What a week it’s been for SPH!

They started the week planning to announce a big strategic restructuring that would turnaround the company.

And they ended it with their share price down 15%, and their CEO going viral for all the wrong reasons.

Look through all that noise though, and beneath the surface is a very interesting deal that I wanted to cover.

Explained: What is SPH Restructuring?

In one sentence – SPH is selling their entire media related business.

And the price they’re selling it at?

-S$110 million.

Yep that’s right. The negative is not a typo.

In a normal M&A you get paid for your assets, in this deal SPH is paying to get rid of the media business.

Don’t worry, I had a double take when I saw this one too, so I can kind of see why the stock sold off 15% yesterday.

Straits Times has a good summary, but the broad steps are:

- SPH will transfer the entire media business into a new subsidiary

- This new subsidiary will be injected with:

- 80m cash,

- 30m of SPH shares and SPH REIT,

- SPH’s stake in 4 of its digital media investors

- New subsidiary will be sold for nominal consideration ($1), to a new Company Limited by Gurantee

What is a Company Limited by Guarantee?

A Company Limited by Guarantee is basically a kind of charitable organisation (not for profit).

This will “allow SPH’s media business to get funding from private and public sources, including extra financial support from the Government”.

Other companies limited by guarantee include the Esplanade and The Arts House.

Sold at Nominal Value?! Plus S$110 million?!

So again, I had a double take at this one.

I mean the media business is not a good one to be in, but with Straits Times, Business Times, Lianhezaobao, AsiaOne etc SPH does own quite of few of the main media sources in Singapore.

With more than 28 million monthly unique visitors across all their sites, according to SPH.

Surely that business is worth something?

But no, under this deal, not only does SPH lose the entire media business, they are also paying $110 million to capitalise SPH Media before they give it away.

BTW – we share commentary on financial markets every week, so do sign up for our mailing list, its absolutely free (goes out every Sunday).

Don’t forget to join our Telegram Channel and Instagram(or YouTube)!

[mailmunch-form id=”928667″]

Why are they doing this?

The official reason from SPH is set out below.

To sum it up – the traditional media business is in trouble, profitability is declining, and running the media business as a listed entity with quarterly reporting is not feasible when you have shareholders to answer to.

Why are they doing this… really?

But this reason doesn’t really make sense.

So I dug a bit deeper, and I noticed they keep referencing the Newspaper and Printing Presses Act (NPPA).

They even have a full slide on this in the presentation:

Under the law, no shareholder can hold more than 5% of a newspaper without approval from the government.

This is to prevent external actors from gaining control of Singapore’s media and influencing popular opinion on this island.

SPH owns a newspaper, so no one can hold more than 5% of SPH without approval from the government.

Once SPH loses the media business, this factor is no longer in play.

Which means that someone can come in and buy up a significant stake in SPH, or even privatise SPH entirely.

In fact the presentation slides keep talking about how this is the “First step in the ongoing strategic review”.

Is the next step to bring on board a strategic investor or a sale of the entire company?

What is SPH left with after the restructuring?

To answer that, we need to know what is left in SPH after this restructuring.

Basically:

- 65% stake in SPH REIT ($1.59b)

- Orange Valley – private nursing home operator

- Seletar mall

- Bidadari development – The Woodleigh Residences and The Woodleigh Mall (50% stake)

- UK and Germany Student Accommodation

- 0.1% of Coupang (S$93m)

The biggest one of course is the 65% stake in SPH REIT. At $1.59 billion, that’s almost 65% of SPH’s current market cap.

It’s quite a diverse portfolio, but there’s actually value in this portfolio.

Options to unlock the value will be to:

Sell it on a portfolio basis – At SPH’s current market cap of $2.45 billion, it’s quite an easy target to be bought out. A guy like Blackrock can come in and buy out a 30% stake, or the entire company.

Break it up for parts – Each of the individual assets could fetch a good price if sold separately too. Sell off the properties, the nursing home, the student accom, and sell Coupang on the open market.

So yeah, if “Phase 2” is a sale or break up of SPH, there could be real value to be unlocked here.

Valuation of SPH

I did a valuation of SPH a few months back, and this was my conclusion then:

I agree with UOB’s valuations of the property business, which is $2.26.

UOB gave the newspaper business a $0 valuation, which to be honest, I don’t think is fair because there still is value there. It is the number one newspaper in Singapore after all, and generates half of the revenue for SPH.

I will use DBS’s $0.16 value of the newspaper business (based on DCF analysis).

Less off the debt, and you get a final sum of the parts valuation of SPH of $1.77

When I valued it then, I assumed the newspaper business had real value ($0.16 per share). Clearly SPH disagrees, so we need to adjust the valuation to take this into account. We need to set the newspaper business value at 0, and also less off the $110 million SPH is paying to get rid of it ($0.16 and $0.068 per share respectively).

Some of the stakes like SPH REIT and the UK student accom have increased in value since, but SPH is also losing some of their leases that will be injected into the new Media business, so they net each other off.

The valuation is quite a complex issue, so I did a follow-up post exploring this:

SPH: What is the true valuation of the stock?

SPH’s own book value

The strange thing though, is that SPH’s own book value of their company is $2.08 per share.

But I couldn’t figure out how they arrived at this final number so I couldn’t examine the assumptions used.

If anyone knows how they arrived at this number do let me know in the comments below.

It’s strange their own tabletop valuation differs so much. Are they booking their value of SPH REIT at book value instead of market price?

Is there value in SPH at this price?

Using SPH’s own book value – SPH is trading at 0.73x book value.

By comparison, a best in class property developer like CapitaLand trades at 0.8x book value.

SPH before the restructuring – an operating company

When I looked at SPH a couple months ago, this was my conclusion:

But as a long term investor, I find it hard to be excited about SPH.

The real estate business is not best in class, so it makes little sense to me when a behemoth like CapitaLand is at a cheaper valuation and has much higher quality properties (Raffles City China, stakes in CICT, Ascendas REIT, etc).

The media business is okay, but it definitely is in secular decline. It will stabilize eventually, but really tough to say when and where.

The answer’s clear for me though, I will not invest in SPH. I just don’t see a place for it in my portfolio.

If I wanted real estate exposure I would go with the REITs / a player like CapitaLand. If I wanted media exposure I would go with Google or Facebook where the future lies.

SPH today – an investment holding company

The SPH of today is a very different proposition.

Subject to shareholder approval, the loss-making media business is gone.

It’s basically a holding company, with property stakes, a nursing home, and some student accom.

The play here is whether SPH can unlock value from the sales of these stakes – either individually or on a portfolio basis.

It’s no longer about SPH as an operating business, trying to turnaround the media arm.

So it all goes back to valuations.

Based on my numbers, SPH is close to book value at current price (post-restructuring).

If you sell the stakes you can probably sell them at a premium. So let’s assume SPH can get a 10-15% premium on their underlying portfolio, then that’s the upside here.

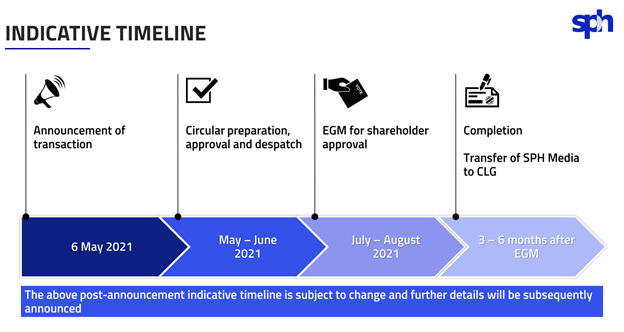

It will take time though. The deal will not be completed until end of 2021.

Even if SPH lines up all the buyers beforehand, the earliest they can move to “Phase 2” is end of the year.

Realistically, it will probably take longer than that.

Why did the market sell off on this news?

Couple of readers have asked why CapitaLand’s share price rose after their restructuring announcement, and why SPH’s plunged.

In CapitaLand’s case, they were privatizing the unwanted development business at a significant premium to what the market was pricing in. So they were unlocking value.

Whereas in SPH’s case they’re actually selling the unwanted media business at a loss.

The equivalent in SPH’s case is if SPH sells their media business for $500 million. Then the share price would rally.

Should investors “take umbrage” at this deal?

Sorry, couldn’t resist.

Full disclosure, I am not a SPH shareholder, so there is no skin in the game for me.

Initial reaction – I didn’t like the deal. Felt like a cop out to me.

There is some truth in all those memes that if you can’t make money from it, just call it non-profit and be done.

Other players like the New York Times and the Guardian and Financial Times have managed to turn around their media business, so it’s not impossible.

Hard yes, but not impossible.

But the more I thought about it, the more I think that there could be value unlock for shareholders here, if “Phase 2” is properly executed.

Of course, that’s a big if, and only time will tell.

Will I buy SPH at this price?

It’s quite an interesting play that all goes back to risk-reward for me.

At current price, I don’t think risk-reward is all that attractive.

But if the price continues to trend downward in the coming months, could be an interesting play to buy in and watch for the “Phase 2” unlocking of value.

I’ll definitely be watching how the share price plays out going forward.

For those who are keen, my full portfolio and stock watch are available on Patron.

Closing Thoughts: Why is everyone privatizing their loss-making business?

Now SPH is not a Temasek linked company, but they’ve been going down the same trend of Temasek companies in privatizing the loss making business.

Started with Keppel, then Sembcorp, CapitaLand, and now SPH is doing the same.

Is this part of a broader trend for Singapore going forward?

Whatever the case, would be interesting to see who is coming up next.

Read Part II of this post: SPH: What is the true valuation of this stock?

Love to hear your thoughts!

As always, this article is written on 8 May 2021 and will not be updated going forward. Latest thoughts (and my stock watch and personal portfolio) are available on Patron.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Both are THE best quality investment courses available to Singapore investors out there!

What will be the yield assuming same payout given that the loss making media business is sold?

Would the discount ascribed be lesser in the event that it is privatised? Would the conglomerate discount be removed and value closer to its market value? Remember most of its assets are operational rather than in development phase and hence it could trade closer to that value.

Yeah very good points FCY.

My current fair value doesn’t apply any conglomerate discount, but I’m definitely being conservative with my numbers, and like some readers pointed out, I didnt include certain stakes like iFast or M1 etc.

So an argument can be made that the true fair value would be even higher.

I think it really goes back to risk-reward. Buying in now is taking up a fairly lengthy holding period + uncertainty over whether the transaction is approved + what is the eventual buyout/privatisation price (if at all). That’s quite a lot of uncertainty, for an unknown upside. If price trends downwards such that upside goes up, or some of the uncertainty is removed, then that would change the analysis in a big way.

But yes – great points, I don’t disagree with you.

Oh….the stake in M1 and iFast are sizeable too which collectively add 30 to 50 cents to its net book value (based on privitisation offer of M1 and iFast current market capitalisation). Maybe there is where the disparity between your valuation and SPH’s net book value of $2.08 per share.

You are right – I have just updated the valuation in this post: https://financialhorse.com/sph-what-is-the-true-valuation-of-this-stock/

New valuation is about $2, which brings it much closer to SPH’s own book value.

Thanks for pointing this out. 🙂

No worries! Hope it has been helpful.

Do you think a CLG can be a successful model for media enterprises like SPH?

Well, depends on what you mean by successful. Quality of content sure. But profit making – the whole idea of the CLG is that it’s no longer profit making. 😉