As you would have noticed of late, a lot of analysts are no longer expecting a US recession in 2023/2024.

As US markets continue their march upwards, most bears have capitulated and are talking about the start of a new bull market.

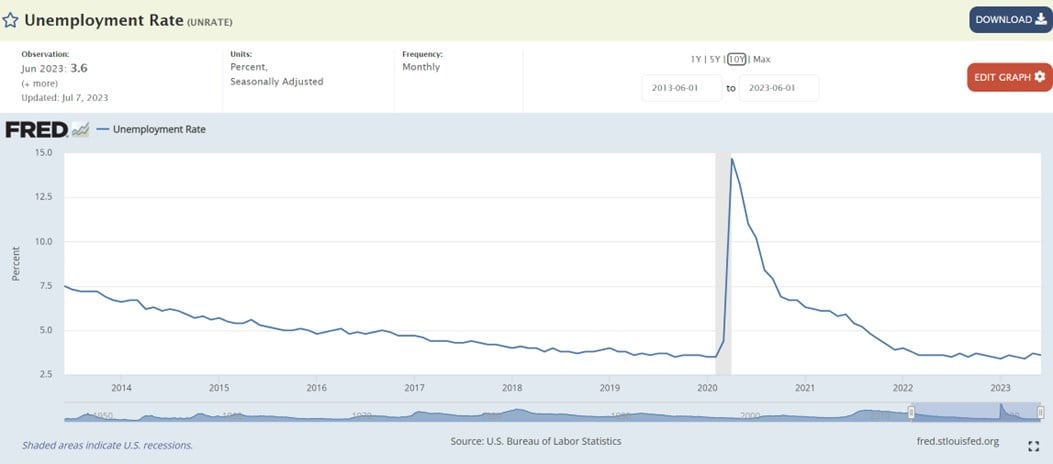

Today’s consensus seems to be that the Feds will pull off what many thought impossible, bring inflation down without a rise in unemployment (or recession).

So I wanted to spend some time to discuss this, and analyse whether there is any truth to it.

This is a modified version of the original article which first appeared on Patreon. If you find this useful, do sign up as a Patreon for more regular macro content like this.

Why is the US economy so strong?

First off – why is the economy so strong?

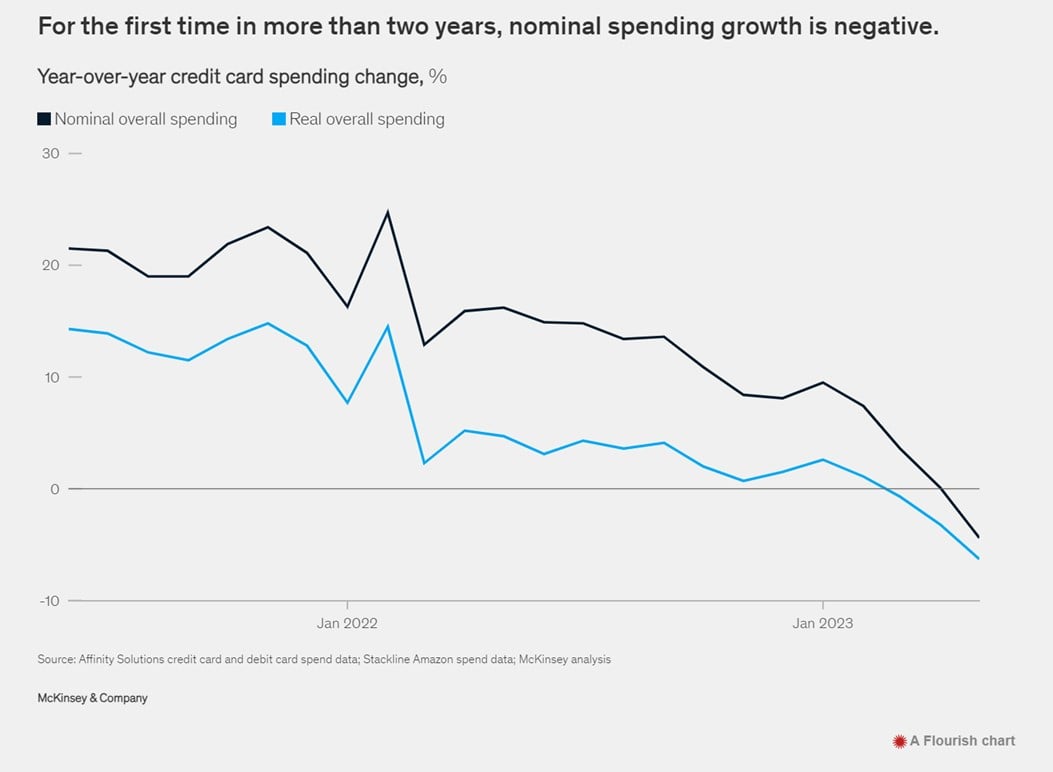

Very simply – because consumer spending is holding up well.

In previous rate hike cycles, once interest rates went up, consumer spending usually went down.

The way this then plays out is:

- Consumer spending going down means lower corporate earnings

- When corporate earnings goes down companies start to retrench

- The weak labour market affects consumer sentiment and causes them to cut spending even further

And so on in a vicious cycle.

The difference this cycle that seems to have caught everyone off guard.

Is that even though interest rates went up, consumer spending did not go down significantly.

Look at the chart of nominal spending below, and you’ll find that until the last 1 or 2 months, consumer spending has actually been holding up very well.

Why exactly the consumer is so willing to spend despite higher interest rates is not so clear, but here are a couple of plausible reasons:

- Consumers still have a lot of COVID era savings

- They locked in mortgage rates at low rates (not vulnerable to rising interest rates)

- Income growth remains high

- After COVID, consumers are eager to spend again

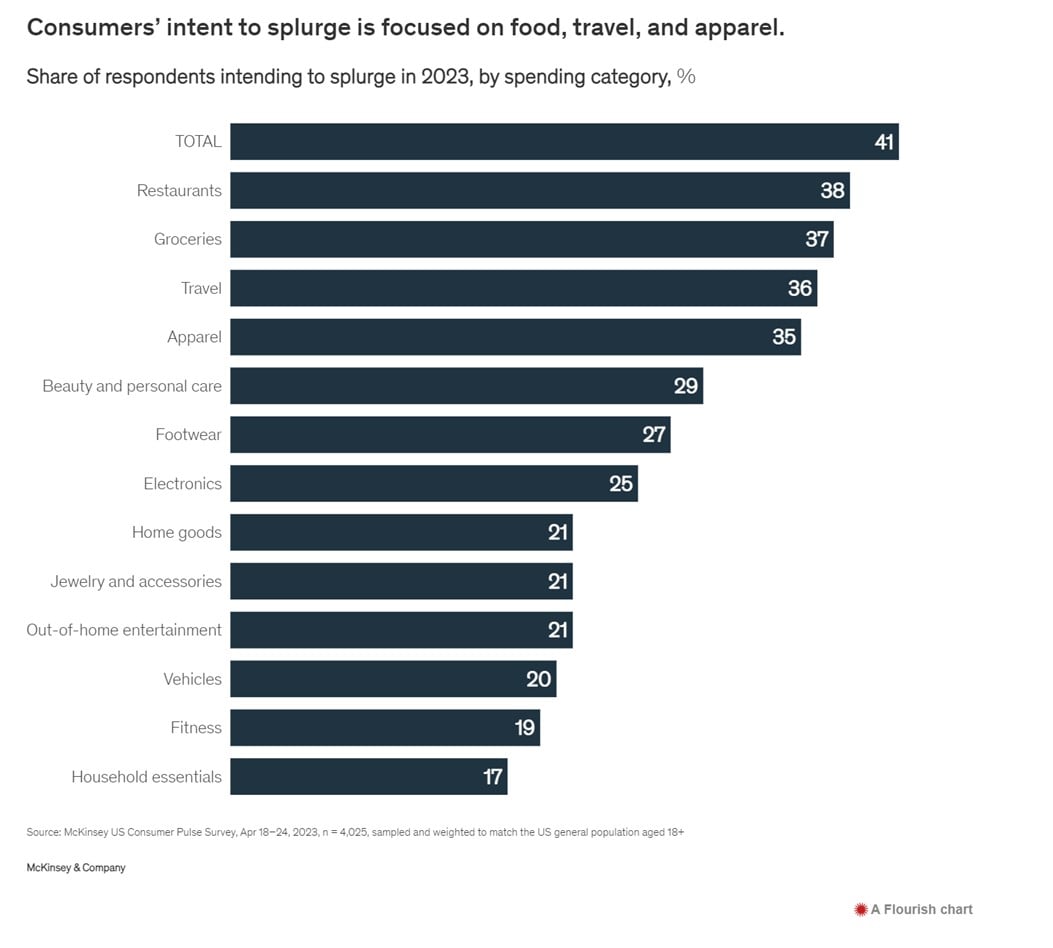

The breakdown on retail spending (in the US, but similar trends in Singapore) supports this last reason.

Namely – that the top 4 areas consumers are keen to spend on are:

- F&B

- Travel

- Groceries

- Apparel

Save for Groceries, it is the exact opposite of what consumers were spending on in COVID.

Think Singaporeans with concert tickets and F&B and holidays to Japan, and you start to get an idea of why consumers are so keen to spend to make up for lost COVID experiences.

What happens next?

This places the Feds in a conundrum.

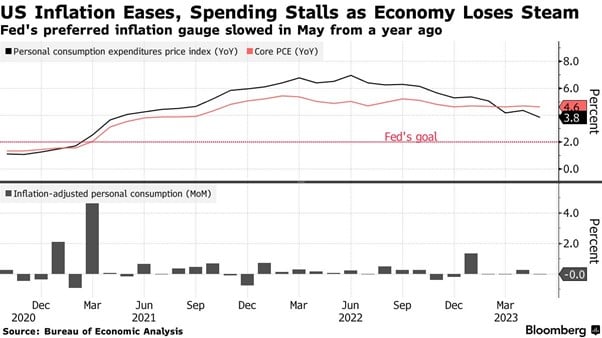

Yes, no doubt that inflation is coming down.

But core inflation (excluding food and energy) remains at 4.6% – way above the Fed’s target of 2.0%.

A big part of this is driven by services inflation, which is exactly what consumers are keen to spend on – F&B, travel etc.

And the biggest part of services inflation is high manpower costs, which is itself driven by a tight labour market.

Hence you start to see the vicious feedback loop here:

- Services inflation is high because of high manpower costs, due to tight labour market

- Tight labour market drives wage growth

- Wage growth drives higher consumer spending, as consumers have higher income

This level of consumer spending is actually well supported by wage growth.

Think about a case where your annual spending rises 5%.

But your employer gives you an 8% salary increase.

That 5% spending increase just looks perfectly sustainable now, because it’s not fuelled by debt but by a rise in income.

Which for the Feds trying to bring core inflation down to 2.0%, starts to look a bit worrying.

Because it doesn’t look like current level of monetary policy will be sufficient to bring inflation down to the 2% target.

What do we need for inflation to come down to the Fed target?

Let’s flip this around.

Let’s assume the Feds are serious about bringing core inflation down to 2.0%.

What do they need to do?

They probably need to achieve some combination of the following:

- Real interest rates to go up (inflation adjusted)

- Consumer spending to weaken

- Unemployment to go up

How do they achieve that?

2 ways:

- Hike interest rates even higher than what the market is expecting

- Keep interest rates at current levels longer than what the market is expecting

Either you play around with how high you go, or you play around with how long you stay here.

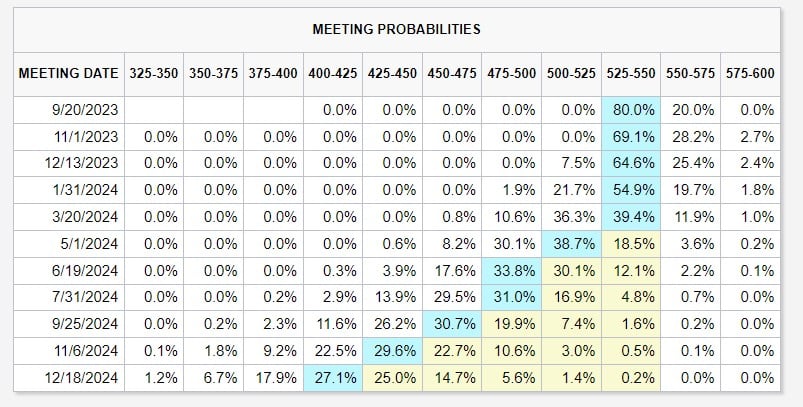

What is market pricing on interest rates?

Current market pricing on interest rates is basically pricing in a soft landing.

Market prices in:

- No more interest rate hikes in 2023

- 4 – 5 interest rate cuts by end 2024 (starting in Q2 2024)

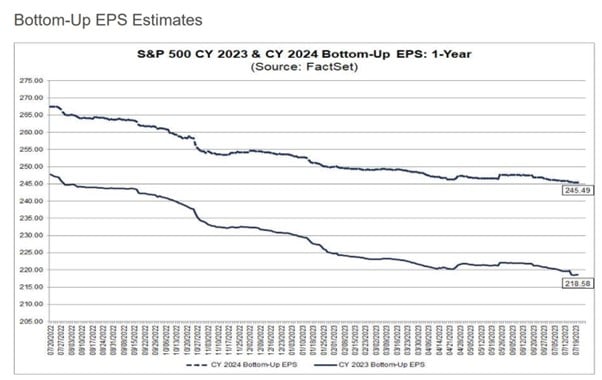

At the same time – expectations are for a 12% increase in corporate earnings in 2024 (vs 2023).

To put it simply – market thinks we get 4 or 5 interest rate cuts in 2024, with 12% earnings growth.

Is this realistic?

I’m not sure how realistic this is.

We discussed above how the current levels of consumer spending are sustainable.

Which means that based on current level of tightening, this may be insufficient to break inflation.

Which means that to see 4 – 5 interest rate cuts in 2024, you probably need to see rapidly weakening economic growth, that force the Fed’s hand (to cut rates).

And if economic growth is weakening, I’m not sure you’re going to see 12% earnings growth for stocks.

The way I see it – either the bond market is right, or the stock market is right.

Either we see 5 interest rate cuts, or we see 12% earnings growth.

I’m not sure we will see both happen.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

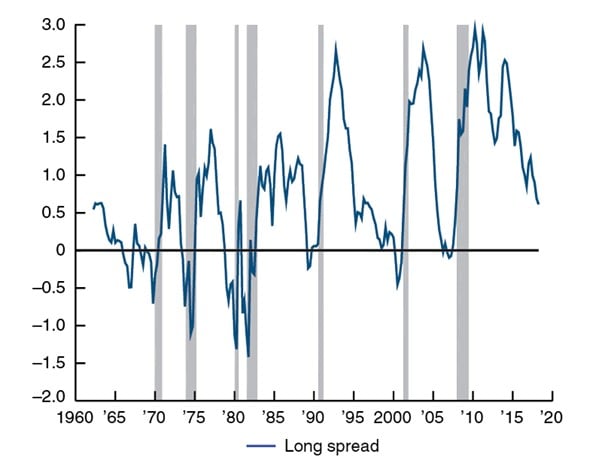

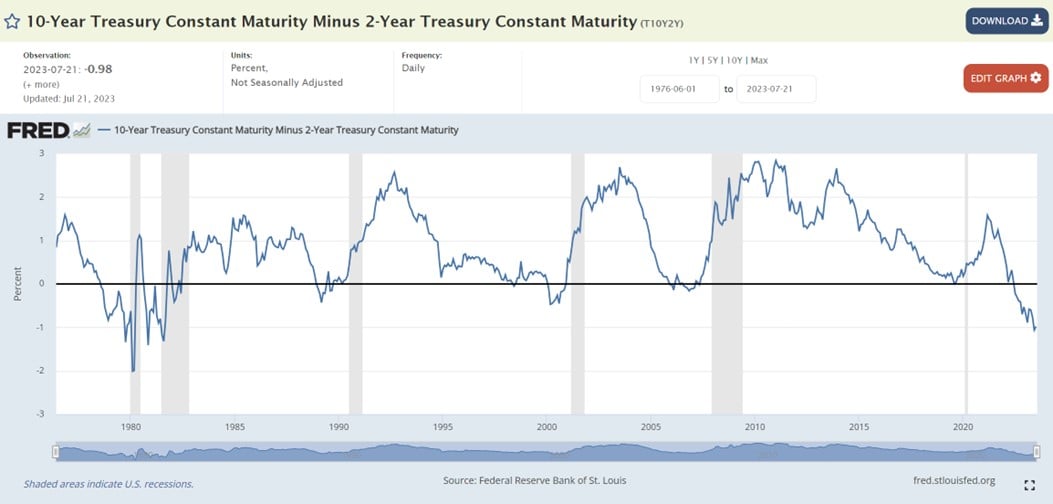

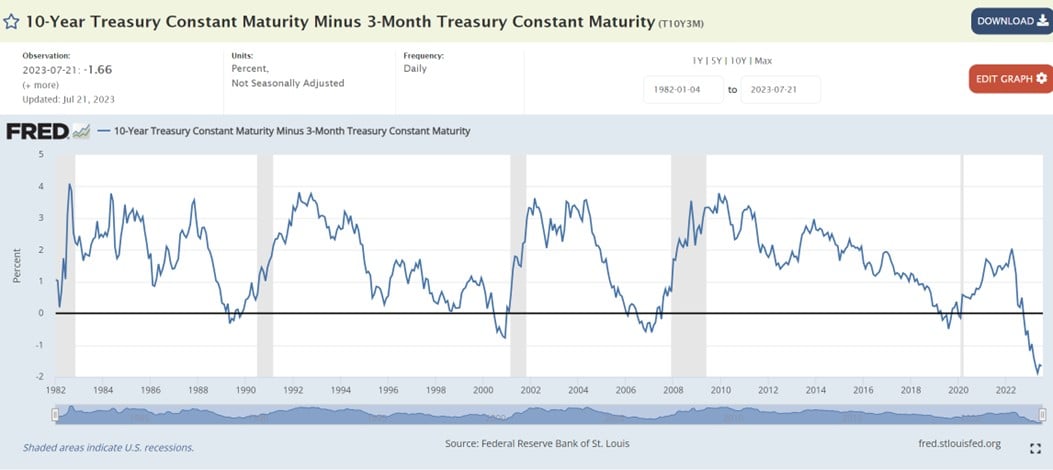

Past cycles – recession hits about 6 – 12 months after the steepening

I also want to point out that in previous economic cycles, the yield curve will invert prior to the recession.

But timing wise, the recession only hits about 6 – 12 months after the yield curve starts to steepen:

Here’s where we are today on the 2-10s and 3-10s yield curve.

We are deeply inverted on both yield curves – the most inverted since 1980.

And more importantly – the curve hasn’t even started to steepen yet.

Or in plain English – The real risk to the economy only comes when the yield curve starts to steepen, which hasn’t even happened yet.

We are not out of the woods yet…

I suppose to sum up what I am trying to say.

Is that I know all the commentators are declaring victory on inflation and talking about a soft landing.

But in my view, it’s a bit premature to make this call.

Based on latest data it looks like the slowdown will hit around 4Q2023 – 1Q2024.

We’re not even there yet, so to say the recession is averted just looks a bit premature to me.

Just to be clear… I am not calling for a mega recession

I just want to put it out there that I am not calling for a big recession.

As of today – it’s not clear to me whether we get a soft landing, a mild recession, or a big depression.

The big factor to me still goes back to what Powell is going to do when the time comes.

When core inflation goes down to the 3-4% range.

Does he declare victory and cut interest rates?

Or does he keep interest rates at current levels until core inflation comes down to 2%?

What he does there, has massive implications on how markets play out.

What is priced into the market today?

Now the reason why a new bull market is such a great buy is because valuations are dirt cheap.

And also because after the economy bottoms out, monetary and fiscal policy switches to being stimulative.

So you have a (1) cheap starting valuations, and (2) supportive policy.

The problem today, is that it’s hard to say that you have either of the above.

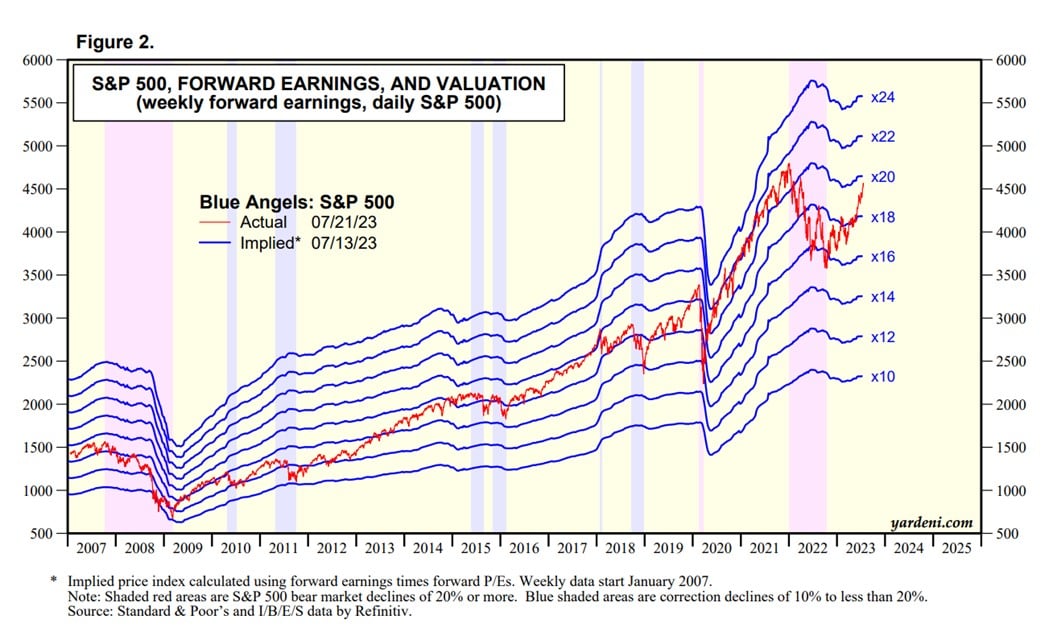

Stock valuations are not cheap

Here’s the S&P500 valuations, at 20x forward earnings.

20x forward earnings with the Fed Funds at 5.5%?

Sure, maybe it goes higher short term, but at these levels you’re pricing in quite an optimistic future.

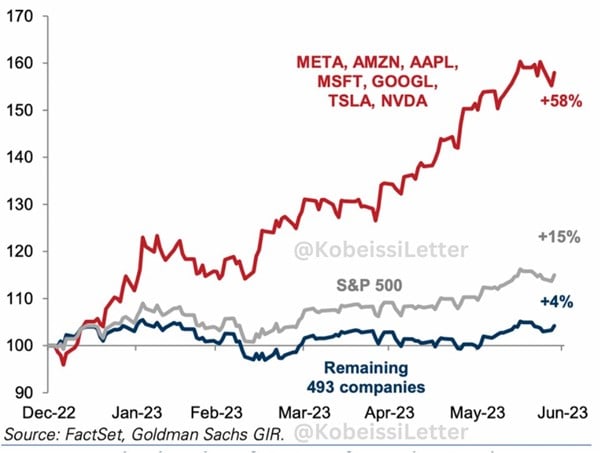

Interestingly if you look under the surface, you’ll find that much of the returns have come from the FAANG/AI.

Take out those 7 stocks, and the S&P500 only returned 4% year to date.

Which does suggest opportunities for savvy stock pickers.

I’ve been buying stocks / REITs that I see as attractively priced, and I will continue to do so going forward. Full list on Patreon if you’re keen.

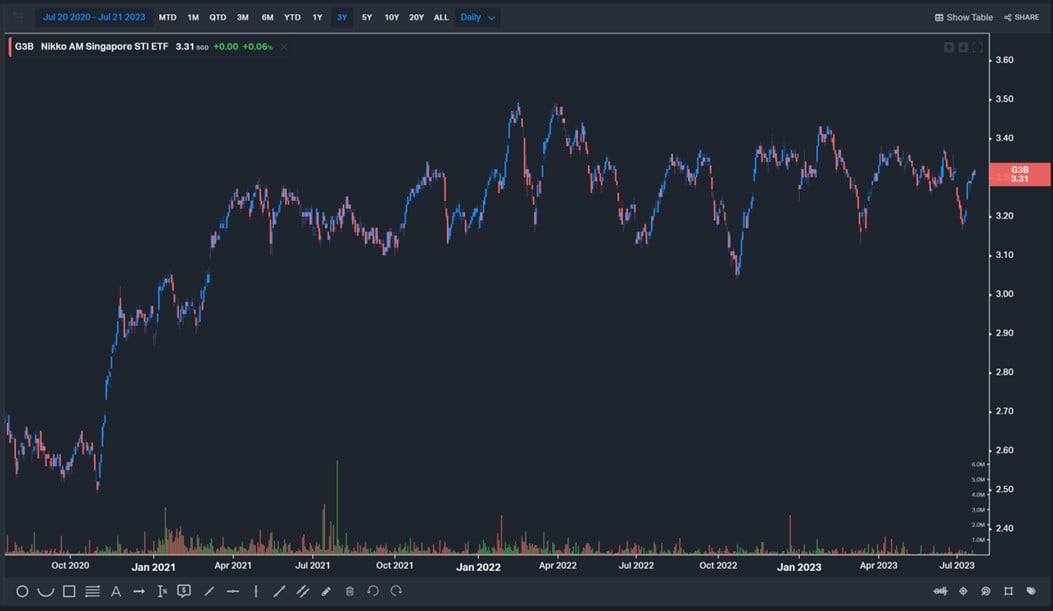

Here’s Singapore, strip out the dividend and share prices have gone nowhere since 2021:

(here’s the dividend adjusted chart)

Policy is supportive?

Policy wise we discussed above.

For policy to turn supportive you basically need to have the Feds to start cutting, or governments to start big stimulus.

What the Feds do in the next 12 – 24 months, really anyone’s guess.

Will governments pump big stimulus in an election year?

Well yeah – definitely possible.

I wouldn’t rule out fiscal stimulus in an election year.

How to position as an investor?

So let’s sum up.

How to position as an investor.

Based on the discussion above, it’s hard to say you want to go all-in at this point in time.

Valuations are not cheap, and if the Feds decide to get serious on 2% inflation you could be looking at pretty bad outcomes.

But it’s also not all doom and gloom.

If the Feds keep us at current level of rates, and government stimulus continues to flow, you could see a soft landing for the economy – where economic growth stabilises at current levels, and inflation stabilises at the 3-4% range.

At this point in time, both scenarios look plausible, it just goes back to what policy makers choose to do in an election year.

What is the right asset allocation?

As I always say, it goes back to asset allocation.

I’ve shared with Patreons the current level of equity exposure I am running.

It’s a level of equity exposure that allows me meaningful upside if the market continues to go up.

And it’s a level of cash that allows me to sleep at night, and to buy in if we get a meaningful decline.

After all when you’re getting close to 4% yield on cash.

And 5-6% on low risk bonds.

The need to go out the risk curve and take on equity risk is the lowest it has been since 2008.

Ever since 2008 when interest rates were stuck at zero you pretty much were forced to go out there and take risk.

A REIT yielding 6% is almost 5% yield higher than what you’re getting on cash the past decade.

Today, the same REIT yielding 6% is only 2% yield higher than what you’re getting on cash.

And the longer interest rates stay high, the more uncertain the impact on the global economy.

Ultimately though, asset allocation has to go back to risk appetite.

If you’re a young investor with a rock solid income stream for the next 30 years, yeah sure a higher risk allocation makes sense.

If you’re a retiree with minimal income, then the answer might be very different.

This is a modified version of the original article which first appeared on Patreon. If you find this useful, do sign up as a Patreon for more regular macro content like this.

This article was written on 28 July 2023 and will not be updated going forward. For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do sign up as a Patreon.

WeBull Account – Get up to USD 800 worth of shares (expires 31 July)

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 500 free fractional shares.

You just need to:

- Sign up here and fund $300 SGD

- Execute 1 buy trade within 30 days of funding

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Best investment books to improve as an investor in 2023?

Check out my personal recommendations for a reading list here.

FH,

As usual , great analysis of the market macro and scenarios playing out . Always enjoyed your analysis and thank you for your time and effort and sharing ! ????????

No worries – hope it helps! 🙂

Hi FH, really appreciate your videos. Can you do one on China & its Tech pls?

Understand the Hang Seng Tech Index is up 20pct from the lows?

Think a lot of your readers have positions in China & would love to hear your thoughts.

Thank you!

I did a piece on China recently actually: https://financialhorse.com/china-banks-icbc-plunge-to-9-1-dividend-yield-why-i-am-buying/

It’s on the China banks, but a lot of the macro analysis is applicable to tech as well.

Key question is whether you think this is the policy bottom. And what is the role of China tech in China going forward. And dont forget geopolitical risk as well.

With all that in mind – what is the right valuation for China tech? Especially given how bombed out the sentiment on China is right now.

That said I get what you mean. Will see if I can do a piece on China, but it might be a Patreon post first.

Yep, theres not much to buy. Fortunately we can just get paid to hold spare cash, no pressure to buy. After more than a decade of zero rates, finally There Is An Alternative.

Yup, opportunity cost of cash is the lowest it’s been for a decade and a half.

What recession?

I said a few years ago there won’t be a recession.

Times have changed, paradigm has shifted.

Fair enough – let’s see!

I don’t believe we’re out of the woods yet; feels like the market is overly optimistic & overly euphoric.

Generally inclined to agree with this. The real risk to the economy is in the end 2023 / early 2024 period.