I was planning to write on Singtel this week.

But after the articles on ST Engineering, Keppel, and Sembcorp, I figured let’s take a break from the TLCs.

Let’s cover a topic that a lot of you have been asking for, and that I’ve been dying to do a deep dive.

Electric Vehicles – and Tesla.

Let’s go!

Basics: Are Electric Vehicles (EV) the future?

70 million cars were sold in 2020.

Of that 70 million – 97% were traditional, internal combustion engine (ICE) vehicles.

The kind where you pump petrol in, and the car moves forward. Fundamentally, the technology has been around for 100 years.

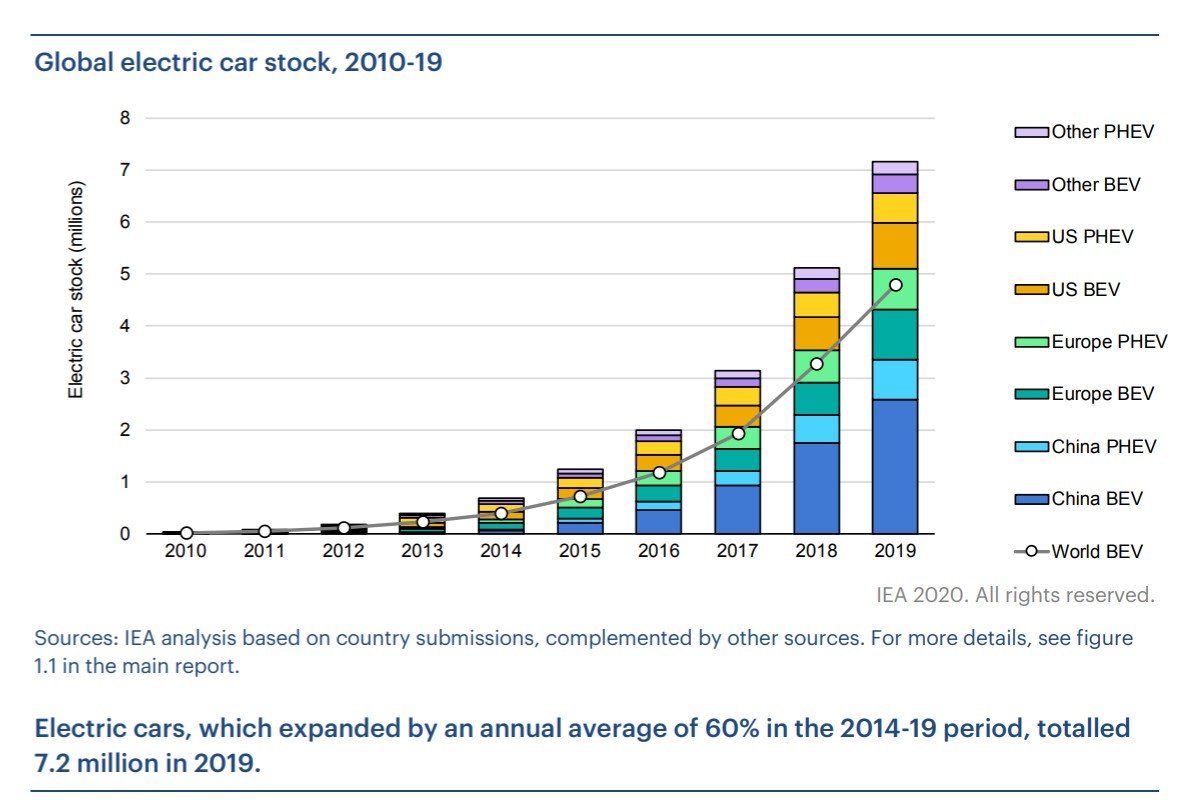

But the world is now moving towards electric vehicles.

The biggest reason is environmental.

A traditional ICE car converts about 17% of the fuel into energy, while an electric vehicle can go up to 50%.

And with an electric vehicle, you connect it to the mains to charge, so if the power grid runs on renewables, it can be pretty environmentally friendly.

What is required for EVs to take off?

To go to full electric vehicles, there are 3 big areas that need to be addressed:

- Regulatory – Subsidies for EV, emphasis in phasing out traditional vehicles

- Infrastructure – Charging points, and lots of them, all around the country

- Technology – Split into 2 big elements:

- Price – needs to be brought down to be competitive with traditional ICE cars

- Range – range needs to be brought up to be on par with traditional cars (500-600km, 350 miles per charge)

Why is making an Electric Vehicle so hard?

As it turns out, making Electric Vehicles is very hard.

Like with any new technology, it takes years and years to perfect the technology and manufacturing technique.

For an EV manufacturer, there are 3 big areas to focus on:

- Battery

- Manufacturing Technique

- Technology

BTW – we share commentary on financial markets every week, so do sign up for our mailing list, its absolutely free (goes out every Sunday).

Don’t forget to join our Telegram Channel and Instagram or (YouTube)!

[mc4wp_form id=”173″]

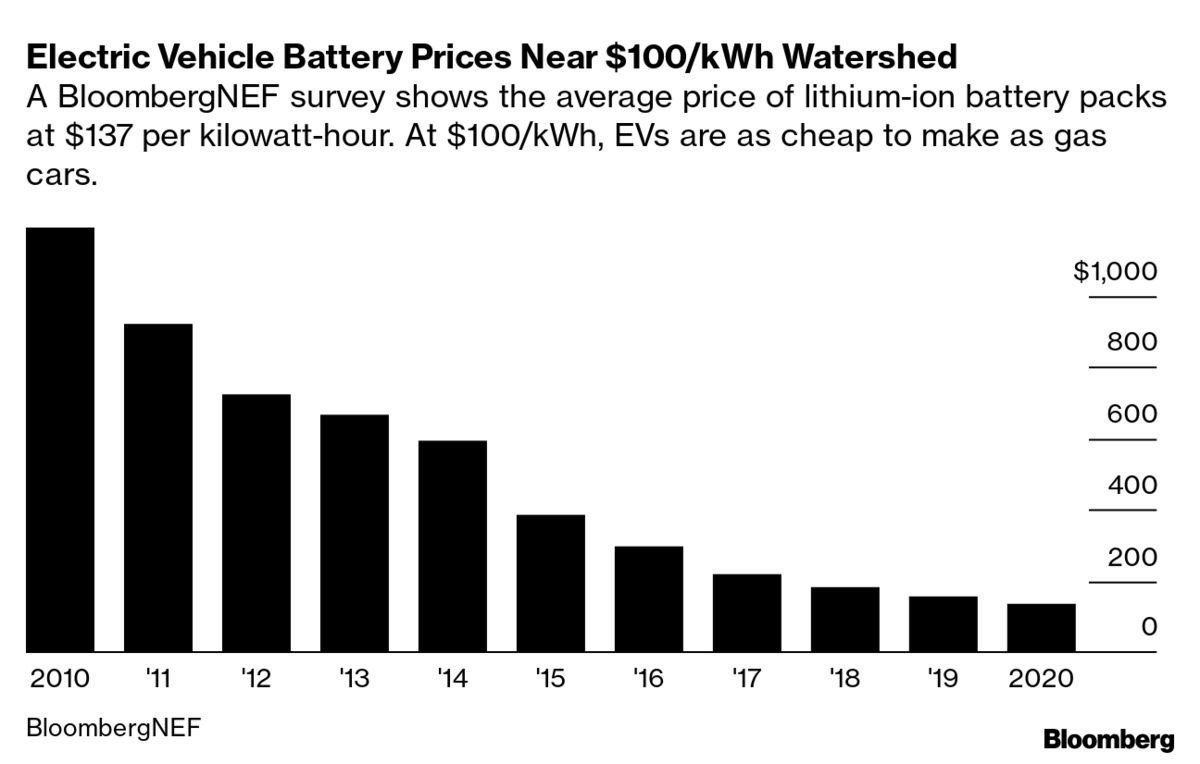

Battery

The battery is the single largest cost of making an EV, coming in at c.30%.

For a Tesla Model 3 that costs $40,000, $10,000 of that would be the cost of the battery.

The good news, is that battery prices have been falling consistently:

It’s a classic S-curve here.

The technology starts out slow, then it hits a point where there is exponential growth, and before you know it’s cheaper than petrol cars.

Battery technology is a whole topic in itself.

For now, what you need to know is that even the best players like Tesla are unable to manufacture their own battery packs (buys from Panasonic).

Most of the best battery manufacturers are Asian companies, and securing a long term supply contract to buy at (1) a good price (2) good capacity, and (3) securing the supply is itself a competitive advantage.

Manufacturing

A traditional car has about 30,000 parts, and assembling that into 1 car is not easy.

It’s why Toyota came up with lean manufacturing, which is now studied by MBAs the world over.

With Electric Vehicles – the complexity of the vehicle is fundamentally reduced.

At its core, there’s really only a few parts:

- Chassis

- Battery

- Electric Motor

- Onboard computer

The Internal Combustion Engine with its 10,000 parts, and the entire gearbox, are all thrown out the window.

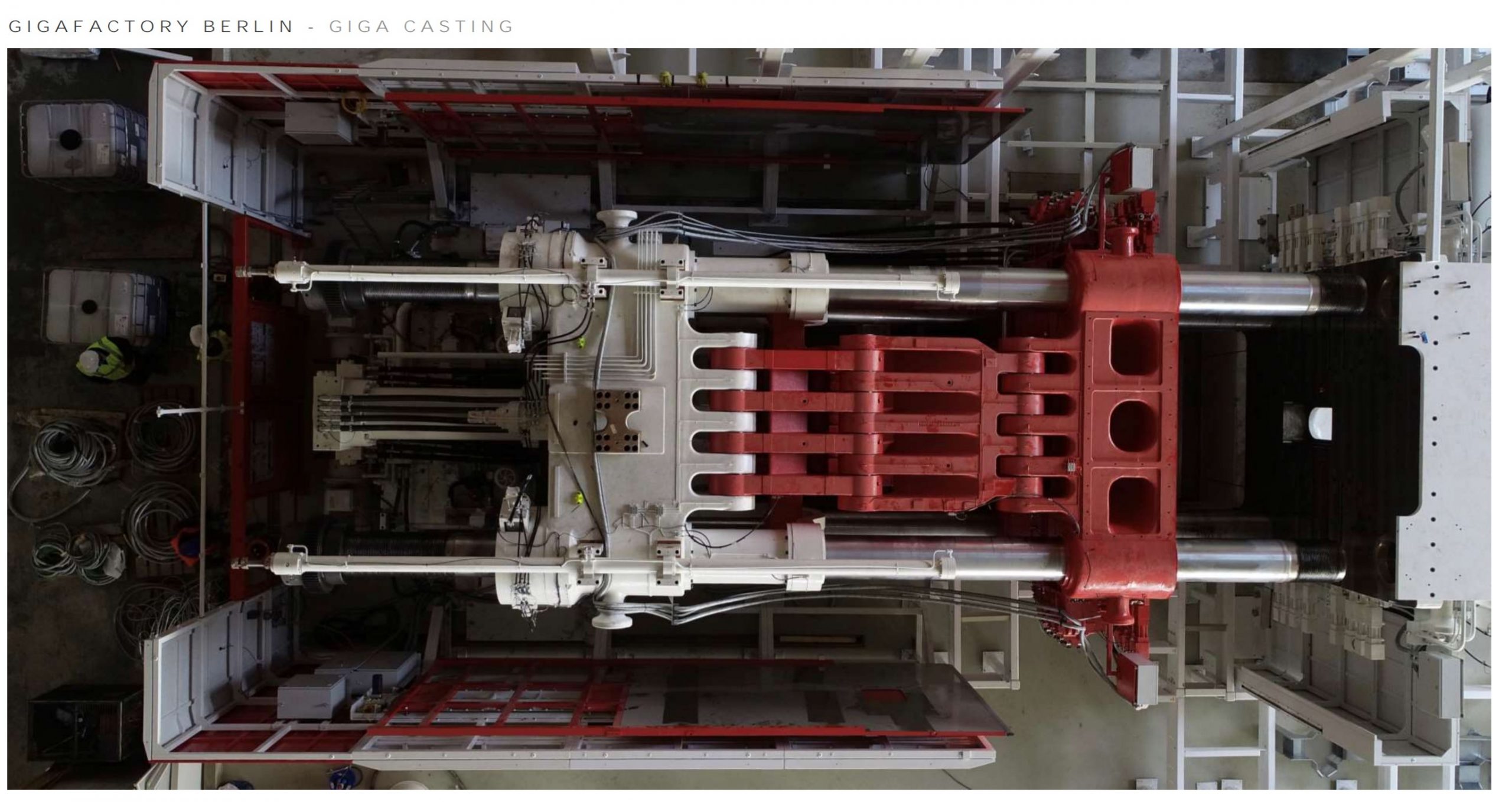

For revolutionary problem solvers like Elon Musk, this offers an opportunity to relook manufacturing from first principles.

Which is why Tesla uses stuff like the Gigapress – which builds the entire Chasis in 1 go to cut costs and production time.

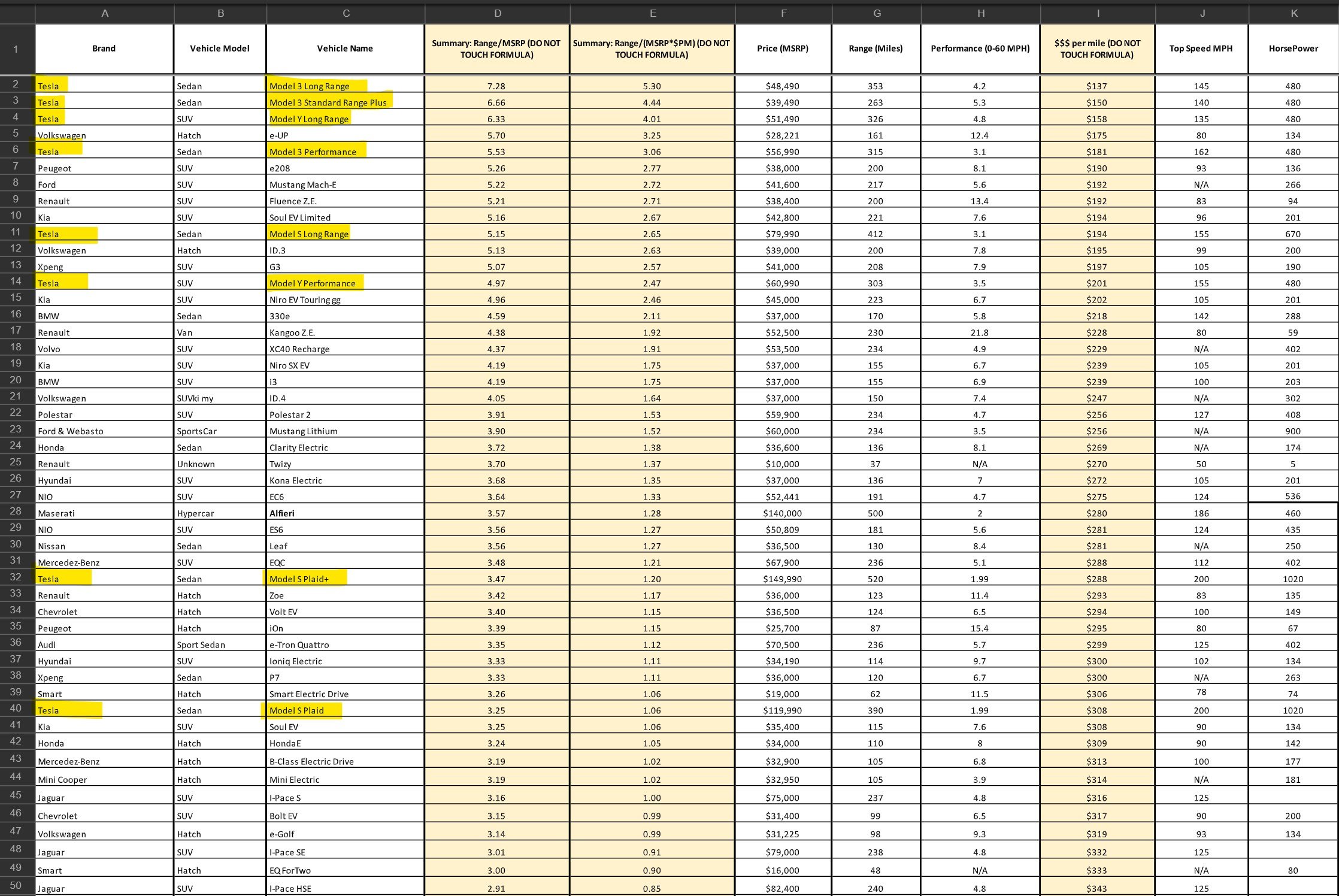

Technology – Range + Fuel Economy

The 2 big categories are range + fuel economy.

I’ve set out range and fuel economy numbers below, with the Teslas highlighted in yellow.

As you can see – Tesla is leading the pack.

Self Driving

Self-driving for now is still being perfected.

It turns out self-driving is a lot harder than expected – because the fringe cases are hard for computers to solve. Think of a balloon floating across the road, does the car brake?

So we may need a few more years before we see widespread adoption.

Once it does though – it will revolutionise travel.

Think about a fleet of self-driving Ubers in every city, driving 24/7. It’s how you make ride-hailing a profitable business.

Is Tesla the best EV maker?

No article on Electric Vehicles will be complete without a discussion on Tesla.

Elon was investing in Tesla since 2004, when traditional automakers thought of EVs as toy cars. Who’s laughing now?

How good is Tesla’s Technology?

Tesla has effectively had a 10-year runway to focus on perfecting EVs while everyone else was working on Internal Combustion Engines.

In technology – that 10 years usually translates into a big lead.

Now I’m not an engineer by any means, but as I was doing my research, some of the leads that jumped out at me:

- Battery – bigger capacity

- 2 Engines – Electronic coordination between the 2 engines creates better acceleration and efficiency

- Manufacturing – Gigapress manufactures the entire chassis at one go

- Self Driving – software and GPU used are years ahead of the competition

- Software – Fully electronic car allows for performance updates to be rolled out over the air (OTA) just like an iPhone update

From Bloomberg:

Tesla’s FSD computer, which to date is still not capable of ‘Fully Self Driving’, claims a compute performance of 144 trillion operations per second, a significant increase from their use of NVIDIA’s Drive PX2 in the previous version of Tesla’s compute solution.

Tesla’s new FSD computer has capabilities that have dumbfounded the other auto manufacturers to the degree that they aren’t really sure what to do. A Nikkei tear-down of the Tesla Model 3 found that Tesla’s electronics are 6 years ahead of the #1 and #2 car manufacturers in the world, Toyota and VW.

They even said an engineer at a major Japanese auto manufacturer was stunned, saying that, “we cannot do it.” This puts many of Tesla’s competitors at a significant disadvantage in terms of keeping up with the company’s capabilities and how close they could be to fully autonomous driving capability. With Tesla already putting the hurt on them last year, the near future doesn’t look bright for them unless they adapt, quickly.

From the Nikkei:

Most parts inside the Model 3 do not bear the name of a supplier. Instead, many have the Tesla logo, including the substrates inside the ECUs. This suggests the company maintains tight control over the development of almost all key technologies in the car.

And with this hardware in place, Teslas can evolve through “over the air” software updates. Right now, the vehicles are still classified as Level 2 or “partially autonomous” cars. But Musk has stressed that they have all the necessary components — “computer and otherwise” — for full self-driving.

From software to electric drive systems, Tesla is steadily bringing more development tasks in-house. If this strategy succeeds, competitors will have little choice but to follow suit, upending their old business models and supply chains as they try to overcome Tesla’s head start.

Now I have little doubt that the other EV makers will catch up eventually. If they throw enough money at the problem and spend enough time on it, they will catch up.

The question is timing.

My sensing based on what I read, is that Tesla is probably 3 to 5 years ahead of the competition.

They may be more ahead in some like self-driving, and less ahead in others like battery which are bought from a third party.

Total Addressable Market for EVs

Let’s run a simple thought experiment to see – If Tesla executes flawlessly over the next 10 years, and becomes the Apple of EVs, what does valuation look like.

So there are 70 million cars sold a year.

Let’s say in 2030, all cars sold are Electric, and Tesla has 30% market share (and Elon Musk is recognised as Steve Jobs II).

That’s 21 million cars sold by Tesla a year.

If we assume average selling price of $40,000, that’s $840 billion revenue.

Let’s assume long term margins of 7% (average for most car manufacturers today, Tesla today is at 3%) – that’s $58 billion profit a year.

If we apply a 20 times P/E, that’s a $1.1 trillion valuation for Tesla, in 2030.

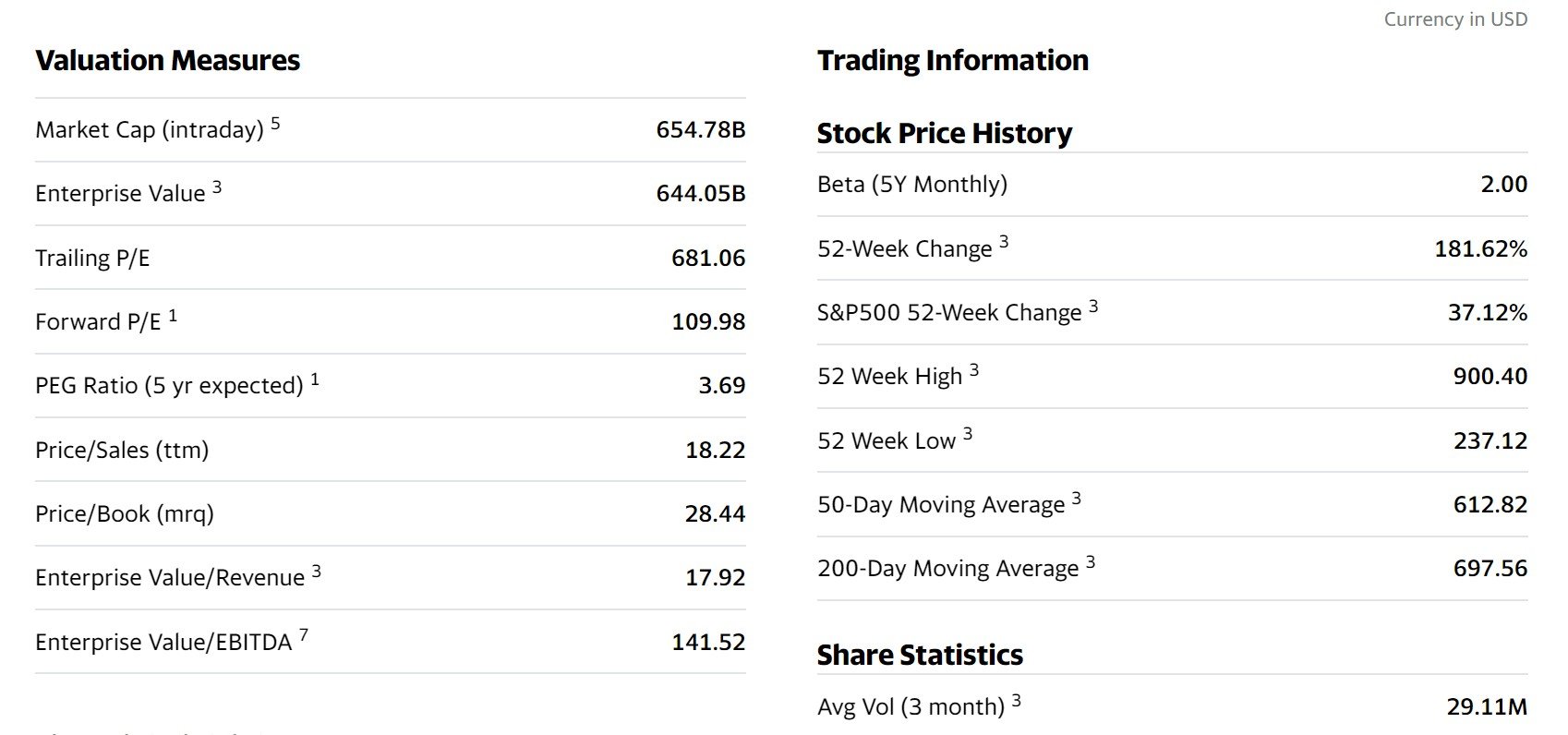

At Tesla’s market cap of $650 billion today, that’s a 70% upside.

What does this mean?

This really surprised me, because it shows that current valuations for Tesla are very aggressive.

We’re assuming Tesla has 30% market share of the entire EV market, and that only translates into a 70% upside.

Even Apple today only has 19% market share in smartphones.

Which means that the key for Tesla to justify its valuation, is to be able to increase its margins.

On the hardware front – it needs to focus on drastically reducing production costs, while increasing supply capacity.

And it needs to be less a hardware player, and more of a software / network provider.

A fleet of robo-tesla, paid upgrades to car firmware, Car as a service, things like that.

And Elon being Elon, I wouldn’t rule it out.

Capex requirements are brutal

There’s a cute story I heard from a VC a while back.

The story is like this – if you have $1 billion to invest in the EV industry, how do you do it?

With software companies – you’ll split it up, and invest $100 million into 10 different companies. You hope that one becomes the next Google.

With EV – you take than $1 billion, and give it to one guy.

The reason why, is because the capex requirements in the EV industry are ridiculous.

The EV makers burn through cash like crazy.

And having more money is itself a competitive advantage

By giving $1 billion to 1 guy, you actually raise his chances of succeeding. Whereas if you give $500 million to 2 guys, both may fail because the $500 million wasn’t enough.

Elon Musk the Visionary Fundraiser

I suppose that’s the advantage of having Elon as your CEO.

Love him or hate him, public markets hang on his every tweet, and this guy can raise money easily.

In the world of EVs where the capex costs are brutal, that is a huge advantage in itself.

And after the $420 take private “joke” nobody really dares to short Tesla in size anymore.

What about the competition?

There’s a whole list of competitors just chomping at the bit:

- Nio

- Xpeng

- BYD

- Volkswagen

- Volvo

- Porsche

But it really turns out that manufacturing EVs is not an easy task, and many of them are running into difficulties.

Porsche recently recalled their flagship Porsche Taycan because of a software issue that could cause a complete power loss. And they also had to drop their range to 200 miles per charge, versus about 300+ for a Tesla.

My take on the EV industry

I see the EV industry today as similar to the car industry in 1920s.

Back then – it was fairly obvious to everyone that cars were the future.

100s of car companies sprang up, but very few survived.

The ones that survived, didn’t necessarily make a lot of money, because the competition and capex was so intense.

There are some industries that are destined to changed the world, but may not necessarily be a good investment.

It’s very tough to call how the EV industry will play out in the coming years.

The technology is evolving very quick, and there are a lot of players in this space.

If I were to make a bet though, it would probably be on Tesla.

I see their technology as being years ahead of the competition, and in Elon Musk they have a brilliant innovator able to solve problems from first principles – a vital skill when breaking into completely new technology.

Oh, and he can manipulate the stock price with a single tweet too.

Play Tesla via Call Options?

Interestingly, one way to play Tesla might be via long-dated call options.

You get exposure to the upside, but you cap your downside.

Could be a great way to play this kind of speculative industries where risk-reward is skewed.

If Tesla succeeds, the share price is going up a lot. If they don’t, it’s going down, a lot.

Closing Thoughts: Kicking myself for missing Tesla

After this article, I am absolutely kicking myself for missing out on the entire Tesla / EV trade.

I’ve never really done a deep dive into EVs, and I always dismissed Tesla as being overvalued.

I remember looking at Nio at $2 in 2019 and deciding to pass because I didn’t know enough about the industry (it’s at $50 now).

Better late than never though.

Having done this deep dive, I kind of get it now. The total addressable market is massive, and the growth that lies ahead is ridiculous. And there are real technological challenges to solve, which creates a good moat.

But EV stocks have gone on a massive runup, and where we stand today, I’m not so sure about risk-reward.

Short term the Feds are determined to start draining the emergency liquidity, and that will start to impact valuations going forward.

I do want some exposure, but buying in now may not be the best idea.

Perhaps some call options or a small position to average in. Haven’t made up my mind yet.

Whether you are a longtime tesla investor, or you love your gas guzzling Ferrari – I want to hear your thoughts! Who will dominate the EV industry? What’s the best way to invest?

As always, this article is written on 3 July 2021 and will not be updated going forward. Latest thoughts (and my stock watch and personal portfolio) are available on Patron.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Both are THE best quality investment courses available to Singapore investors out there!

Hi FH,

Interesting article. I am not sure if the 70M vehicles number you quoted is for advanced economies or for the entire world but the assumption of 100% electric vehicles by 2030 is very aggressive if it is the entire world.

– only advanced economies and even then only a select group of them will be able to build out the charging infrastructure required to support widespread use of fully electric vehicles in the next 9 years. For the rest of the countries, it is highly doubtful that they would be selling 100% electric vehicles.

– the average price of 40K per vehicle at today’s prices is really at the luxury end of normal markets (exclude outlier of Singapore) and it will limit take up. Of course, their production costs will likely fall as batteries get cheaper and so they may also price cheaper in future but it remains to be seen how their margins evolve.

Net net, Tesla is priced for perfection now and if you correct your calculations for the above points, it will look that much riskier.

Hi CMC – sorry I forgot to clarify in the article, the 70m and 30% market share was an optimistic best case scenario.

I wanted to understand if Tesla executes flawlessly, goes on to become the Apple of EV, what would their valuation be in 2030? And the fact that it wasn’t all that big an upside surprised me – I expected a 5x return easily. And that gave me pause.

So yes, I agree with you that valuations look stretched now.

What is tricky I would say, is that with tech sometimes the network effects just get out of whack. For example if Tesla has full self-driving, and you can buy a tesla and have it plugged into the Uber network to earn money for you while you sleep – would that fundamentallly shift Tesla’s valuations? When their tech is this far ahead, and they have a founder like Elon, we shouldn’t discount such possibilities.

The equivalent is to value Amazon in 2010 without taking into account AWS. Sure, valuations are stretched, but then the team went on to build a revolutionary product riding on existing success. I could see the same thing here.

Which is why call options could be a good way to play this – getting exposure to the upside, but capping downside.

But for now, I have no position, and havent decided how I want to play this.

don’t forget about the solar business. Tesla has multiple streams of revenue besides just car sales.

Interesting – do you see solar growing to become a significant part of the business over time?

only if the solar-battery technology/business model is revolutionary; 1_battery material mining/disposal become trully environmental/cost friendly. 2_selling decentralised energy is widely adopted by policy makers

But technologically – does Tesla has a big enough lead in solar/battery? My understanding was that solar is a pretty commoditized product, lots of cheap Asian manufacturers. And battery is battery, Tesla doesn’t manufacture the Li-ion themselves too.

Great article. I agree that Tesla valuation is stretched. I suspect that the current investors is betting that Tesla becomes the Intel+Microsoft of cars. If Tesla is a few years ahead of the rest, they will be better off licensing their technology to other companies (including Uber and car companies). Tesla is not leader in Autonomous yet, Google’s Waymo is, but Tesla do not use Lidar, so it is very cost effective. It will be interesting to see if Tesla can maintain their EV technology lead.

Yes that’s a great point. This is definitely one potential business model.

Elon being Elon, I suspect he’ll want to go at it himself and continue making breakthroughts though. But perhaps that’s exactly the appeal of investing in Elon. 😀

what are your thoughts on comparing tesla to apple in terms of back when it first launched iPhones? Both are disruptive technologies to revolutionize an everyday item and similar in aspect, putting a computer into an everyday item and ramping up the battery capacity massively. Would you invest in Tesla given its valuations now, if you expect it to follow a similar trajectory to Apple when it first started mass producing iDevices?

If Tesla becomes Apple – Absolutely I think Tesla is a buy. With this kind of tech ecosystem + network effects, I think we are more likely to underestimate rather than overestimate the true upside and ways that it can change the world.

But of course, there are real execution issues and uncertainties that lie ahead, which is why the valuation is not already 1-2t. 😀

No love for my boy Peter Rawlinson from Lucid? I see them as the only viable competitor to Tesla in the US, and I’d say the stock price has much more upside than Tesla given they’ll only start delivering vehicles this year.

Interesting – quite a few readers have brought up Lucid. Will take a look. 🙂

Hmm… 70% upside over 9 years in most optimistic scenarii does not give you exactly a great CAGR, in my opinion. An additional risk is the “key person” with Elon Musk; he’s not exactly a triathlon athlete. I surfed TSLA a short while, left with a 3x. The only one I keep for the long term is BYD – mix of big track record in electrification, protected market in China, expansion, Shenzhen culture…

Yeah I agree on the upside point. This was valuing it as a old world, earnings based stock though.

If investors look at it as a cloud/network play, with high margins, a much higher valuation is definitely possible. That might be the emphasis going forward – and with Elon at the helm, can’t rule it out. Fleet of Robo-Teslas plugged into Uber, subscription based cars, performance tuning via subscription service etc.

BYD is interesting, will take a closer look as well. China’s EV market has a lot of potential.