So… it’s the final weekend of 2023.

No matter how well (or badly) your investment portfolio did this year.

The scores are reset, and it’s a new year on 1st Jan.

Now 2023 was a volatile year.

The playbook for 2023 was to be long stocks/bonds in Q1 – Q2. Take profit or go short in Q3. Then flip back long in Q4.

That volatility doesn’t look like it will go away any time soon, and 2024 might be as much of a roller coaster ride.

With that in mind, how would I invest as a Singapore investor in 2024?

What are the key short / mid term trends for this decade? (as a Singapore Investor)

The way I see it, the key mid term trends for investors this decade are:

- Rise of a multipolar world – higher geopolitical conflict

- Structurally higher interest rates and inflation

- Weaker economic growth from China (can’t expect China to save the world this time)

But shorter term – with a 6 – 12 month timeframe?

The key trends look to be:

- Global economic growth remains weak (possibly recovering)

- Interest rate cuts / monetary policy easing likely in 2024

- Upcoming elections in many countries including US (big incentive to avoid recession)

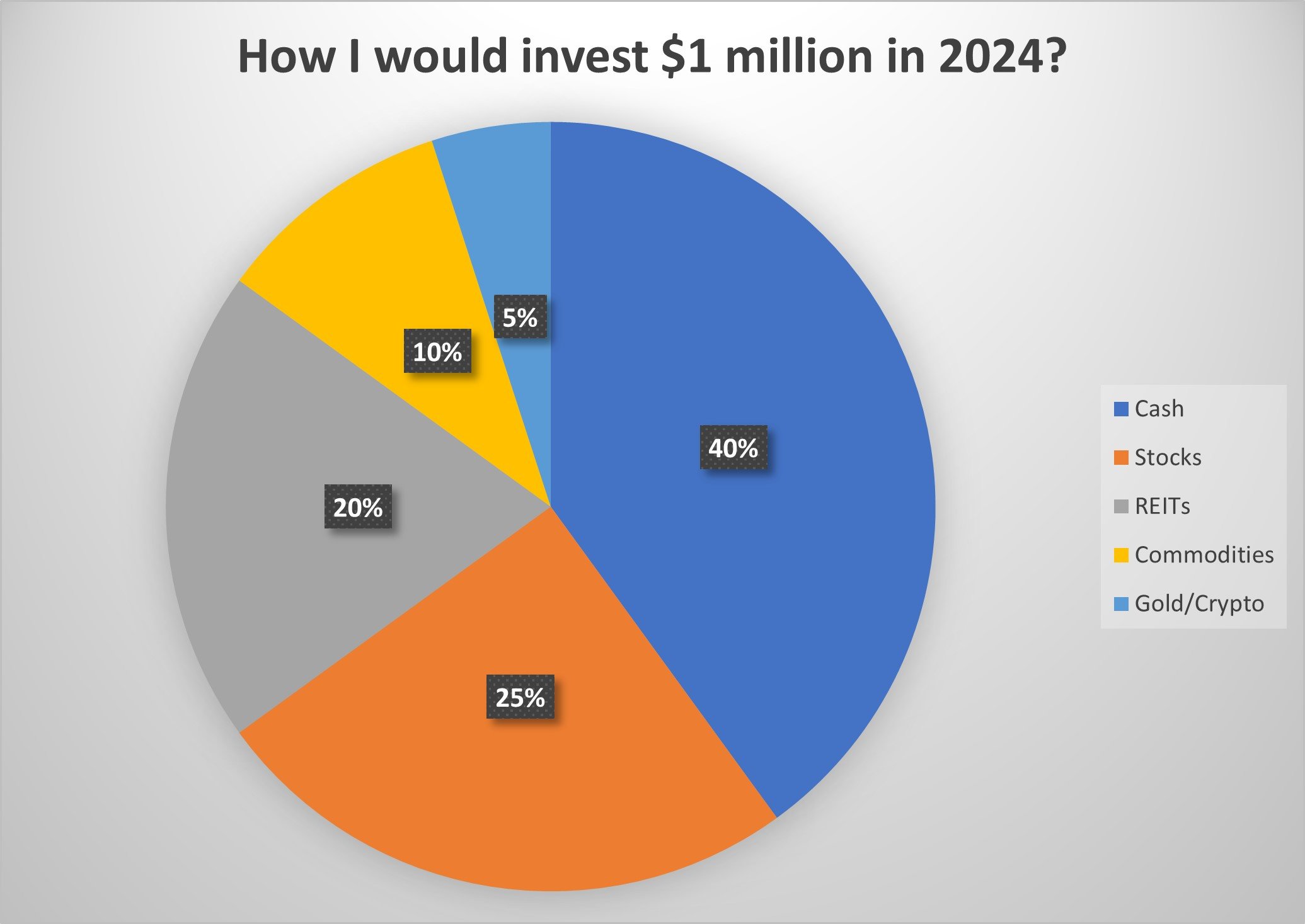

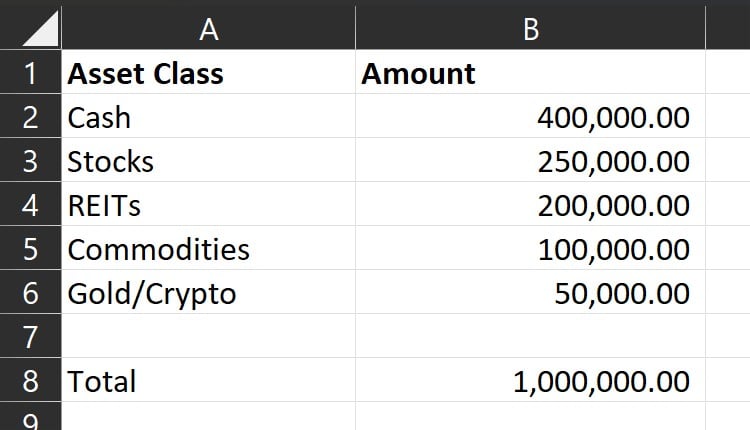

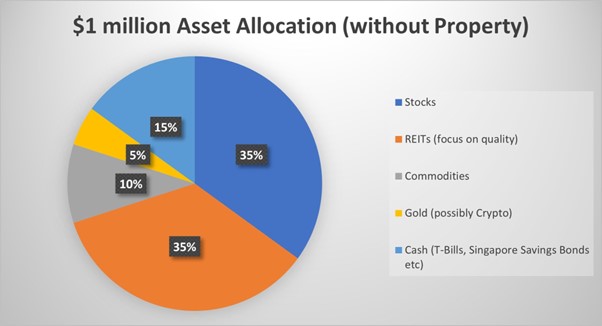

How I would invest $1 million in 2024?

Given all of the above, how would I invest $1 million in 2024?

This was the rough asset allocation I came up with:

I wanted to share more about the thought process below.

It came down to 3 key questions for me:

- How much cash to hold?

- What stocks to buy? Do you overweight US? Do you buy growth or value/dividend?

- What is the path for inflation / interest rates going forward?

Key Question 1 – How much cash to hold?

The key question in my mind, is how much cash do you hold, and how much risk do you take in 2024?

While this is ultimately a question each investor needs to answer for themselves.

Let’s try to get some clues from the macro backdrop, and current valuations.

Macro backdrop is bullish?

Jerome Powell’s Fed and Janet Yellen’s Treasury have flipped dovish in the past 2 months.

This has juiced financial markets, which has surged ever since Yellen’s “Pivot” in late Oct, and again after Powell’s “Pivot” 2 weeks ago.

I’ve shared with FH Premium subscribers that I increased risk exposure after the Powell “Pivot” 2 weeks ago.

And yes – no doubt the market can continue to run in the short term.

But how long can it run?

What is the market pricing in, vs what is likely to materialise?

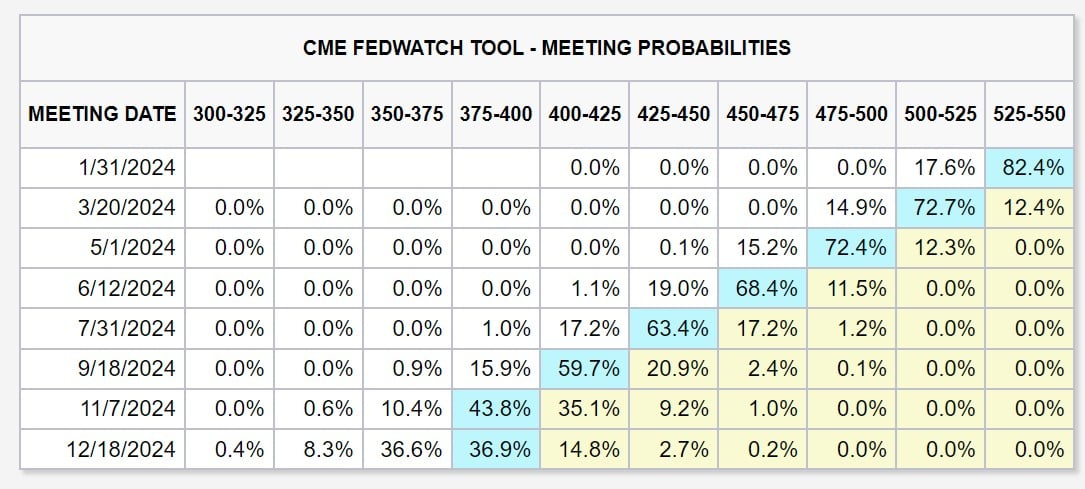

The market today, is pricing in a whopping 6 rate cuts in 2024.

That’s a total of 1.5% in interest rate cuts:

I mean you guys know me – I’ve been saying for a while now that the Feds will need to cut in 2024.

But if the market is pricing in 6 rate cuts.

For any further upside – you’re going to need to see more than 6 rate cuts (which I don’t think you’ll see that outside of a recession).

Which means that if the economy stays strong, and we get less than 6 rate cuts.

That’s an implicit tightening in monetary policy, which is bad for stocks / bonds.

Whereas if the economy weakens, and we get more than 6 rate cuts.

That implies a recession, which is not going to be good for stocks (but good for bonds).

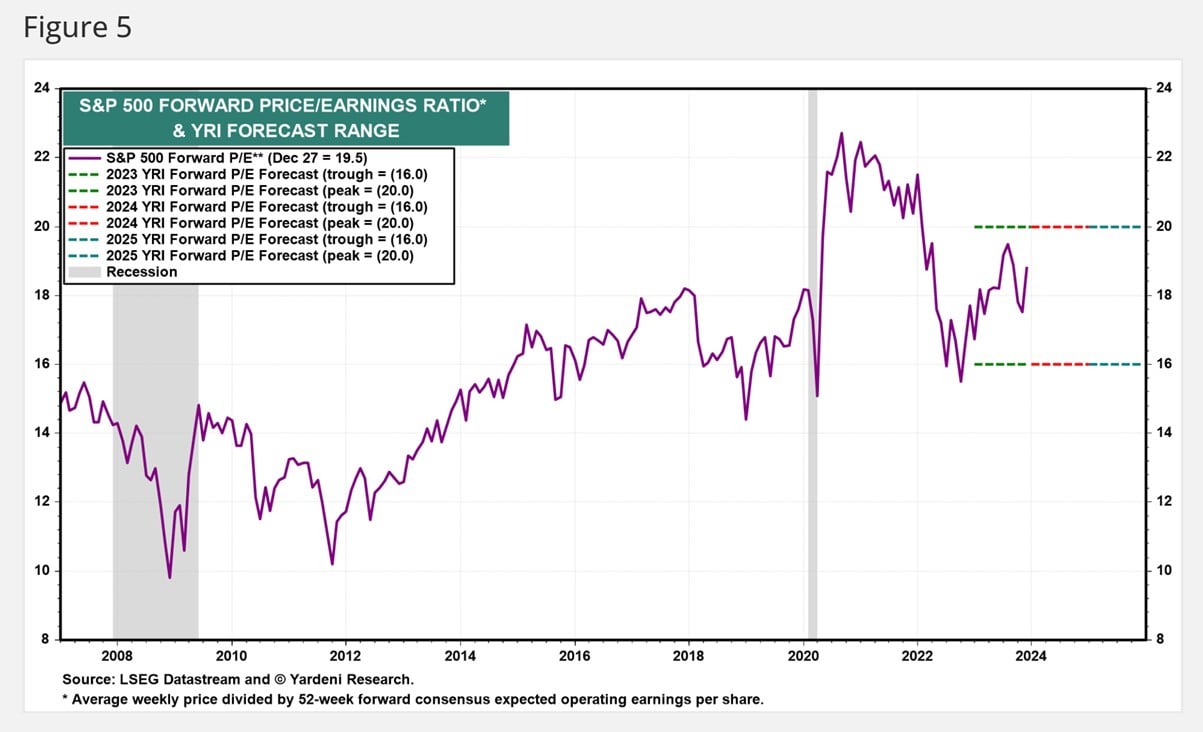

Stock valuations are not exactly cheap

At the same time, it’s kind of hard to say that stocks as a whole are “cheap”.

Yes I agree that on an individual stock level some stocks are still cheap, so no doubt stock picking still works.

But as a whole, the S&P500 trades at 19.5 times forward P/E.

That is well above the long term average in the 2010s, which don’t forget was a period of zero interest rates and non-stop QE.

The thing about valuations is that the cheaper the valuation you buy, the higher your probability of gains.

With such a high starting point, I would at least be a bit cautious here.

So… how much cash to hold?

With that in mind, I decided to run a 40% cash allocation for this portfolio (ie. 60% gross exposure).

Given what the market is pricing in vs what is likely, given the starting valuations.

And given the fact that T-Bills are still paying 3.73% absolutely risk free.

I didn’t feel a need to go all-in into this market.

Yes, some allocation is required because there’s always pockets of value in the market, and it’s never wise to sit out entirely.

But 40% cash probably gives a sufficient margin of safety that if things head south you have optionality to buy in.

And if risk assets have a blow-off top at least you are allocated.

Update: Some of you have asked about long term bonds, and whether it deserves an allocation. Personally I’ve been trading in and out of long term treasuries in 2023 (as shared on FH Premium), and I think this is a position that requires nimble positioning. At 5.00% on the US10 year I thought bonds were a no brainer. At 3.8% today? Much less certain on the future path here, as the earlier pivot could mean robust economic growth and the return of inflation down the road (resulting in higher long term yields).

What about for long(er) term investors?

Now I just want to caveat that this is more of a short term tactical asset allocation.

If you’re a long term investor, you don’t want to market time, and you want to buy and hold for 10 – 20 years?

Then all the short term macro is just noise for you.

I wrote an article last year for ultra long term investors, which remains very much relevant.

Cash allocation would be significantly lower, and might look something like this:

Key Question 2 – What stocks to buy? Do you overweight US? Do you buy growth or value/dividend?

The next big question – is what stocks to buy.

Namely – do you overweight US stocks?

And do you overweight growth stocks (instead of dividend stocks)?

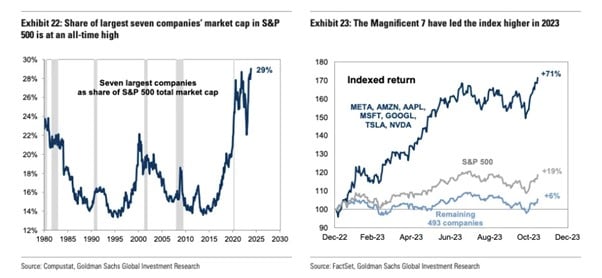

The US stock market is driven by 7 stocks these days

Without a doubt – overweighting US growth stocks was the big winner in 2023.

To be more precise – overweighting 7 specific US stocks was the big winner in 2023 (the Magnificent 7).

But we’re kind of getting to the point where there’s really no point buying the S&P500 at all – you might as well just buy those 7 stocks and be done with it.

If history is any guide, whenever things get this extreme, it usually reverses at some point.

The tricky part is calling the turning point.

If you sell too early you underperform the market.

If you sell too late – well at least the market sells off too so you don’t underperform.

So unfortunately, you still need to run an allocation to the “Magnificent 7”.

But I do think you want to watch this very closely in 2024 for signs of reversal.

And some of the smaller cap techs have not rallied significantly too, so those may have the potential to outperform in 2024.

What other stocks to buy instead of Tech?

I know that I have been neutral on the banks for most of 2023 on expectations of interest rate cuts in 2024.

Recent events though, may have changed my mind.

I don’t think you can underestimate the impact from the Fed/Treasury Pivot the past 2 months, as an indication of how 2024 may play out as an election year.

If the policy makers are going to inject liquidity to improve the economy ahead of the elections.

What would benefit in a scenario like that?

Tech, REITs, commodities, gold/crypto no doubt.

But within stocks – banks could also be a winner in such a scenario.

Economic growth stays resilient, interest rates down but not zero, lots of cheap funding in the market – that could be bullish banks simply due to higher loan growth and low default rate.

Same logic for industrials / cyclicals, which could be another area to look at, especially for those that are still cheap.

What are the specific stocks to buy?

Now the point of this article was to discuss high level asset allocation and not specific stocks.

I set out the specific stocks / REITs I am keen to buy, with rough target pricing, on FH Premium.

Do subscribe for FH Premium if you’re keen.

You can also see how I am positioned today, with weekly updates on how what I buy/sell.

Key Question 3 – What is the path for inflation / interest rates for the next 6 months? What about the next 2 – 3 years?

Looking beyond the immediate 6 – 12 months.

The premature policy easing by Jerome Powell worries me.

I’ve always said that Powell has to strike a fine thread here.

Cut too late – you risk a bad recession.

Cut too early – you risk inflation roaring back.

The events of the past month – suggest Powell may be making the mistake of cutting too early.

If that is indeed the case, I would be worried about the implications for inflation 6 – 12 months down the road.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

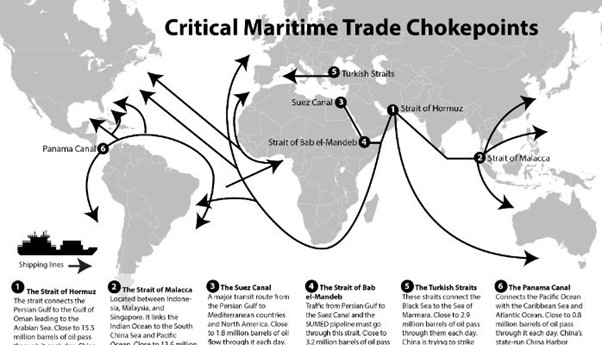

Geopolitical tensions remain high – and are likely to stay that way this decade

In case you forgot – there are 2 active wars in the world right now.

The European theatre in Ukraine-Russia.

The Middle-East theatre in Israel-Gaza.

The past 2 weeks already showed what could go wrong.

A bunch of rebels in the middle east taking potshots at boats.

Has the potential to disrupt commercial freight – forcing them to take a much longer route around the Cape of Good Hope in South Africa.

The way Powell/Yellen are easing – there are not buffering in any margin of safety for geopolitical tensions, and its potential impact on inflation.

And if I’ve learned anything from the past 3 years.

It is to expect the unexpected.

Any wildcard on geopolitics in 2024 – could have material implications on inflation given how policy makers are easing.

How to hedge geopolitical risk as an investor?

Because of that, I allocated 15% of the portfolio to a mix of commodities and gold/crypto.

In the original version I actually allocated as high as 20% allocation to commodities/gold/crypto.

But the short term outlook for commodities remains murky because of weak global economic growth, and a weak China, so I dialled that down a notch.

Mid term though, I’m quite bullish on commodities.

On the demand side you have all the tailwinds from east-west decoupling, building entire new supply chains from scratch, and the green energy transition.

On the supply side you have a decade of underinvestment in supply, and weaponisation of commodities supplies.

Will we see a return to money printing medium term?

The other thing about wars – they always lead to a surge in government spending, inevitably financed by money printing (eventually).

Take a look at both World Wars for example, or go further back in history if you like.

If you think the US-China rivalry is going to continue (and there’s no reason to suggest why it wouldn’t).

This would suggest huge government expenditure on both sides – to build up new supply chains, invest in “strategic sectors”, even to fund hot wars (see Ukraine/Israel).

Money printing is an inevitability?

The way I see it.

If you leave aside the short term attempts to tighten monetary policy and bring down debt levels.

I frankly do not see a sustainable mid term path without money printing in some form.

Look at the chart of money supply below.

Yes, money supply has definitely come down over the past 2 years – but what about the next 5 years?

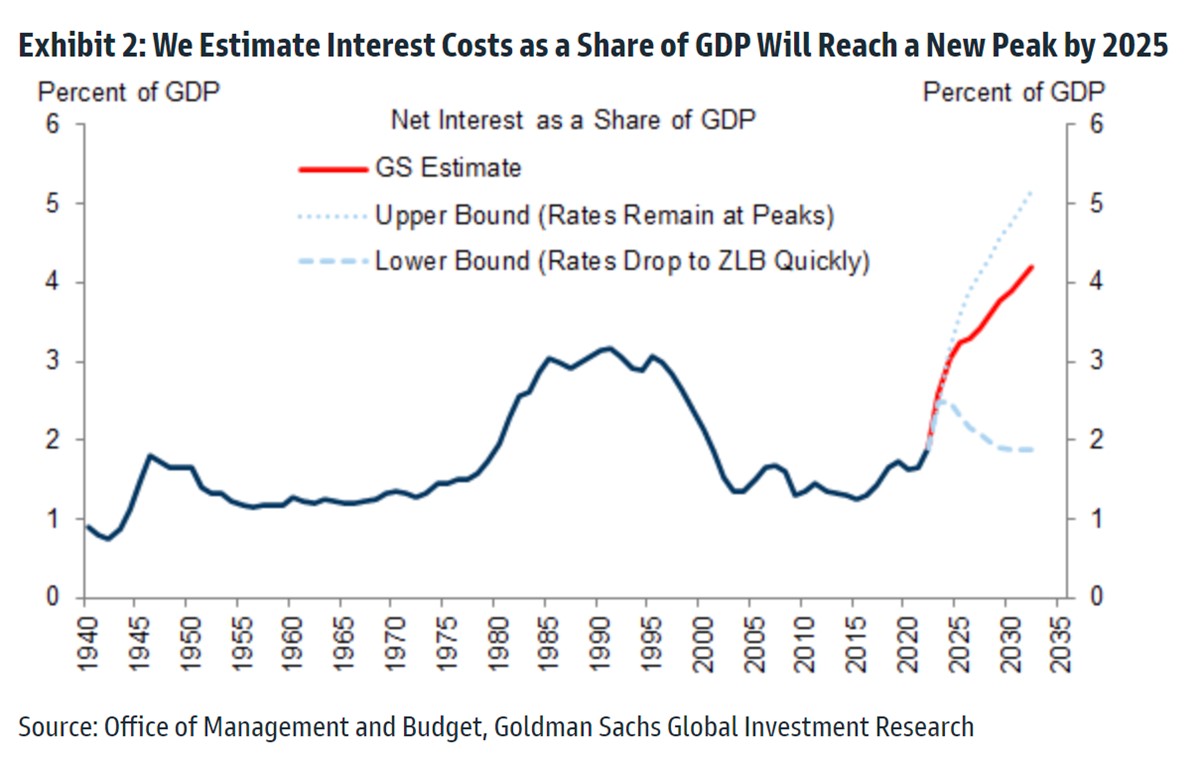

The US is spending more than they earn.

And because of higher interest rates, an ever increasing amount of government spending is going towards paying interest on existing debt:

In the mid term, there are only 3 sustainable solutions:

- Decrease spending

- Increase tax revenue

- Cut interest rates / monetise the debt

(1) is never happening in a large way given the great power conflict with China.

And c’mon – which politician wants to cut spending.

(2) is possible, but I’m not sure it can be done to the extent required to meet government spending given structurally higher interest rates.

So while both (1) and (2) may be used, inevitably when the problem gets big enough, there is a good chance we return to (3) money printing.

How to hedge money printing as an investor?

In a climate like that, you do inevitably have to own hard assets.

Think commodities, gold/crypto, real estate, stocks.

So while this portfolio is running a higher short term allocation to cash at 40%, I don’t doubt that in the mid term that cash allocation will likely need to be reduced.

But reduced by how much, and when?

That’s the million dollar question – and I will be guided by the markets on that.

FH Premium subscribers will get regular updates as and when I change my thinking / portfolio allocation.

Closing Thoughts: Don’t be afraid to change your mind if the facts change

In case it wasn’t already clear from 2023.

We are living in unprecedented times.

We are living in an era where US supremacy is being challenged by the rise of a more multipolar world.

With 2 hot wars taking place, that are reshaping global alliances and supply chains.

At the same time – unprecedented boosts in productivity are being developed from AI.

If you think about it, the industrial revolution took 70 years, while the IT revolution took 40 years.

The AI revolution is going to play out at breakneck pace, as quick as a decade or two.

In a climate like that – its perfectly fine to not have the answer to everything.

As investors, you want to be nimble and flexible in your positioning.

And if the facts change, don’t be afraid to change your mind, and change your asset allocation.

I came across a great quote from Nassim Taleb recently:

If you change your mind too frequently, it suggests that you do not think carefully and responsibly before formulating an opinion & don’t know when to remain silent or neutral.

If you never change your mind on anything, it indicates that you are an intellectually dishonest.

That pretty much sums it up for me.

As an investor – you want to put enough thought into your asset allocation, based on what you know today.

But if the facts change, don’t be afraid to change your mind.

This article was written on 29 Dec 2023 and will not be updated going forward.

For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do subscribe for FH Premium.

WeBull Account – Get up to USD 5000 worth of shares (Best promo of 2023 – Now Extended)

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now (Best Promo of 2023)

You can get up to USD 5000 free shares.

You just need to:

- Sign up for a WeBull Account here

- Fund any amount (get 5 free shares)

- Hold for 30 days (get 5 free shares)

OCBC Online Equities Account – Trade on 15 global exchanges, all via the OCBC Digital Banking App!

Did you know that can you trade shares on your OCBC Digital Banking App?

With an OCBC online equities account, you can buy stocks, local ETFs, REITs, bonds and more directly through your banking app.

Even better? Enjoy reduced commission rates of just 0.05% for buy trades on SG, US and HK market until 31 December 2023.

Everything on one app! Fuss-free funding, with access to 15 global exchanges

For SGD trades, you can fund and settle automatically via your OCBC account.

And for FX trades, you can settle using the foreign currency held in your OCBC Global Savings Account.

This means fuss-free trade settlement and minimising forex costs – saving you time and money.

Start trading with your OCBC Online Equities Account here!

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Best investment books to improve as an investor in 2023?

Check out my personal recommendations for a reading list here.