So I’ve had some time to digest the Keppel Offshore & Marine (O&M) + Sembcorp Marine merger, and I wanted to share fuller thoughts.

Basics: Keppel O&M + Sembcorp Marine Merger

If you missed it, you can check out Thursday’s article for the full details of the Keppel O&M Sembcorp Marine merger.

To sum it up:

- Keppel O&M will merge with Sembcorp Marine

- Sembcorp Marine is doing a $1.5 billion rights issue

- Temasek will be a controlling shareholder in the new company

- Keppel’s shares in the new company will be distributed out to existing Keppel shareholders

- Merger is in the discussion stage now, completion of the deal likely to be in 2022

And as expected, after the news went out, Keppel Corp’s share price is up 5%, and Sembcorp Marine is down 25%.

Mistake with Sembcorp Marine’s Market Cap

A mistake on my part – I pulled Sembcorp Marine’s market cap wrongly for the previous article, it should be $2.4b instead of $0.4m.

Thanks to the readers who helped point it out.

Running the new numbers – it now looks like Sembcorp Marine will be the party to acquire Keppel O&M.

Sembcorp Marine’s latest market cap is $1.9 billion.

Add in $1.5 billion for the rights issue, and we have $3.4 billion market cap for Sembcorp Marine.

Keppel O&M is about 21% of Keppel’s revenue, so if we assume 20% of Keppel’s current market cap ($9.8b), that works out to a rough $2 billion valuation for Keppel O&M, give or take.

Sembcorp Marine is by far the bigger of the two, so it makes sense that Sembcorp Marine will acquire Keppel O&M.

It’s easy to see how this deal can be structured too:

- Sembcorp Marine acquires Keppel O&M

- Keppel gets shares in Sembcorp Marine, distributes it out to Keppel shareholders

- Sembcorp Marine spins out the unwanted assets into a new Asset Co that is sold

- Sembcorp Marine remains listed and changes its name to reflect the merged entity

It’s the path of least resistance, and the $1.5 billion rights issue from Sembcorp Marine just makes a lot of sense now.

Keppel the big winner?

So the path of least resistance is for Keppel to spin off Keppel O&M into Sembcorp Marine, get shares in Sembcorp Marine, which it then distributes to shareholders.

Sound exactly like a recent other deal – the Sembcorp demerger.

In that case, Sembcorp shareholders received shares in both Sembcorp and Sembcorp Marine, and Sembcorp share price went on an absolute tear after (cross is when the deal was announced):

Okay maybe you will argue that some of this was because of COVID recovery, but hey, that recovery didn’t seem to help Sembcorp Marine:

Could the same thing happen with Keppel here?

Keppel is a pretty decent infrastructure + land business, weighed down by the loss-making marine business.

Take out the marine business, and watch the rest fly.

Makes sense, on paper at least.

BTW – we share commentary on financial markets every week, so do sign up for our mailing list, its absolutely free (goes out every Sunday).

Don’t forget to join our Telegram Channel and Instagram or (YouTube)!

[mc4wp_form id=”173″]

What is Keppel left with after this?

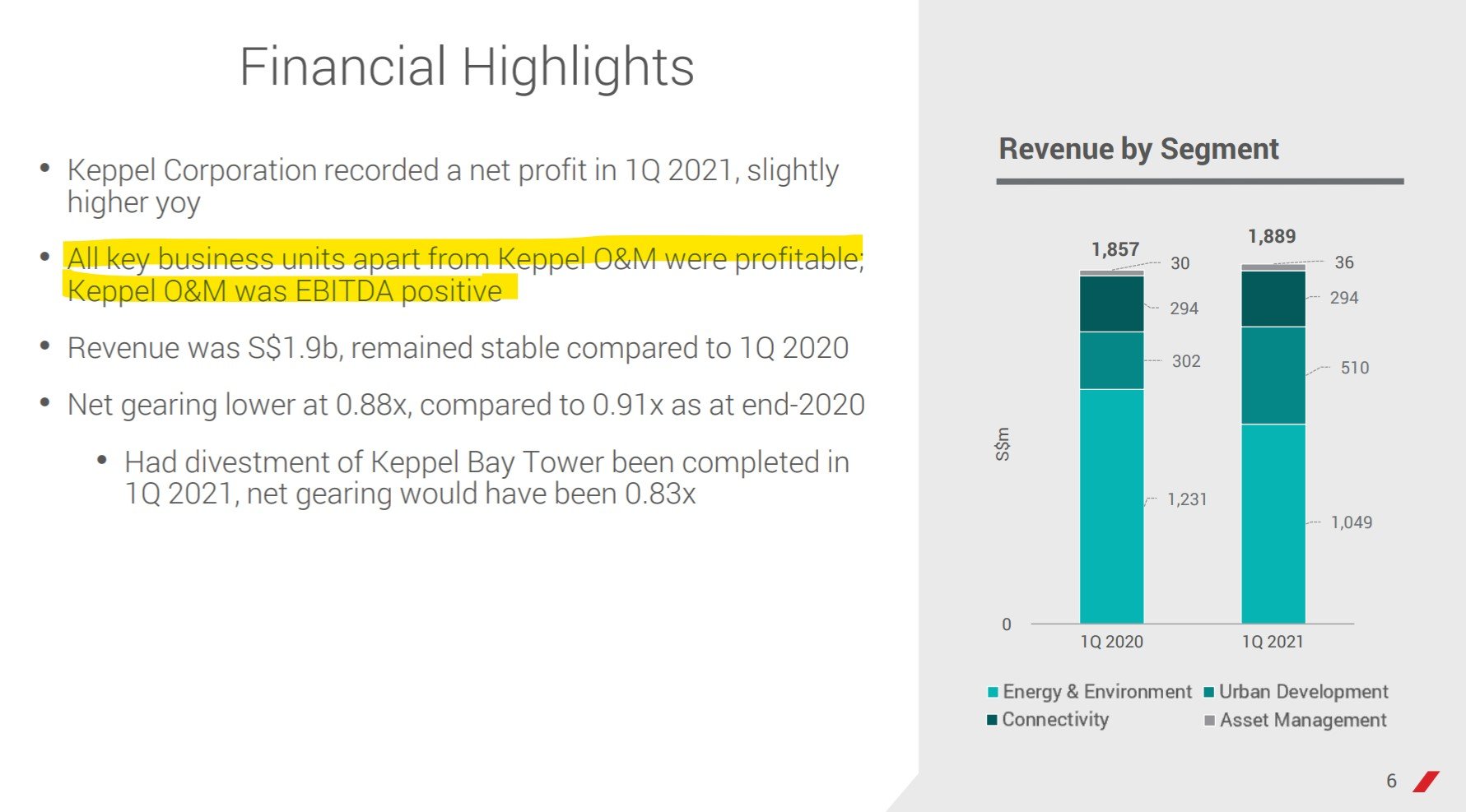

In Q1 2021, basically every business other than Keppel O&M was profitable.

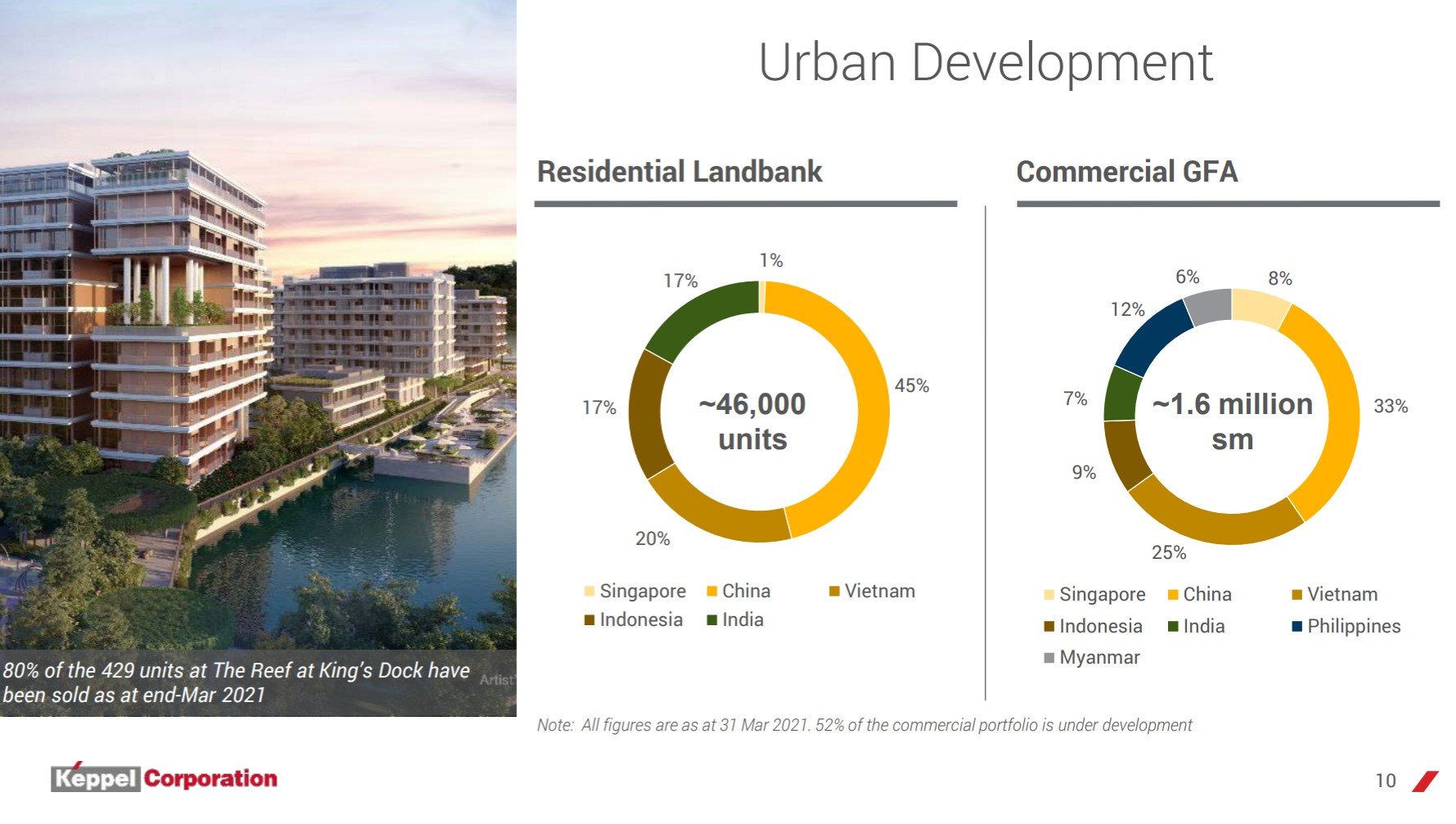

Strip out the marine business, and what you’re left with is:

- Energy & Environment – pivoting to renewables and Electric Vehicles (EV)

- Urban Development – basically Keppel Land

- Connectivity – Telco, M1 and data centres

- Capital – Asset Manager

Okay it’s not a sexy business like SEA with 100% year on year revenue growth.

But it’s still a very solid underlying business, that generates very strong cash flow.

You could argue it’s a superior version of Sembcorp, or a ST Engineering without the defence business.

And that’s a lot to like about that.

Note: For a detailed writeup on each business line, check out my 2020 article on Keppel here.

Valuation of Keppel Corp

Valuation for Keppel is really hard to do because we don’t know the price at which Keppel O&M will be sold for.

And Keppel O&M will most likely be sold in exchange for shares in the new entity, of which we also don’t know the true valuation.

Too many variables, too many moving parts.

No point trying to model everything.

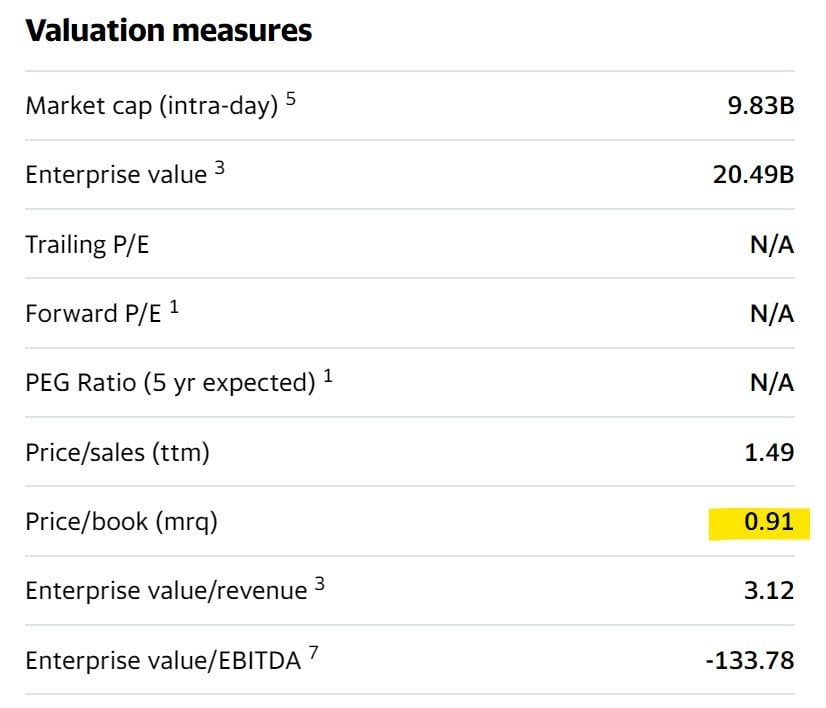

So I’ll just keep it simple, and look at Price to Book.

Keppel today is valued at 0.91x Price to Book.

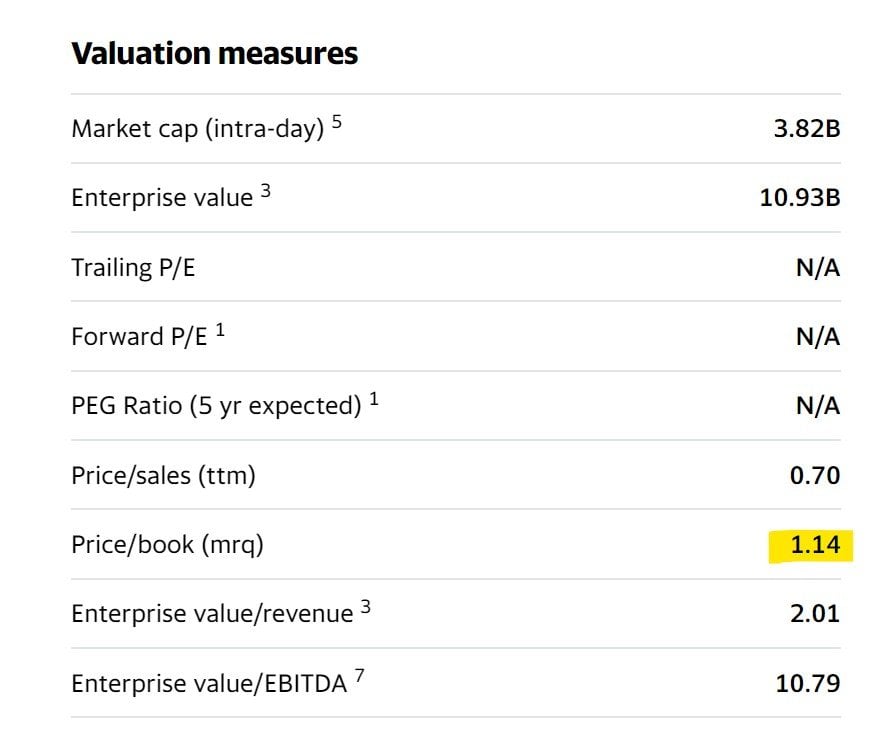

Sembcorp on the other hand, is at 1.14x book value:

Gun to my head, I would think Keppel’s core assets should be valued more highly than Sembcorp, no?

I don’t see any strong reason why Sembcorp should trade at a higher multiple than Keppel (once Keppel O&M is divested).

If so, that could imply a 10% – 15% upside from here for Keppel’s core assets.

But don’t forget you’ll also get the shares in the merged Keppel O&M / Sembcorp Marine. Whether you can sell that on the market at a decent price, really hard to tell at this stage when we don’t know the valuations.

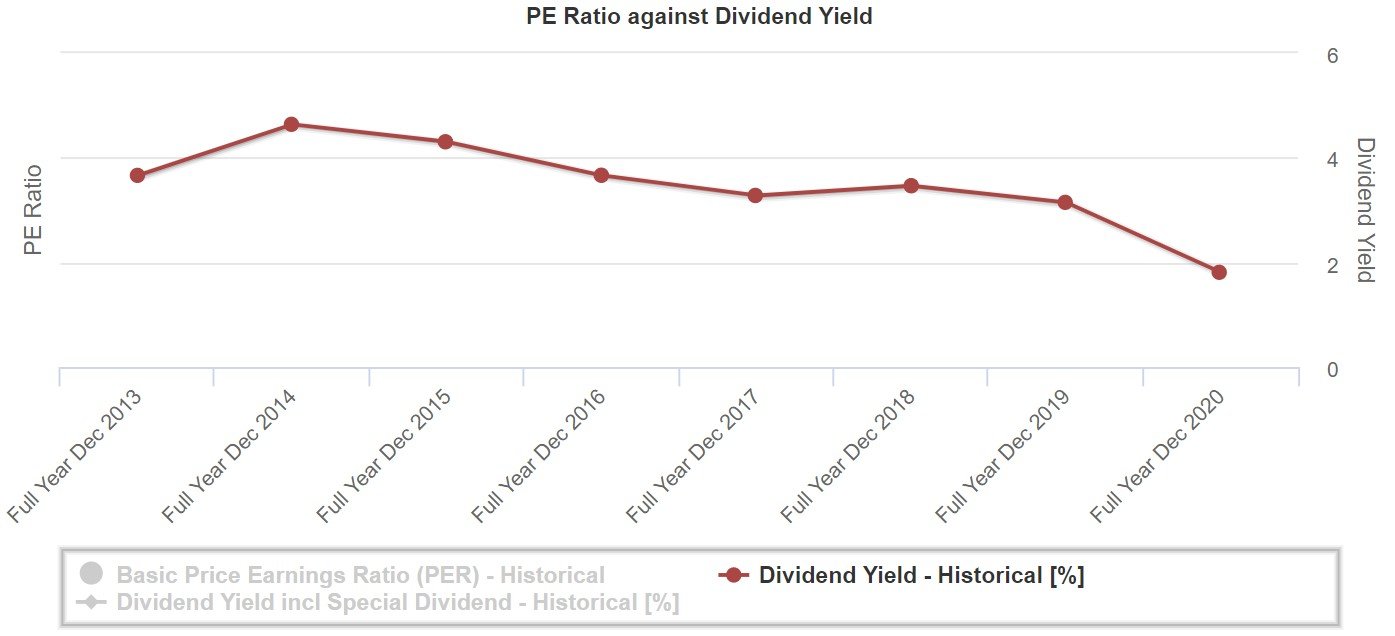

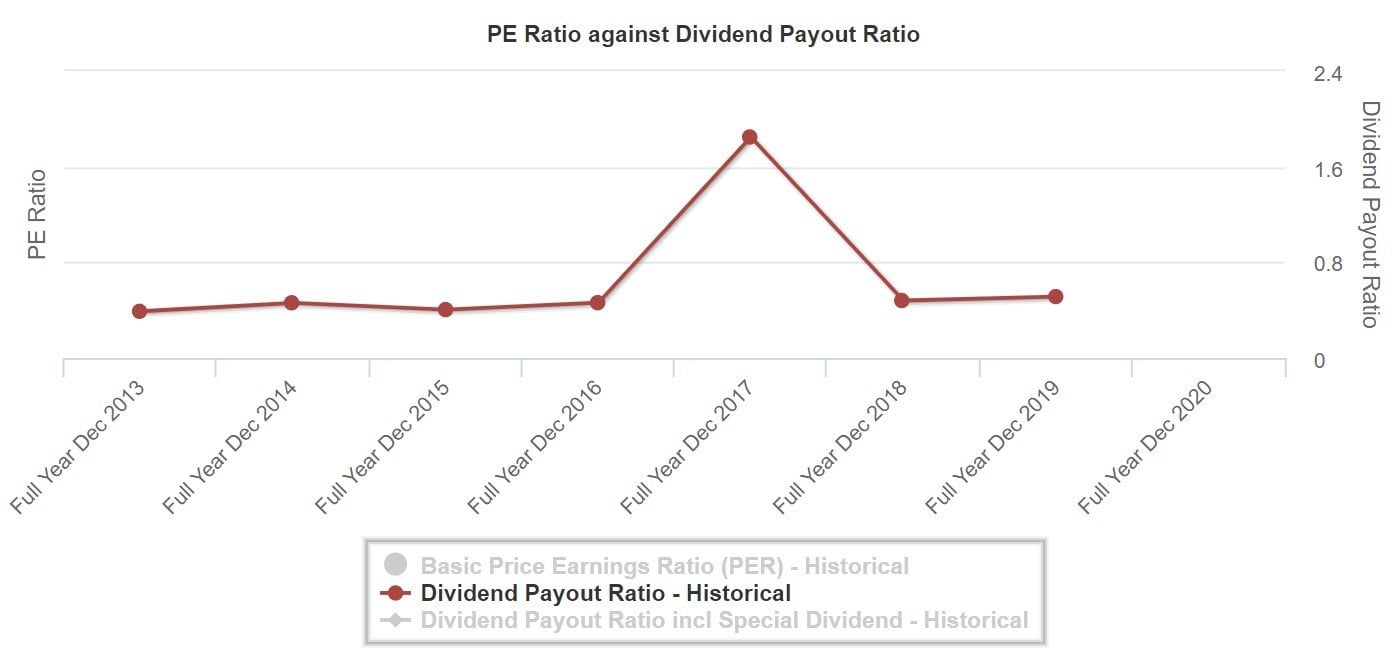

Keppel’s Dividend

A quick note on dividend.

Dividend was a solid 4% back in the heydays of Keppel (2015).

Since then, it’s been on a downward trend, and the FY 2020 dividend is less than 2%.

That said, 2020 was a COVID year, and the marine business is a big loss maker.

Once COVID passes, and the marine business is sold, that would free up a lot of cash flow.

If the 50% payout ratio stays, we might be able to see 2-3% yields in time to come.

It’s not amazing, but still better than nothing.

Timing of the Keppel / Sembcorp Merger

Now this is going to be a very complex deal to negotiate.

Minimum, I would say 3 – 6 months to hammer out the details – which means it will be end 2021 before we know the full price and restructuring details.

Throw in a couple months for the EGMs and shareholder approvals, and we’re looking at Q2 2022.

By the time this deal completes, we’ll probably be in Q3 – Q4 2022.

So if you buy into Keppel for this deal, be prepared to wait.

Pricing details should be out by end of the year though, so there could be a small catalyst for the share price if the news is good.

Will Keppel get a good price for Keppel O&M?

That said, I’m not super optimistic on pricing because Sembcorp Marine is a listed entity with their own shareholders to answer to.

If they overpay for Keppel O&M, Sembcorp Marine shareholders will be up in arms.

If they lowball, Keppel shareholders will freak out.

Really tough to please everyone, which usually ends up with a middle price that is decent for all parties, but doesn’t really benefit anyone strongly.

Don’t forget that Temasek only holds 20% of Keppel:

Longer term – can the Keppel business do well?

That’s the short term though.

Longer term, there’s really only one thing that matters – can the restructured Keppel business perform on the world stage?

Which essentially is a proxy to the question – How competitive is Singapore Inc in the new world?

The big boys like ST Engineering, Sembcorp, Keppel, Singtel, how effectively will they be able to compete on the world stage?

They did very well in Singapore’s first phase of development. Names like SIA, DBS and CapitaLand brought Singapore Inc to where it is today.

But the world has changed a lot since.

The past few years have been tough on the TLCs, which is why we’re seeing so many restructurings now.

The TLCs need to reinvent themselves, and find a way to differentiate on the world stage.

And that’s the million dollar question here.

No amount of restructuring can save the share price if the underlying business is just not competitive.

Frankly I don’t know the answer to this one as an investor. In some ways it goes back to the political situation, and the future of Singapore as a nation state.

But as a Singaporean, I am cautiously optimistic.

I think that we’ll find a way to do it.

Necessity is the mother of invention.

Macro tailwinds for Keppel

Macro wise – there’s a lot to like though.

Like I shared in last week’s article on ST Engineering, I think the coming decade will see strong economic growth.

I see a lot of fiscal stimulus, a lot of capex spending, a lot of inflationary pressures in the years ahead.

And I think we’re still in the early to mid stages of this post-COVID cyclical upturn.

There could be some volatility short term as the emergency liquidity fades away and yields go up. But broader economic growth should remain strong this decade.

That’s very bullish for infrastructure plays like Keppel.

Could be a rising tide lifts all boats scenario.

A quick note on the Sembcorp / Keppel Marine business

You have got to feel for the Sembcorp Marine shareholders though.

Just when the share price was starting to recover, there’s a big dilutive rights issue and the share price tanks 25%.

And you have to take up the rights or be diluted.

Not a great situation to be in.

Frankly though, the offshore & marine business is a really tough one to be in.

The recapitalisation and merger will definitely help, but the problems go deeper – it’s the poor underlying industry dynamics.

With all the moves away from oil to renewables, the rise of state backed competition in Korea and China, it’s become a very cutthroat business to be in.

So longer term, I’m not so optimistic on this one.

Closing Thoughts: Will I buy Keppel?

Funnily enough, my thoughts on Keppel are pretty similar to ST Engineering last week.

I think once you strip out the loss-making marine business, the underlying business is a pretty decent infrastructure + land play.

Some strong macro tailwinds too.

That said, I’m probably not buying Keppel now, for the same reasons as ST Engineering.

Opportunity cost of funds, and also the value end of my barbell is already fully allocated.

I just see better uses for the capital elsewhere.

Long term secular plays like tech / China, or pure cyclicals like banks and oil.

For those who are keen, you can check out my personal portfolio and FH Stock Watch on Patron.

Love to hear what you think though! Is Keppel a good buy after this restructuring?

As always, this article is written on 25 June 2021 and will not be updated going forward. Latest thoughts (and my stock watch and personal portfolio) are available on Patron.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Both are THE best quality investment courses available to Singapore investors out there!

Necessity is the mother of invention.

> This I just felt so compelled to thank you for the sudden jolt of inspired hope.

For Singapore Inc, I am also cautiously optimistic. I see our current ministers as being clear on the direction needed for SG to push forward in the post-Covid world where the rules of globalisation is being revamped, with more protectionist approaches and where the global institutions led by the US are being exposed for being massively incapable/irrelevant (WTO, WHO, World Bank, IMF). Greece as an example, who needs the IMF to provide bailout when the ECB can buy up all Greek bonds and push down the cost of borrowing to negative? Or the WHO which can only lament that the poor countries are being trampled on by rich countries in sourcing for vaccines, but are unable to do anything meaningful to change this situation?

Though the direction is clear, the onus is on us SGeans to step up our game and for many to reskill ourselves using the Govt schemes. Our production capabilities will probably be limited and contained to the higher end of the value chain, hence most of our value add has to be intangible capabilities. I see the path of being the gateway to SEA as the only viable option for SG. Perhaps as a platform type of service provider, linking up the production capabilities across SEA countries and coordinating them from SG. Hopefully such a direction can help produce enough jobs to prevent a shift towards more populist tones in SG.

Sorry for the long message haha.. just felt inspired to add on to your views on SG’s future.

Yes! Exactly this. 🙂

It’s easy to complain and pass the buck on to the next crop of 5G leaders, but really, if we as Sgeans want to see change, we need to start with ourselves.

Like the saying from Gandhi goes – if you want to change the world, start with yourself.

I don’t think the next phase will be easy. What got us here will not get us to where we need to go. Technology, Deglobalisation, the rise of China has changed the world in many ways.

But I see the number of Singaporeans out there who are achieving great things on the global stage and it’s clear to me that Singaporeans as a whole are punching way above our weight.

If we all set our mind and contribute to the future growth of Singapore, I see no reason why we cannot achieve success.

While I agree this is the optimistic and ideal view of how SG can pivot ourself for the future, the political risks involved is still very high, isnt it?

In this instance, not domestic political risk but foreign political risks in terms of SEA countries ranging from Malaysia, Thailand, Indonesia and to a certain extent to Cambodia and also Vietnam.

While SG try to make ourself the middle men, what is stopping the other countries from trying to rival SG and does everything themselves? In addition, the countries will always be protectionist and also try to get a pie from SG as well. SG will be exposed to such risks.

Citing an example of SG companies’ investments into India, where some major investments have soured largely due to corruption (imo). we have to deal with this in neighboring countries as well.

Yup I don’t disagree.

Whether SG can execute, and surmount all of these challenges – that is the million dollar question! If we can’t, the future of Sg looks bleak, so for our own sake let’s hope we can. 🙂

“I just see better uses for the capital elsewhere.”

As an existing Keppel shareholder, I share your assessment on Keppel.

There are better investments than what’s available in SGX.

How will Singapore Inc compete in the new world with the lack of growth companies in SGX?

Well Singapore does have good growth companies like SEA and Grab, although none are listed on SGX. And the big names like Tencent, Alibaba, Bytedance are all coming to Singapore as well to use as a regional hub.

But yeah, I agree that the SGX these days is mainly just old world companies and a few small cap growth stocks (the likes of iFast or Nanofilm).

I think its unfair especially to the engineering/technical section of Keppel to say its belongs to the old world industry. I believe Keppel has a strong heavy industry engineering expertise than can easily be adapted to renewable energy to power the growth of the company. Its the management that was slow to acknowledge this and switch towards the green initiative happening around the world. Anyway better late than never and the management has finally moved in this direction. The renewable energy area has just started to move to the golden era, waste recycling, water purification, clean energy, natural resource conservation, etc, which is the next big thing that will fully transform the landscape of this planet. Keppel can play a big part in this. All it needs is to dream big.

Interesting point – thanks for raising. Appreciated.