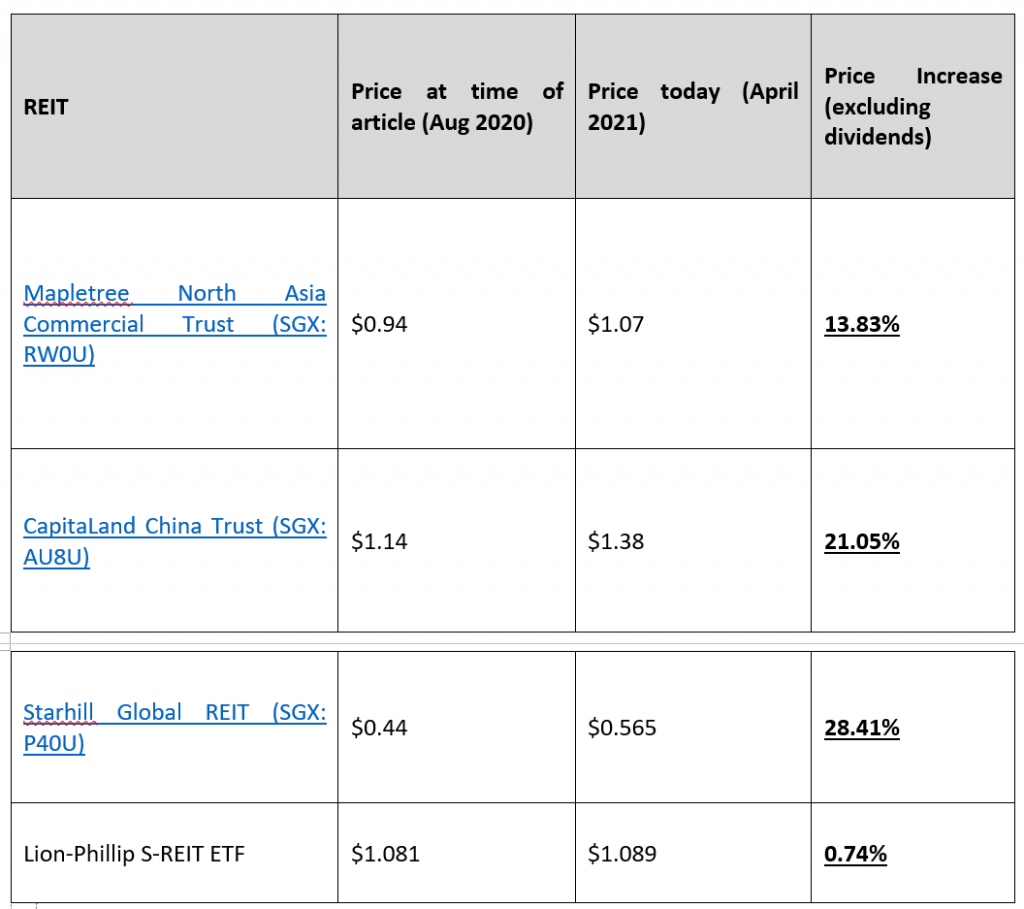

In Aug 2020, I wrote a post on the best 3 Singapore REITs to buy now.

8 months on, I checked back on the results:

Results were very good actually.

The average return of the 3 was 21% excluding dividends, handily beating the Lion-Philip S-REIT ETF which only hit 0.74% capital gains.

Even the worst of the 3 on the list, Mapletree North Asia Commercial Trust, hit a 13.8% return which isn’t too shabby.

Starhill Global REIT did very for me (28% returns). My fair value estimate for Starhill back in 2020 was in the high 50s, so it’s hit the price target for now. You can learn more on how to value REITs in the REITs MasterClass if you’re interested.

BTW – we share commentary on financial markets every week, so do sign up for our mailing list, its absolutely free (goes out every Sunday).

Don’t forget to join our Telegram Channel and Instagram or (YouTube)!

[mc4wp_form id=”173″]

General Views on Singapore REITs today (2021)

But that’s all in the past.

Fighting yesterday’s battles is a poor recipe for success, so the big question – what are the top 3 Singapore REITs to buy now for 2021.

Personal Views on Singapore REITs

And that’s where it gets tricky.

As I was doing this article, I found it really, really hard to pick out 3 REITs that I liked at today’s price.

So I dug a bit deeper, and it turns out the entire REIT index has rallied significantly.

The graph below sets out yield spread between the REIT Index and the 10 year Singapore government bond.

It’s not rocket science.

The black line is the average (mean), and the bars are 1 or 2 standard deviations from the mean.

So if you buy REITs when they are above the black line, you raise your chances of making money.

If you buy REITs when they are below the black line, your chances of making money are reduced.

The further you get from the black line, the further you skew your chances of making / losing money.

Based on this, REITs are looking fairly valued, but of course, not as overvalued as they were in 2019.

Macro Views on REITs

But Valuations don’t provide a timing guide, for that we need to look at macro.

And macro is not supportive as well.

As shared previously, I think the broader trend for yields going forward is up.

We’ve had a brief respite the past month, but at some point yields will continue their march up as the world continues to reopen.

And there’s nothing scarier for a REIT investor than rising interest rates.

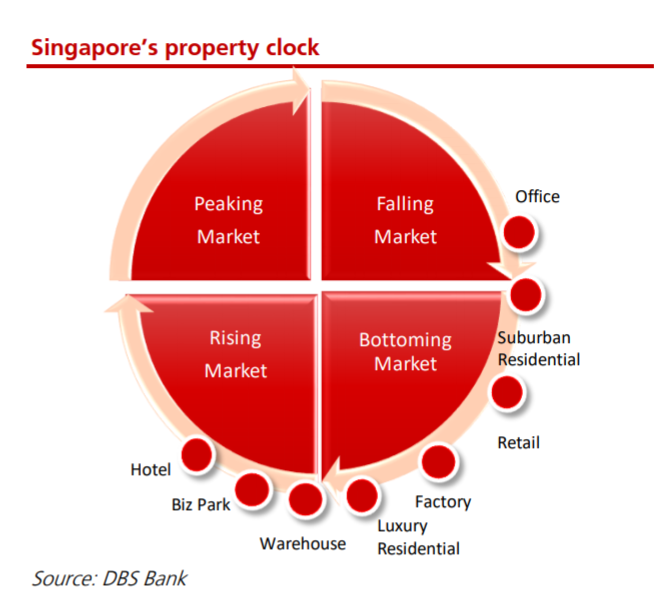

REIT Asset Classes

So that’s REITs generally, then we need to break down by asset classes.

I just love the property clock by DBS below – which shows you where each asset class is in the cycle:

Office REITs

I agree with DBS on this one.

Office rents are in a falling market, yet to bottom.

COVID has changed the way we work, and companies have realized that we can move to a flexi working model and still achieve similar results.

While drastically reducing rent.

The past 12 months, most companies took a wait and see approach, signing short term 6 to 12 month renewal of their office leases.

As 2021 starts to play out, I think more companies will decide that flexible working is a viable option, and look to cut office footprint.

Longer term, perhaps this trend will reverse when companies find flexible working not as efficient, but this looks to be the trend for now.

I’m still very bullish on Grade A office spaces in the CBD longer term, but short term I think rents will continue to correct.

Retail REITs

Last year’s unwanted child is this year’s best performer.

Which just goes to show you that as long-term investors, you cannot be subject to the whims of the market.

Per DBS’s chart, Retail is in the process of bottoming, and I would generally agree with that.

I think the worst is over for Retail, and going forward will be a gradual recovery.

The problem is that a lot of that has been priced into the REITs today.

There’s a saying about how the market is forward looking by 6 to 12 months.

To catch today’s retail recovery, you need to have invested 6 months ago. Around the time I wrote my previous article ????.

I think the right time to buy retail was last year. I bought the big names like MCT and CMT in bulk last year, and even the smaller ones like Starhill Global REIT.

But today, prices are very close to fair value, and I don’t see much opportunity anymore.

They still do well in the long term, but short term they’ll probably be range bound.

Industrial REITs

And again – last year’s best performer is this year’s unwanted child.

Industrial REITs had an amazing 2020 because it was the only real estate class that was immune to COVID.

Throw in interest rate cuts and that was rocket fuel for Industrial REITs.

But now the world is reopening, and yields are going up, so Industrial REITs are falling.

I think we’re still on the early side for this trade, but I think in the next 3 to 6 months there could be a great opportunity to add to Industrial REITs.

Of the 4 asset classes, I see the most opportunity here in 2021, at least for long term investors who can buy and hold.

Hospitality REITs

Hospitality is a weird one.

Hospitality REITs have been very strong throughout the entire COVID crisis, which just blows my mind because earnings have been hit badly.

It’s like the airline trade where investors have piled in to support prices.

Anyway, the tricky part about hospitality is that every market is different.

Owning a Singapore hotel vs owning a China hotel vs a US hotel are just completely different investments.

Singapore hospitality tends to be stable because the government controls the land supply that can be used to go into building hotels, and Airbnb is not allowed for short stays in Singapore.

But every country is different.

My current view is that I would prefer to play hospitality via the online travel agents (OTAs – Airbnb, Booking.com, Trip.com etc), but that’s just my view.

Top 3 REITs to buy now for Singapore Investors (2021)

With that out of the way, let’s look at the Top 3 REITs to buy for Singapore Investors.

Disclaimer – Please do not take this as financial advice. You need to understand your own investment objectives and risk appetite before investing. If in doubt, check with your financial advisor.

Ascendas REIT A17U (SGX)

It suddenly occured to me that after loading up in REITs in 2020, the only REIT purchase I made in 2021 was Ascendas REIT.

At today’s price of $3.1, Ascendas REIT trades at 1.36x book value, and a 4.73% trailing yield (3.17% yield spread vs the 10 year SSB at 1.56%).

Not exactly cheap, which is why I would be more keen to add only if it corrects in the second half of 2021. But frankly, it’s the same problem with all the REITs out there today.

But no denying that Ascendas REIT’s underlying portfolio is great. It’s split between industrials and business spaces, in Singapore, Australia, US, UK/Europe.

They’ve recently made a move to acquire a bunch of data centres, which will bring exposure up to 10% after this, which will be helpful to future proof the REIT.

Data Centers today trade at a much bigger premium to book than industrial space, so the market price has adjusted in recent weeks to reflect that.

Great REIT by a great sponsor (CapitaLand), all that is left to pick it up at a great price.

You can argue that all these REITs are cheap today if you adjust for record low interest rates, and sure, that’s one way to look at it.

Mapletree Commercial Trust N2IU (SGX)

At current price of $2.12, Mapletree Commercial Trust trades at 1.24x book value, 3.54% historical yield.

Trailing twelve month yield is not meaningful because COVID impacted the retail space very heavily.

I would say Mapletree Commercial Trust is about fairly valued at this price.

Which is exactly the challenge with coming up with this list. All the REITs are looking very fairly valued today, so in such a market I would rather go with quality.

And that’s where MCT shines – very strong underlying portfolio.

They own 2 absolute gems in the Singapore commercial real estate space – Vivocity and Mapletree Business City.

These comprise almost 80% of the portfolio, and is pretty much all you’re buying the REIT for.

There is some office exposure which will hold the REIT back short term though.

The committed occupancy numbers are very strong, but many landlords are keeping occupancy up by cutting rents.

So the number is not meaningful without looking at rental reversions, which unfortunately we don’t have at the moment.

That said, Mapletree Commercial Trust and CapitaLand Integrated Commercial Trust are about the bluest blue chip REITs you can get if you’re buying into the retail space in Singapore.

Long term it’s hard to go wrong with either of them unless economic growth in Singapore drops. Which means all that is left is to pick them up at a good price.

Mapletree Industrial Trust ME8U (SGX)

At current price of $2.8, Mapletree Industrial Trust trades at 1.65x book value, 4.34% trailing yield (2.78% yield spread).

Again, that’s just not cheap, and the reason why is because of the 38% data center exposure versus Ascendas REIT’s 10% exposure.

Truth be told, I’m not a big fan of data center REITs longer term.

To me, the guy running the data center REIT is just providing the building and the electricity.

Whereas the real value comes not from the building, but from the servers that go in, and the information that flows through it.

So the guys like Nvidia, AMD, Intel, or the guys like Google, Alibaba, Tencent, are the ones who hold the real value.

Longer term, it’s not that hard for other real estate developers to come in and build competing data centers.

And it’s not like retail where the location of the building is a strong moat. With data centers, as long as you’re in the rough vicinity of the population center you’re fine. A couple hundred km either way doesn’t affect latency all that much.

But I won’t deny that some diversification makes sense, and Mapletree Industrial Trust has a very solid Singapore industrial portfolio as well.

Organic DPU growth year on year is 3.8%, which just shows you the climate we are in today.

All that excess liquidity and low interest rates have bid up asset prices, creating very high asset prices across the board.

Honourable Mention: Other REITs to buy

Very honourable mention to some very solid REITs that almost made it onto this list:

- CapitaLand China Trust

- Mapletree Logistics Trust

- CapitaLand Integrated Commercial Trust

- Starhill Global REIT

- Lendlease REIT

Truth be told, I think most of the REITs are looking very fairly valued today.

This isn’t like August 2020 when the big REITs had recovered, but the smaller REITs were still priced at a discount, which made an easy arbitrage by sticking to the small cap REITs.

What about US / Europe / Australia REITs?

Some of you have asked why I stick mainly to REITs that hold Singapore and China properties.

The answer is mostly personal.

Real estate is a very local business.

Once you understand the global macro trends, picking between REITs requires you to have a good understanding of the local property market.

And I find that I just don’t have the time or interest to keep up to date with US or European property markets (or Australia).

So I just keep it simple and I stick with Singapore and China.

Both are markets I am familiar with, and both I am very bullish on in the longer term.

But this one is unique to me. If you lived in Australia for a long time and are familiar with the real estate there, by all means go ahead! That could well be your edge as an investor.

Closing Thoughts: Are Singapore REITs a good buy now?

If I were to sum up this article in 1 line, it would be this:

REITs today are about fairly valued, but rising yields going forward will create interesting opportunities.

Sounds like a fortune cookie note now that I think about it.

2020 was a monster of a year for REITs, and I absolutely loaded up back then.

But 2021 has been an absolute snooze-fest in the REIT space, and I only added a small amount of Ascendas REIT this year.

I’ve been spending more of my time adding in the tech space in China and US, building long term positions. My personal stock watch (and personal portfolio) for REITs and stocks are available on Patron if you’re keen.

But if I’m right, then at some point the respite we are in will be over, and yields will continue their march upwards. Once that happens, the whole REIT space could become very interesting again.

I would say some time in second half of 2021, give or take.

Some of you have asked me whether to buy REITs at this price. I think the answer really depends on you.

If you have zero REITs exposure today, then maybe averaging in would make sense. Or if your strategy is to DCA for 10 years, then market timing shouldn’t really be something you’re focusing on. But if you’re like me and you loaded up on REITs in 2020, then it’s also an option to take a break from REITs for a few months and focus on other sectors like tech, and then come back to this space later in 2021.

Do note though that things can change very quickly in this market. This article is written on 24 April 2021 and will not be updated going forward. You can find my latest thoughts on REITs (and my stock watch and personal portfolio) on Patron.

Love to hear your thoughts!

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Both are THE best quality investment courses available to Singapore investors out there!

MIT is expensive. Most investors focus on the data centre but how about the rest of the properties? Light industrial, flatted factories are lousy assets and the occupancies are low (relatively). Their business parks occupancy is also not impressive. Just my thoughts.

Interesting. What would you replace MIT with on this list in that case?

Thank you for the very useful article. Any reason why none of the Frasers related REITs is in your Honorable Mention list?

Personally I think the entire market is quite fairly valued right now. In which case I would want to go with quality – which are the CapitaLand and Mapletree names in my view.

But to be fair, the Frasers names are very strong too, so feel free to go with them if you like the Frasers REITs.

Most are fairly valued. Maybe if I have to choose one, then its FLCT. Well run company . So may have more upside as it just replace Jardine Strategic in STI.

Interesting, thanks for sharing! I hear a lot of good things about FLCT as well. Unfortunately I don’t follow Aussie real estate closely so can’t really comment there.

Maybe good to diversify away from writing about ah kong reits all the time? The reit space has many reits. Good stuff must share. 🙂

Hahaha I hear you. Will try to cover more of the non-ah gong REITs. 😉

At 2.98, Ascendas REIT looking attractive today? 🙂

Would love to get it lower. I remember adding at 2.8+ earlier this year, so even after the drop it’s still higher than my last buy in. 😉

What do you think of cict now that it’s dropped a decent amount and it’s at S$2.10?

I think it’s pretty fairly valued now to be honest.

I really like REITs with a mid term perspective because I think we’re going into a more inflationry era, and real estate is a great hedge.

But short term, I think rising interest rates are going to cause a problem. Of course, not everyone would agree with me that the path ahead is for rising interest rates, so let’s see. 😉

Thank you for the insightful article. Looking forward to your next update on REITs in 2021 – curious to see if you’ve any new views on the performance and if you are keeping your eyes on any other REITs.

Sure, will do an update soon. I still think interest rates are going up – which will create good opportunities here. 🙂