So… Keppel and Sembcorp Marine both called for trading halts this morning.

That’s when you know something big is brewing, and boy was it big.

Keppel Corp and Sembcorp Marine: What is going on?

To sum it up in 1 sentence: Keppel Offshore & Marine (O&M) and Sembcorp Marine will merge into 1 entity, which will be separately listed on the SGX.

Oh, and Sembcorp Marine is doing a massive $1.5 billion rights issue.

Keppel Offshore & Marine and Sembcorp Marine Merger

The details:

- Keppel O&M and Sembcorp Marine to merge into 1 entity (let’s call it X)

- X will be listed as a separate entity on the SGX

- Keppel Corp will receive shares in X (not decided whether this will be distributed to Keppel shareholders or held by Keppel directly)

- Sembcorp Marine shareholders will receive shares in X to replace their existing shares in Sembcorp Marine

- X will enter into a 50-50 JV with Keppel for future marine work

Keppel’s legacy rigs will be sold to a separate Asset Co, that will not be part of X.

We’re still at the discussion stage now, and pricing has not been finalised, so this will take many months to complete.

The full press release is here, and I extracted some key highlights below for your reading pleasure.

Keppel Corporation Limited and Sembcorp Marine Ltd have entered today into a non-binding memorandum of understanding (“MOU”) to enter into exclusive negotiations with a view to combining Keppel O&M and Sembcorp Marine (“Combined Entity”).

- Combined Entity better placed to compete for larger contracts and to pursue synergies arising from combined scale, footprint and capabilities

- Opportunity to accelerate pivot to the energy transition, including offshore renewables, while capitalizing on gas and other production facilities

- Keppel O&M’s legacy rigs and associated receivables will be sold to a separate Asset Co that would be majority owned by external investors, and omitted from the Combined Entity

- Combination would allow companies to bring together their best talent, engineering skills and know-how

- Keppel O&M and Sembcorp Marine to engage with workplace unions, to address labour considerations for the Combined Entity, and to continue to attract and retain O&M engineering talent

Sembcorp Marine $1.5 billion Rights Issue

At the same time, Sembcorp Marine is doing a massive $1.5 billion rights issue.

For every 2 shares in Sembcorp Marine, shareholders get 3 rights at $0.08 (versus market price of $0.19).

It’s a very big and dilutive rights issue (current market cap is $2.39b vs $1.5b raised – 60% capital call!), so it’s a tricky one for Sembcorp Marine shareholders.

The entire rights issue is underwritten by Temasek and DBS.

Press release here, key highlights extracted below again:

(1) Sembcorp Marine Proposes a Further S$1.5 Billion Rights Issue to Strengthen Financial Position Amid Continuing COVID-19 Disruptions

- S$1.5 billion fully committed Rights Issue will strengthen Sembcorp Marine’s financial position and accelerate its strategic pivot towards renewable and clean energy

- Recapitalisation will de-lever Sembcorp Marine and address temporary working capital depletion

- 3 renounceable Rights Shares for every 2 existing shares held at a Rights Issue price of S$0.08 per share, representing a 35.7% discount to TERP 1

- Startree Investments Pte. Ltd., a wholly owned subsidiary of Temasek, has committed to subscribe for its pro-rata 42.6% entitlement and excess rights such that its total subscription will be up to 67.0% of the Rights Issue; DBS is underwriting the remaining 33.0% of the Rights Issue

- Separately, Sembcorp Marine and Keppel Corporation have entered into a non-binding memorandum of understanding to explore a potential combination of Sembcorp Marine and Keppel Offshore & Marine

What does this mean?

To fully appreciate this deal, we need to go back to October 2019.

Phase 0 – Temasek’s takeover bid of Keppel

In October 2019, Temasek launched a S$4.1 billion bid to take control of Keppel Corp.

Before this, Temasek already owned 20.5% of Keppel Corp.

If the takeover was successful, Keppel would hold 51% of Keppel Corp. This majority stake would given them lots of control over the future direction of Keppel Corp.

Of course, COVID happened, and Temasek pulled out of the deal, causing Keppel’s share price to crash.

Because of M&A rules, Temasek was prohibited from coming back with a new offer within 12 months, without regulatory consent.

This was what I wrote back in Sept 2020:

What will happen?

A lot of people are expecting Temasek to come back with a revised offer.

Again, I could be wrong here, but I don’t think this is as likely as what people are expecting.

I think more likely if something happens, it will be a different kind of corporate restructuring. Perhaps a spin-off of the marine business.

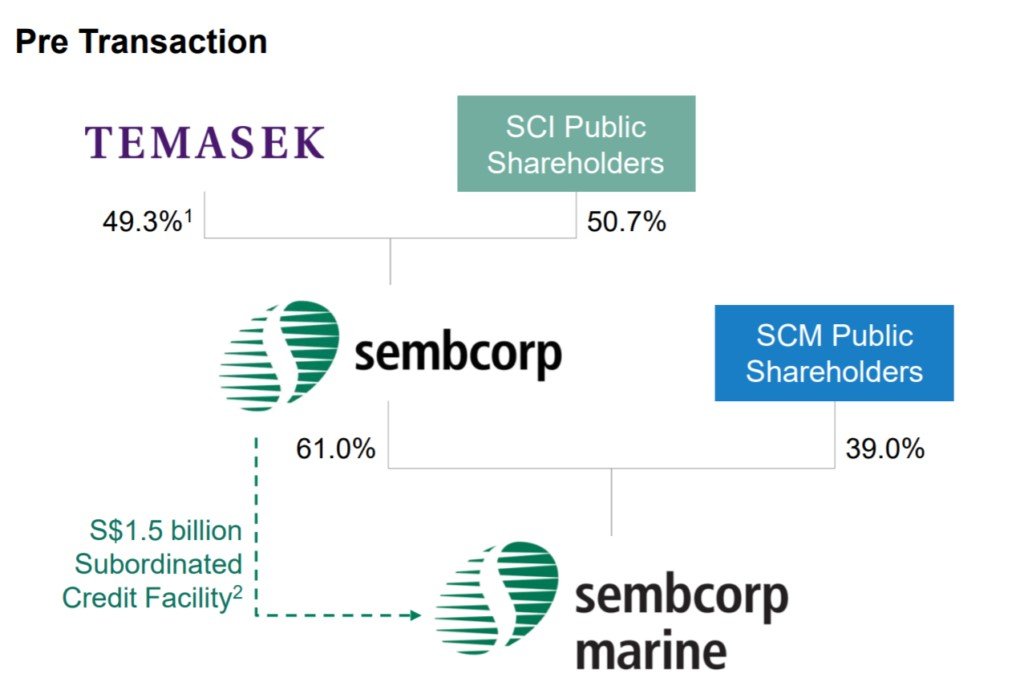

Phase 1 – Demerger for Sembcorp Marine

In June 2020, Temasek pulled off a big restructuring for Sembcorp Marine.

Before this, Sembcorp Marine was 61% owned by Sembcorp, which was itself owned by Temasek.

After the restructuring. Sembcorp Marine was spun off as a separate entity, owned by Temasek and shareholders directly.

Before and after charts below:

After:

At the time, this was what I wrote about the deal:

This is Phase 1 for Sembcorp Marine

My personal view though, is that this is merely a Phase 1 deal for Sembcorp Marine.

After the De-Merger, Temasek is left with a 30% to 58% stake in Sembcorp Marine. And it really doesn’t make sense to stop there.

If I were to try and think like Temasek…

I will find a way to merge it with Keppel Offshore and Marine…

I think that just makes the most sense here.

There are real economies of scale in this business, and it doesn’t make sense to have a Keppel and Sembcorp marine arm that compete against each other on the world stage. Rather, merge them, and create a national marine giant that can more effectively compete on the world stage.

That’s also in line with the broader strategy of creating national giants within each industry.

Phase 2 – Keppel O&M merger with Sembcorp Marine

Now I hate to say I told you say, but I literally did write about this in both of my Sembcorp Marine and Keppel articles.

And if this simple horse can spot it, I bet that literally everyone in the market saw what was coming.

Which is exactly what we saw today.

A merger of Keppel O&M with Sembcorp Marine, to be spun off into a new listed entity.

Makes perfect sense.

Why the merger of Keppel O&M and Sembcorp Marine?

Official reason is for economies of scale.

To have one big player who can compete for larger contracts, and to pursue “synergies” arising from the increased scale.

Fair enough.

BTW – we share commentary on financial markets every week, so do sign up for our mailing list, its absolutely free (goes out every Sunday).

Don’t forget to join our Telegram Channel and Instagram or (YouTube)!

[mc4wp_form id=”173″]

3 Quick Thoughts on the Keppel O&M / Sembcorp Marine Merger

Now I literally just read the press releases an hour or two ago, so I might not have had the time to fully digest this information.

So if I missed anything just leave a comment below, and I might do a fuller analysis over the weekend.

3 quick thoughts that spring to mind for now:

- Who is buying who? At what price?

- Value unlock for Keppel?

- Will share price go up?

Who buying who? At what price?

Singlish is so efficient.

Who buying who, at what price?

Saved me a whole bunch of words there.

Some back of the napkin numbers:

Sembcorp Marine has a market cap of $2.3 billion.

Keppel has a market cap of $9.3 billion. FY19 revenue for Offshore & Marine was 29%, so if we simplistically assume O&M is 20% of the current market cap, that puts its valuation at about $1.8 billion.

That means Keppel O&M is slightly smaller than Sembcorp Marine (pre-rights issue).

But now factor in Sembcorp Marine’s $1.5 billion rights issue, and things get a lot more interesting.

With the $1.5 billion recapitalisation, it seems that Sembcorp Marine might actually be the one to acquire Keppel O&M.

Very interesting.

Value unlock for Keppel Corp?

So Keppel Corp will get to spin off the marine business, and also sell a bunch of their legacy rigs.

If they do so at the right price, does this remind you of another deal?

Like CapitaLand spinning off its development business at a juicy premium – unlocking some nice value for shareholders?

We’ll need to see the final pricing to answer that, but definitely possible.

It will take some time though.

Per official announcements:

Keppel and Sembcorp Marine will undertake mutual due diligence and discuss the terms of the potential combination, which is expected to take several months.

Will share price go up – Keppel Corp vs Sembcorp Marine?

Here are the charts for Sembcorp Marine and Keppel Corp:

Both haven’t really gone anywhere the past 6 months.

For now, there’s still too little details on the final pricing to call whether it’s good or bad for shareholders.

It’s definitely nice to see something being done though, because the whole marine business has been in a rough spot since 2015, and this merger of 2 competing businesses to create a local champion is long overdue.

But whether there’s money to be made for shareholders, it will need to wait for the fuller details.

Gun to my head, I think Keppel Corp trades well tomorrow, while Sembcorp Marine trades poorly because of the big dilutive rights issue.

But let’s see. Trading is halted so no way to profit off this trade. ????

Love to hear what you think!

As always, this article is written on 24 June 2021 and will not be updated going forward. Latest thoughts (and my stock watch and personal portfolio) are available on Patron.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Both are THE best quality investment courses available to Singapore investors out there!

Completely agree that keppel shares will go up initially tomorrow since the deadweight is lifted. Similar to sembcorp when that happens.

I think is a good chance to finally buy keppel as property counter and it should trade well going forward.

Good point – this could be a sembcorp style play, which did pretty well after the demerger. Will see if I can look further into this for the weekend article.

SCM market cap is about 2.4b not 0.339b

My bad you are absolutely right. I have updated the article. With this, it seems like Sembcorp Marine might be the one to acquire Keppel O&M.

Temasek call off Kep deal because Kep did not meet some financial parameters, not because of Covid.

P/s : I am a Kep shareholder.

You’re right, I just googled and the MAC clause was tied to financial parameters:

The MAC clause mandates that Keppel’s profit after tax must not fall by more than 20 per cent, or below S$557 million, over the cumulative four quarters from the third quarter ended September 2019.

I suppose it’s a bit of chicken and egg because the drop in profit was itself due to COVID.

Thanks for raising this though, appreciate.

PS. You must be pleased with this deal as a Keppel shareholder, nice 5% bump on Friday 😉

Sell all and go wall st, SGX stock suck big time, I am lucky to go wall in May last year, I am up 2.2X even after the correction. Give SGX a miss, unless u are damn lucky to hook on ifast or similar, wiah i dont think u are so lucky. At wall st, u are spoil for choices,

Haha, definitely works too. 😉

Actually they got the business order not from 2 competing companies but as a whole team dividing orders shares. Example 1 team goes in for the deal and divides to 2 companies 60/40 or other values, Keppel always gets the bigger pie. Although Marine companies tend to be messier than other industry, Keppel is a far better operating company compared to SM which is so messy like old Chinese Workshop especially their top management to Managerial positions. A few years ago when business began to be bad, they had reshuffled and left incompetent HOD/GM Managers who create a lot of havocs while the good Managers had left after mistreatment. From my experiences, they can ask contractors to work but will not pay up when job done, not like Keppel who is more honest in this case.

Very interesting comment – appreciate the sharing!