You’ve probably felt it: the same grocery run costs more, kopi feels pricier, and a “simple” dinner somehow turns into a big bill.

So it’s natural to ask: Is inflation eating away our money in Singapore?

Recent official data shows inflation has cooled, yet many people still feel squeezed.

You can protect yourself by measuring your personal inflation, fixing the big three costs (housing/transport/food), and making cash + income move forward faster than prices.

This article was written by a Financial Horse Contributor.

What inflation actually does (in plain English)

Inflation means prices rise over time.

If prices go up but your income and savings don’t rise at least as fast, your money buys less.

Think of it like this:

- Last year, $100 bought 10 things.

- This year, the same 10 things cost $102.

- If your pay and savings didn’t rise, you’re effectively poorer—even if your bank balance looks the same.

That’s how inflation “eats” money: not by taking your cash, but by shrinking its buying power.

“But I read inflation is low now—why does it still feel bad?”

Your inflation rate is not the national inflation rate

Official inflation numbers are based on an “average” basket of goods and services. But your life isn’t average.

If you spend a lot on:

- Rent

- Transport (especially private transport)

- Food for a family

…you may feel inflation more than someone with different spending patterns.

In fact, Singapore’s commonly cited MAS Core inflation excludes accommodation and private transport, so it can look calmer than what many households experience.

Prices don’t need to keep rising fast to feel painful

Even when inflation cools, prices often stay high.

“Chicken rice used to be $3.50. It’s $4.50 now. Even if it stops rising, it still feels expensive.”

That’s because inflation is about change, but your wallet cares about the new level.

Some rises are structural, not temporary

Singapore also had policy-driven cost changes. For example, GST is 9% from 1 Jan 2024, which affects many purchases directly or indirectly.

So even if headline inflation slows, you can still feel the “after-effects” of earlier increases.

So… is inflation “eating away” our money?

Yes, if your money is standing still.

No, if you’re actively managing it.

What matters is the gap between:

- How fast your costs rise, and

- How fast your income + savings returns rise

If your costs rise faster, inflation is eating into your lifestyle.

If your income and returns rise faster, you’re fine.

The best way to know: calculate your personal inflation

Here’s a simple method that beats guessing:

- Look at your spending for the last month (bank app is enough).

- Identify your top 3 categories by dollars (usually housing, food, transport).

- For each category, ask:

- Did the unit price rise? (same item costs more)

- Or did my usage rise? (more deliveries, more rides, more “treats”)

This step matters because “inflation” often gets blamed for habit drift/ lifestyle inflation.

“I didn’t change anything.”

(Turns out: delivery once a week became delivery 3x a week.)

Practical ways to fight inflation in Singapore

1. Fix the “Big Three” first: housing, transport, food

Finances explode because people focus on small savings while the big bills leak.

Housing

- If you rent, start negotiating early. Collect 3 comparable listings before renewal.

- If you’ve bought, actively monitor your mortgage rates and refinancing opportunities.

Transport

- Set a weekly limit for ride-hailing.

- Make public transport the default and ride-hailing the exception.

Food

- Decide your “default mode” (hawker/food court/home) and plan restaurant meals as treats instead of impulse.

2. Cut subscriptions like a barber

Subscriptions are sneaky because they’re quiet and “not that big” individually.

One household found:

- multiple streaming services

- unused cloud storage

- a premium telco plan they never needed

They saved ~$60/month. That’s ~$720/year with almost zero lifestyle pain.

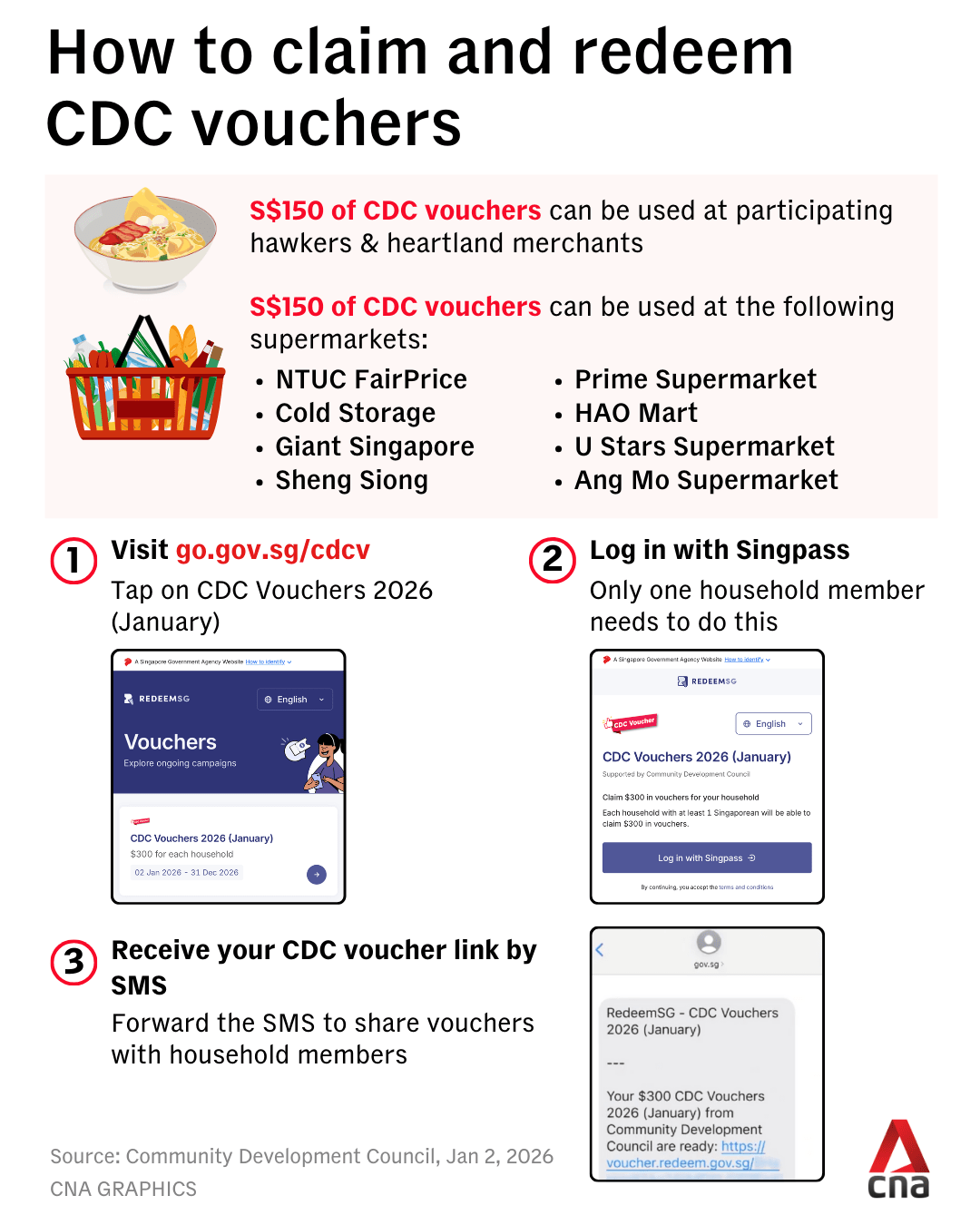

3. Don’t miss out on gov freebies!

If you’re Singaporean, make sure to claim your benefits:

- CDC Vouchers: households can claim $300 in Jan 2026, valid till 31 Dec 2026.

- U-Save / S&CC rebates: MOF has announced rebates for eligible HDB households, including Jan 2026 disbursement details.

4. Make idle cash earn

Inflation punishes cash that sits still.

You don’t need to do anything complicated—just avoid the trap of:

- too much idle cash earning little, and

- too little buffer when emergencies happen

A healthy structure is:

- Emergency fund (liquid, safe)

- Near-term goals (low-risk, timeline-matched)

- Long-term investing (diversified, consistent)

A high yields saving account like DBS Multiplier should be a no brainer – credit your salary & you can earn interest on your idle cash seamlessly.

5. The strongest inflation hedge is still income growth

Cutting spending has a ceiling, income growth doesn’t.

Focus your time and energy where it has the highest ROI i.e., scaling the corporate ladder, investing in yourself: both skills and network.

Bottom line

Inflation in Singapore isn’t a monster that wipes out everything overnight. It’s more like a slow tax on doing nothing.

If you:

- measure your personal inflation,

- fix the big three costs,

- stop recurring leaks,

- claim what you’re eligible for,

- and keep income moving,

…inflation becomes manageable instead of scary.

Never miss a post! Follow Financial Horse by subscribing or following us on your favorite platform:

Subscribe to our mailing list for exclusive content straight to your inbox: