If you haven’t been following the interest rates space closely, you might have missed the huge moves in interest rates the past 2 months.

Just 2 months ago, the market was pricing in 4 rate cuts in 2023.

As of today, the market is pricing in up to 3 more interest rate hikes in 2023, taking us close to a peak of 6% on the Fed Funds rate.

We’re already starting to see this show up in higher yields for T-Bills and Singapore Savings Bonds.

And if this keeps up, we’ll start to see more shifts in global asset pricing.

So I wanted to take some time out to discuss this move and its impacts.

And venture some guesses as to what might happen with interest rates in the next few months.

You can see the impact on US interest rates – which spiked this week post ADP data

You can see this shown very clearly in US interest rates.

After a massive plunge in March after the collapse of Silicon Valley Bank.

US interest rates have roared back.

1 year interest rates have surpassed their March highs.

2 year interest rates are back to their March highs.

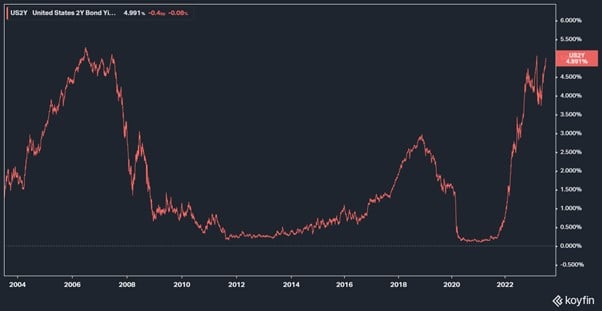

It’s even more stark when you pull up the 20 year chart.

US 2 Year Treasury yields are the highest they’ve ever been since 2007, and we all remember what happened after that.

Just 2 months ago, the markets were expecting 4 interest rate cuts.

Today, it’s pricing in rates potentially going to 6% (3 more hikes).

Crazy stuff.

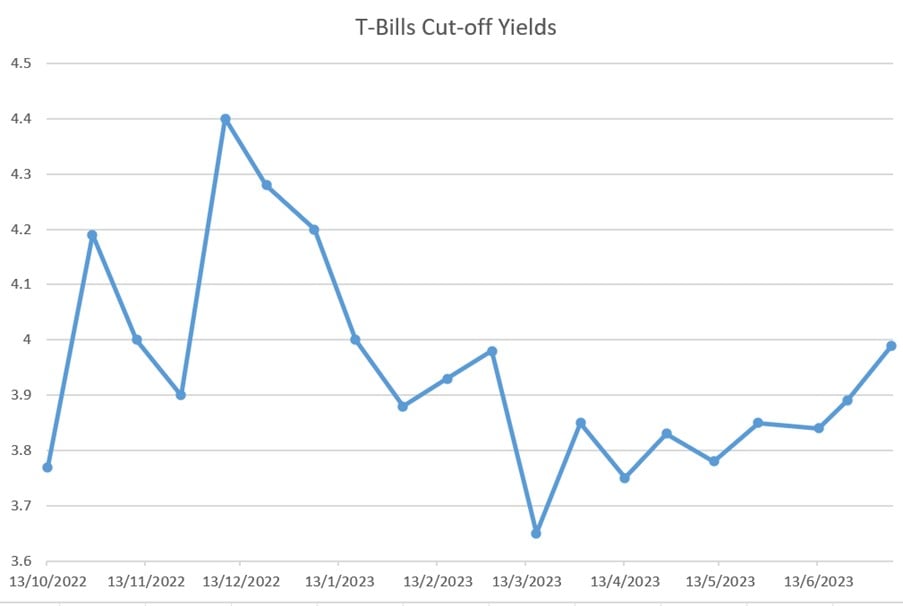

T-Bills yields have been going up too

Closer to home, T-Bills yields have been marching up too.

T-Bills yields closed at 3.99% in the latest auction, the highest yields since March:

Why are Interest Rates going up again?

Long story short – the US economy is proving stronger than expected.

Remember back in March 2023 after the failure of Silicon Valley Bank when everyone was expecting the US economy to crater and the Feds to cut rates rapidly after?

Yeah well… none of that has panned out so far.

Rather, the US economy is proving to be stubbornly resilient despite the Fed’s interest rate hikes.

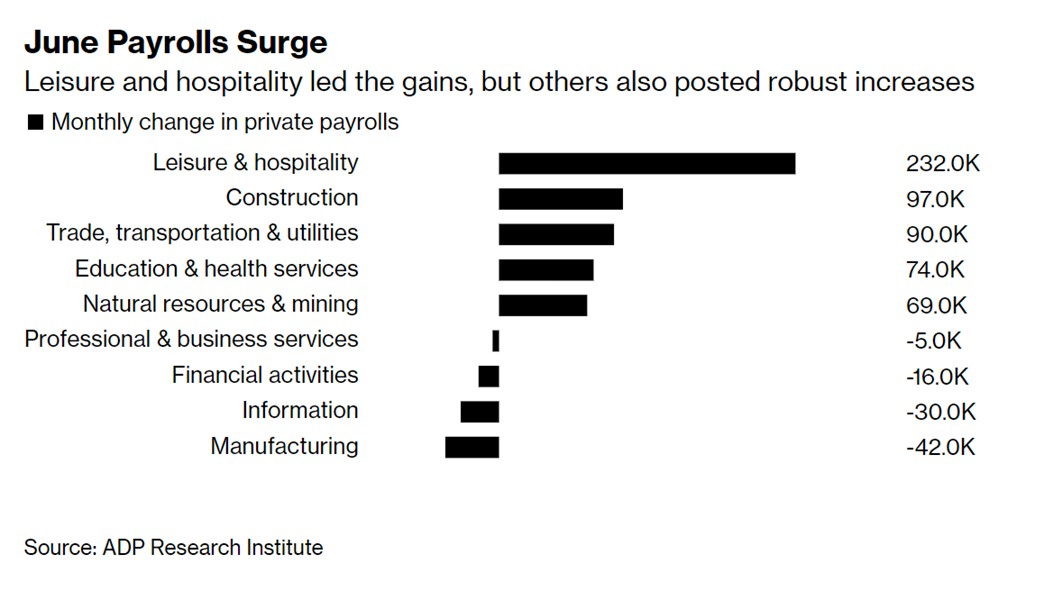

Latest ADP data out this week showed that the US economy added 500,000 new jobs last month, which indicates that the labour market is still very strong:

But… Feds want inflation to come down

The problem of course, is that the Feds are hiking interest rates to bring inflation down.

And the most sticky part of inflation right now is services inflation.

Think restaurant prices, car wash prices, massage prices etc.

With services, the biggest input cost is labour cost.

Which means that to break services inflation, you need to break the labour market (or at least loosen it up).

If the labour market is running red hot, that means services inflation doesn’t come down, which means more rate hikes from the Fed.

And hence short term interest rates go up:

My personal view on interest rates?

Remember how in early 2023 I wrote a bunch of articles saying how I think market pricing on interest rates is wrong?

The market was pricing in rapid interest rate cuts in 2023 – and to me that was just plain wrong looking at the strength of the US economy.

I said interest rates may need to go as high as 6%, and no cuts in 2023.

Well today, the market pricing on interest rates is starting to reflect exactly what I was saying in early 2023.

Interest Rates (Fed Funds) to go as high as 6% in 2023, with no interest rate cuts until mid 2024:

So as of today, I no longer think market pricing on interest rates is wrong anymore.

To me – I think market pricing is very close to the end game here.

But let’s not miss the forest for the trees.

If the Feds hike to close to 6%, and keep us there until mid 2024 – what do you think is going to happen to the global economy?

If I had told you 12 months ago that interest rates would be going to 6%, you would have laughed me out of the room and told me no way that happens without a financial crisis.

And yet today the market is pricing in interest rates possibly going to 6%, and everyone thinks we avoid a recession and we’re going to have a “soft landing”.

Forgive me if I’m slightly skeptical on this.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

So… soft landing or hard landing?

Just to be clear – I am not saying that my base case is for a deep recession.

Much will depend on how the Feds react over the next 6 – 12 months.

But I can’t help but shake the feeling that the higher the Feds hike, and the longer the Feds keep us there – the worse the downturn will be when it comes.

Whatever the case, I’ve always said that the economic slowdown will hit in 2H 2023 – 1H2024.

In the next 6 – 12 months, we’re going to see the economic slowdown start to hit, and how the Feds respond to slowing growth.

What are the implications of this?

US treasury rates basically dictate interest rates for the whole world.

So the implications of the above, will ripple through the global economy.

Unlike in 2022, I think where we are today, it makes sense to start thinking about the reversal in interest rates.

This has huge implications for all asset classes, and I will try to unpack all the implications in future articles for Patreons.

But for today’s article I thought the dilemma was best illustrated via cash management options.

Specifically – should you hold cash in T-Bills or Singapore Savings Bonds.

Should you redeem Singapore Savings Bonds to buy T-Bills?

A question I’ve been getting a lot is whether to redeem Singapore Savings Bonds to buy T-Bills.

Or whether to park liquid cash in Singapore Savings Bonds or T-Bills.

Let me put it this way.

T-Bills carry refinancing risk.

Yes you’re getting 3.99% on a T-Bill today.

But what about 6 months later in Jan 2024?

Or later in June 2024?

Or Jan 2025?

Do you think interest rates will stay at these levels for the next 12 – 18 months, without major consequences for the global economy?

I mean just look at the 20 year chart of the US 2 Year yield below.

Do you think the next big move is up, down, or sideways?

Singapore Savings Bonds at 2.99% yield are a decent buy for long term investors

Whereas with a Singapore Savings Bond, you’re locking in interest rates for up to 10 years, and get to redeem the money any time if you’re wrong.

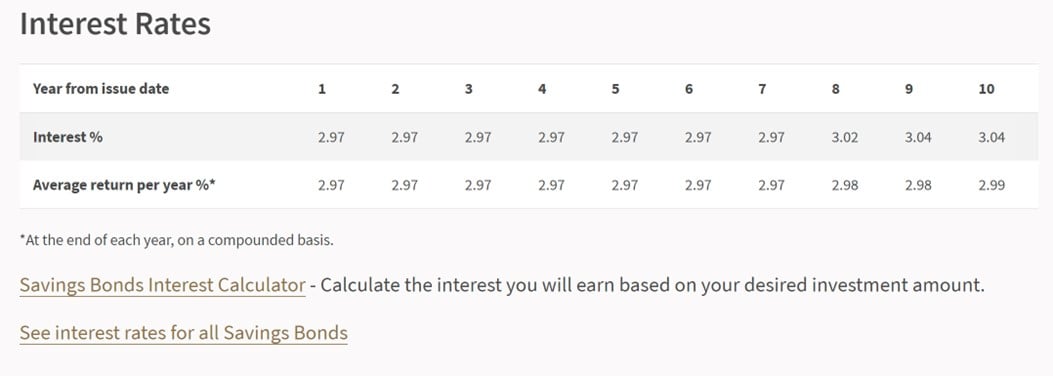

And the latest interest rates on the Singapore Savings Bonds are starting to creep up again.

You’re looking at 2.97% for the first 7 years, and 2.99% over 10 years.

Just to be clear I’m not saying that Singapore Savings Bonds are a must buy.

It all goes back to asset allocation, what is the right mix of each asset class.

All I’m saying is that these things let you lock in current interest rates for up to 10 years.

In the event that interest rates get cut, they could be a decent place to park cash.

Singapore Savings Bonds interest rates likely to go up further next month

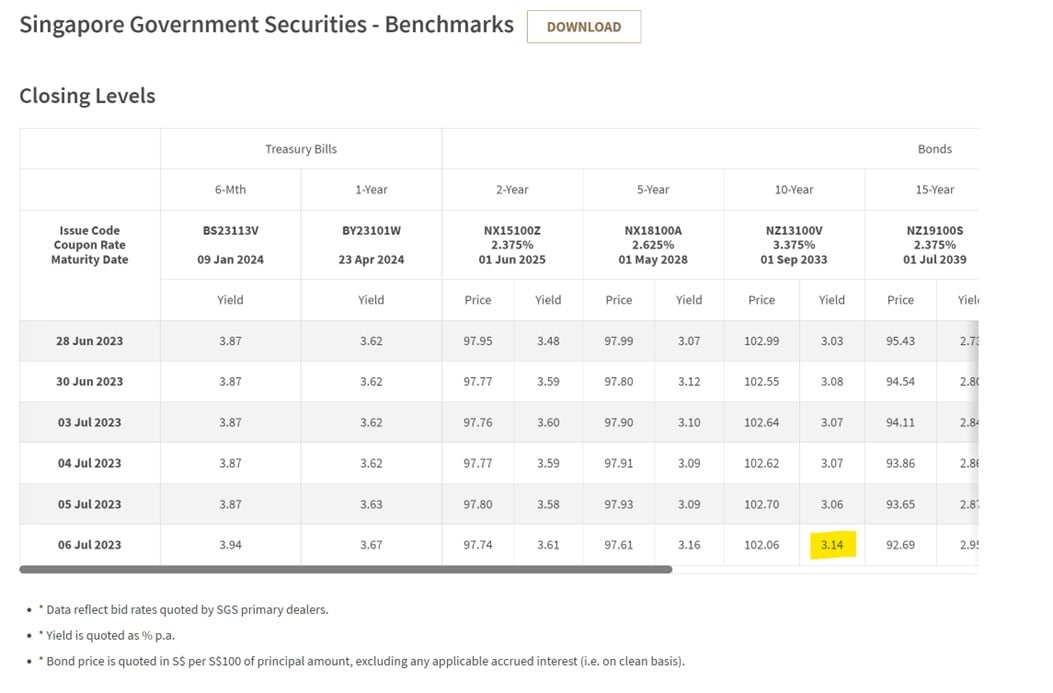

If you look at latest SGS pricing, you’ll find that Singapore Savings Bonds interest rates may even go up further next month.

10 year SGS now trades at 3.14%, which if this holds up means we’ll see short term interest rates on the Singapore Savings Bonds go to 3.1%.

Possibly even higher depending on how the rest of this month plays out.

Application Timeline for Singapore Savings Bonds

In any case, the application timeline for Singapore Savings Bonds below.

Deadline to apply (or redeem) the Singapore Savings Bonds is 9pm on 26 July 2023.

This article was written on 7 July 2023 and will not be updated going forward. For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do sign up as a Patreon.

WeBull Account – Get up to USD 800 worth of shares (expires 31 July)

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 500 free fractional shares.

You just need to:

- Sign up here and fund $300 SGD

- Execute 1 buy trade within 30 days of funding

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Best investment books to improve as an investor in 2023?

Check out my personal recommendations for a reading list here.

Hello FH, pls do enlighten us or any free articles to refer as how to capture US yields at this rate for long and short term? Also do you think it’s good to lock US yields with SGD hdge for potential return upto 4% for 10 yrs. I believe US treasuries to be more secure or at par with SG giv securities.

I have been getting some questions on this might see if I can write a piece. Long story short is that there are many ways to do it, but each has their own pros and cons, and the timing is crucial.

For average retail investors, one of the medium term managed solutions via Endowus or Syfe might be the best bet. But those only lock in yields for up to 4-5 years.

If you want something longer like a 10-20 year treasury, then you’re effectively taking on duration risk (risk that prices go down if yields go up), which makes it a very different kind of bet.

Thats what your title does to the latest casualty in the AU financial arena.

Philip Lowe to be replaced as RBA governor with cabinet meeting …

Michele Bullock becomes first woman to serve as RBA …[14/07/2023]

A case of conflicting interest or additional keynesian research suggestion?? Please share your views and thoughts

Not sure if I’m understanding your question right.

But the way I see it, central banks made a big mistake by keeping rates too low into the economic boom, and we’re now paying the price.

Depending on how bad the downturn gets (to tame inflation), I can easily see central banks and central bankers becoming the fall guy. Especially for savvy politicians who need someone to pin the blame on.

This show is not over.

Just like the minimum rental market has shot up as homeowners struggles to meet rising interest repayments and that’s a real observable fact in realtors listings and classifieds. The option is not available for the IRS, and as corporations struggle with the ‘I’ in EBIT and leave less for the ‘T’. This becomes a big problem. The most humane option would be to bring down the overall Interest Rates. And you did mention the scale of present gov debt in an earlier post would inhibit interest rate s from staying up for longer that is sustainable. Which would be good for the home investors l, share traders, but bad for the savers. And the cause of the inflation 3 years post pandemic is partly still linked to the supply chain shortages in some part of the world and increased logistics cost. A post graduate student friend taught me all this from a professors explanation of his.

Interesting points raised, appreciate the sharing.