So the next T-Bills auction is on 14 September (Thursday).

Now T-Bills yields have been very disappointing of late – closing at 3.70% the last auction.

And based on market conditions it doesn’t look like this will change materially for the current auction.

3 questions I wanted to discuss:

- What is the estimated yield on the next 6-month T-Bills auction?

- How does T-Bills compare against other alternatives – for CPF-OA / Cash buyers?

- Will I still buy T-Bills?

Next T-Bills auction is on 14 Sep (Thursday) – (BS23118S 6-Month T-bill)

First off – next 6 months T-Bills auction is on 14 Sep 2023 (Thursday).

If you’re applying in cash do apply by 9pm on 13 Sep 2023 (Wed)

For CPF-OA you’ll want to get it done by 12 Sep.

What is the estimated yield on the next 6-month T-Bills auction? (BS23118S 6-Month T-bill)

T-Bills trade at 3.71% on the open market

Latest 6 months T-Bills trade at 3.71% on the open market.

In fact the yields have actually gone down from late Aug, when they traded around 3.75%.

This is not a good sign for the T-Bills auction.

12-week MAS Bills trade flat at 4.01%

The institutional only 12-week MAS Bills are generally flat at 4.01%.

There was a period the past week where yields on MAS Bills went up a fair bit – but this did not translate into a higher T-Bills cut-off yield for the previous auction.

MAS Bills are a good indicator of the trend for T-Bills, so if you are submitting a competitive bid I do suggest taking a quick look at the latest MAS Bills pricing before you apply.

You know, just in case there are any big changes (can access it here).

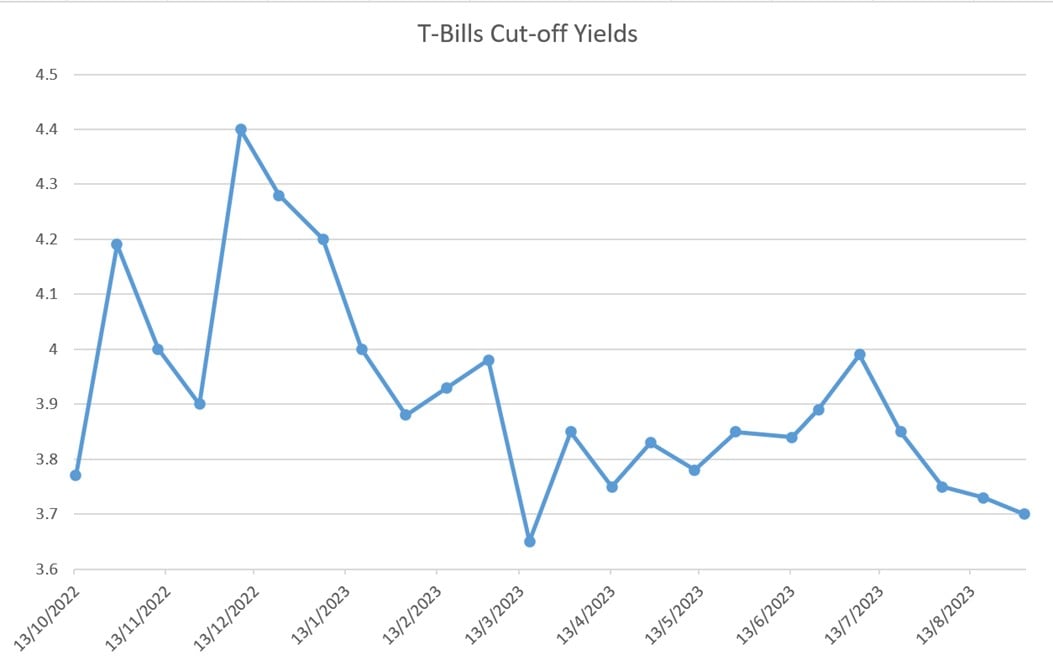

T-Bills yields on a downtrend due to China risk-off?

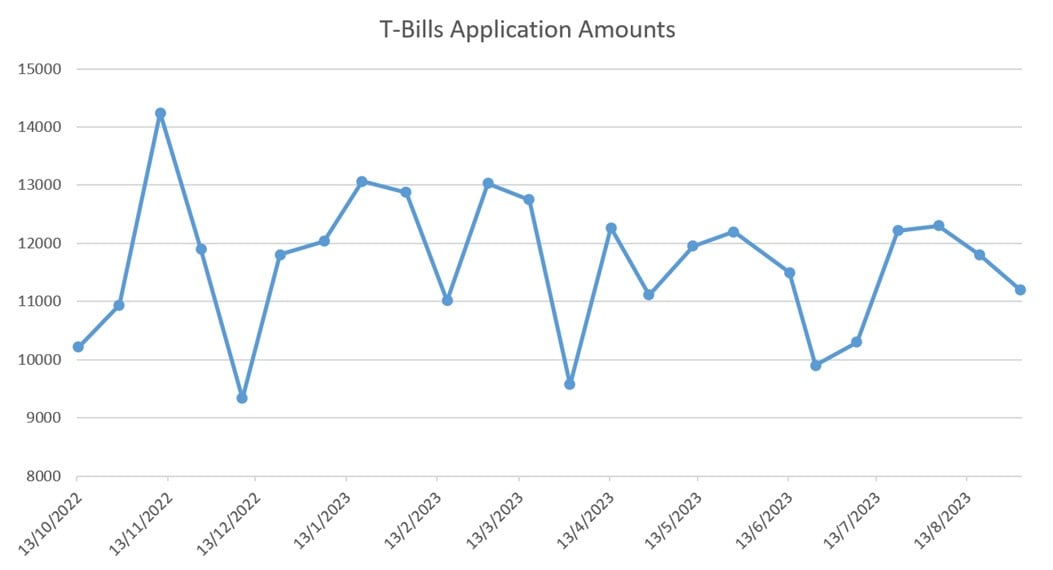

As you can see, T-Bills yields have been on a downtrend the past few auctions.

This is despite the fact that T-Bills application amounts have actually been going down, instead of up.

This is especially strange when you consider that US 1 year yields have been generally flat the past 2 months.

This shows that the market is not expecting any big changes in US interest rates over the next 12 months.

So why the big decline in Singapore T-Bills yields?

My suspicion, as shared previously, is that this is due to the influx of liquidity into SGD due to the China risk-off move.

But frankly this is just an educated guess – and if anyone has better explanations I am keen to hear them.

You’ll notice that the decline in T-Bills interest rates comes at a time when 10 year SGS yields are marching up relentlessly – as low as 2.65% earlier this year to 3.2% today.

This has actually increased the attractiveness of Singapore Savings Bonds vs T-Bills, which I will write more on below (and also been negative for REITs – because of rising long term interest rates).

Estimated yield of 3.65% – 3.75% on the 6-month T-Bills auction? (BS23118S 6-Month T-bill)

Looking at all of the factors above.

I don’t think we will see a big move in T-Bills yields from the previous auction.

Estimated yield of 3.65% – 3.75% on the next T-Bills auction would be my base case.

As always, I encourage investors to submit a competitive bid (just in case there is a freak result and yields drop a lot).

And submit as close to the deadline as you can, so you can take a look at where market pricing is at that time before deciding on your bid.

How does T-Bills compare against other alternatives – for both cash and CPF-OA buyers?

Are T-Bills still attractive vs other alternatives?

The analysis differs depending on whether you’re using CPF-OA or cash, so let’s discuss each.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great charts & insights on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

T-Bills still a great buy for CPF-OA buyers?

If you’re a CPF-OA buyer, there’s frankly no other option for you.

There used to be fixed deposit CPF-OA options, but those have been mostly taken off the market for now.

I’ve run the numbers below – you can see that even at 3.70% it is still comfortably above CPF-OA’s 2.5%.

It’s a 26% increase in interest earned vs CPF-OA (assuming no changes in CPF-OA rates).

The more CPF-OA you have, the more worth it it becomes.

What about Cash Buyers?

Bank Fixed Deposits yield 3.50% for 3 months with Bank of China ($5,000 minimum)

The best fixed deposit in the market today is 3.50% for 3 months with Bank of China.

Do note that this is for a 3 months lock-in, and a minimum amount of $5,000, and must be done via Mobile Banking.

Frankly not all that attractive vs T-Bills.

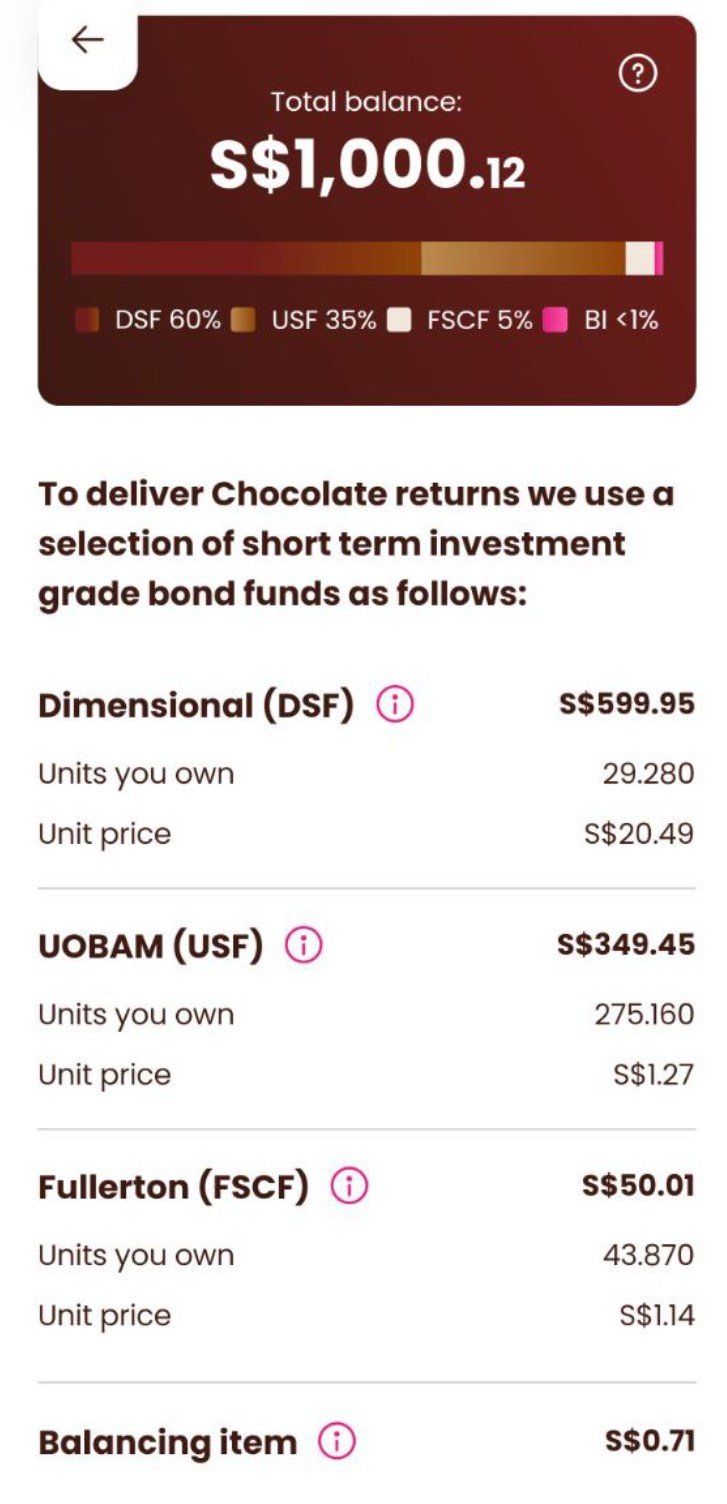

Chocolate Finance pays 4.5% on $20,000 – but NOT SDIC insured

A lot of you have asked for my views on Chocolate Finance, to the point where I went out and did a full in depth analysis.

To sum it up quickly, Chocolate Finance offers:

- 5% yield on $20,000

- Instant liquidity – withdraw any time

- No minimum amount

- NOT Risk Free – Not SDIC insured or backed by the Singapore government

The asset allocation is a mix of short term bond funds with about 1 – 2 years duration, which means there is exposure to underlying credit risk and duration risk:

- Dimensional Global Short-Term Investment Grade Fixed Income Fund SGD – 60%

- UOBAM United SGD Fund – 35%

- Fullerton SGD Cash Fund – 5%

Long story short, it’s not that straightforward to quantify the risk, and you can check out my fuller analysis on Chocolate Finance here.

For me personally, I probably won’t be putting in more than the $1000 I funded to write the article.

Syfe Cash+ Guaranteed – 3.70% yield for 3 months (no minimum)

Syfe just launched a new cash management option recently.

I did an in depth review on Syfe Cash+ Guaranteed.

The long and short is that:

- 70% yield

- 3 month lock up period

- Funds are deposited with institutional class fixed deposits

3.70% for 3 months is competitive vs T-Bills.

However the Syfe Cash+ Guaranteed is technically not risk free, in that it is not SDIC insured or backed by the Singapore government.

Granted, the risk is miniscule (risk is that the bank goes under), but still an important point to note with Syfe Cash+ Guaranteed.

It’s the same logic with money market funds, where yields are competitive with T-Bills and you get T+1 liquidity, but technically not risk free.

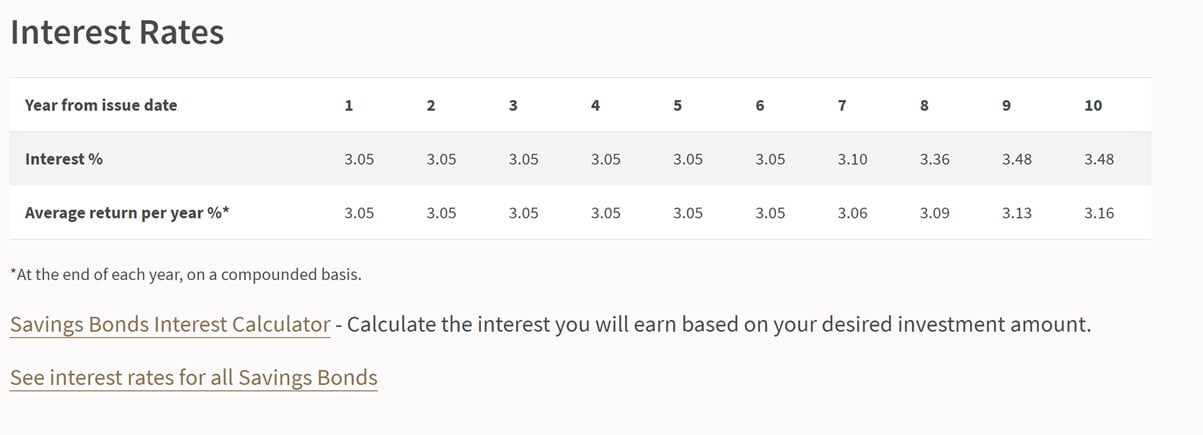

Singapore Savings Bonds at 3.01% yield

As shared above – given that 10 year SGS yields have been going up of late.

This has made Singapore Savings Bonds more attractive (they track 10 year SGS yields).

Latest Singapore Savings Bonds yield 3.05% for the first 6 years, stepping up to 3.16% for 10 years.

Benefits of Singapore Savings Bonds?

The huge benefit of Singapore Savings Bonds though, is no refinancing risk for the next 10 years.

Whereas with T-Bills you need to refinance every 6 months – and if interest rates go down in 2024 you’re out of luck.

Singapore Savings Bonds also have the flexibility to redeem any time with accrued interest and no capital losses.

Which means that in the unlikely event that interest rates go even higher in 2024, you can get your full principle back without any capital losses – and reinvest into whatever you want then (had you invested in long term bonds you would be sitting on a capital loss).

It’s a heads you win, tails you win kind of scenario.

The only trade off of course, is that the short term yield is 3.05% instead of 3.70% (and also no capital gains if interest rates go down – so treat this more as a cash management product).

I myself am applying for Singapore Savings Bonds this month as I think it’s a no brainer.

The only question is how much to apply for, and how much of the older Singapore Savings Bonds to redeem, which is probably a topic for another day.

Will I still buy T-Bills?

With CPF-OA, it’s still a no brainer to buy T-Bills.

Cash though, gets a bit more tricky.

For the first time this cycle – I am starting to get concerned about interest rate cuts in the next 6 – 12 months.

You guys know me.

For much of the past 12 months I’ve been saying the market is too optimistic on interest rate cuts, and Fed need to hike higher and longer than the market is pricing in.

That has all played out.

Where we are today, I think the bigger risk going forward is that the economy weakens faster than the market is pricing in, and the rate cuts come faster and harder than priced in in 2024.

I mean there are no sure things in investing, so obviously I could be wrong on this.

But if I am right, the bigger risk going forward with T-Bills is that when they mature in 6 months you might be looking at a different interest rate climate.

It’s why I have started to look at ways to play the potential reversal in interest rates via REITs, Treasuries etc (shared more on Patreon).

So… will I still buy T-Bills?

That said, I have a large chunk of money in OCBC’s fixed deposit yielding 4.08% from the Chinese New Year period (boy… remember those days?)

Just out of curiosity I checked the OCBC Fixed Deposit rate were I to roll over – and they were offering an abysmal 2.70% interest rate.

No thank you.

Of all the options for cash that are risk free – T-Bills are still the highest yielding today.

So I’ll probably still be applying for the next T-Bills auction.

No doubt there will be refinancing risk in 2024, but let me just earn the 3.70% for the next 6 months first.

This article was written on 7 Sep 2023 and will not be updated going forward. For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do sign up as a Patreon.

– Get up to USD 800 worth of shares

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 800 free fractional shares.

You just need to:

- Fund any amount

- Hold for 30 days

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading .

Get a free stock and commission free trading with .

Get a free stock and commission free trading with .

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Best investment books to improve as an investor in 2023?

Check out my personal recommendations for a reading list here.

3.7% p.a. “risk free” return is still not terrible, you’re probably matching core inflation (or getting close). If you want to build a DIY fixed interest portfolio then you can do a lot worse. SSB’s are great for most of your safety fund (say 75% of it), and are arguably a much better deal than the fixed deposit rates at the banks. As always it depends on an individual’s own situation. Long-term in Singapore, the better REITs and the big 3 banks are probably going to deliver better returns. One sensible strategy is to emphasize equities more if you’re younger, and progressively more fixed interest as you age – after all that’s what fund managers do for us (for a fat fee!).

Spot on!

Thanks for the insights!

You might have included two potential typos:

1. In the opening line, you listed the next auction as “14 August (Thursday)”. I think it should be September (didn’t spot August anywhere else), but because this is right at the top of this post, you might want to correct this.

2. In the paragraph above the FOMC meetings chart, you wrote “I think the bigger risk going forward is that the economy weakens faster than the market is pricing in, and the rate hikes come faster and harder than priced in in 2024.” Should this be referring to rate cuts instead?

My apologies – you are absolutely right on both points.

I have corrected both typos, my bad!