First mainboard listing on the SGX since COVID-19!

And very hotly subscribed – insane demand from institutional investors.

But is it worth investing? Let’s find out!

Basics: What is Nanofilm Technologies?

Nanofilm Technologies was founded in 1999 by a NTU professor, Dr Shi Xu (featured on the cover photo).

It was a spinoff from NTU, and is a high-tech materials company, “offering surface solutions based on vacuum deposition, including using our FCVA technology”

Basically, it uses advanced manufacturing techniques to manufacture materials, that have many uses in the industry.

What I like about Nanofilm Technologies?

Leading FCVA technology

It’s a technology company, so the technology better be great.

And if the reports can be trusted, Nanofilm’s technology some of the best in the industry, way ahead of their competition.

Their FCVA technology is particular is supposed to be very good.

I extracted the technical description (for those who are more engineering inclined), but it’s basically a technique to coat normal materials like metal or plastic with a thin layer of advanced materials like diamond or ceramic. This gives the materials great properties, very useful when building consumer products.

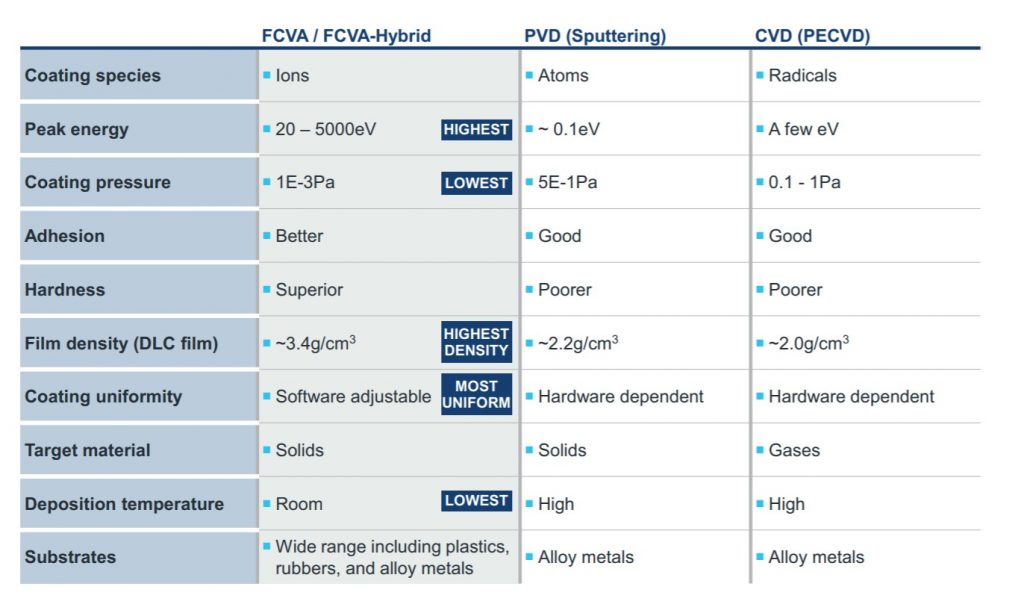

FCVA is an arc-deposition process which deposits a thin film of advanced materials such as carbon, metallic, ceramic, nitrides, oxides or composite materials on a variety of substrates. Substrates which can be coated include metals, ceramics, glass, plastics, rubber and other materials with a low melting point. Under our Advanced Materials BU, we offer surface solutions to deposit our advanced materials onto substrates either by solely utilising our FCVA technology or in combination with our other deposition technologies.

Components to be coated are passed through a short cylindrical-shape vacuum chamber, with our advanced materials deposited on the substrate through the use of ionised plasma beams produced by striking an electric current through the surface of the coating source. As the components are passed through the vacuum chamber, a striker (anode) strikes on the surface of the target materials (cathode) through electrical current, generating plasmas in the arc source, which are then passed through a filtering bend to filter the unwanted particles. In this process, only pure ion species would enter the coating chamber, forming our advanced materials for deposition on the substrate.

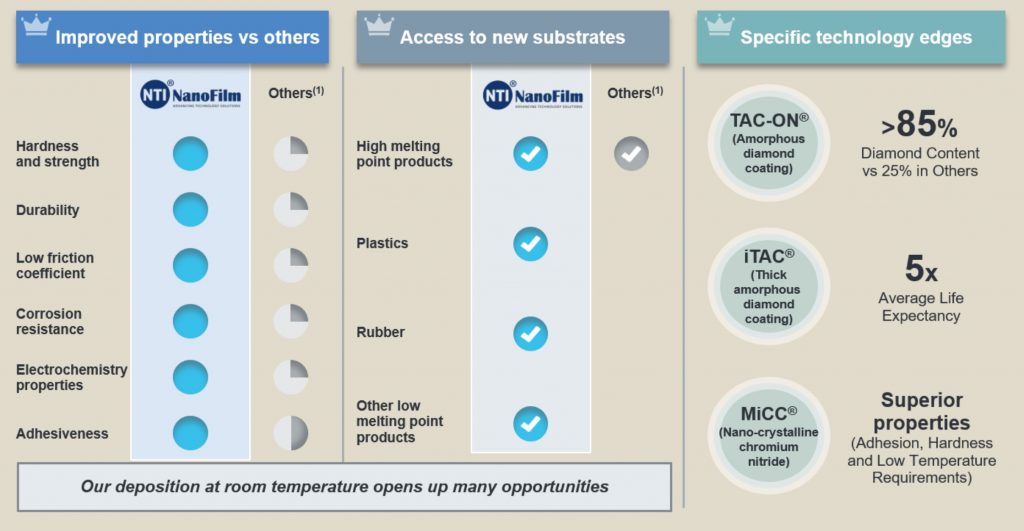

Based on the chart below, Nanofilm Technologies’ FCVA technique is way ahead of industry standards.

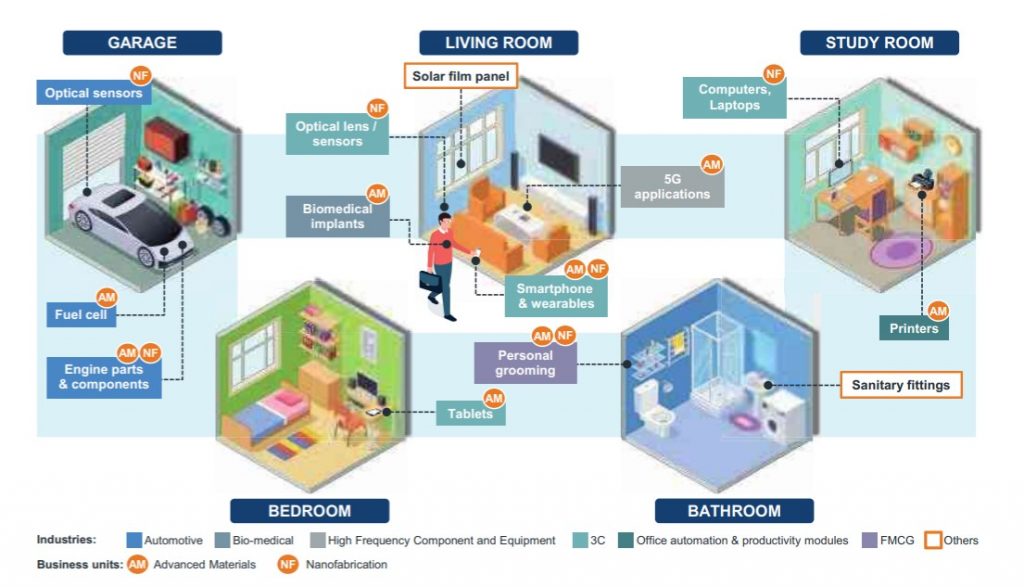

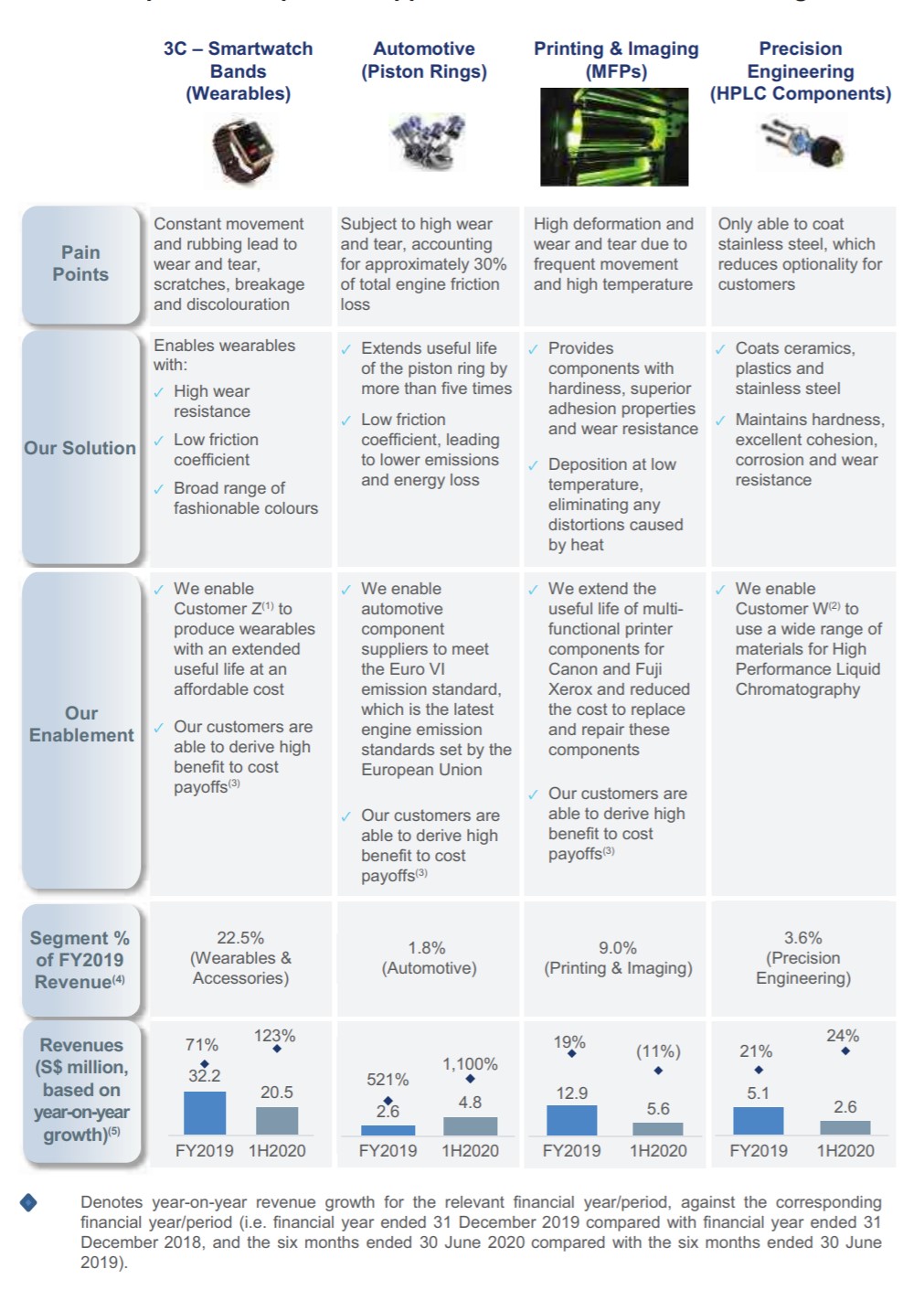

The materials produced have multiple usages within industry, as set out below:

I’m not a specialist in this area, so it’s tough to comment meaningfully beyond what I read in the prospectus.

The industry consultant Frost and Sullivan does seem very excited by the technology though.

FYI we’ll share commentary on the 2020 crisis every weekend going forward, so for those of you who haven’t signed up for our mailing list, please do – its absolutely free.

It’s a weekly newsletter that goes out every Sunday, and rounds up the week’s posts so you never miss anything.

[mailmunch-form id=”928667″]

Very strong institutional demand

Institutional demand for this IPO is VERY HOT.

Per Reuters:

The bookbuild portion of Singapore’s Nanofilm Technologies International’s up to S$510 million ($375 million) initial public offering (IPO) has been subscribed about 19 times, two sources with knowledge of the matter said on Friday.

Demand for the bookbuild segment came in at about S$4.4 billion versus the S$230 million worth of shares being offered, said one of the sources who declined to be named as the information is not public.

“This is a total blow out. We had to stop taking orders early,” said another source.

If you look at the 13 cornerstone investors, there are very big names like Temasek, Aberdeen, JPAM, Fullerton, Lion Global etc.

- Aberdeen Standard Investments (Asia) Limited,

- AIA Investment Management Private Limited,

- Avanda Investment Management Pte Ltd,

- Credit Suisse AG, Singapore Branch and Credit Suisse AG, Hong Kong Branch (on behalf of certain of their private banking clients),

- Eastspring Investments (Singapore) Limited,

- Employees Provident Fund Board,

- Fullerton Fund Management Company Ltd.,

- JPMorgan Asset Management (Singapore) Limited,

- Lion Global Investors Limited,

- Nikko Asset Management Asia Limited,

- Principal Asset Management (S) Pte Ltd,

- SMALLCAP World Fund, Inc. and American Funds Insurance Series – Global Small Capitalization Fund (which are funds advised by Capital Research and Management Company), and

- Venezio Investments Pte. Ltd.

So whether you like it or not, institutional investors love this IPO, which is a very strong signal.

The 13 cornerstones above have already mopped up more than 50% of the shares on offer.

And with the hot institutional demand, I’m pretty sure most of the rest has already been filled.

In fact the public offering seems like it was more of an afterthought, to ensure retail investors don’t feel left out. The public offer here is a tiny $10 million (out of the total $470 million).

That’s a ridiculous 2% of the offering size.

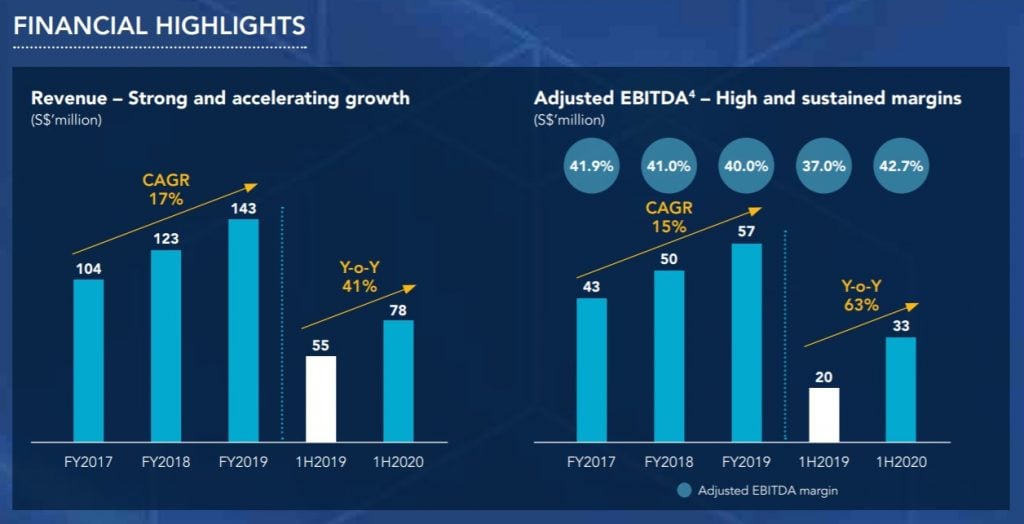

Strong Growth and good margins

As you would expect for a tech company like this, growth is very strong.

17% annualized growth over the past 3 years, and 41% year on year growth for 1H2020.

I would suspect that the big growth in 1H2020 is partly due to the COVID lockdown driving demand for certain tech products, so it may not be replicated going forward.

Whatever the case, the long-term growth trend is still very strong.

Margins are also very good, coming in at around 40%.

Reasonable Valuations

The Price/Earnings Ratio (PE) using 1H2020 numbers (annualized) is 42.

That’s actually very reasonable for a high growth company like this.

Market cap post listing is a tiny S$1.7 billion.

For a high growth company with supposedly best in class technology, the valuations are actually very reasonable. Especially considering the frothy IPO scene we are in globally now.

What I don’t like about Nanofilm Technologies

There are a couple of points I don’t like about Nano Technologies though.

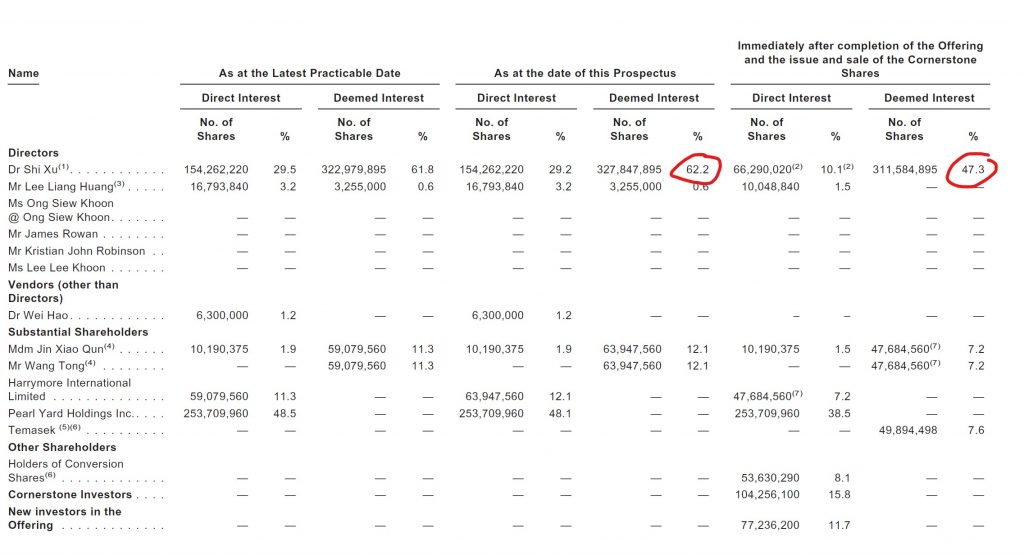

Founder is “cashing out”

Per Business Times:

Nanofilm’s founder and executive chairman Shi Xu will see a S$157.7 million payday after the sale of some 60.9 million shares in his name. Meanwhile, chief executive officer Lee Liang Huang and company executive Wei Hao will be selling 10 million and 6.3 million shares respectively.

And as you can see in the chart above, the founder Dr Shi Xu is selling out.

His stake will be reduced from 62.2% to 47.3% post-IPO, which is a selling out of $157 million.

No reason was given for this, and this is a part I don’t like.

I always feel that when a founder sells out at IPO, whether consciously or not there is potential for a drop in motivation level. I mean if you gave me $150 million I would probably be a bit less motivated to grow my company at all costs, because whatever happens going forward my financial security is already secured.

So I would have liked it a lot more if the founder retained his entire stake, like some of the other big IPOs like SEA, Facebook, Alipay etc. If the stock doubles from here, that $150 million could become $300 million. So why sell out early on?

A couple of question marks here.

Concentration risk from “Customer Z”

There’s also big concentration risk, because one customer accounts for 56% of the 1H2020 revenue:

Our largest customer (who is an end-customer) accounted for approximately 50.1%, 45.6%, 51.1%, 43.3% and 56.5% of our revenue (which includes sales to its contract manufacturers) for the financial years ended 31 December 2017, 2018 and 2019, and the six months ended 30 June 2019 and 2020, respectively.

Our largest customer’s revenue contribution is primarily in our Advanced Materials BU segment, although we supply nanoproducts under our Nanofabrication BU to this customer as well.

Our top five customers (both direct customers and end-customers, including our largest customer) in each year overall account for approximately 82.6%, 67.5%, 72.8%, 67.3% and 81.9% of our revenue for the financial years ended 31 December 2017, 2018 and 2019, and the six months ended 30 June 2019 and 2020, respectively

Whoever Customer Z is, it drove a big part of the revenue increase – rising from 43% in 1H2019 to 56% in 1H2020.

The name of Customer Z cannot be disclosed for confidentiality reasons, but it is said to be “a global technology company that designs, develops and sells consumer electronics, computer software and online services”.

My guess is that this is Apple.

If so, Apple is known for being tough negotiators and squeezing their suppliers on margins, which is not good. The big jump in revenue in 1H2020 may also not be replicated going forward because the COVID driven demand for tech products is a one-off tail wind. Once consumers get a new laptop (or Apple Watch), they’re not buying another for a few years.

But to be really honest, I could be wrong on this one, it’s just an educated hunch.

Just how good is the Nanofilm technology?

The key to the Nanofilm IPO to me, is just how good is the technology.

Is it really the case that the technology is amazing, way ahead of industry standards, and tough for competitors to catch up?

It’s tough to find much information on this publicly, because Nanofilm Technologies is mainly B2B, so there aren’t that many customer reviews to pull up.

Based on my checks, the story generally holds up, but I cannot rule out the possibility of potential new competition down the road.

So I would say I’m cautiously optimistic on their claims. Especially so given the strong institutional backing.

But if you’re in the materials industry and have something to share, do leave anonymous comment below!

Nanofilm IPO Offering details

|

Events |

Timing |

|

Offering price |

S$2.59 per share |

|

Opening time and date of IPO |

23 October 2020, 6pm |

|

Closing time and date of IPO |

28 October 2020, 12pm |

|

Balloting of applications for IPO |

29 October 2020 |

|

Commence trading |

30 October 2020, 9am |

We only have until Wednesday 28 October to “press button”. Not a lot of time, so do it soon if you’re keen.

The public offer is tiny though – 3.9 million shares, totalling $10 million out of the total $470.

So frankly speaking, don’t get your hopes up about getting an allocation for this one.

Do I like Nanofilm Technologies IPO?

I actually really like the Nanofilm Technologies IPO.

I’m willing to accept the company’s claims as to its market leading technology, and the valuations are very reasonable for a high growth tech company in today’s frothy IPO climate. Institutional demand for this IPO is also off the charts, and the list of cornerstones are amazingly strong.

I don’t like the part where the founder sells down though. Raises a bit of a red flag to me – does he know something we don’t?

The concentration risk is worth looking out for in the short term too. If Customer Z cuts purchases, it will make the short term earnings look very bad, which will hit the share price.

But longer term, it all goes back to the strength of the technology. If the materials are as good as they appear to be, then there shouldn’t be a problem finding buyers in the industry.

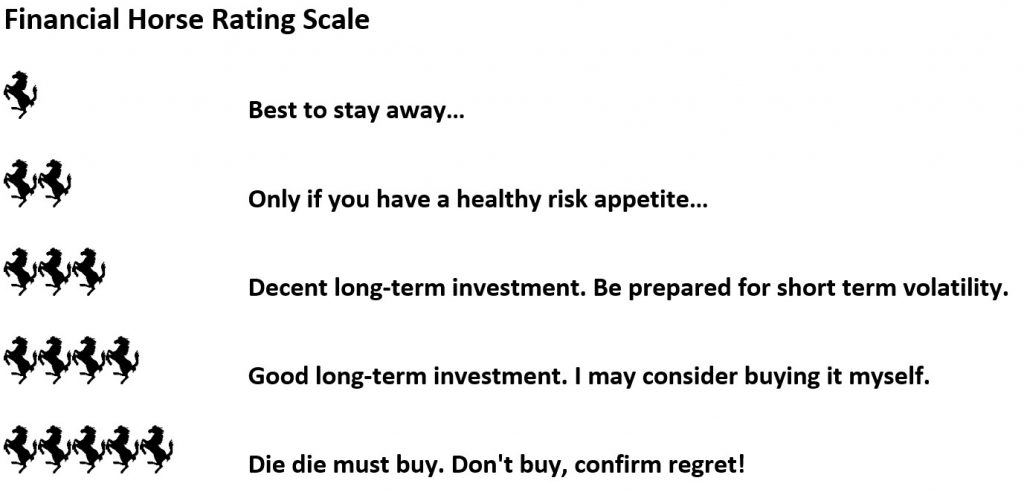

So I’ll give Nanofilm Technologies a 3.75 horse rating.

I would give Nanofilm a 4 – 4.5 Horse rating if I were able to independently verify the claims as to Nanofilm’s technological superiority (and difficulty in replicating it by competitors). Unfortunately I can’t – but let me know if you have any information on this!

Will I be subscribing for the Nanofilm Technologies IPO?

That said, I’ll probably give the IPO a miss.

The public tranche is so small that the chances of getting any are very slim. And even if you do get it, it’s probably going to be a tiny allocation that isn’t meaningful.

I’ll wait for the share to start trading on the open market, before deciding whether to pick up some.

Nanofilm Technologies IPO Rating

As always, this article is written on 24 October 2020 and will not be updated going forward. Latest thoughts (and my stock watch and personal portfolio) are available on Patron.

Share your comments below!

Support the site as a Patron and get access to my personal stock watch list, as well as my personal portfolio allocation.

Do like and follow our Facebook Page, or join the Telegram Channel. Never miss another post from Financial Horse!

Join our Facebook Group to continue the discussion, everyone is welcome!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Both are THE best quality investment courses available to Singapore investors out there!