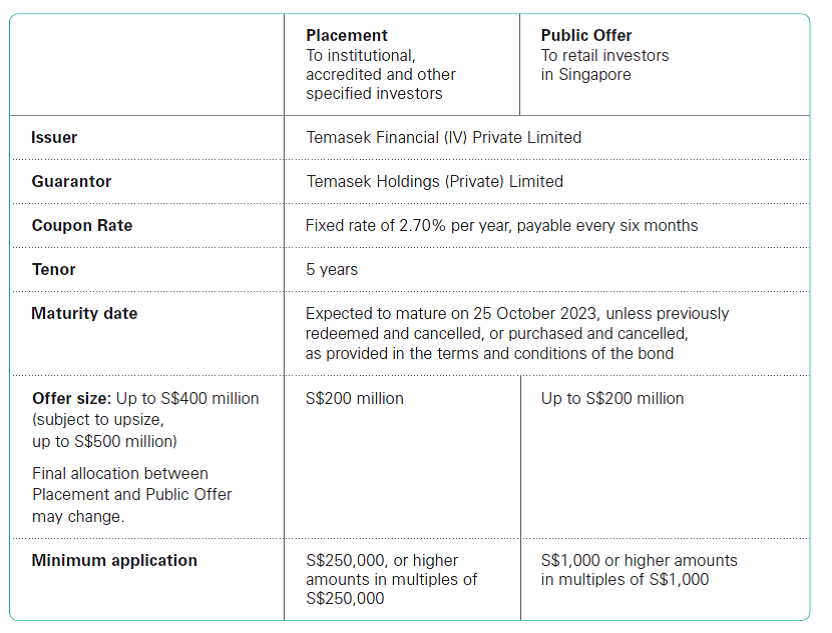

Basics: T2023-S$ Temasek Bond Offer

These bonds are not the most complex things on earth. They’re issued by a subsidiary of Temasek (which is fairly standard corporate structuring). They’re backed by the Temasek parent, and they pay a fixed rate of 2.70% per year, bi-annually. They will be redeemed by Temasek after 5 years. The bonds will be listed on the SGX-ST so you can sell them on the open market, but apart from that there is no way to exit your investment before the 5 years.

I’ve extracted some further information below, as well as some excerpts from Temasek:

What was the coupon rate for the August bond?

The coupon rate for the T2028-US$ Bond was 3.625%.

How is this different from Astrea Bond?

The Astrea IV PE Bonds are asset-backed securities that are backed by cash flows from a diversified portfolio of private equity funds, which offers potential for higher returns but also comes with higher risks. Conversely, The T2023-S$ Temasek Bond is a type of plain vanilla corporate bond that is reliant on Temasek’s own credit quality. It is fully guaranteed by Temasek, a triple-A rated issuer, with significantly lower risks than a private equity-linked product, but with a lower return profile.

How did you decide on the T2023-S$ interest rate?

The T2023-S$ Temasek Bond interest rate was determined via a book building process, based on demand from institutional and other specified investors. These investors could have considered credit quality, risk, market interest rates, outlook, and other factors in their bids. Bid results of this market-based price discovery were then used to determine the bond interest rate. This is how we have always set the rate on our bonds.

Retail investors are offered the same interest rate as institutional, accredited and other specified investors.

Can I use Central Provident Fund (“CPF”) funds or Supplementary Retirement Scheme (“SRS”) funds to apply for the Temasek Bond in the Public Offer?

The T2023-S$ Temasek Bond is eligible for inclusion under the CPF Investment Scheme – Ordinary Account. You can use up to 35% of their investible savings in your CPF Ordinary Account to apply for the T2023-S$ Temasek Bond in the Public Offer.

You cannot use your SRS Funds to apply for the Public Offer. You should consult your stockbroker and the relevant bank in which you hold your SRS account if you wish to use your SRS Funds to purchase the Temasek Bond from the secondary market after the completion of the offer, and the listing of the Temasek Bond on the Main Board of the SGX-ST.

Default Risk

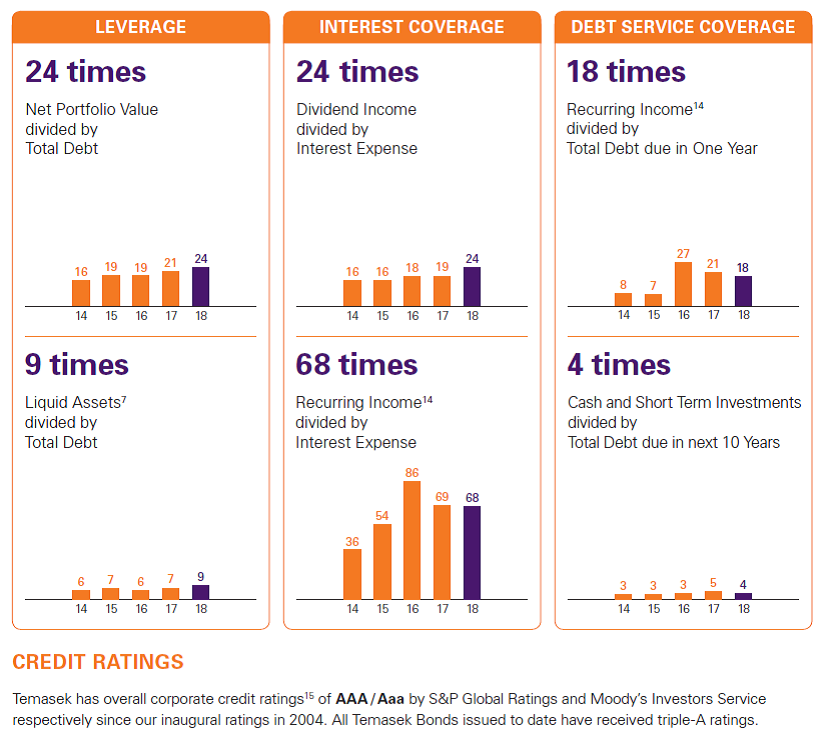

On to the juicy stuff. Default risk. There’s a fancy chart below that shows you the financial coverage ratios for Temasek. But frankly, we all know that we’re wasting time here. Temasek is not going to default in the next 5 years. As a sovereign wealth fund, Temasek in some ways is a proxy to the credit rating of the Singapore government, and a bellweather of the Singapore economy. The global perception of a Temasek default would be catastrophic for Singapore as a country. I’d even go so far as to say that if Temasek defaults, we as Singaporeans have bigger problems than worrying about a bunch of retail bonds.

Long story short, these bonds are risk free. I’m prepared to stake my reputation as a financial blogger on them, that’s how confident I am.

Yield

The most natural comparison for these Temasek Retail bonds,will be the Singapore Savings Bond (SSB), the Singapore Government Securities (SGS), and Fixed deposits.

I’ve extracted the full yields below, but broadly, they are:

- SSB: 2.22% (if you hold for 5 years)

- SGS 5 year: 2.3%

- Fixed Deposit: 1.8%

For reference, Temasek actually recently issued 10 year USD bonds at 3.625%, but that was USD, so it’s not really an apples to apples consideration (USD borrowing costs are higher that SGD).

To sum up, we’re looking at about 40 to 50 bps premium for these Temasek Retail bonds, over prevailing SSBs and SGS. My personal take is that the 2.7% yield for 5 year SGD bonds with no default risk is by far the best you’re going to have access to in the market today as a retail investor. There really is no alternative product out there for retail investors with this kind of characteristics.

| Year from issue date | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

| Interest, % | 1.80 | 2.09 | 2.27 | 2.42 | 2.54 | 2.63 | 2.69 | 2.75 | 2.84 | 2.98 |

| Average return per year, %* | 1.80 | 1.94 | 2.05 | 2.14 | 2.22 | 2.28 | 2.34 | 2.38 | 2.43 | 2.48 |

Singapore Government Securities

| TREASURY BILLS | BONDS | |||||||||||||

| 1-YEAR | 2-YEAR | 5-YEAR | 10-YEAR | 15-YEAR | 20-YEAR | 30-YEAR | ||||||||

| ISSUE CODE COUPON RATE MATURITY DATE |

BY18102F

31 JUL 2019 |

NY05100N 3.250% 01 SEP 2020 |

NX13100H 2.750% 01 JUL 2023 |

NX18100A 2.625% 01 MAY 2028 |

NZ13100V 3.375% 01 SEP 2033 |

NZ16100X 2.250% 01 AUG 2036 |

NA16100H 2.750% 01 MAR 2046 |

|||||||

| YIELD | PRICE | YIELD | PRICE | YIELD | PRICE | YIELD | PRICE | YIELD | PRICE | YIELD | PRICE | YIELD | ||

| 10 Oct 2018 | 1.87 | 102.19 | 2.06 | 101.59 | 2.39 | 99.91 | 2.64 | 105.62 | 2.91 | 90.49 | 2.94 | 95.61 | 2.99 | |

| 11 Oct 2018 | 1.87 | 102.21 | 2.05 | 101.80 | 2.34 | 100.37 | 2.58 | 106.26 | 2.86 | 91.12 | 2.89 | 96.41 | 2.94 | |

| 12 Oct 2018 | 1.87 | 102.23 | 2.04 | 101.80 | 2.34 | 100.35 | 2.58 | 106.25 | 2.86 | 91.18 | 2.89 | 96.49 | 2.94 | |

| 15 Oct 2018 | 1.87 | 102.27 | 2.01 | 101.92 | 2.32 | 100.55 | 2.56 | 106.51 | 2.84 | 91.51 | 2.86 | 96.95 | 2.91 | |

| 16 Oct 2018 | 1.88 | 102.25 | 2.02 | 101.84 | 2.33 | 100.30 | 2.59 | 106.13 | 2.87 | 91.11 | 2.89 | 96.37 | 2.94 | |

| 17 Oct 2018 | 1.88 | 102.22 | 2.04 | 101.85 | 2.33 | 100.34 | 2.58 | 106.28 | 2.85 | 91.27 | 2.88 | 96.61 | 2.93 | |

Fixed Deposit (12 Month)

| Bank/financial institution | Min. deposit amount | Tenure | Promotional interest rate |

| CIMB | $10,000 | 12 months | 1.84% p.a. (online only, expires 31 Oct) |

| Maybank | $20,000 | 12 months | 1.75% p.a. (with $2,000 deposit in current/savings account) |

| ICBC | $20,000 | 12 months | 1.75% p.a. |

| HSBC Advance | $30,000 | 12 months | 1.65% p.a. (expires 31 Oct) |

Liquidity

These Temasek bonds are not like SSBs. You can’t just put in an application to have them redeemed any time you want, with pro-rated interest. If you buy these things and you want to exit them before the 5 years is up, your only way out is to sell them on the SGX, where liquidity for retail bonds is “low”. And “low” is actually me being polite, because for reference, the liquidity of the Astrea IV Bonds on the SGX today is, and I kid you not, “Sell Volume 166, Buy Vol: 21”.

So if we use Astrea as an indicator of market liquidity, it’s going to be “challenging” to exit these bonds on the open market. You’re probably going to have large bid-ask spreads, so do expect to have to price them below the trading price, or to be quite patient, when exiting these bonds.

Perhaps in time the retail bond scene will deepen to the point where we see active trading of SGD bonds on the SGX. Will moves like these from Temasek, there’s actually a decent chance we may get there within the next decade. Unfortunately, as at the time of this article, I don’t think the local market has evolved to that point yet.

Rising Interest Rate environment

The other problem, is the rising interest rate environment. The US Federal Reserve is on a rate hike cycle, and this is likely to spill over to Singapore bond yields. Depending on how aggressive the Feds are, this may actually result in quite a significant rerating of yields for Singapore bonds over the next 1 to 2 years. And when yields go up, bond prices fall.

Don’t get me wrong, none of this matters if you plan to hold the bonds for 5 years. No matter how much interest rates go up, these bonds will still continue to pay a 2.7% fixed interest per year. The concern though, is how would rising yields impact the market price of these bonds, as traded on the SGX. Personally, I think over the mid to longer term, prices may get negatively impacted, as the SGS yield goes up. I could be wrong though.

The net effect of these, is that we a low liquidity bond and a rising interest rate environment. In other words, trying to exit these Temasek bonds before the 5 years is up may prove challenging.

How to play this?

The way I see it is this. These bonds are fantastic if you have money that you don’t need for 5 years, and don’t want to take any risk with them. There’s a lot of people who can fit this profile, for example:

- You’re overexposed to equities, and you need exposure to risk free SGD fixed income.

- You’re an older investor nearing retirement, and you want a safe investment that wouldn’t keep you awake at night, but can keep up with inflation.

- You’re basically Singaporean Elon Musk and hugely exposed to risks in your business, so you want something safe for your personal investments.

For any of the persons above, the 2.7% yield you’re getting from these Temasek Bonds is much better than anything else you’re going to get on the market today, which will mainly be SSBs, SGS and Fixed Deposit.

Don’t forget that these Temasek Bonds can be subscribed for through CPFIS. If you have more than S$20,000 in your CPF-OA, and don’t plan to use the excess money in the next 5 years, just buy as much of these bonds as you can, you’ve basically just made that 0.2% (over the CPF-OA 2.5% yield) spread for free.

Financial Horse, are you subscribing for this?

I really like these bonds. I really like that Temasek is making efforts to open up the retail bond scene here. I really like that they offer a nice spread over comparable SSBs and SGS. Unfortunately, these Temasek bonds just don’t fit into my current portfolio strategy. As a young investor, I want huge exposure to equities and REITs, and for the remainder of my portfolio, I want them in liquid assets that I can access at a moment’s notice. And these bonds just don’t fulfil that liquidity criteria. For me, I’ll stick to savings accounts like DBS Multiplier or UOB One, or SSBs, for the fixed income portion of my portfolio. The yield is lower, but that’s the price I have to pay for better liquidity.

I will be giving these Temasek Retail Bonds a 4 financial horse rating. The yield is good, and they are risk free, but unfortunately liquidity may be a concern, so they will not be for everyone.

Financial Horse Rating –T2023-S$ Temasek Bonds

![]()

![]()

![]()

![]()

Financial Horse has a set of 7 Commandments for Successful Investing, that I ask myself before making every investment, and that I will never break regardless of the situation. Enter your email below to receive a copy in your inbox!

[mc4wp_form id=”173″]

Enjoyed this article? Like our Facebook Page for more great articles, or join the Facebook Group to continue the discussion!

Hi, I know this is not a fair comparison, but comparing the GE270 endowment (which has already closed a few months back) and the Temasek bonds, which do you think is a better option?

Apologies for the delayed response as I was on the road the past week. I’ve responded to you here: https://financialhorse.com/temasek-bonds-debrief/

Isn’t it cheaper to buy in the secondary market when fed hikes later this year

Apologies for the delayed response as I was on the road the past week. I’ve responded to you here: https://financialhorse.com/temasek-bonds-debrief/ 🙂

Okay, I must first put the disclaimer that I do not have any substantial grounds to make the points I am going to make here; are there any chance that the money raised will be used to fund the purchases of “distressed” assets from HNA in the very near future? One can google “Temasek” and “HNA” together and you will get a picture of the possible upcoming deals with the troubled Chinese conglomerate.

This sounds scary. Defaults in China is going up.

Apologies for the delayed response as I was on the road the past week. I’ve responded to you here: https://financialhorse.com/temasek-bonds-debrief/ 🙂

i m taking the opposite view. while i totally agree with all the risk rating analysis etc but as to the part were you are comparing to fixed deposits i do not agree. today SCB esaver and Maybank isavvy (and for priority) we are getting 1.8-2% by december 2018 and probably 2.5-3% as we expect FED to increase rates by another 75-100 basis points by dec 2019. its better to put in savings above and let interest rates roll up

I test sell Sgs on Sgx for 6 months in queue. Yes its was very very difficult to sell without taking a loss. Even if i was willing to take a small loss, still no buyer. The market makers are all the banks and boy they are much smarter than al of us. So FH is right to be cautious about liquidity risk.

From the past 1 year trend, I am guessing that in 2 years’ time or maybe even shorter, the 5Y yield may touch 2.7%, which means the market price will be below $1. It is just 0.3%+ away. So buy with the mindset of a 5 years lockup is safe approach.

Apologies for the delayed response as I was on the road the past week. I’ve responded to you here: https://financialhorse.com/temasek-bonds-debrief/ 🙂

In the last PE bond, those who applied for > $1M only get $11K. They must be cursing, thinking WTF waste my time, only got 0.1% allocation.The problem again is the $200M issue size is too small. Just take a few UHNWI (with net worth more than US$50M which SG has plenty) to dump in some money and it will be hugely overscribed.

I didn’t apply the last round but for avergae joe, not too happey too if I did apply. Those who apply for $60K only got $5K. Again I think they will probably think “waste my time” since the annual coupon of $200 is so little.

Since the media blew this up, don’t expect to get more than $5K even if you throw in a lot. So was wondering is it worth the effort and my $2 this time?

Apologies for the delayed response as I was on the road the past week. I’ve responded to you here: https://financialhorse.com/temasek-bonds-debrief/ 🙂

In a fast rising interest rate environment, it is foolish to lock-in 5 years for only 2.7%p.a. Currently at 2-2.25% with one more hike(almost a certainly) in Dec 2018 and another 3 more in 2019, it really doesn’t make sense. Historically at 25 basis points for each hike, or a quarter % each time, it means another one full percentage to the current 2%, making it 3%!

So at end 2019 or from 2020 onwards, this T2023 bond investors will be sucking thumb seeing their peers having 3% in FD while they are locked up till 2023 with a measly 2.7%?

Yea bro you are spot on. I have a 5Y trench in July at 2.12% but Sg 5Y benchmark has jumped to 2.35% last Friday. I lost 0.23% in barely 3 months. Want to sell must take a loss now. With 5Y at 2.35% now, just another 0.35% shy of the 2.7% from Temasek.

Apologies for the delayed response as I was on the road the past week. I’ve responded to you here: https://financialhorse.com/temasek-bonds-debrief/ 🙂

[…] docs available on their website) comes hot on the tails of the previous Astrea IV Retail Bonds and Temasek Retail Bonds. It definitely looks like like Temasek is trying their best to open up the local retail bonds […]

[…] docs available on their website) comes hot on the tails of the previous Astrea IV Retail Bonds and Temasek Retail Bonds. It definitely looks like like Temasek is trying their best to open up the local retail bonds […]