I received a very interesting question this week:

Hi FH, can you share some perspectives why the 3 local bank share price have been falling and what are the signals we should look out for as a good time to buy?

Very interesting – and I’ve had quite a bit of thoughts on the local banks that I wanted to share for a while now.

There’s actually 3 parts to the reader’s question:

- Are DBS, OCBC, UOB bank stock prices dropping?

- Why are they dropping?

- When will I buy bank stocks in 2024 – and what signals will I look out for?

Let’s discuss each.

Are DBS, OCBC, UOB prices dropping?

First off – are the bank stocks even dropping?

I extracted the chart of DBS below.

Yes, price at 31.4 has come down 15% from cycle highs of 37 (hit in Feb 2022).

But it’s also hard to say DBS is in a clear downtrend.

While the stock is making lower highs, it hasn’t made a lower low just yet.

It looks more rangebound from $31 – $34.

Likewise with UOB.

Yes, share price at $27.4 has come down 17% from cycle highs of $33 (also hit in Feb 2022).

But it also hasn’t broken below new lows yet.

While OCBC is the outlier – on an uptrend.

I suppose this is because OCBC’s post-COVID recovery hasn’t been as strong as DBS or UOB, so it is merely catching up to its competitors here.

So no clear downtrend for the bank stocks? Are DBS, UOB, OCBC bank shares rangebound?

Looking at the charts above, it’s hard to say that there is a clear downtrend for the Singapore bank stocks.

But no doubt share price has come down a fair bit the past few weeks.

With the exception of OCBC – both UOB and DBS are down 15%ish from their Feb 2022 highs.

And share prices have been rangebound for the past year and a half.

This is despite the fact that the profits for the 3 banks remains near record highs, with non-performing loans near cycle lows.

|

|

OCBC |

DBS |

UOB |

|

Quarterly revenue growth (yoy) |

27.7% |

37.1% |

23.8% |

|

Return on Equity (ttm) |

12.8% |

17.0% |

12.4% |

|

Non-Performing Loans |

1.1% |

1.1% |

1.6% |

Why is this the case?

And what will happen next?

Bank stocks (DBS, UOB, OCBC) pricing in risks over interest rate cuts and slowing economy

If you ask me, it comes down to 2 key concerns:

- Interest Rate cuts going forward

- Slowing Economy

Interest Rate cuts going forward

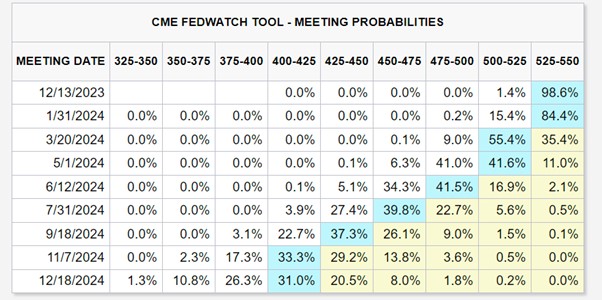

A lot of investors are buying REITs on the expectations of interest rate cuts in 2024.

The market is pricing in interest rate cuts as early as March 2024.

With a total of 5 interest rates – totalling 1.25% in 2024.

Whether this is right or wrong, and whether we will see more or less interest rate cuts than what is priced in is a whole debate in itself.

But if we assume that interest rates are going down in 2024.

This might not be good news for bank stocks.

The core business for the banks is lending (70% of their business).

Lower interest rates means lending at lower rates means lower revenues.

But… 2 key rebuttals to this

As you would have realised by now, things are never that straightforward.

There are 2 key rebuttals to this simplistic analysis of lower interest rates = bad for banks.

They are:

- If rates go down, banks’ funding costs will go down too

- If rates go down, borrowers may borrow more money = loan growth

If rates go down, banks’ funding costs will go down too

The argument here – is that yes interest rates are going down in 2024.

But while DBS / UOB / OCBC will lend out at lower rates.

They may also pay a lower rate to depositors.

Think lower fixed deposit rates, lower rates on UOB One / DBS Multiplier / OCBC 360.

If rates go down, borrowers may borrow more money = loan growth

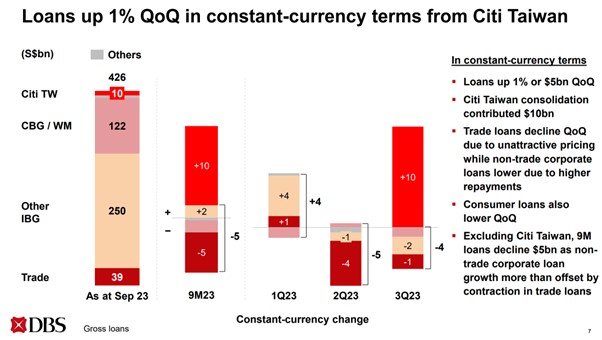

The higher rates and slower economic growth has impacted loan book growth.

Here’s DBS – showing only 1% quarter on quarter growth in its loan book.

So the argument here – is that if interest rates go down while the economy remains resilient.

This may spark demand from individuals or companies to borrow money to buy houses or to invest in new businesses.

So even though headline interest margin may drop, profitability may stay strong due to loan growth.

Both are plausible – key question mark for bank stocks is what happens to the economy

Both arguments are valid.

Which means that to understand how bank stocks trade in the next 12 months.

We need to understand what happens to the economy – does it (1) go into a sharp recession forcing rapid interest rate cuts, or (b) avoid a recession (but growth stays slow), resulting in minimal Fed rate cuts.

In previous macro outlooks I shared 2 possible futures:

- Scenario 1 – Hard landing (economic recession, Fed rate cuts)

- Scenario 2 – Slow Grind Down (economy avoids a deep contraction, minimal Fed rate cuts)

At this point in time, it’s really not so clear to me which we see.

Policy makers reaction in a US election year will have a material impact on which outcome we see.

A Fed that cuts interest rates pre-emptively, vs a Fed that keeps interest rates at 5.5% even as growth slows, will produce 2 very different outcomes.

So if you don’t know which outcome we will see, how do we decide whether to invest?

In a scenario like that – we need to understand risk-reward.

How much do you make when you are right, vs how much you lose when you are wrong?

How much do you make on DBS if you are right? – Scenario 2 (Slow Grind Down)

Back to risk-reward.

As a bank investor today, your ideal outcome is Scenario 2 (Slow Grind Down).

You avoid a recession, minimal Fed rate cuts in 2024.

What’s the upside in this scenario?

Let’s use DBS as an example.

In this scenario economic growth probably stays muted, so DBS probably stays within their current trading ranges.

Let’s say 5% capital gains to 33-ish, plus the 6% dividend.

About 11%+ upside (for obvious reasons these are ballpark figures).

How much do you make when you are wrong? – Scenario 1 (Hard Landing)

Let’s say you are wrong, and Scenario 1 (Hard Landing) materialises.

The economy goes into a recession, interest rates are cut aggressively.

How much will the bank stocks drop by?

Well it really depends on how deep the recession is – do we get a mild recession like 2000 or a deep recession like 2008?

Let’s be optimistic and assume a mild recession.

Look at the banks’ loan exposure below.

|

Loan Book |

OCBC |

DBS |

UOB |

|

Singapore |

41% |

46% |

48% |

|

Greater China |

25% |

29% |

17% |

|

South East Asia |

14% |

8% |

21% |

|

Rest of World |

20% |

17% |

14% |

Even if Singapore’s economy remains resilient, each bank has almost 50%+ exposure to South East Asia, China and the Rest of the world which will not be immune in a global economic slowdown.

Assuming a mild recession, you’ll probably see around 30% peak to trough declines for the bank stocks.

That implies about $24 for DBS (30% drop from cycle high of $37).

Let’s cross check that against another valuation method.

DBS’s book value today is $21.8.

20 year average book value is 1.3x, so let’s say in a mild recession it goes to 1 standard deviation below (1.1x) – which is about $24.

So assuming a mild recession, DBS’s share price goes to maybe $25 – $25, or a 20% downside from here.

Of course, in a deep recession all bets are off, but let’s just be optimistic here.

20% downside, but in a mild recession the dividend probably gets kept (perhaps with mild dividend cuts).

Let’s assume a 4% dividend yield in this scenario.

Means you’re looking at 16%ish downside if you’re wrong and a hard landing materialises (of course more if it’s bigger than a mild recession).

Is this attractive risk-reward?

Putting it altogether.

You make 11% if you are right and get a Scenario 2 (Slow Grind Down).

You lose 16% if you are wrong and get a Scenario 1 (Hard Landing).

And if s*** hits the fan and you get anything bigger than a mild recession, then you stand to lose much more.

Even assuming simplistically a 50-50 chance of each scenario – those numbers aren’t exactly screaming must buy.

Don’t forget T-Bills are paying 3.74% risk free, so the gains above need to be measured in that context.

Full disclosure that I have taken profit in my bank stocks (so I have no skin in the game here)

Now full disclosure that I have taken profit in my bank stocks.

I have sold all my bank stocks earlier in 2022/2023 (all portfolio updates are shared regularly on FH Premium).

I can’t recall the exact sell price I sold them at, but probably about 5 – 10% higher than current levels.

So you may argue that I’m slightly biased here as I have no skin in the game.

But for what it’s worth – I’m actually a lot more constructive on the banks today than when prices were 10% higher.

If price comes down, risk-reward goes up it’s as simple as that.

When would I buy DBS / OCBC / UOB bank stocks? What signals would I look out for?

To answer the question specifically.

Let’s leave aside technical analysis for a moment.

From a fundamental perspective – I think what would cause me to change my mind and buy the banks in a big way is one of the following:

- Price of DBS / OCBC / UOB comes down further

- Macro picture clears up

Price of DBS / OCBC / UOB comes down further

In a more volatile investing climate like today where you don’t have the tailwinds of QE and zero interest rates to bail you out.

Buying at the right price becomes a lot more crucial.

And the way I see it – investing in bank stocks is not rocket science.

This is the 25 year chart of DBS Price/Book below.

Generally speaking you want to buy DBS in the lower bands, and sell at the higher bands.

That’s how you maximise the risk-reward.

Where we are today – the banks are no longer that overvalued given their sell-off.

But they’re still not in the range where I would back up the truck just yet.

Macro picture clears up

I wanted to add that at this point in the cycle – a mild recession may not be the worst thing in the world.

A mild recession will cut excess demand for labour, allow the Fed to cut interest rates, and allow for the start of a new business cycle.

Whereas if there isn’t a recession and the economy stays slow (say -1 – 1% levels of real growth) – the Feds may not be able to cut interest rates aggressively, and the high interest rates just weigh on asset prices across the board.

The way I see it:

- If we get a recession and bank stock prices drop, I will buy

- If we don’t get a recession and bank stock prices stay rangebound, I want to have more clarity on how the policy makers are going to react

A Fed determined to hold interest rates high into a slowing economy, vs a Fed that cuts pre-emptively to avoid an economic slowdown in an election year – those are going to produce 2 very different outcomes.

So that’s what I would be looking out for from a fundamental perspective.

Closing Thoughts: Everyone’s a long term investor until prices go down

I am reminded of an old saying in markets.

“Everyone’s a long term investor until prices start going down.”

Now just to be clear – I am not saying DBS / OCBC / UOB stock prices are going down.

Nothing could be further from it.

I am saying that I don’t know where DBS / OCBC / UOB stock prices goes in the next 12 months.

But I see 2 plausible scenarios that may play out for the economy.

In one scenario I make a small bit of money on the bank stocks, in the other scenario I lose a small bit of money.

That’s an okay investment, but not necessarily amazing.

Whereas there are other asset classes like REITs or tech or bonds where if I am right on the path for interest rates, I stand to make quite a bit of money.

That’s what I would prefer to go for in this climate – full list of names that I like is shared on FH Premium. You can also see my full portfolio breakdown on FH Premium.

So that’s how I am positioning, but frankly there’s no right or wrong here and it goes back to timeframe.

If you’re a true long term investor and you’re buying DBS / OCBC / UOB to pass to your children 4 decades later – frankly all this is just noise for you.

This article was written on 8 Dec 2023 and will not be updated going forward.

For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do subscribe for FH Premium.

– Get up to USD 5000 worth of shares (Best promo of 2023 – Now Extended)

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now (Best Promo of 2023)

You can get up to USD 5000 free shares.

You just need to:

- Fund any amount (get 5 free shares)

- Hold for 30 days (get 5 free shares)

OCBC Online Equities Account – Trade on 15 global exchanges, all via the OCBC Digital Banking App!

Did you know that can you trade shares on your OCBC Digital Banking App?

With an OCBC online equities account, you can buy stocks, local ETFs, REITs, bonds and more directly through your banking app.

Even better? Enjoy reduced commission rates of just 0.05% for buy trades on SG, US and HK market until 31 December 2023.

Everything on one app! Fuss-free funding, with access to 15 global exchanges

For SGD trades, you can fund and settle automatically via your OCBC account.

And for FX trades, you can settle using the foreign currency held in your OCBC Global Savings Account.

This means fuss-free trade settlement and minimising forex costs – saving you time and money.

Start trading with your OCBC Online Equities Account here!

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Investment Research Tools

I use Trading View for my research and charts. Get $15 off via the FH affiliate link.

I also use Koyfin for fundamental and macro research. Get a 10% discount via the FH affiliate link.

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Best investment books to improve as an investor in 2023?

Check out my personal recommendations for a reading list here.

basically, if bank stocks go down, the STI Index goes down.

Which means you dont buy anything in the stock market.

hehe.

Yes pretty much haha – so those who want the passive exposure still have to buy the banks.

I think what is important for the banks is not interest rates per se but rather NIM. Before rates shot up last year, they were near zero (even minus) so banks had little to no flexibility to adjust, both for their customers deposits as well as their borrowers. But the much higher rates currently prevailing permit them to time manage their reductions of rates on deposits and lendings to minimise erosions to their NIMs if rates drop as many are expecting..

My other point is, as you indicated, it is still uncertain that the FED will start cutting rates as the market is perceiving. My reason for saying so is because this time there may be other factors than the traditional ones to consider, eg if aversions to investing in US Treasuries deepen.

Finally, as I said in a comment to your earlier post on DBS, higher rates had negative affected DBS book values lower rates will provide a boost to DBS (and the other banks hold such securities) equating to higher prices for their holdings of treasuries that had taken some severe beatings over the last 2 years from the fallIng prices of treasuries.

I continue to be invested in DBS and OCBC, having both them much earlier. Eg the rights shares of DBS @$5.42ps is more than fully recovered thru dividends over the years! OCBC has long been my favourite bank share.

That’s a fair comment, don’t disagree with you.

It really goes back to timeframe.

Investors with a longer term timeframe, who do not want to time the cycle – any dip is just a buying opportunity.

Banks are cyclical stocks to me. I had profited from both AFC and GFC. About 300% profit excluding dividend on each occasion. Money in the pocket is more important to me. Till the next time,…. hehe.

Haha.. agreed! Don’t know when the next time will be, but let’s see. 😉