Since the market top in the NASDAQ in early Sep, I’ve been getting a couple of questions on:

- Are we in a stock bubble?

- Is a bigger market crash coming?

- Should I sell my stocks now and buy back later?

- Is it a good time to buy stocks now?

So I wanted to share my views in this article.

If you disagree, feel free to share your views below. Nothing I love more than constructive disagreement.

Are we in a stock bubble?

It’s funny that we’re in the biggest global recession since WWII, and the question that pops up is whether we are in a stock bubble.

It’s definitely strange, but the response from the Feds back in March have created a very liquidity fueled market. And all that liquidity needs a home to go to.

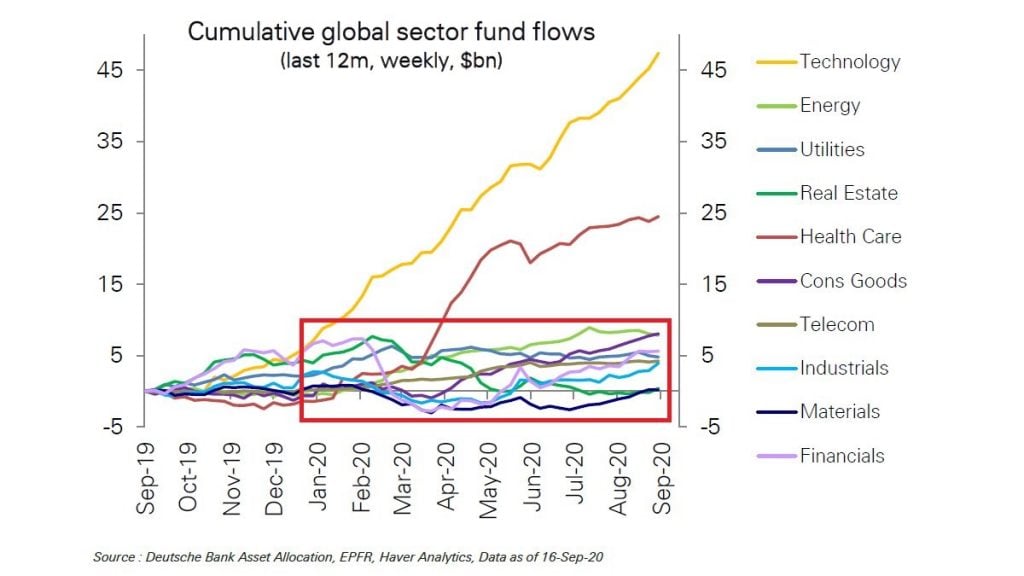

Tech is the most resilient sector and actually benefits from COVID, so a lot of the liquidity flowed there.

It’s reminiscent of the 2000 Dot Com Bubble, which took place in the backdrop of the Asian Financial Crisis. Money from all around the world flowed into US Tech stocks. This inflated a bubble, and eventually the bubble burst.

Similar dynamic today, as you can see in the chart below.

FYI we’ll share commentary on the 2020 crisis every weekend going forward, so for those of you who haven’t signed up for our mailing list, please do – its absolutely free.

It’s a weekly newsletter that goes out at noon every Sunday, and rounds up the week’s posts so you never miss anything.

[mailmunch-form id=”928667″]

Signs of Froth

There’s definitely some signs of froth in this market, that usually you only see in a late stage cycle:

- Market outperformance has been limited to a handful of stocks (FAANG)

- Bullish retail sentiment rising to speculation level in some stocks (Tesla, Nikola, Hertz etc)

- Flood of IPOs at aggressive valuations (Snowflake, Nongfu Spring etc – the IPO window just opened, but we’ll see more in the coming weeks and months – big one in Alipay)

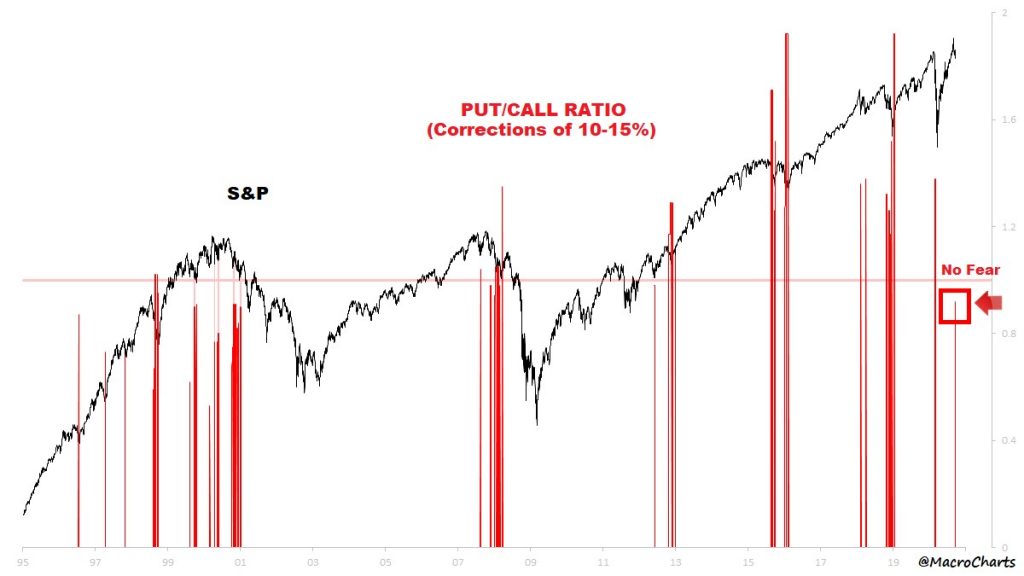

Interestingly, there’s also been very little fear in the market, especially when compared to previous corrections. Investors are still very bullish, even after the recent correction. It’s changed a bit the past few days, but still very different sentiment from March 2020 or Dec 2018.

My personal take?

There’s a famous example from the 2000s of Larry Ellison (Oracle CEO).

Oracle shares were trading at 10 times sales at the time, which he though was crazy.

He put it this way – You’re paying 10 times of yearly revenue to buy the company. So if a company gets to keep all its revenue in a year (which assumes there is zero expense which is impossible), then you’ll only get your money back after 10 years.

Larry thought this was crazy.

At the time of writing, Snowflake trades at 150 times sales, with a $60 billion market cap.

I mean I do get that there’s a lot of growth in this company, and the total addressable market is massive. But 150 times sales just seems very, very steep to me. It will need to grow at 30 – 40% for many years to even make sense.

So personal view – I do think there are signs of froth in this market, but mainly concentrated in tech names.

Outside of US Tech (and China Tech to a certain extent), the market has been somewhat rational.

That said – even in Tech, we’re nowhere near 2000 levels of insanity. Microsoft trades at 10 times sales today. In 2000, it went as high as 30.

If we do go to Dot Com levels, there’s still a lot of room to rally in stocks.

But Microsoft’s chart tells a cautionary tale.

Investors were right – Microsoft did turn out to be a fantastic company that continued to grow its revenue for many years.

But the investors who bought in at the top, at 30 times Price/Sales? They needed to wait 10 years or more to break even.

So a company can do fantastically well, but whether you make money still depends on the price you bought it at.

What are the market technicals telling us now?

There’s been a lot of interesting moves since early Sep.

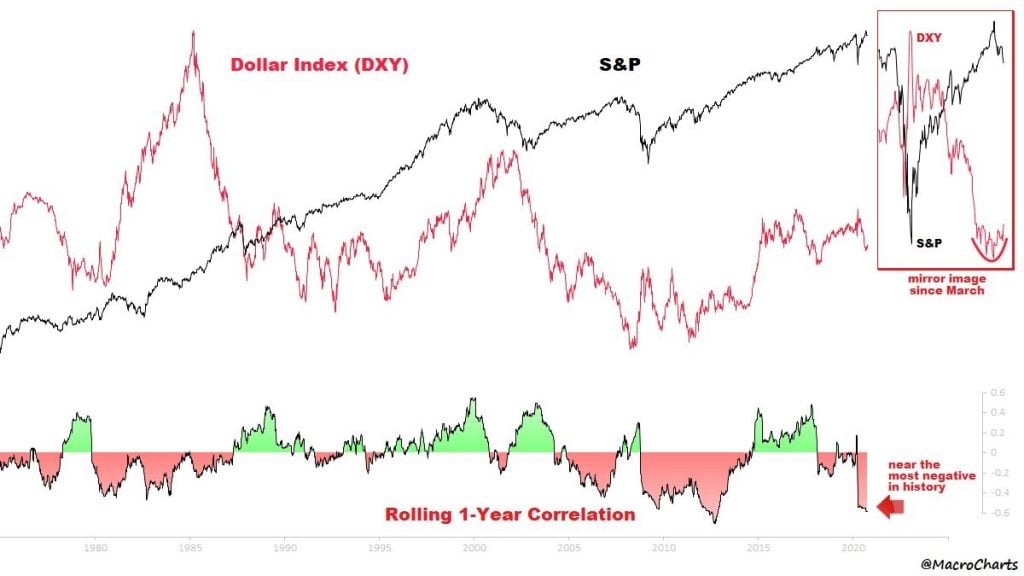

The biggest one to me, is the dollar rally.

USD – DXY Index

Back in March, we talked about how everything goes back to USD strength. The USD is the world reserve currency, and it determines financial conditions for the whole world.

If the dollar drops, everything goes up. If the dollar goes up, everything goes down.

Since its peak in March, the dollar has absolutely collapsed. This has sparked a massive rally in global risk assets.

You can see this on the chart below. It’s a very powerful correlation – one of the biggest in history.

Since July however, the dollar started to consolidate / bottom.

And of course, risk assets also started to consolidate.

And in the past week, dollar has started to rally. And you guessed it – everything else, stocks, commodities, gold, silver etc, has fallen.

My personal take?

I agree that mid term (say 2 to 3 years out), the dollar will be significantly lower than where it is now.

I’m just not so sure about the short term.

Short term, I think the Euro is still way too strong, and a lot of emerging market currencies are still looking very unstable (esp the Turkish Lira). I still think there is a possibility of a dollar strengthening short term, before a midterm collapse.

If so, this could spark another risk off event. A big one to watch.

Investment Grade Credit

IG Credit is also worth watching.

The LQD ETF has rallied a lot since March lows, but is starting to show some weakness. If it breaks 134, that could be big.

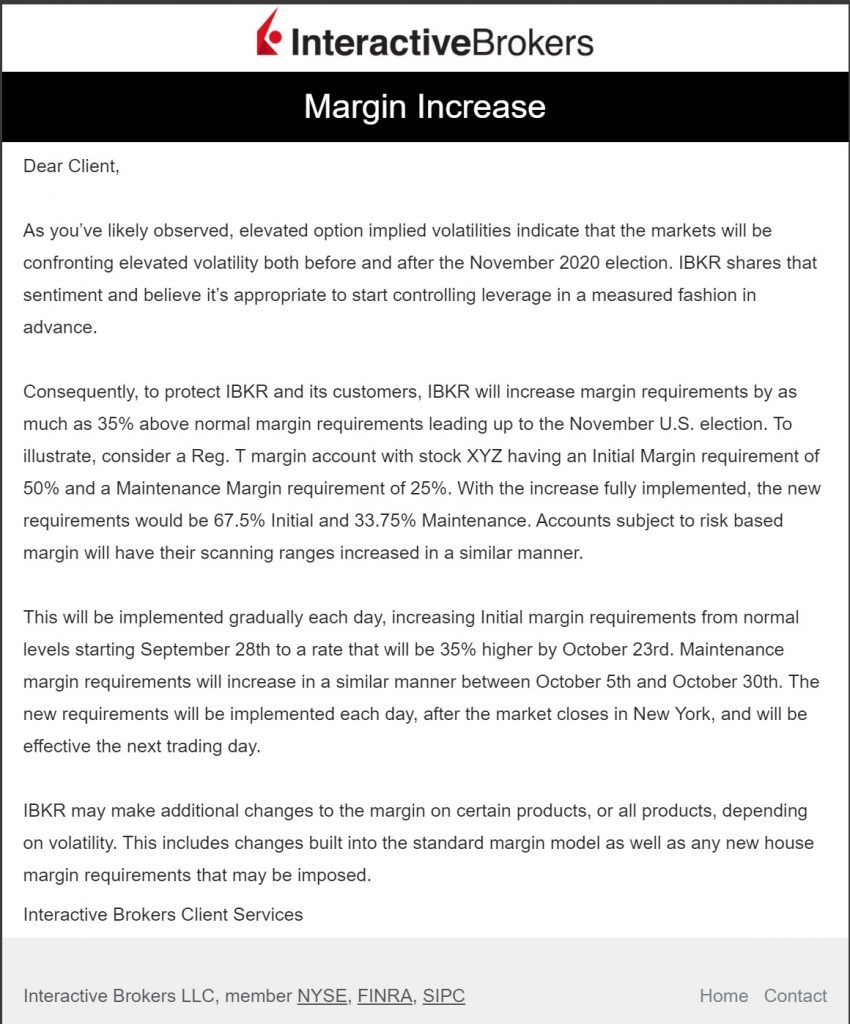

Margin Trading

The past week I received this notice from Interactive Brokers.

Long story short – They anticipate elevated volatility heading into the Nov elections, so they are raising margin requirements.

It’s one of those chicken and egg situations here. Does the margin raise cause the volatility, or does the volatility cause the margin raise?

We’re in this business to make money and not to debate philosophy, so bottom line is – If brokers are going to raise margins heading into Nov in anticipation of volatility, that could be self-fulfilling.

My Personal Take on Market Technicals?

There’s a saying that market bottoms are an event, market tops are a process.

I think it’s too early to say that this is THE market top, and sell everything now.

Big tops around market events tend to take time to play out. It’s not a liquidity event like March where everything just breaks in a few weeks.

We’re still getting into the insolvency phase, and I think it’s going to be a lot choppier than people expect.

If the market is going a lot lower from here, there’s still be some signs before then… I think.

What about fundamentals?

This is where fundamentals can come into play, by giving us some clues on what may happen.

And there are 2 big points to look out for:

- COVID situation

- Fiscal stimulus

COVID Situation

I penned a long post for Patrons recently on this (do sign up if you’re keen on such premium content).

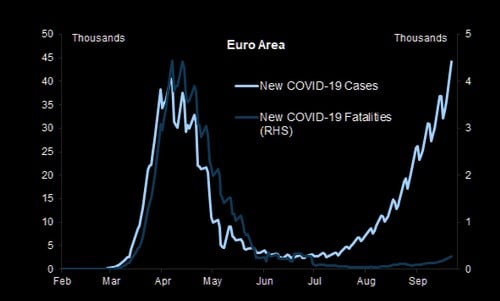

The gist is that I am worried about the COVID situation heading into the winter months.

This is what Europe looks like, which looks a lot like a second wave.

In terms of options available, there are two ends of the spectrum here. On one end there is (1) lock down to combat the virus, but cause massive economic damage, and on the other end you have (2) don’t lock down, and let the economy run free.

I suspect Europe will eventually settle somewhere between (1) and (2). This will impact the economy, and raise the possibility of a double dip recession.

As we head into winter, more and more countries in the northern hemisphere may run into this problem as well.

This will be a big drag on the economic recovery.

I also think that a vaccine may not be the holy grail everyone is expecting, because there are so many logistical problems (how effective is it, who foots the bill, how do you vaccinate the whole world, do you force people to take it etc). Even after a vaccine is released, it will be many months before life can go back to “normal”, by which time there would be long term structural damage to the economy.

I genuinely think the only historical comparison for COVID from the last century is World War II. The world as we know it has changed permanently, and the world we emerge into post-COVID will be as different as the world post WWII.

Fiscal Stimulus

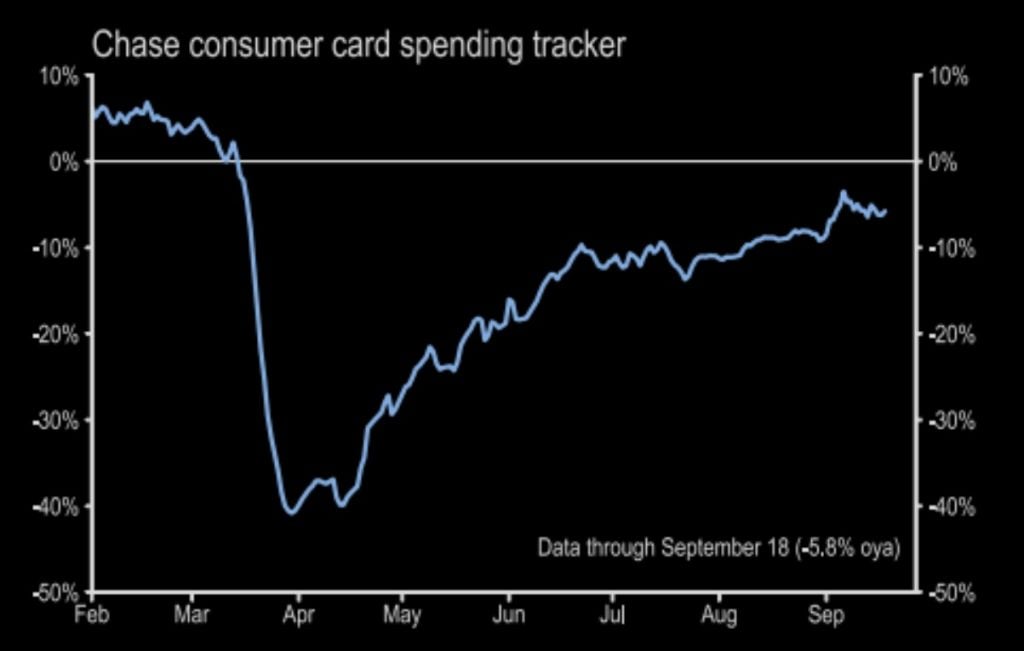

A lot of the fiscal stimulus this cycle was front loaded.

Back in March, everyone thought COVID would be a few months thing. So you just inject massive money to tide the economy through until lockdowns go away, and then you have a massive recovery.

It turns out COVID is going to be a lot longer than what people expected. So the original fiscal stimulus started falling away, and once it did, the recovery started to stall.

The chart below shows this – US consumer card spending recovered very strongly from the bottom, but in recent months that recovery is starting to stall.

Singapore injected almost $100 billion, or 20% of our GDP into the economy this year. It would be tough to keep up that pace of stimulus, as it will quickly burn into reserves.

Similar stories for a lot of other economies like HK and the EU. Emerging Markets are even worse because they don’t have the reserves to do fiscal stimulus, without depreciating the currency.

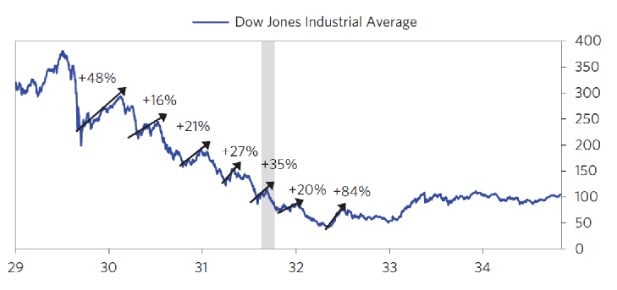

Great Depression analogy

I know the Great Depression was a very different time, and the circumstances don’t apply here.

But I can’t help but notice certain similarities.

The Great Depression started with a sharp market selloff in 1929. Then there was a big rescue package, creating a recovery in stocks that lasted about 6 months.

After that, economic data continued to disappoint, and from there stocks kept on going down. There were very strong rallies along the way, but the broader trend was down.

This eventually became a banking crisis because of all the bad loans from corporate bankruptcies.

This only ended in 1932 when Roosevelt took the USD off the gold standard and depreciated the dollar by around 30%.

Seems similar here right, at least so far?

A sharp selloff in March, a big monetary and fiscal package creates a 6 month recovery, after which it starts to stall.

As it gets worse, it may transition into a banking crisis.

Endgame – The problem only goes away eventually when the USD (and global fiat currency) is depreciated massively.

My Personal Take?

We have only just started to move into the insolvency phase. So we’ll see a lot more insolvencies and unemployment, before it gets better.

To really solve this, we need (1) COVID to come under control, and we need (2) decisive and unprecedented action from politicians on fiscal stimulus.

Both of which carry their own problems.

As discussed, I think a second wave of COVID heading into winter is a real possibility. And a vaccine is not a holy grail. This takes us into mid to late 2021 optimistically, before we can start thinking about life after COVID.

Fiscal stimulus brings political uncertainty. Unlike a central bank which can just decide to cut rates unilaterally, fiscal stimulus cannot be passed without going through politicians.

And politicians have their own agenda.

As we’re seeing in the US now, these issues quickly become politicized, and used for personal benefit. And it’s not just the US – EU, Japan, China, will all need to pass fiscal packages to get the world out of this. That’s a lot of moving parts.

So while I like to think we’ll avoid the mistakes of the Great Depression, I do see the possibity of policy mistake here.

A tale of two investing legends

There’s this story I really like – It’s about George Soros and Stanley Druckenmiller, the two legendary investors that broke the Bank of England… and Malaysia.

In 1999, Stan was working for George Soros.

Portfolio managers at the fund could choose to invest their money with Stan or George. At the start, most went with George Soros because of his reputation, and Stan was a distant second.

George Soros was short tech. He thought the Dot Com Bubble was a bubble, and he shorted stocks as they went up. He was losing lots of money.

Stan was long Tech. The Dot Com Bubble was going up, and he was buying stocks all the way up. He made a ton of money.

As 1999 wore on, more and more of the PMs started moving their money from George to Stan. And of course, as the bubble inflated, those PMs who moved made more and more money. So the PMs betting on George had FOMO, and they started coming over to Stan.

In 2000, the bubble burst. The guys who had switched over to Stan lost a ton of money, and they eventually sold at the bottom for 10 to 15 cents on the dollar.

But, and here’s the interesting part – Both Stan and George made money eventually.

Stan continued buying tech stocks as they crashed, and held on to 2007 when he sold his tech stocks for a profit. George lost a lot of money at the start, but once the bubble burst he made massive profits.

The only guys who lost money? The PMs who chased the fad – who were with George at the start, and then shifted to Stan along the way, and sold at the bottom.

What’s the moral of the story?

The lesson here, is that there are many ways to make money even in an irrational market. There is no correct way to make money.

BUT – You need to decide how you want to make money. And then you have to stick with your plan.

What you want to avoid, is fad chasing. You want to avoid chasing the bubble up, and avoid chasing it down. Find a plan, and stick with it.

Today’s market

I think today’s market is very similar.

There’s just so many ways to make money in this market.

You can buy tech and ride the bubble up. You can short tech and ride the bubble down. You can buy cyclicals like oil or banks at dirt cheap prices and ride the reflation. You can short counters like retail or F&B as they go bust. You can buy gold or bitcoin to bet on a fiat depreciation.

All of which can make you money. But you need to find one, and stick with it.

Don’t chase the fad, unless you can get in early.

My Macro View on the global economy

My personal macro view hasn’t changed drastically since March.

I still think the short-term cycle is deflationary in nature. Short term, unemployment will continue going up, and more companies are going to go bust.

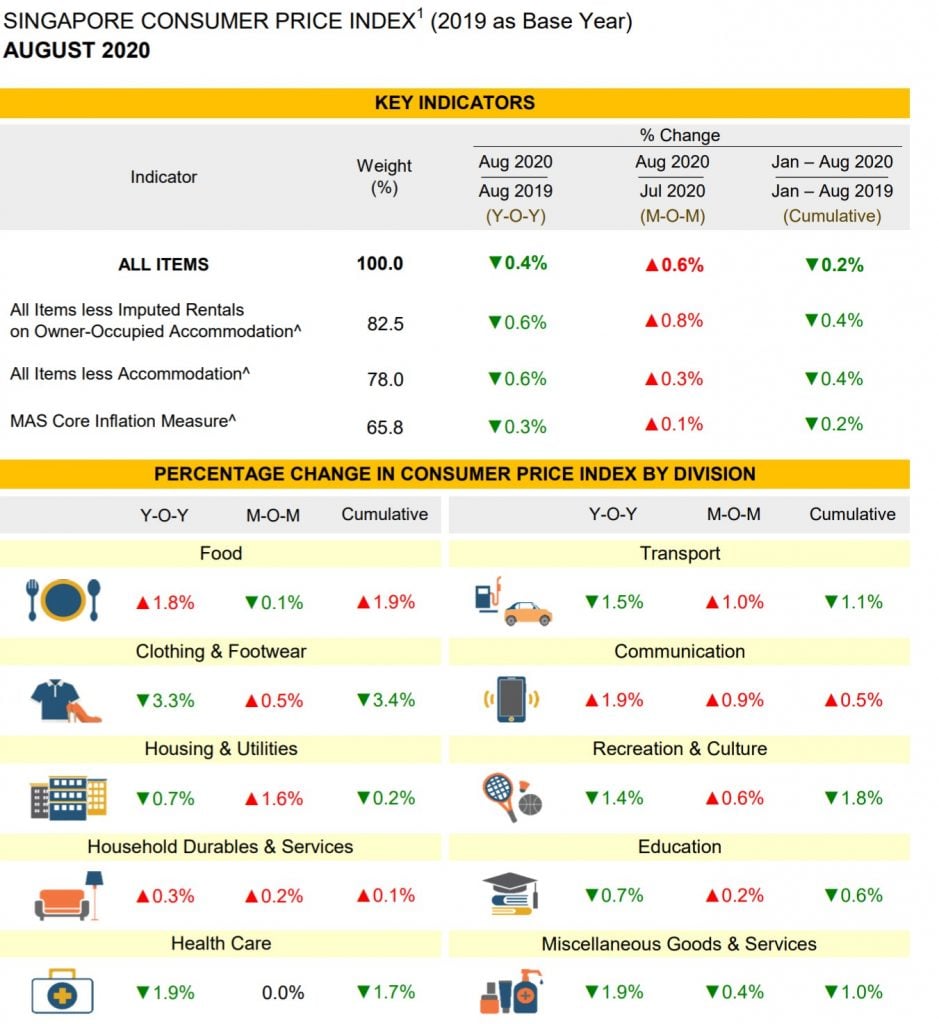

Latest CPI numbers from Singapore also support this view, and point towards deflation:

But I still think the ultimate solution to this crisis is to engineer inflation.

The problem now is that nobody wants to borrow money and invest in production, because they don’t think they can make money running a legit business. Instead, they borrow money and use it to buy a house, or buy stocks. This inflates the asset bubble, but it doesn’t help the real economy.

With inflation, companies incomes will start going up relative to debt levels, so it makes existing debt easier to service. This encourages companies to take up debt to invest in business.

Once this happens, it will start to transition into an inflationary cycle. But the exact timing will depend on how governments and central banks react.

But that’s the big picture. And when you zoom in to the day by day, week by week perspective, there’s just incredible opportunity out here now.

Big money is made and lost in each crisis. Be sure to be on the right side.

Closing Thoughts: Is it time to sell stocks?

So is it time to sell stocks? Really depends on your investment strategy.

If you’re in something like gold, then there may be a short term correction, but the mid term trend should still go up.

If you’re in something like oil or banks, they’re already down 50% or so from highs. Short term they can go lower, but longer term, risk-reward starts looking attractive.

If you’re in Tech, you’re already up big. You can take profits now and hope to buy in if it drops, or you can just hold on for the long term.

So there’s no one size fits all here. It really depends your investments, and your holding power.

As always, this article is written on 25 Sep 2020 and will not be updated going foward. Latest thoughts (and my stock watch and personal portfolio) are available on Patron.

Love to hear your thoughts – Share your comments below!

Support the site as a Patron and get access to my personal stock watch list, as well as my personal portfolio allocation.

Do like and follow our Facebook Page, or join the Telegram Channel. Never miss another post from Financial Horse!

Join our Facebook Group to continue the discussion, everyone is welcome!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Both are THE best quality investment courses available to Singapore investors out there!

Excellent article, FH. Controlling the behaviour is key. Following an asset allocation model acc to ones fin goals is vital.

Just to add – there is enough provisioning done by SG Banks and some REITs. Currently at low P/B they are looking good. Need holding power.

The idea is to look beyond next 1 year.

Hi Amit, thanks for sharing, and yes, I do agree.

The short term is very uncertain, so holding power is important.

There are many ways to make money sure, but there are even more ways to lose it. The important thing to recognize is the distinction between “trading” and “investing”. Most of us with jobs, children and lives away from our computer screens are not going to be successful traders. For investors (not traders), what happens over the next 6, 12 or 18 months to stock prices is irrelevant. What matters is the next 20 or 30 years. If you think stock prices will be higher in 20 years from now, and historical precedent suggests they will be, then why would you sell out?

For retail investors, the best investment advice is to put the same amount of money each month into a broad market, low cost ETF, ignore the endless market commentary and stick with the plan for the long term. Don’t try to pick winners, or rotate sectors or short-sell. Boring maybe, but there is decades of quantitative evidence that it works. Selling out, or trying to time the market, is generally a bad idea. When do you buy back in? What if the market grinds higher in the interim, do you continue to sit on the sidelines and hope for a pull back? How much of a pull back? Shorting tech stocks is even worse advice. Have a read of Reddit to see the number of people who have lost huge sums shorting Tesla and Uber, despite the fact that they are terrible companies to be invested in and will almost certainly be worth substantially less in the years to come.

Over the long run even professional active money managers with huge teams of research analysts, complex modelling software and access to sophisticated instruments can’t consistently beat the market. There is vast amounts of research demonstrating this. Trying to pick winners and time markets is active management, whether we do it as retail investors or professionals. This chart shows how many active managers beat their benchmarks:

https://data.ifa.com/content/charts/345/3420/package/SPIVA_report_Pie%20-9-22-2020-Q2.svg

What makes us as retail investors think we can do better?

Hi Matt, I don’t disagree with you actually. For the bulk of retail investors, I agree that a long term buy and hold strategy would deliver the best returns.

But I also don’t think it’s impossible to beat an index fund for certain types of investors. Just something as simple as adding more money on dips, or buying big say in March, can lead to outperformance.

So it really goes back to the kind of investor one is. Does one want to achieve market returns, or try for something bigger (but risk falling short).

While I agree on the point, here’s a thought: Would you prefer that every investment blog and website only post about monthly dollar cost averaging into a broad market, low cost ETF? Would be pretty boring, wouldn’t it?

Haha great point Zach. In a perverse way, the more people that do that, the easier it becomes to outperform because of market inefficiencies.

Hi FH,

Great article. Lot of food for thought and indeed, I have been wondering if this is the start of a longer term downward trend. On the medical side, while I think cases will inevitably go up in the coming months given the level of spread in Europe and the US, the broader question is whether management of these cases can be done without overwhelming the healthcare systems. There have been significant advances in the treatment of Covid with dexamethasone, remdesivir etc. which have reduced the severity of disease progression and overall mortality so doctors know how to handle this better even without a vaccine.

Agree with what Matt said about overall approach to investing. However, sometimes people do get stock grants etc. from their companies and have to decide whether to sell or hold on. Also, we are also in a new world compared to the last few decades. Given the low yield on US treasuries and the fact it will be unlikely for US rates to go negative, the ability of bonds to act as a stabiliser for equity is much reduced and many are re-assessing the traditional 60-40 split.

I don’t think anyone yet knows how to invest in this new world of prolonged low rates with almost broad every asset class highly valued vs historicals. What has worked in the last few decades may not work for the next few decades. Thus, the more food for thought the better.

Hi CMC,

Agree on the 60/40. We’ve talked about this on the site for a while now, and I genuinely think the bond portion of that portfolio is dead. That was illustrated in March and in the recent declines, that at the zero bound long term treasuries lose their hedging capability. I dont think there’s any asset class that can replace treasuries perfectly, so investors will need to go into things like gold / tail risk hedging, and accept a different risk profile for their portfolios going forward.

And yes – I do think a lot of things will change going forward. Tweaks to the asset allocation will be required, and the best historical precedents will come from the 1940s period (and to a lesser extent 1970s). Treasuries no longer make sense, and interest rates are never going up for the foreseeable future, not even when inflation comes around.

@Zach

It depends whether the blog is offering advice on long term investment decisions or short term trading and speculation. If it’s long term investment, then yes unfortunately, based on decades of evidence, it’s incredible simple and boring, assuming you want to have a chance of building wealth and achieving retirement goals of course. If it’s trading and speculation, which is fine by the way, most of us enjoy a bit of gambling, then it shouldn’t really be presented as investment advice (which is the distinction I drew at the start of my previous post). What retail *investors* need more than anything, and I include myself in this, is clear, evidence based, long term investment education, even if it’s boring.

@Chan Mali Chan

My view is that COVID is a painful short-term shock, and will cause some equally painful societal, economic and political adjustments, but long term it’s just a blip. The disease will become just another of myriad viruses we live with already and, as you say, treatments will improve significantly. Every crisis feels like the end of times, but they rarely are. I imagine WWII was pretty depressing to live through but we survived and prospered.

Your point about the decades ahead is interesting. COVID has coincided with some really significant structural shifts; climate, technology and demographics. From an investment point of view, demographics is the one that worries me the most. Charles Goodhart has a great recent book and a paper on this:

https://www.amazon.com/Great-Demographic-Reversal-Societies-Inequality/dp/3030426564

https://www.bis.org/publ/work656.pdf

Worth a read.

Good point on the long term investing, will take it into account going forward.

I wouldn’t say COVID is just a blip longer term. I’ve found that human history just tends to amble along, and then there are catalysts that spark off profound change in the course of human history. The Battle of Trafalgar for example. American Civil War. WWII. Small events when viewed through the lens of history, but big in the impact they had on the course of human history. COVID looks to be one of this.

FH – this is totally unrelated but why don’t you think of doing an article on SPACs, which have been the recent craze? I think there are great opportunities and the whole concept (with the limited downside) is a good risk-reward play.

That’s an interesting one – which part are you keen on. Do you mean whether SPACs are worth investing in?

Hi FH. I seek your clarification.

Short term, I think the Euro is still way too strong, and a lot of emerging market currencies are still looking very unstable (esp the Turkish Lira). I still think there is a possibility of a dollar strengthening short term, before a midterm collapse. <<<=== Do you mean to say "dollar is still way too strong"?

Sorry but i was a little confused reading this para

Actually I meant the opposite – that dollar is too weak. I think a lot of currencies are too strong vs the dollar short term, and if this keeps up their exports will be impacted. Short term, I think many economies esp the Euro will need to depreciate their currencies vs the dollar.

Could be wrong though. This is the million dollar question – that determines how everything plays out.

Hi Matt, I hear you. And I average in on plenty of ETFs myself. In fact, with the exception of Singapore, most of my exposure into China and US are through quarterly ETF purchases, with a few 1-2% dabbles here and there into specific companies I like, timing the entries with stop losses in place. So I agree with you, really I do.

But here’s the thing: Clearly, you are a person who already know full well about the long proven benefits of dollar cost averaging into ETFs, the advantages of “time in the market” vs “timing the market”, and all those related stuff. But you scour the internet for more, because you want to add value to yourself. All investors do. You want to know more about the geopolitical macro. You want to know which are the new growth sectors and emerging markets out there. You want to know more about the correlation between the dollar index vs precious metals vs the S&P500 vs the upcoming US election. You want to know about the different views on the US-China cold war. You want to level up yourself on such knowledge and THEN you can decide whether to deviate from your decades-proven ETF DCA strategy and dabble into active investing, or not. You want to be informed of things and be able to make your own decision based on your short and long term investment objectives.

Please don’t tell me you want all the investment blogs like Financial Horse and websites like Motley Fool etc to constantly preach about disciplined dollar cost averaging over and over again. I know it’s historically proven and all. I get that. But to be frank I’m completely sick and tired of reading about it all over the internet. I’m sick of reading about something I already know. I don’t need FH to tell me about putting $1000 a month into ETFs for the next 30 years of my life. I want FH to tell me about something I don’t already know. That’s why I’d rather all these blogs offer their insights on stock picking and market timing rather than teach the same things over and over, even if they may or may not be right. This isn’t the only blog I read. I’m old enough to apply my own thinking and judgement to the different views.

Hope you get what I mean. And no, I don’t give a damn if it causes misinformation to the new investors out there. In fact, their loss is my gain. That’s pretty blunt but hey, It’s (mostly) a zero sum game.

I have read numerous books and studies touting the benefits of index investing and I don’t disagree that it is what works best for most people.

However, I don’t think index investing is the silver bullet to all of one’s investment needs. It has its flaws.

If everyone indexes, then there is no price discovery, and the market breaks down.

Most studies/examples focus on the US market. Success has been more limited in countries like Japan, Singapore, China, to name a few.

In markets that are inefficient (eg. Em equities) passive indexing does not work.

For bonds, investing in the index entails heavily weighting the heaviest debtors; not always the wisest choice.

Unintended concentration, eg big tech in s&p 500, big banks in the STI.

Personally I split my portfolio into passive and active. The active part helps to satisfy my “animal spirits” :).

@Matt. Here’s an example of what I mean:

https://blog.seedly.sg/us-presidential-election-us-stocks

Even though I’m a long term investor and not a swing trader, I actually felt insulted having wasted my 2 minutes reading the article. It’s literally just clickbait.

That is a bad article indeed haha.