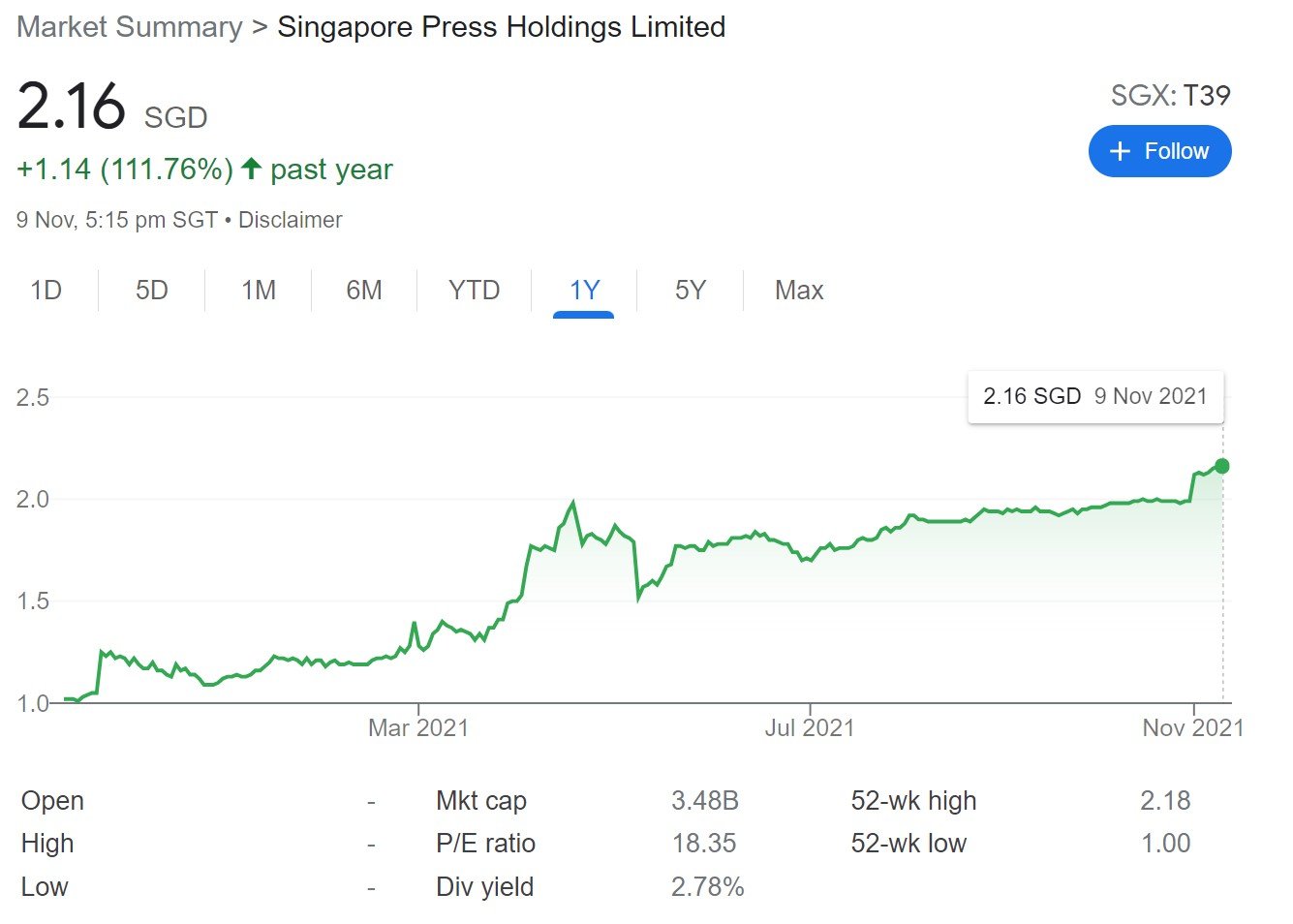

What a difference a year makes!

In that time, SPH has gone from unloved media stock, to the hottest thing since sliced bread.

What is going on? Bidding war for Singapore Press Holdings (SPH)?

For those of you who are new to this saga, a quick recap:

- May 2021 – SPH announced a big restructuring, to spin off their media company at a cost of $110 million (you may remember this as the “Umbrage” event)

- August 2021 – Keppel offers to buyout SPH for $3.4 billion, or $2.099 per share. This is payable with a mix of cash, Keppel REIT units and SPH REIT units.

- October 2021 – A rival consortium swoops in with a $2.10 all cash offer for SPH. This consortium is made up of:

- 40% – Hotel Properties Limited / Ong Beng Seng (Majority Shareholder of HPL)

- 30% – CLA Real Estate Holdings (Temasek Owned but independently managed)

- 30% – Mapletree (Temasek Owned but independently managed)

At the time, we speculated whether Keppel would come back with a new and improved offer.

Well, we have our answer now, and it’s a resounding yes.

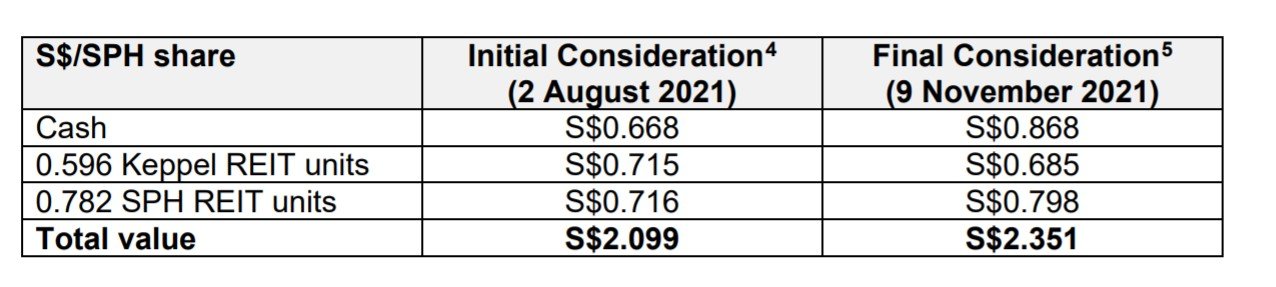

Keppel increases offer for SPH to $2.351 per share

The new offer from Keppel increases the cash component by $0.20.

Based on the latest unit prices of SPH REIT and Keppel REIT, this new offer works out to $2.351 per share of SPH:

There are a couple of important terms to note:

- Revised offer is final and will not be increased – In other words, if the rival consortium comes back with a higher offer than $2.351, they will likely win the deal. Keppel’s offer is final and will not be increased.

- Any competing offer must come in by 16 Nov – Any competing offer must come in by next Tuesday, 16 Nov. This makes sense, because Keppel doesn’t want SPH to go shopping around with their offer. This gives the rival consortium about a week to decide whether to up the offer.

And a couple of other logistics:

- SPH’s EGM to approve the transaction to be held in early Dec (no later than 8 Dec) – Unless there is a competing offer (in which case it must be 21 days after the competing offer)

- Keppel’s EGM to approve the offer to be held no later than one business day before SPH’s EGM

3 Key Takeaways from me on the Keppel SPH offer

3 Key Takeaways from me:

- New Offer for SPH is fair market value

- Will the Rival Consortium outbid Keppel with all cash?

- What is the bigger picture here? Just dollars and cents?

New Offer for SPH is fair market value

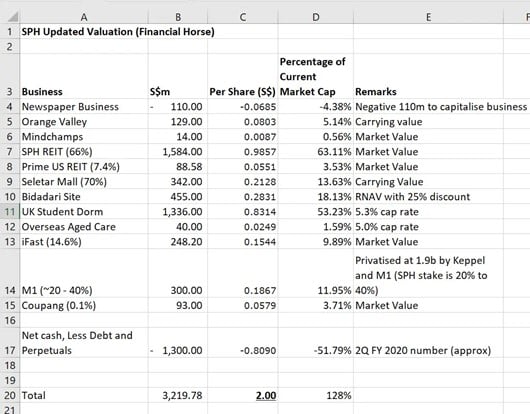

Back in May, I did up a rough sum of the parts analysis for SPH, and my fair value then was $2.00.

I think it’s fair to say that market prices have moved up materially since. I mean just look at stock prices and house prices.

If we add 5% – 10% to the valuation, we get a fair value today of about $2.1 to $2.2.

Throw in a small buyout premium, and the $2.351 offer from Keppel looks very fair.

Before this you could argue that the $2.099 offer was a great deal for Keppel, possibly at the expense of SPH shareholders.

But I think the new revised price reflects fair market value for SPH’s assets today.

If I were a SPH shareholder, I’ll probably take this deal now, it’s a very decent offer.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Will the Rival Consortium outbid Keppel with all cash?

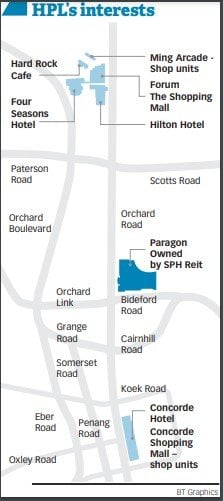

In our previous article, we talked about how the new consortium has better synergies with SPH than Keppel.

Long story short, Hotel Properties Limited can keep the Orchard assets, CLA Real Estate can sell the residential / mixed development assets to CapitaLand, and Mapletree can keep the commercial properties.

And given that it’s a consortium, the financial exposure for each of the 3 players is much lower, reducing their risk.

If they want to, they can easily come back with a $2.35 all cash offer for SPH, which is just a 11.9% increase from their opening bid.

And being an all cash offer, the SPH shareholders will probably pick it to avoid the uncertainty that comes with being paid in SPH REIT and Keppel REIT units.

So the million dollar question is – Will they up the offer?

What is the bigger picture here? Just dollars and cents?

I’ve been thinking and thinking about this SPH buyout deal, and I can’t help but feel I’m missing something here.

Why the need for this bidding war?

Keppel is 20% owned by Temasek.

Entities fully owned by Temasek (indirectly) own 60% of the rival consortium that is trying to outbid Keppel.

Now I get that Keppel, Mapletree, CLA Real Estate are all independently managed and not directed by Temasek.

But again, I can’t help but think there is a bigger picture here I’m missing.

From a valuation point of view, the rival consortium can probably very easily come back with a revised offer and clinch the deal to buy SPH. If they break SPH up for parts, there is real value to realise there.

But is this deal purely about dollars and cents?

Or is there something deeper here?

I can’t quite figure this one out, so I would love to hear your thoughts. What am I missing here? Or am I just overthinking?

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a Free Apple stock (worth S$200) when you open a new account with Tiger Brokers and fund $2000.

Get 1 free Apple share (worth $200) you’re new to MooMoo and fund $2700.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!