Planning for retirement can feel intimidating, especially when CPF rules, retirement sums, and payout options start to sound technical.

But at its core, the goal is a simple one: to build a steady income you can count on later in life.

For many Singaporeans, CPF is not just a savings system — it is the foundation of that security.

This article was written by a Financial Horse Contributor.

Optimise for payout, not for optionality

A common mistake is to optimise for the ability to pull cash out at 55, instead of for lifelong payout strength.

That feels flexible, but it often weakens the one pool of money designed to keep paying you no matter how long you live.

CPF itself warns that withdrawing now lowers future monthly payouts.

Its Retirement and Health Study also found that around four in 10 members aged 55 to 70 did not make any cash withdrawals after 55 even though they could; among those who did withdraw, many simply parked the money in banks or used it for near-term spending. In other words, “I can withdraw” does not automatically mean “I should withdraw.”

That does not mean withdrawals are always wrong. A member who is house-rich, cash-tight, or facing a real liquidity need may reasonably choose otherwise. But the default should be caution. Once you top up retirement savings, those top-ups are irreversible and reserved for retirement payouts. CPF is telling you, quite plainly, that this is long-term money.

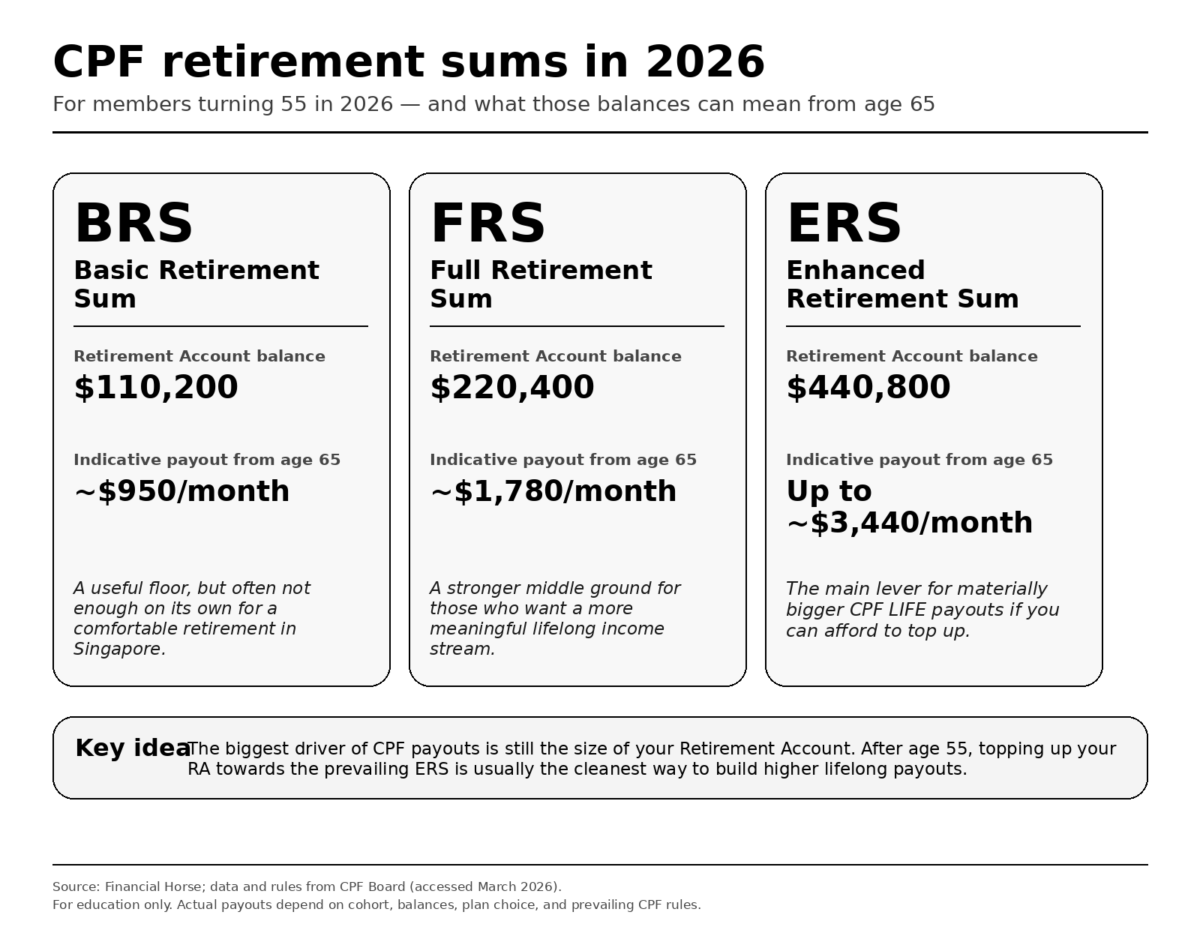

After 55, the cleanest move is to keep funding the RA up to ERS

A lot of old CPF chatter focused on hacks around the Special Account. That world changed. For members aged 55 and above, the Special Account was closed on 19 January 2025; SA savings moved to the Retirement Account up to the Full Retirement Sum, with any excess going to the Ordinary Account. For members 55 and above today, the focus is now on the Retirement Account itself.

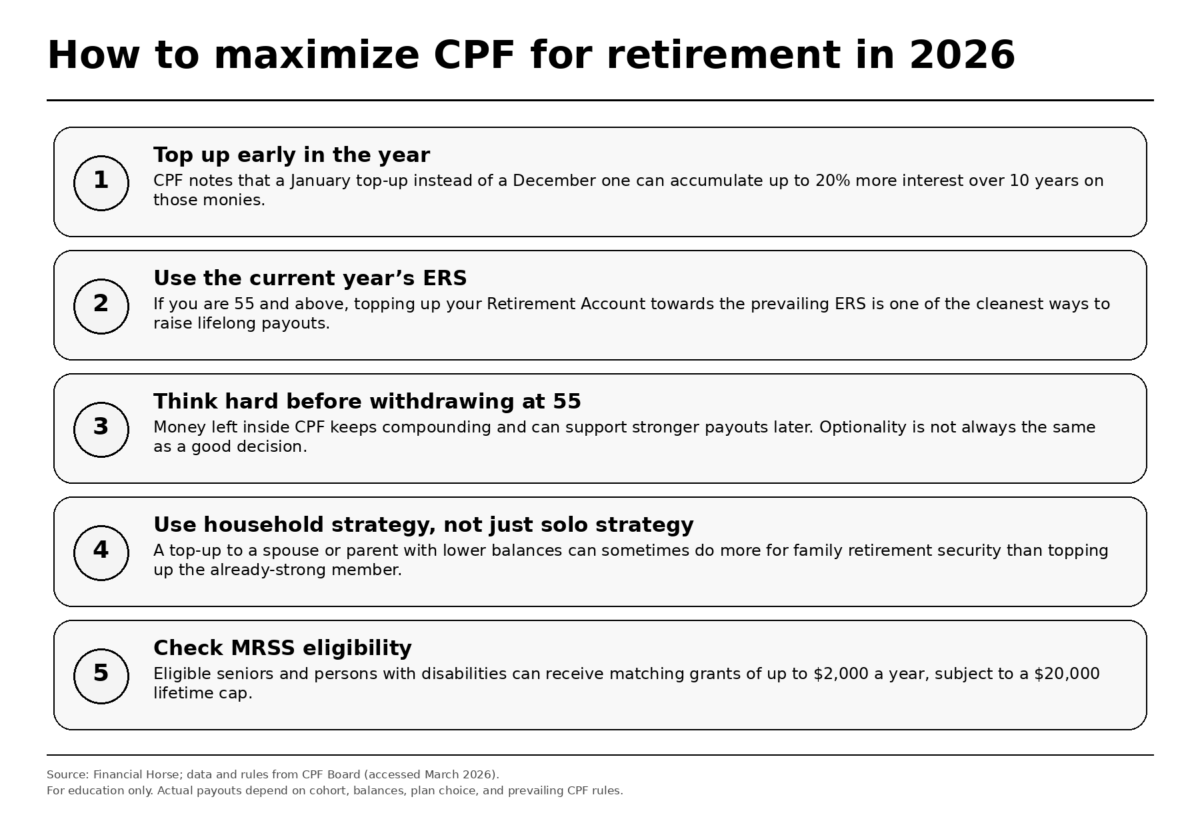

That is why one of the best practical habits is simple: check your RA every January and decide whether to top up to the new prevailing Enhanced Retirement Sum (ERS).

CPF explicitly notes that from age 55, you can top up your RA to the current year’s ERS, and because ERS rises over time, you can make further top-ups each year for higher future payouts. CPF also notes that topping up early matters: a January top-up instead of a December top-up can earn materially more interest over a decade.

Deferring payouts is one of the strongest levers, and many people underuse it

CPF lets you start payouts any time from 65 to 70. If you defer and you are on CPF LIFE, your payouts rise by up to 7% for each year of deferral, or up to 35% if you wait to 70. That is not a small tweak. It is one of the most powerful risk-free payout levers in the whole system.

The math is straightforward:

Higher payout later = payout at 65 × up to 1.35

So if your indicative Standard Plan payout is S$3,440 at 65, deferring all the way to 70 could lift that to roughly S$3,440 × 1.35 = S$4,644 a month. At FRS, S$1,780 × 1.35 = about S$2,403.

These are illustrations, not promises, because actual payouts depend on your cohort, plan and balances, but the point stands: if you do not need the cash at 65, deferral is powerful.

This works especially well for people who are still earning, have rental income, or simply want to insure more strongly against living into very old age.

It is less attractive if your health is poor or you need the income immediately. Maximising payout is not always the same thing as maximising wisdom.

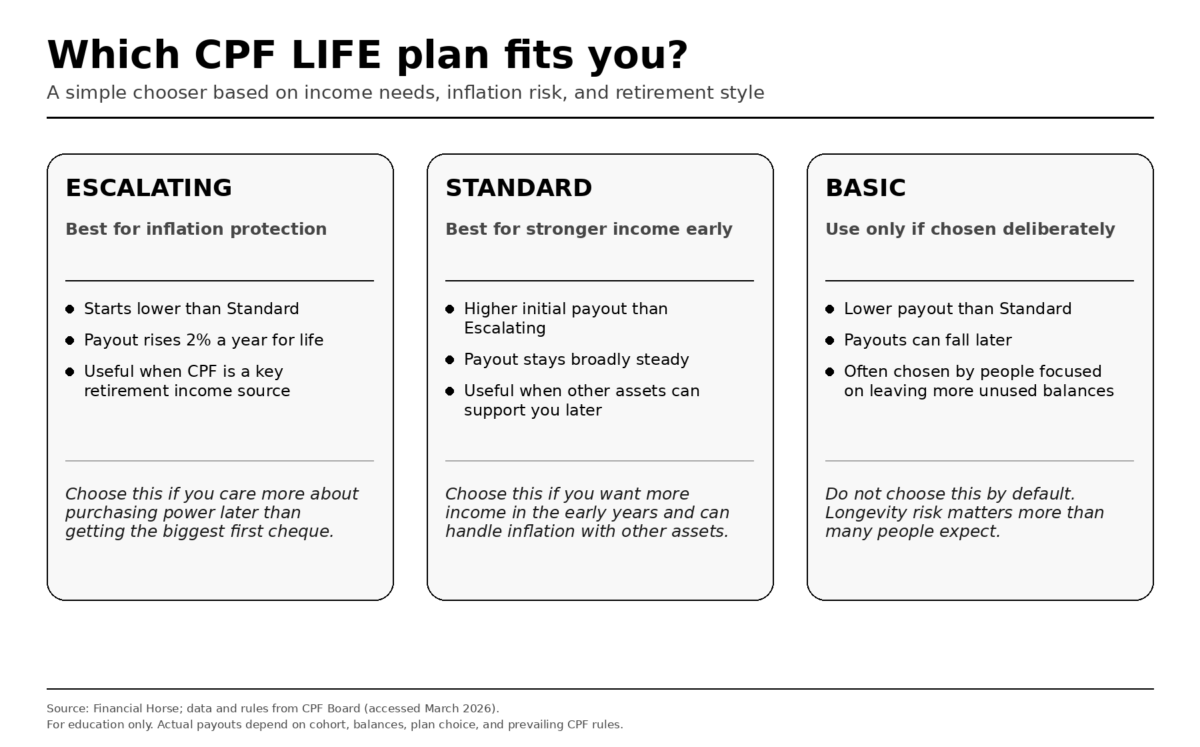

Pick the CPF LIFE plan with inflation in mind

CPF LIFE gives three broad choices.

The Escalating Plan starts lower but rises 2% a year for life. The Standard Plan pays a steady amount. The Basic Plan starts low and can fall later once balances drop below S$60,000.

CPF itself frames the choice around how willing you are to reduce your lifestyle as prices rise. That framing is useful. Inflation risk is real, and a “higher first cheque” is not always the best long-term outcome.

For many people, the most underappreciated plan is Escalating.

If most of your retirement spending will be funded by CPF, a payout stream that grows can age better than a flat payout stream. The Standard Plan suits people who want more income earlier and are comfortable that other assets will handle later-life inflation. The Basic Plan should be a deliberate choice, not a lazy default.

Some people look at CPF LIFE and think, “Which plan leaves more unused money for my family if I die earlier?” That is the bequest mindset.

But CPF warns this should not be the main reason for choosing a plan, because the real purpose of CPF LIFE is to give you income for as long as you live.

Bequest-focused thinking: “What happens if I die earlier?”

Retirement-income thinking: “What happens if I live much longer than expected?”

Never miss a post! Follow Financial Horse by subscribing or following us on your favorite platform:

Subscribe to our mailing list for exclusive content straight to your inbox:

Working longer can matter more than clever structuring

From 1 January 2026, total CPF contribution rates for employees above 55 to 60 are 34%, and for those above 60 to 65 they are 25%.

For members 55 and above, contributions that would previously have gone into SA now flow to RA up to FRS, and only then to OA.

Separately, from 1 July 2026, Singapore’s retirement age rises to 64 and re-employment age to 69 for the relevant cohorts. The quiet takeaway is that one extra stretch of good earnings in your late 50s or early 60s can lift retirement payouts materially, especially if those extra contributions are landing in RA territory.

This is one reason many retirees and pre-retirees now think in layers rather than in a hard stop. CPF becomes stronger when retirement is phased, not binary.

Household strategy often beats solo strategy

Many people obsess over their own CPF and ignore the household balance sheet. That is often a mistake.

CPF allows cash top-ups to yourself and loved ones, with up to S$8,000 tax relief for top-ups to yourself and another S$8,000 for eligible loved ones in a calendar year. But there is a catch: tax relief is not granted for top-ups beyond the current year’s FRS, and cash top-ups that qualify for MRSS matching grants do not also get tax relief.

So the smarter question is often: where does the next S$1 most improve household retirement security? If your own RA is already strong, topping up a lower-balance spouse or parent may create more useful household resilience, especially if that person qualifies for the Matched Retirement Savings Scheme. MRSS now offers dollar-for-dollar matching of up to S$2,000 a year, subject to a S$20,000 lifetime cap, and from 2026 it also covers eligible Singaporeans with disabilities of all ages. That can be a very high-impact move.

MediSave can help retirement more than people realise

In 2026, the Basic Healthcare Sum is S$79,000 for members aged 65 and below, and the applicable BHS is then fixed once you hit 65.

When MediSave savings are above the BHS, the excess goes to SA or RA depending on age, and if the Full Retirement Sum has already been set aside, it can then flow to OA.

That means a well-managed MediSave balance can indirectly support retirement adequacy, especially for self-employed people and later-career earners whose inflows continue.

This is not the main lever. RA top-ups are still more direct. But it is a useful secondary engine that many people overlook.

A few human lessons …

Lorna Tan, a longtime personal finance writer in Singapore, offers a useful example of how strong CPF planning is usually built through discipline rather than clever tricks. In DBS articles, she describes topping up her Retirement Account to the prevailing Enhanced Retirement Sum at the start of the year, adding to MediSave, and making a top-up to a parent’s Retirement Account, while also saying she intends to keep doing this each year to raise her future CPF LIFE payouts.

Loo Cheng Chuan, who became known in Singapore personal finance circles for reaching S$1 million in CPF by age 45, is another useful example of what long-term CPF compounding can look like when someone starts early and stays consistent.

His story is not really about a secret hack, but about making regular decisions over many years, including building up higher-interest CPF balances early and giving them time to grow. The takeaway is not that everyone should try to copy his exact path, but that CPF can become far more powerful than many people realise when it is treated as a long-term wealth-building and retirement tool, rather than just a mandatory deduction from salary.

CPF’s own study adds a sobering final lesson: retirees’ expenses can rise later in life because of inflation and care needs, and many people who withdraw at 55 do not deploy the money into something obviously better.

Withdrawing a lump sum can feel like freedom or a reward after decades of work, but if that money is then left in low-yield deposits or simply spent, you may have traded away a stronger lifelong income stream for short-term comfort.

That matters because retirement costs do not always fall with age. Inflation, healthcare, and care needs can push expenses up later in life, so preserving a solid CPF income floor may be more valuable than immediate access to cash. The real question is not just whether you can withdraw at 55, but whether doing so leaves your future self better protected at 75 or 85.

What to focus on at each stage

| Life stage | Main priority | Best practical moves | Watch-outs |

|---|---|---|---|

| Below 55 | Protect compounding | Build CPF steadily over time. Consider OA-to-SA transfers only after you are comfortable on housing needs and emergency cash. Let time and higher long-term interest do the heavy lifting. | Do not over-transfer if it leaves you too cash-tight for housing, family needs, or liquidity. |

| Age 55 to 64 | Strengthen the Retirement Account | Focus on RA funding. Review the prevailing ERS each January and consider topping up if affordable. Avoid withdrawing at 55 by reflex. | After 55, the story is no longer mainly about SA. The key question becomes how much you can build inside the RA for higher lifelong payouts. |

| Age 65 to 70 | Make deliberate payout decisions | Decide whether to start payouts or defer them. Choose the CPF LIFE plan that fits your spending needs and inflation risk. Consider whether withdrawable balances are better left inside CPF to support higher payouts. | Doing nothing is still a decision. If you do not act, payouts will auto-start at 70, and if you do not choose a CPF LIFE plan, you may be placed on the default plan. |

The bottom line

The best way to get bigger CPF payouts is usually not to look for clever tricks.

It is to work with the system as it is designed: build up a larger Retirement Account, let your savings compound for longer, choose your CPF LIFE plan carefully, avoid taking money out too early, and defer payouts if you do not need the income right away.

In other words, CPF tends to reward patience, consistency, and leaving more money inside the system for longer.

A final 2026 footnote: eligible Singaporeans aged 50 and above with lower retirement savings will receive a CPF top-up of up to S$1,500 in December 2026, depending on their balances and property annual value. That will not transform a retirement plan on its own, but for the right household it is still worth checking.

I’d also add that for those who have spare cash, they can also consider topping up their children’s SA account from a very young age, as the power of compounding over 50-60 years at 4% p.a. (at least) is significant.

Good point, thanks for raising