In this article, I wanted address an idea that’s been gaining stream recently.

It’s the idea that “cash is trash”.

Ray Dalio was the first to coin the term. He said it in 2019, and again in Jan 2020, which looked very silly just 2 months later. But post COVID19, he again reiterated his views that “cash is trash”, and that investors should be holding their money in other asset classes like stocks, gold, real estate etc.

And it’s a view that’s gaining a lot of popularity recently.

I’m seeing a lot of big institutional investors echo it in some form, and even some investors in our Facebook Group share this view.

Yet at the same time, just last week I wrote an article detailing how COVID19 is still in full swing, and there are significant uncertainties that remain for the global economy.

How do we reconcile these views? What is the right balance for retail investors in Singapore?

*Promo* We’re running a huge GE Promo for the REITs MasterClass right now. Sign up now and you also get free 3 months access to the highest tier of Patron (worth $150).

We’ve also added a completely new 2020 Case Study series, where I do detailed case studies on S-REITs as 2020 plays out. We just added a 20 page case study on Mapletree Industrial Trust the past week. Buy now and get lifetime access to the rest of the case studies as they come out! ?

Take your REITs investing to the next level with the MasterClass!

Find out more here.

Basics: Understanding how we got to where we are today (1930 – 2020)

The biggest mistake that I notice beginner investors make is that they look at markets through the lens of a 5 to 10 year period.

I’m not saying that’s wrong, but the way I see it, that’s like trying to predict the weather by looking at things on a daily basis.

Sure, maybe you get the broad trends right. But to really understand how weather works, you need to look at it over the course of many years. Only then, can you observe the 4 seasons, and how it repeats over time.

Market cycles are the same. You get the short term cycles that last maybe 5 to 10 years, and long term cycles that last 50 to 70 years.

So to use the weather analogy, to be able to witness “one full year” with four seasons, you need to be looking at least over a 50 to 70 year period.

So in the course of one’s investing career, you usually only see one, maybe two “seasons” at all.

Because of this, it’s very easy to lose sight of the big picture, and believe that what we’re going through is unique and unprecedented.

But what I’ve learnt is that that’s seldom true. If you look back far enough in history, you’ll find that history always repeats in some form.

And it is my belief that we are nearing the end of the current long term debt cycle, and we’ll see this phase change happen in the coming years, as we transition into a new long term debt cycle. This will result in big volatility in global financial markets, just like it did all throughout history.

Phase 1 – Hard Money

But enough with the hyperbole. Let’s get down to it.

This story starts in 1945.

It’s 1945, and the Allied forces had just won World War II.

They got together at the now infamous Bretton Woods conference (actually took place in 1944 – picture below), to decide what the new global financial system would look like.

The system that they came up with, was this: The USD would become the world’s global reserve currency. This made sense to the allied forces because at the time, the US was the world’s dominant military power (remember this was towards the end of world war 2, and Europe was wrecked by war), it accounted for 50% of the world’s economic production, and it held 2/3rd of the world’s gold.

Under this system, the USD would be the world’s global reserve currency, and the USD would be pegged to gold, at the price of $35 per ounce.

The rest of the allied forces (eg. UK, France etc) would then peg their currency to the value of the USD.

This would go on to be known as the Bretton Woods system, which we’ll call Phase 1.

Exchangeability of Gold

So under Phase 1, gold is the ultimate store of value, and the value of the USD comes from the fact that is has a fixed rate in relation to gold.

Under this system, the total supply of USD cannot grow faster than the gold supply, because the value of a USD is pegged at $35 per ounce of gold. To get more USD, you need more gold. And gold needs to be mined or bought, so you can’t get more gold that easily, and accordingly, you can’t increase money supply easily.

But of course, human nature is human nature, and that didn’t stop the Feds (the US Central Bank – it controls money supply) and the government from trying anyway.

So to be able to increase spending, the Feds printed more USD, and the supply of USD went up relative to the amount of gold the US had.

This meant that using the price of $35 per ounce, there was more USD than the US had gold.

So if everyone holding a USD took it to the bank to exchange it for gold, the bank would run out of gold.

Once shrewd investors realized this, they started buying USD in bulk to exchange for gold, creating a run on the gold.

Eventually the entire system broke down because the US simply didn’t have enough gold relative to dollars, and the USD broke its peg against gold.

Phase I for the USD lasted from Bretton Woods (1940s) up till around the 1970s, when the gold peg broke.

Phase 2 – Fiat Currency

So in a Phase II In this system, USD is not linked to gold. The value of the USD comes from the value that investors give to it.

USD, and not gold, becomes a store of value in itself. It is an artificial construct that market players choose to accord value to, because they perceive it to have value.

In this system, there is also no limit on the amount of new USD that can be created by the central bank.

The central bank can create as much USD as it wants, and investors will continue to hold USD for as long as they believe it to still hold value.

Phase 2 started with the breaking of the gold peg in the 1970s, until where it is today.

Impact of the Phase Change?

The USD is the global reserve currency, so a bulk of the world’s trade, and many other countries had they currencies pegged or linked to the USD in some way.

Accordingly, once the USD peg broke and it depreciated in a big way, this resulted in massive turmoil across financial markets.

The exact details are not so important for this article, but for those who are curious, what essentially happened during the phase change (approx. 1970s to 1985) is that:

- After the breaking of the gold peg, investors lost faith in the USD. They rushed out of the USD into hard assets, or other currencies.

- This created a run out of the USD, causing the USD to depreciate.

- A depreciating USD resulted in soaring domestic inflation, because imports are now more expensive with a weaker USD.

- The Feds (under Paul Volcker) raised interest rates to combat inflation, and interest rates hit almost 17% at one point – which is unimaginable today.

- This eventually succeeded in reversing the capital outflow.

- Capital flowed back into the US, strengthening the USD. Between 1980 to 1985, the USD strengthened almost 50% against the Japanese yen, Deutsche mark, French franc and British pound.

- This was horrible for American exporters, so eventually, the Plaza Accord was struck in 1985 between France, West Germany, Japan, the United States, and the United Kingdom, to depreciate the U.S. dollar.

Again, the full details are not important.

But if there’s one thing you take away from this article, let it be this.

Periods of phase change in the global monetary regime are periods of massive volatility in financial markets.

The USD breaking its peg against gold in the 1970s sparked a decade of turmoil for financial markets, and things only settled down in 1985 after the Plaza Accord, almost 10 years later.

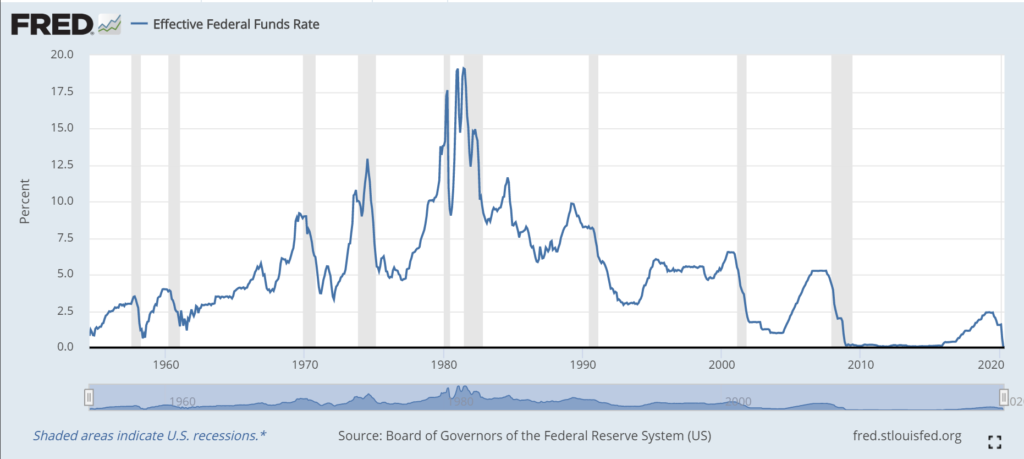

From the table above, you can actually see the 2 phases play out clearly. Phase 1 was a period of rising interest rates that ended in the late 1970/1980s, at which time Phase 2 started and it was a period of falling interest rates, up till where we are today with rates at zero.

The grey shaded areas are recessions, so within the 2 longer term cycles, you can also see each short term cycle play out. Each lasts about 5 to 10 years, ends with higher interest rates and begins with lower interest rates, but individually, none of them break the longer term trend.

What happens next?

My belief is that we are approaching the late stage of Phase 2, and this system will end in the coming years.

It is not possible to predict the exact timing, or what will replace USD fiat currency as reserve status.

But I do believe that COVID19 and the responses to COVID19 have sped up the timeline.

It really goes back to human nature again, as it has all throughout history.

Politicians have 2 choices – Austerity, or Money Printing

In the coming years, politicians are going to be faced with two choices. Do they (1) go into austerity to balance their budgets, or (2) do they stimulate the economy with unlimited amounts of stimulus to return to growth.

And if history is any guide, it may take some time to get there, but in the end, politicians almost always go with option 2.

It’s really a no brainer if you think about it. Why save all that money, and cause a big recession, only to lose your seat in the next elections. When you can spend all that money with reckless abandon, jump start the economy, and win your elections easily – when the only consequences manifest themselves in financial markets over a long term period?

If you look at what governments around the world have done during COVID, from the US to Europe to Japan, it’s quite clear the path they have chosen. The only difference this time was how quick it took to arrive at the conclusion.

Why is this time different?

The difference this time though, is that we’re going to embark on massive money printing and stimulus, just when we are at the later stages of the long term debt cycle.

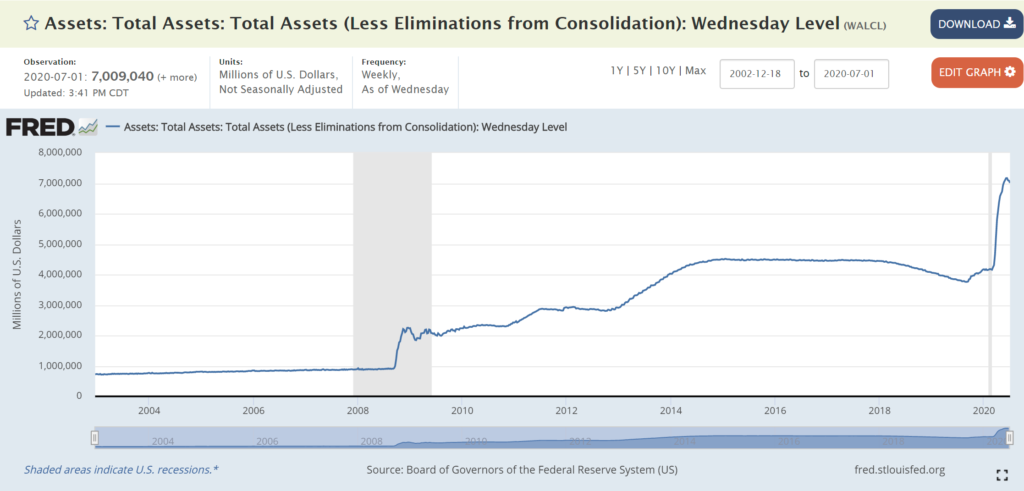

The chart below of the Fed Balance Sheet shows how big the stimulus is.

In 2008, under QE1, the Feds injected about $1 trillion into the economy, that ended the 2008 Financial Crisis. From 2010 to 2015, via QE2 and QE3, the Feds injected another $2 trillion.

So from 2008 to 2015, over the course of 7 years, $3 trillion was injected into the global economy.

And then in March to June 2020, the Feds injected another $3 trillion. Everything that was done over the course of 7 years, was done in 4 months this time.

And we’re barely even getting started. There’s going to be more fiscal stimulus and monetary stimulus coming.

So again, it’s impossible to predict the exact timing of the Phase change. The exact timing depends on how central banks and governements act, and how investors respond, which can’t be predicted with certainty.

But we do know, that we are at the later stages of this cycle, and at some point in time, the Phase change will occur.

It’s really like weather. Some years the summer months may last longer, and we may skip autumn, but winter will come, no doubt about it.

How to invest? What advice does history have?

What is the lesson we can take from the 1970s Phase change?

The lesson from the 1970s, is that in periods of phase change, you want to be invested in hard assets. So things like real estate, gold, commodities, REITs. And of course, stocks with pricing power.

In other words, you want to invest in objects which have intrinsic value, and not where their value is derived in relation to a fiat currency.

So an example of something you do not want to own, is a government bond like the USD. If the USD is going to depreciate, the real value of the USD bond will drop.

What you do want to own, will be things like real estate, where their value comes from the fact that they have intrinsic value.

So… Cash is Trash?

Which brings us back to the original debate – Is Cash trash?

And there are 2 points that I wanted to raise: (1) The currency matters, and (2) The timing matters

(1) The Currency Matters

The currency of your cash matters… a lot.

If you’re holding the Brazilian Real, or the Turkish Lira, I would say absolutely, cash is trash.

You want to hold anything but your local currency. Gold, USD, real estate, stocks, commodities, anything beats holding cash.

But what if you’re a Singaporean investor, and your domestic currency is SGD?

Now the SGD is a very well managed currency. Singapore has historically been very prudent about its management of the SGD, with hefty reserves to back it up, to the point where the SGD almost has a safe haven status. In some ways, it is the Swiss Franc of South East Asia.

So when the currency is SGD, I think the cash is trash argument is less compelling.

Cash is trash, but some cash is less trash than others.

(2) The Timing Matters

Which brings me to my next point – Timing matters.

In my March and April articles, I talked about how we were in the liquidity phase of the COVID crisis, and we would eventually move into the insolvency phase.

With the number of new bankruptcies we see each day, we’re probably getting there soon.

And the key about the insolvency phase, is that it is deflationary in nature, not inflationary.

So on one hand we have the titanic force of the long term debt cycle that will end in the coming years, and would likely be inflationary.

And on the other hand we have the equally titanic force of the greatest recession since the Great Depression that will play out over the next few months, which should be deflationary.

Which force will win is anyone’s guess.

But a healthy dose of respect for both is warranted.

Closing Thoughts: Where do I stand in this debate – Cash is Trash?

My personal thinking, is that we need to be both tactical, and strategic as we play this game.

Tactical to recognize that the short-term pressure from COVID is broadly deflationary, but inflationary in some areas (eg. Food and essentials).

Strategic to recognize that the long term pressure is inflationary due to the Phase Change in the long term debt cycle.

And wise enough to know that we’ll never be able to predict with exact certainty when the short term switches into the long term.

Which is why now more than ever, I think a balanced All-Weather style portfolio makes a lot of sense. Holding all cash is not ideal because of what governments and central banks are likely to do going forward. Holding all stocks / REITs and risk assets is not idea because short term, there’s still big uncertainty from COVID.

What you really want, is something that gives you allocation to all broad asset classes, so you’re protected against whatever may happen next.

Once you get the fundamentals right, you can then decide how much risk you want to add on. And you can then tilt your allocation towards stocks / REITs accordingly based on your risk appetite. Or towards a more defensive allocation.

But this has to be an individual decision. You need to decide how much risk works for you. Is the goal here capital gains, or capital preservation?

I’ve found what works for me – And for those who are keen, my personal portfolio allocation (and stock watchlist) is available on Patron.

Find what works for you.

If you’re out of ideas, the REITs MasterClass is on promo now and it teaches you about asset allocation, and how to pick REITs to assemble a REIT and real estate portfolio. It’s really one of the best REIT courses out there, so do check it out if you’re interest.

I would really love to hear from you guys though. Share your comments below!

*Promo* We’re running a huge GE Promo for the REITs MasterClass right now. Sign up now and you also get free 3 months access to the highest tier of Patron (worth $150).

We’ve also added a completely new 2020 Case Study series, where I do detailed case studies on S-REITs as 2020 plays out. We just added a 20 page case study on Mapletree Industrial Trust the past week. Buy now and get lifetime access to the rest of the case studies as they come out! ?

Take your REITs investing to the next level with the MasterClass!

Find out more here.

Really like the overview of the financial system that leads us to where we are.

One question: throughout this tussle, have-nots is going to suffer massively. Do you think that play into the narrative of libertarianism resulting in the advent of digital assets?

I do agree that inequality will go up as a result of the central bank / govt policies. And I think this increasing wealth gap will spill over into civil unrest. We’ll see more chaos going forward, but exactly how that plays out in terms of digital assets is really tough to predict. I do think digital assets will eventually gain widespread acceptance (already has in certain markets like China), but whether COVID is the tipping point is tough to say.

Thank you for a great review that lay out the possible scenarios. I agree it can go either way. My view is that the unprecedented financial excesses of the last 20 years has resulted in an unprecedented huge debt bubble. There will be a Great Default which can only be deflationary. Central Banks will have no chance to reflate by printing without a raise in interest rate which would add to the deflationary pressures. Personally I would weight my portfolio more towards deflation rather than inflation for the medium to longer term (3 years and beyond).