There’s an interesting exercise that fund managers like to run. And it goes like this. Imagine that you’re a fund manager and you just raised S$100 million for a new fund. Because your fund is brand new, you own absolutely no stocks at all. This means that over the course of the next 3 to 6 months, you need to deploy most of your newly raised capital into the market. What stocks do you buy?

It’s an interesting exercise because it forces you to set aside all your preconceived notions about where stocks were 1 year ago, where they will be 1 year later, and to focus on one very simple question: Which stocks are sufficiently attractive to invest in right now?

Given the huge run up in global asset prices in January 2019, and all that macro uncertainty out there surrounding the trade war, brexit, interest rate hikes etc, I thought it would be an opportune time to run this exercise.

The ground rules I set for myself are simple:

- Select 5 stocks that I am keen to buy at current market prices

- Singapore stocks only

- Holding period is 5 to 10 years.

Here are my 5 picks, arranged in no particular order.

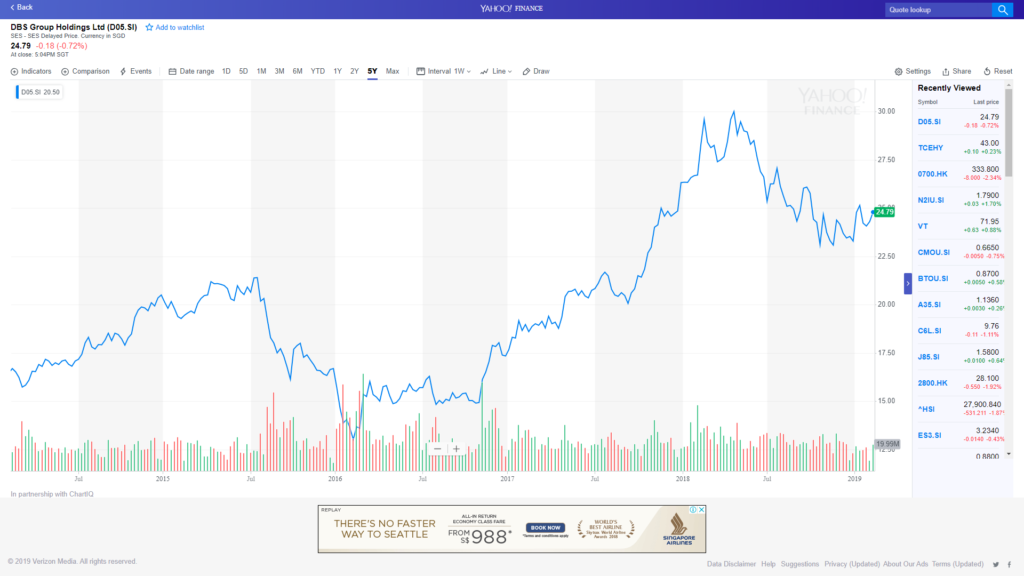

1. DBS Group Holdings Ltd (D05.SI)

I like this stock because:

Biggest lender in South East Asia – As Singapore’s and South East Asia’s largest lender, this stock is practically a bellweather of the strength of the Singapore economy, and you get broad exposure to the Singapore and South East Asia growth story. The fact that it’s Temasek backed is just icing on the cake.

Rising Interest Rates – Rising interest rates are good for banks because a large part of their revenue comes from lending, and when rates go up, their margins go up. There’s a bit of uncertainty over how many interest rate hikes are on the table this year. The Federal Reserve flip flopped from a confident projection of 3 hikes a couple months ago, to no hikes just last month. My personal take is that if economic data surprises to the upside, there may still be 1 or 2 hikes left this year, which makes owning banks like DBS a good hedge.

Digitisation – I picked DBS over OCBC and UOB because DBS to me, is the furthest along the digitisation path. They embarked on an ambitious exercise 1 or 2 years back to completely overhaul the entire backend to be fully digital, and I think that they will reap the benefits from operational efficiencies and new digital initiatives over the next few years. Sure, OCBC and UOB have also made similar steps to digitise the backend, but having spoken to people and having banked with all 3 banks, my anecdotal opinion is that DBS has managed this transition the best of the 3.

Risks

Valuations – The stock has corrected a fair bit from its 2018 highs, which makes for a more compelling entry point right now. However, even after the current correction, DBS’s share price is still not cheap at 1.32 times book value (5 year average is 1.2). By comparison, UOB and OCBC are both at 1.16 times book value. However, with DBS you get a higher dividend of 4.84% (vs 3+% for UOB and OCBC) at a fairly sustainable 53% payout ratio, and you also get a more digital, Temasek backed bank, which I think justifies the higher valuation. Feel free to disagree in the comments below though, I always love hearing contrary opinions.

Recession – Recessions are bad news for everyone, but especially for banks. The popular wisdom is that when a recession comes around, the percentage of non-performing loans go up (lenders go bankrupt and can’t repay their debt), and the bank’s earnings are affected. Unlike 2008, the banks are far better capitalised this time, so I don’t expect the next downturn to be an existential crisis for the financial system, but they’ll still get hit nonetheless.

Technological disruption –The risk is that a new fintech player like Ant Financial comes around, build a completely new payment and banking system from the ground up that completely bypasses the financial sector. If this happens, the legacy banks like DBS, UOB, OCBC, are all in trouble. Personally, I don’t see this happening in the near future. Unlike other industries, the financial sector is highly regulated, existing players are deeply entrenched, and there’s a lot of institutional fightback against such disrupters. It’s like trying to disrupt the oil industry. People have been trying for years, but it’s a lot harder than you would expect.

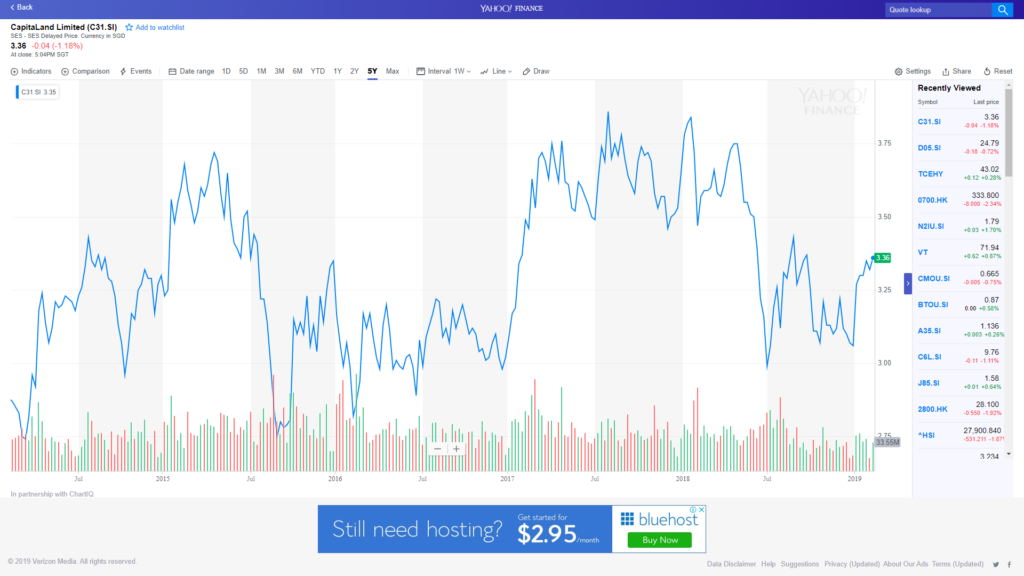

2. CapitaLand Limited (C31.SI)

I like this stock because:

Biggest real estate player in Asia – Post merger with Ascendas Sing-Bridge, CapitaLand will be the largest real estate player in Asia hands down. Unlike DBS, CapitaLand has huge huge exposure to the China market (around 50% of the asset base is in China), so this counter gives you broad exposure not only to Singapore real estate, but China real estate as well. In the longer term, I think there is little doubt that the China growth story will come to completely dominate the 21st century, so the exposure is nice.

Valuations look reasonable – CapitaLand is trading at about a 25% discount to book value, and a 3.5% trailing twelve month (ttm) yield (35% payout ratio). By comparison, CDL is trading at a 15% discount to book, because CDL doesn’t have such large exposure to China. Given the large and high quality portfolio CapitaLand holds, I think the 25% discount is attractive.

Risks

China slowdown – Probably the biggest risk here is a prolonged China slowdown. The flip side of having huge exposure to China is that if China runs into problems, the stock runs into problems. That said, given CapitaLand’s Temasek backing (51% owned by Temasek post merger), any slowdown may actually be a boon to CapitaLand as their financial backing may give them the opportunity to aggressively expand their asset base in China.

Rising Interest Rates – Rising interest rates are always bad for property counters. CapitaLand is no exception. But because we have DBS in our portfolio, and DBS will benefit in a rising interest rate scenario, I think the two counters hedge each other quite nicely.

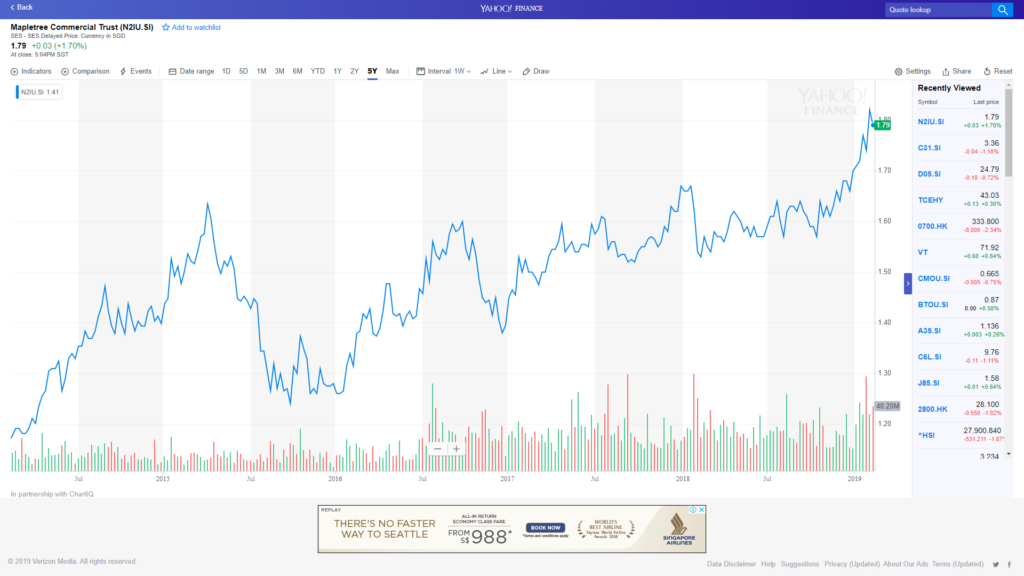

3. Mapletree Commercial Trust (N2IU.SI)

I like this stock because:

Best in class assets – I’ve talked so much about MCT on this site that I’m slightly embarrassed to repeat the same points. You can check out my previous articles here and here on previous thoughts, but simply put, this REIT gives you exposure to some of the best in class assets in Singapore in Vivocity and Mapletree Business City.

Risks

Valuation – Unfortunately, MCT is not cheap at its current price. It’s trading at a 20% premium to book, and a 5.08% ttm yield. As a comparison, CMT is trading at a 4.8% ttm yield and an 18% premium to book, while CCT is at a 4.65% ttm yield, and at book value. Viewed in such light, the stock looks less expensive. If you’re trying to build a completely new portfolio right now, you definitely need to include a REIT, and among S-REITs, I think MCT remains one of the more attractive ones.

Rising interest rates – Rising interest rates hurt REITs because whether correctly or not, the market views them as fixed income products, and trade them accordingly. When interest rates go up, the REITs distributions look less attractive, and the yield has to go up to attract buyers. That said, I think that we are nearing the end of this interest rate tightening cycle. It’s impossible to know for certain the number of hikes left and the exact timing, so the next best thing is diversification, which is why we also hold DBS in this portfolio.

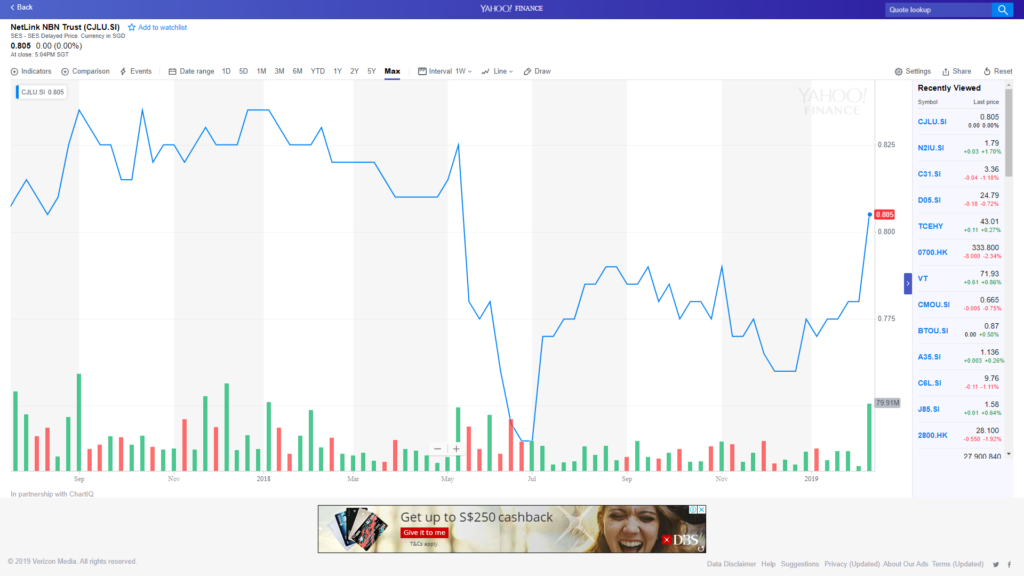

4. NetLink NBN Trust (CJLU.SI)

I like this stock because:

Monopoly status with stable cash flows – I wrote about Netlink Trust about a year ago, and most of the arguments remain valid. As the owner of most of the fibre connections in Singapore, it’s a classic monopoly with high barriers of entry (try laying fibre connections all across Singapore and see how much that costs). If you want to use a fibre connections in Singapore, chances are good that you’ll need to use Netlink Trust.

Stable yield – Because of the monopoly status, this is about as boring and safe a counter as you can get. Using the 4.64 cents projected yield, it works out to about a 5.8% forward yield, which really isn’t too bad.

Risks

Low growth – Unfortunately, don’t buy into this stock expecting breakneck growth. The rates that Netlink trust can charge are regulated by IMDA, so there’s a limit to how much they can raise rates. It’s not a REIT where you can raise rents as and when you please, or buy a new building to drive DPU growth, so if you buy into this, expect low single digit growth going forward.

Technological disruption – Over the longer term, the biggest risk to Netlink Trust is technological disruption. What’s the good of owning all the fibre in Singapore if no one uses Fibre anymore? In the short term, I don’t see any competitor to fibre connections yet. 5G is still in its infancy, and it’s targeted more for mobile customers, rather than the fixed line customers that Fibre is designed for. However, it’s still something to keep an eye on. You don’t want to end up owning a bunch of useless glass wires in the ground.

Recession – All the stocks in this list are affected by a recession. But the one that would be the least affected, is likely to be Netlink trust. Given its monopoly status, regulated rates, and its necessity status (are you ever going to cut your internet connection if you’re pressed for cash?), I expect this counter to be highly resilient in a recession, which makes it a great diversifier for the portfolio.

5. SPDR S&P 500 ETF (SPY)

I cheated on the last one. Try as I might, I simply couldn’t find a fifth Singapore stock that I liked sufficiently to include on this list. The other plays like Singtel, Singapore Airlines etc either had unattractive business models, or the risk-reward ratio wasn’t compelling for me. For the last stock, I decided to look at something far more global.

I like this stock because:

Global exposure through 1 ETF – If there is only one ETF that I can own, it absolutely has to be the S&P500.

And I’m not alone on this. Warren Buffet famously remarked that his instructions to his executors after he passed away are to invest 90% of his assets in the S&P500, and the rest in short term government bonds.

The S&P500 is a market capitalisation weighted index of the 500 largest companies in US. You can say what you want about the US, but it is by far the premier economy on earth right now, with a dynamism that just cannot be replicated elsewhere, and you’d be silly to not have at least some exposure to the US in your portfolio. Because companies this day are so global, a huge part of the S&P500’s earnings are global as well, so it’s really an ETF that gives you exposure to the global economy. And because it’s market capitalisation weighted, you get more exposure to the bigger disrupters, and the index updates itself continually, so you can literally buy this ETF, hold it for 100 years, and watch the money roll in.

Risks

Global slowdown – For very obvious reasons, a global slowdown will hurt this counter. I think in the short term (2 to 3 years), the market really could go either way, it depends a lot on how the trade war, brexit and interest rate hikes turn out, because of the impact they have on business sentiment. However because the holding period for this exercise is 5 to 10 years, I think the S&P500 is still one of the best counters here.

USD depreciation – In the longer term, there is a risk of depreciation of the USD against the SGD. Because the US government is going to issue copious amounts of debt in the coming years to fund their budget deficit, that’s going to make any holder of US treasuries very nervous. The logical outcomes are: (1) Federal Reserve monetises the debt, and prints money to buy Treasuries. The increased money supply causes the USD to depreciate, much as it did during the QE phases post 2008. If there is a recession, this is the most likely outcome. (2) In the absence of a recession, the Federal Reserve cannot justify the money printing. Foreign investors, domestic investors, hedge funds etc are left to pick up the tab. This continues until eventually investors are wary of continually purchasing increasing amounts of debt, and they start to shift assets away from the US.

It’s impossible to predict exactly how this plays out, or when it plays out, but a likely conclusion of the current path of unbridled US government spending is that the USD depreciates. Unfortunately, given the USD’s status as reserve currency and the US’s dynamism, I still think you’ll be a fool not to get exposure to the S&P500 in your portfolio. Singapore is too small an economy, and if you stick purely to Singapore stocks, you’re opening yourself up to concentration risk.

Portfolio Construction

And there you have it! The top 5 Singapore Stocks I would buy right now.

In terms of portfolio construction, I’ll probably go with 30% to the S&P500, and the remaining 70% split equally among the 4 Singapore stocks. And that would be the seed investment for my hypothetical S$100 million Financial Horse Fund! Anybody keen to contribute? 😉

For full disclosure, please note that I hold existing positions in all of these 5 stocks set out above.

Please also note that this article is based on prices and facts as at 16 February 2019. I can’t rule out the possibility that facts may change in the coming weeks and months that would affect the analysis above. If that happens, I may not update this article, but I’ll probably update my thoughts on the FH Stock Watch, so do consider signing up if you’re keen. It basically functions as my own personal stock watch, so I update it as and when I have new ideas for stocks I am interested in, and when situations changes such that existing stocks are no longer attractive.

Closing Thoughts

There’s no shortcut to investing. Making money through successful investment is really as simple as focussing on the basics: owning a broad, diversified portfolio of income generating assets over the long term. I do genuinely believe that a portfolio like the one set out above would form a great starting point for most beginner investors. By buying these 5 stocks, you get broad exposure to Singapore, South East Asia, China, and the US markets, and you get it without having to pay fees to an investment advisor (only brokerage fees). You just need to emotional resolve to hold through market declines! 😉

Till next time, Financial Horse, signing out!

Enjoyed this article? Do consider supporting us and receiving additional exclusive content!

Like our Facebook Page for more great articles, or join the Facebook Group to continue the discussion!

Hi, why the S&P500 over an even more diversified global ETF like the popular IWDA or VWRD ETFs? Wouldn’t that give sufficient US exposure as well as mitigating risks from depreciating USD etc? I’m quite new to investing, so am genuinely curious! Thanks as always for your opinions and insights!

Hi, welcome to FH!

For this I wanted pure US exposure, so I thought the S&P500 would be the best. ETFs like the IWDA and VWRD have European/Japan exposure, which I didn’t really want… But yeah, they are absolutely viable alternatives if you are so inclined.

You have picked s&p500 etf. Would you purchase it in UK market instead for the tax benefit or would you still recommend buying the spy etf on sgx?

Yes, UK one is the most efficient from a tax perspective (VUSD). Go with the UK one if you plan to hold ultra long term.

Didn’t realise that there is a SPDR S&P 500 ETF (SPY) listed in SGX. Is this traded in SGX normal trading hours?

How could one buy into this ETF? Any different from buying the Nikko AM STI ETF or the STI ETF?

My apologies for not clarifying. The SPY is listed on the US exchange. You can also purchaser the VUSD listed on the London exchange, for more favourable withholding tax treatment.

same comments as above, why not the IWDA, instead of SPY?

SPY will also incur withholding tax, since it is US based?

Didn’t like the IWDA because of the European/Japanese exposure. But yeah… the VUSD is a great alternative to the SPY because of favourable witholding tax treatment (15% vs 30%).

Thanks for the analyses. Quick question on Netlink Trust – any thoughts on the sustainability of its dividend please?

Observed in its 3Q 2018 cash flow statement that for both the quarter and nine months, distributions seemed to exceed its net operating cash flow minus CAPEX. This seems to suggest that it’s dipping into existing cash balances to pay those dividends.

Yeah that’s a really good question, I’ve heard this concern raised a couple of times. Let’s take a closer look at the full year numbers once they’re out to understand what’s going on.

Yeah, thanks FH. Am curious about this aspect too. Let’s wait for Q4 results and management’s explanation.

Comparing price to book between CDL and CapitaLand is not a fair gauge. Reason being CapitaLand largely fair value their real estate asset at fair value (ie in the book value), while CDL investment properties and hotel assets are held at cost less accumulated depreciation.

That is a great point. My mistake, and thanks for the correction. Appreciated.

given the 2 titans fighting in the trade war, would you suggest an alternative ETF to SPY? Something China exposed?

DBS cash flow statements are pretty bad especially for the last two years. Does it not worry you about the future of the bank?

Hi there! Able to share which part of the cash flow concerns you? I think ultimately its a risk rewards kind of analysis. I like having exposure to DBS as part of my portfolio, especially since it serves as a diversifier to some of my other counters.

Hi FH, instead of SPY which is listed on the US stock exchange. Why not get the Vanguard S&P 500 index ETF (xhkg) listed in the Hong Kong exchange instead because Hong Kong has 0% withholding tax right?

Hi! There will be withholding tax from US to Hong Kong, so it’s the same. You can use Irish domiciled funds to reduce withholding tax to 15%. 🙂

You can check out the article here: https://financialhorse.com/withholding-tax/