Note: This article is a premium article that first appeared on Patron. Have made it available given the interest around the Ant Group IPO.

If you enjoy articles like this, do consider supporting Financial Horse and getting access to premium articles, my personal stock watch list, as well as my personal portfolio allocation.

Unless you were living under a rock the past few months, you’ve probably heard about the Ant Group IPO.

Very big, and very hot stuff.

It’s the largest IPO in the world to date, raising $34 billion USD, even more than the Saudi Aramco IPO.

It’s been covered to death by the media, so I won’t repeat what’s been said, but I’ll share some of my views here.

There’s a good article from the Nikkei if you want some background: https://asia.nikkei.com/Business/Business-deals/Ant-s-mega-IPO-Five-things-to-know-about-the-fintech-king

Prospectus is available here as well: https://www1.hkexnews.hk/app/sehk/2020/102484/documents/sehk20102101021.pdf

BREAKING: Jack Ma was summoned by regulators to discuss industry guidelines that could hit Ant’s future profits. On Tuesday night, the Shanghai and Hong Kong stock exchanges both announced Ant’s IPO would be postponed.

Pricing of the Ant Group IPO

The offering will be split evenly between HK and Shanghai:

- Shanghai price – RMB 68.8

- Hong Kong price – HKD 80

The listing will be on 5 Nov 2020.

Offering Details of the Ant Group IPO

- Raising $34.4 billion

- Market cap of $313 billion ($320 if over-allotment exercised)

- Sale of 11% of outstanding stock

- 284 times oversubscribed, including GIC, Temasek, CPPIB and Abu Dhabi Investment Authority

FYI we’ll share commentary on the 2020 crisis every weekend going forward, so for those of you who haven’t signed up for our mailing list, please do – its absolutely free.

It’s a weekly newsletter that goes out every Sunday, and rounds up the week’s posts so you never miss anything.

[mailmunch-form id=”928667″]

What I like about Ant Group

Crazy Growth, Exposure to China Fintech Space

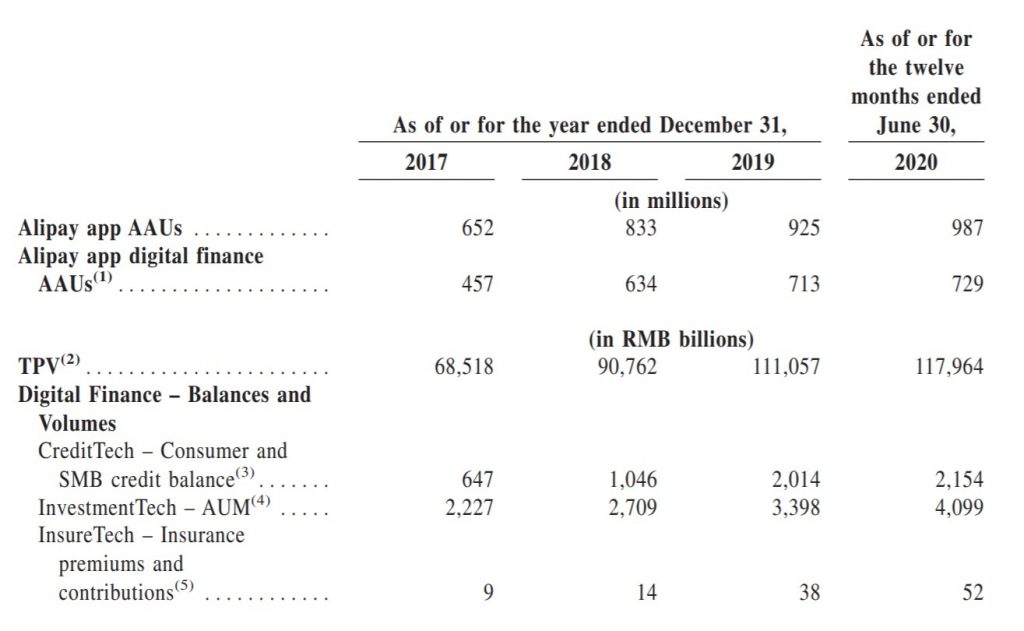

The penetration of Alipay in China is insane. 987 million active users at June 30, means that just about everyone who needs an Alipay account already has one (leaving out babies and the old).

And this is exposure to the high growth China market, with an exploding middle class, and a technology platform. It’s no wonder this was oversubscribed 284 times, including both our sovereign wealth funds.

If you’re an institutional investor, you would get fired if you don’t subscribe for this IPO, and it goes on to gain 20% on listing date. So the big institutional guys have no choice but to subscribe, whatever their view on this IPO.

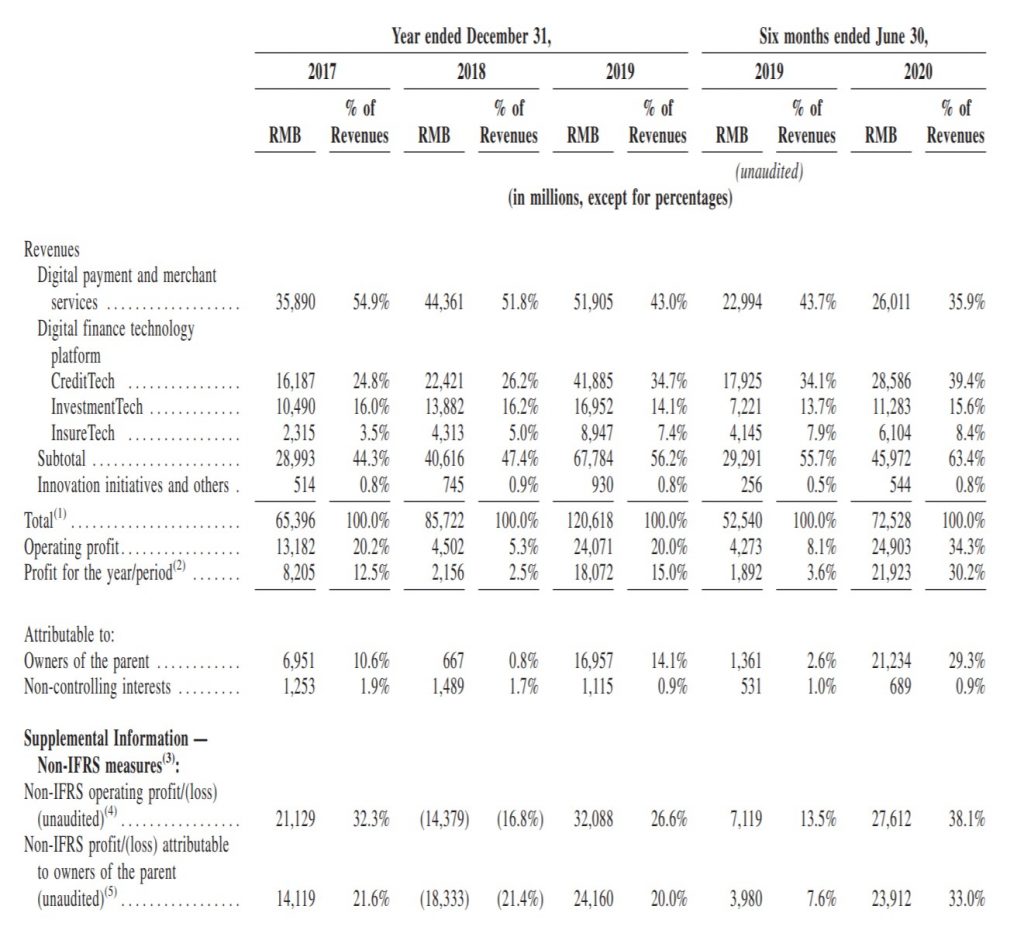

Currently, the bulk of their revenue comes from payments, lending, and investment. In that order.

But really, this is a tech platform, and with the user base and the Alibaba connections, they can easily expand into other areas they set their sights on.

Personal View – If you’re in China, you cannot not have an Alipay account. Taobao only accepts payment via Alipay (not WeChat Pay), and Taobao is crucial to every day life, so everyone has an Alipay account.

Their user base is basically the whole of China. So far, they’ve monetized it mainly via lending and investment services. But frankly, the sky is the limit here, once you have a user base of this size, and the weight of the Alibaba Group behind you.

Valuations of Ant Group

The valuation of Ant Group depends on whether you view it as a tech company, or a bank.

Comparing against other tech companies, the valuation are decent:

|

Company |

Market Cap (USD billions) |

P/E Ratio (trailing twelve months) |

|

Ant Group |

313 |

81 (43x if we use 1H2020 numbers and annualize) |

|

Alibaba |

820 |

33 |

|

Tencent |

700 |

48 |

|

Meituan |

200 |

600 |

|

Pinduoduo |

104 |

Not meaningful (no profits) |

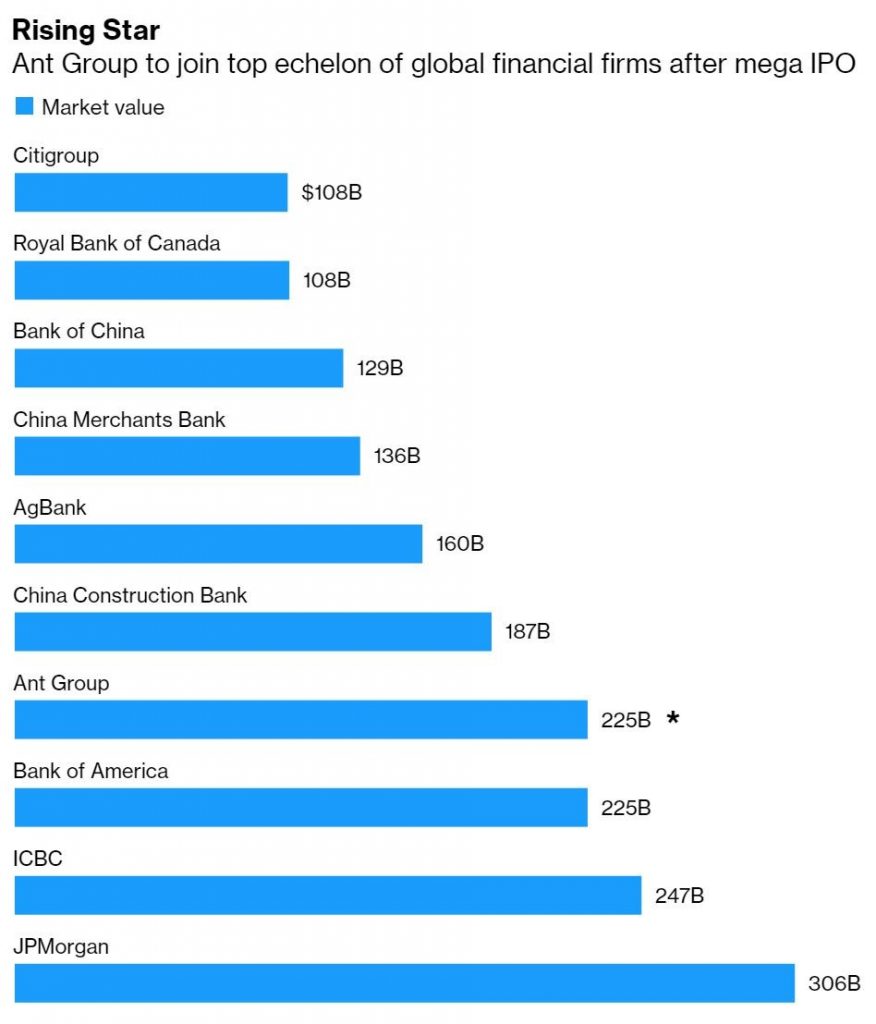

Comparing against other banks, Ant Group will be the largest bank in the world, topping even that of JPMorgan and ICBC.

Note: The placing below is inaccurate, because they’ve upped the valuation to 313b.

Personal View – I think the comparison to tech is more accurate, because with their user base, they can easily build to a super app to rival WeChat. It’s reminiscent of what Grab is trying to do in South East Asia. At a 313b market cap, I think the valuation is reasonable.

What I don’t like about Ant Group

Regulatory Risk

I think the biggest risk to Ant Group is regulatory / political risk.

From the CCP.

In China, everything comes back to political risk. If you don’t get into the good books of the CCP, you can get crushed overnight. There doesn’t even need to be a reason, because this isn’t like the US.

Regulatory / political risk is almost impossible to predict, so it’s something you have to be comfortable with when investing in China.

And to be fair, if you invest in Alibaba / Tencent / ICBC or any other China player, you’re already taking on this risk.

For now, Alibaba seems to be in the good books of the CCP, especially after the stepping down of Jack Ma.

One concern though, is that the PBOC is not happy with the dominance of Alipay and WeChat Pay, and are rolling out a digital yuan, to allow the banks to bypass Alipay/WeChat for payments.

When the government wants something done in China, it’s as good as done, so this will be a threat to both players going forward. It’s tough to fully assess the full implications of the digital yuan though. It could be massive, or it could be a dud, much depends on the execution.

Competition – Tencent/Ping An and Traditional Banks

There is also competition from the tech players like Tencent/Ping An, and the traditional banks like ICBC or CCB.

The China market is intensely competitive, so no getting around this.

But for now, Alipay’s position is incredibly entrenched due to their user base. Once you build up a user base this size, network effects kick in, and it becomes almost impossible to displace.

Same story with Visa and MasterCard in the west. Incredibly hard to displace, leading to fat margins.

Personal View on Ant Group IPO

My concern with the Ant Group IPO though, is how much would it jump on day one.

All the recent big IPOs have had crazy day one jumps, with Nongfu Spring doing almost 100% on day one. And that was a water company.

If it jumps 40%, that’s a valuation of 438b. While such a valuation may make sense longer term, short term it would still look aggressive.

And very tough to get placed into the IPO for this one, unless you’re high net worth and willing to fork out $250,000 to take a punt on an allocation.

Could this play out like the original Alibaba IPO?

I also have concerns that this may play out the same way as the original Alibaba IPO.

A refresher on how the Alibaba IPO played out:

- IPO-ed at $68

- Jumped to 90+ on day one (35% jump)

- Traded to $120 over the next 3 months

- Collapsed to $60 over the next 12 months

- Went on a big uptrend after that to $300 today.

In that case, the ways to make money are:

- Buy on IPO day and flip it shortly after for a small gain

- Wait for the post-IPO crash and buy in

- Buy at any time and hold long term

I have my suspicion this one could play out in a similar fashion, but it really is just a hunch at this stage.

Would I buy?

I think the $313b valuation is reasonable, but in any case I don’t have an allocation for the IPO.

So I still have to wait for it to trade on the open market, and I’ll get to see how big the day one jump is before deciding.

My current view subject to change, is that:

- I could buy on IPO day and flip it shortly after for a small profit

- I could buy on IPO day and average in over a 12 month period to build a long term position

Haven’t decided on which yet. But either way, barring a massive day one jump, I would be tempted to open a position on IPO / shortly after it commences trading.

This article is written on 27 October and will not be updated going forward. Latest thoughts (and my stock watch and personal portfolio) are available on Patron.

Note: This article is a premium article that first appeared on Patron. Have made it available given the interest around the Ant Group IPO.

If you enjoy articles like this, do consider supporting Financial Horse and getting access to premium articles, my personal stock watch list, as well as my personal portfolio allocation.

Share your comments below!

Support the site as a Patron and get access to my personal stock watch list, as well as my personal portfolio allocation.

Do like and follow our Facebook Page, or join the Telegram Channel. Never miss another post from Financial Horse!

Join our Facebook Group to continue the discussion, everyone is welcome!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Both are THE best quality investment courses available to Singapore investors out there!