![]()

In the recent Financial Horse Giveaway, I invited readers to make submissions of companies they wanted Financial Horse to review. Singtel was the first runner up, so without further ado, here is my take on Singtel!

Basics: What is Singtel?

Singapore Telecommunications Limited (Z74.SI) is a Singapore teleco company that I am sure every Singaporean knows about.

SingTel’s description of themselves in their factsheet is actually pretty good:

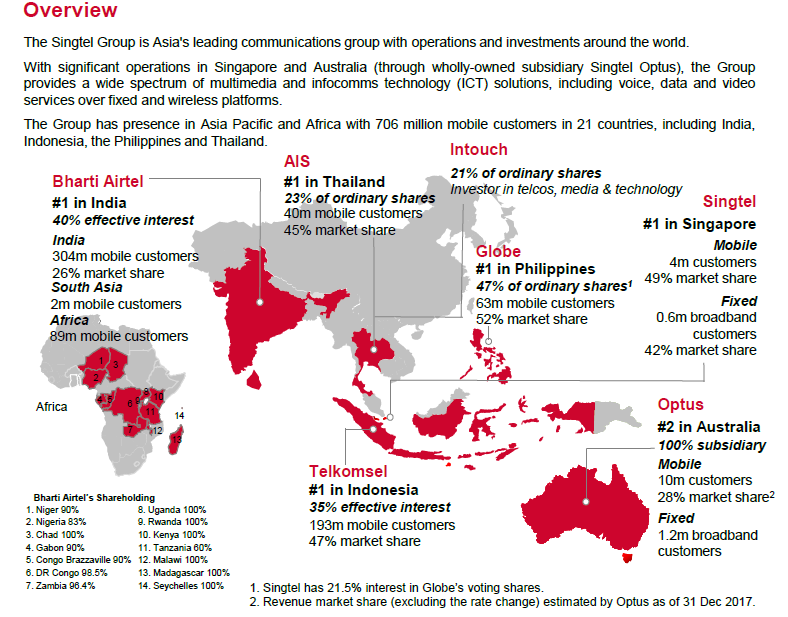

The Singtel Group is Asia’s leading communications group with operations and investments around the world.

With significant operations in Singapore and Australia (through wholly-owned subsidiary Singtel Optus), the Group provides a wide spectrum of multimedia and infocomms technology (ICT) solutions, including voice, data and video services over fixed and wireless platforms.

The Group has presence in Asia Pacific and Africa with 706 million mobile customers in 21 countries, including India, Indonesia, the Philippines and Thailand.

In other words, Singtel is a Singapore/Australian telco company (100% stake in these operations), with large shareholdings in the local telcos in Indonesia, Phillipines, Thailand and India.

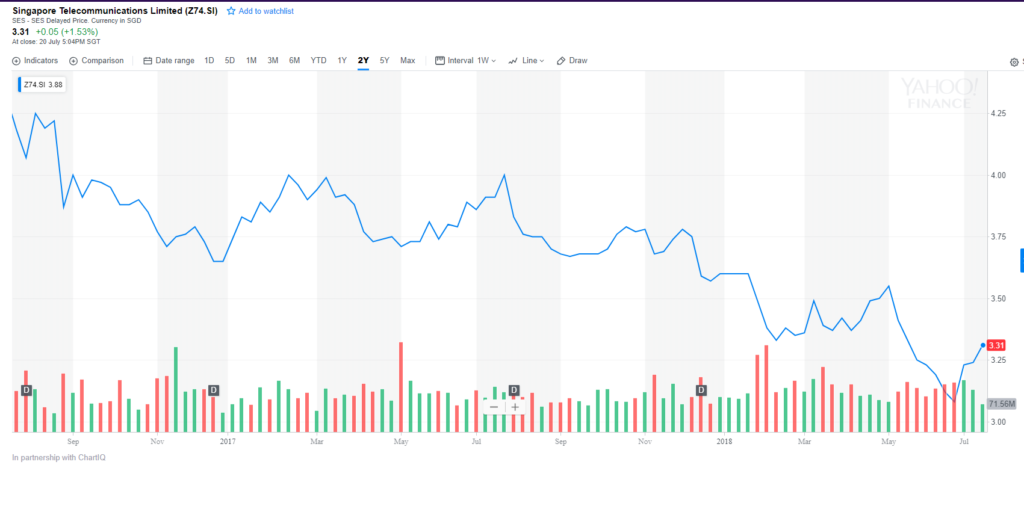

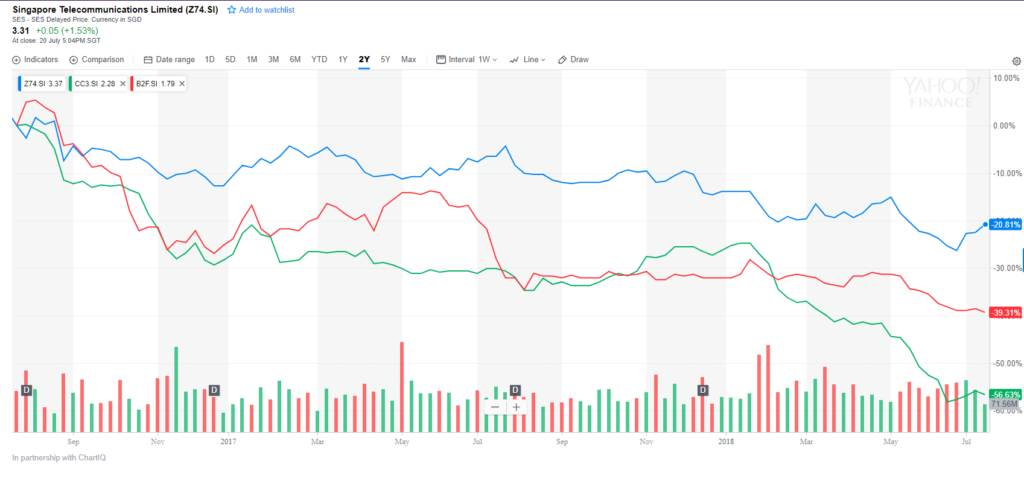

This is that their 2 year share price looks like, and it’s not pretty.

All 3 local telcos have been getting hit by a triple whammy of price conscious consumers, increased competitions and the upcoming entry of a fourth market entrant in TPG Telco. Overlaid against the price performance of Starhub and M1, Singtel doesn’t look as bad (green is Starhub, red is M1).

What I like about Singtel

Valuation

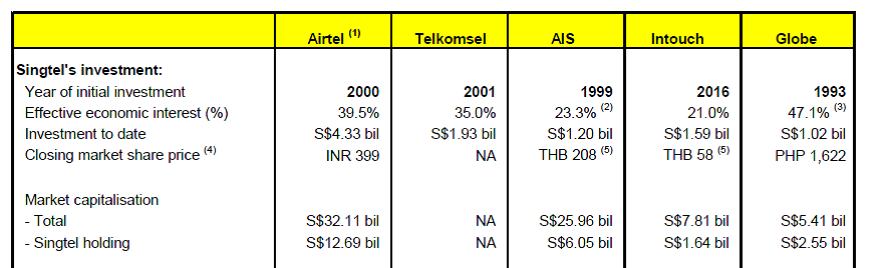

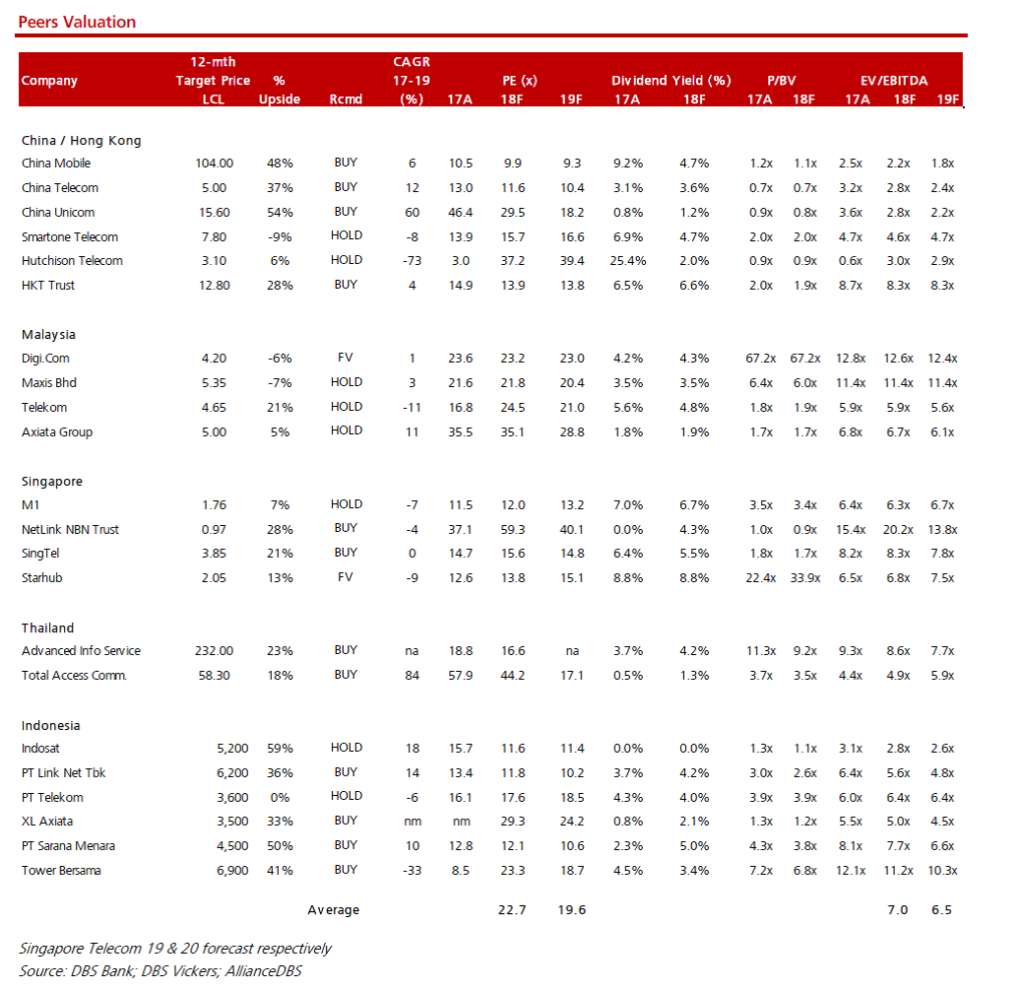

DBS Research has a fantastic table that compares Singtel’s valuation metrics against its competitors in Singapore and across Asia.

Couple of observations:

- Singtel’s P/B ratio is much better than M1 or Starhub. It’s 1.8-1.7 P/B ratio looks surprisingly attractive.

- Singtel’s P/E ratio is higher, and its dividend yield is lower than M1 and Starhub. Given that Singtel is far more diversified regionally, I think this is probably fair.

From a pure valuation perspective, Singtel looks like its trading cheaper than M1 or Starhub. Unfortunately, this isn’t a fair comparison, because Singtel has significant regional investments (about 79% of its earnings comes from outside Singapore), whereas M1 or Starhub are purely Singapore plays. I would like to say it’s a win for Singtel on valuations, but it really isn’t so simple.

Diversified across Asia

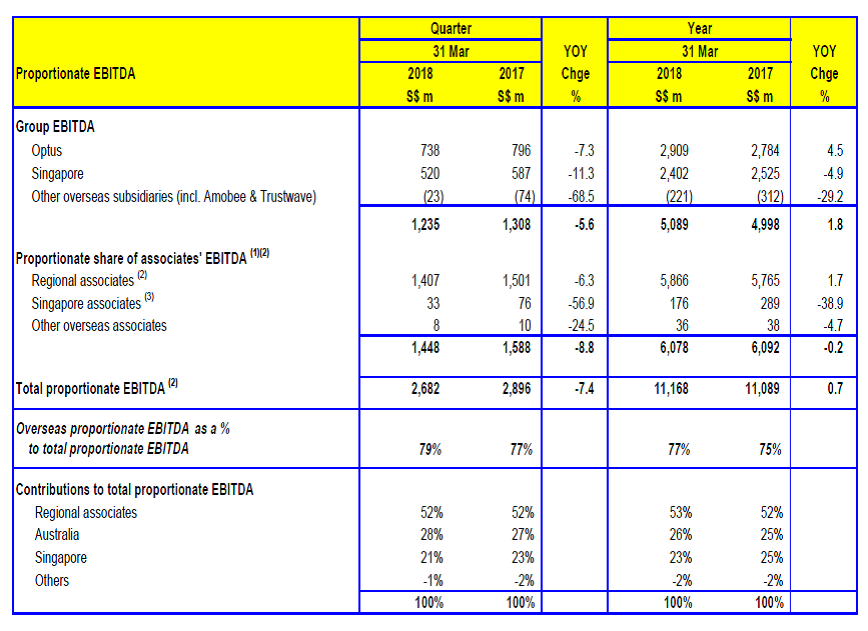

Simply put, what makes Singtel so different from M1 and Starhub, is its significant investment in other regional telcos. As at the latest quarter (Q1 2018), only about 21% of its earnings comes from Singapore.

Depending on how you see it, this can both be a good or bad thing. It’s good in that it smooths out earnings. Currently, the Singapore market is in a bit of a rough spot due to increased competition and potential entry of a fourth telco, so there has been a drop in earnings from the Singapore operations. However, improving earnings from its regional operations means that holistically, Singtel’s earnings are relatively stable.

On the flip side, being so diversified means that it can be hard to have a sustained growth in earnings. Even if the Singapore market were to pick up, Singtel may face difficulties in their Indian or Australian operations, which then creates a drag on earnings and impacts share price. By contrast, with the other pure Singapore players like M1 or Starhub, you know that once the Singapore market recovers, their share prices are going to jump.

It’s quite hard to call a winner here. It really depends on whether you think “big is good”, or you prefer a small, nimble, and focussed player.

Operational performance of business units

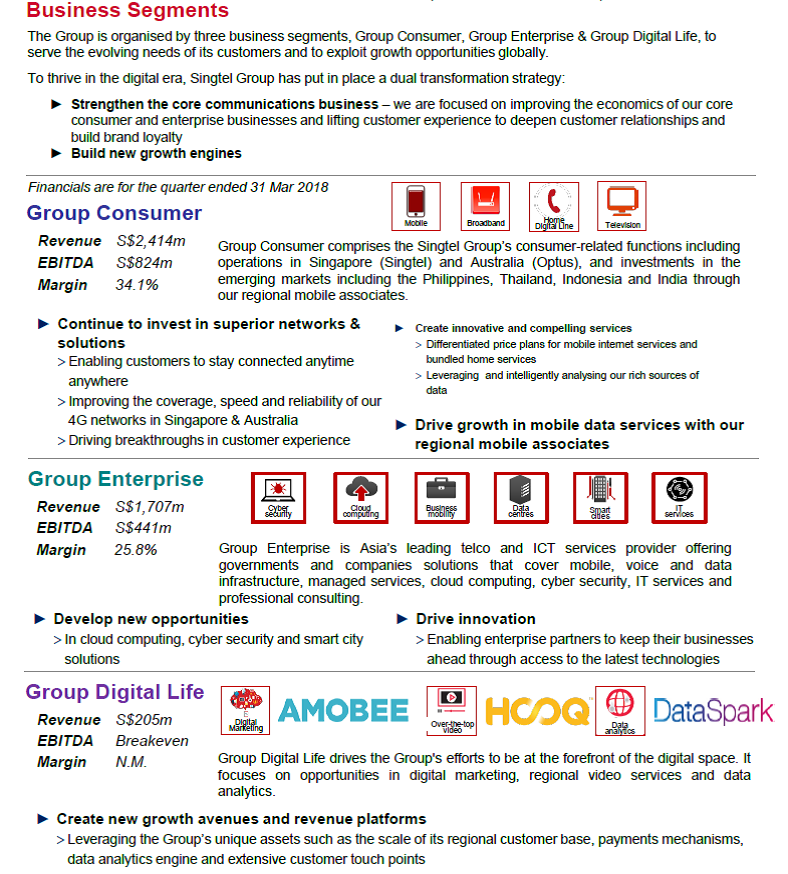

Let’s dive deeper into the various business units. Broadly, Singtel is split into 3 parts:

- Group Consumer: This is basically the consumer arm that you and I know Singtel for, when we head down to the PC Show and sign up for a new phone plan or Fibre broadband. As expected, this is their largest revenue contributor, coming in at 56% of revenue.

- Group Enterprise: This is their corporate arm, providing telco services to companies and governments. This is their second largest revenue contributor, accounting for 39% of revenue.

- Group Digital Life: I like to think of this as the “Startup” arm, where the companies essentially compete in the startup space, in services such as video streaming, digital marketing, data analytics etc. It’s the area of the company that’s showing the greatest growth (about 100% year on year), but it’s really too small to be meaningful for now. It contributes only about 4% of revenue.

There’s a lot of information disclosed in the financial reports and MD&A, so do take a look if you need more information. But my takeaway (after painstakingly crawling through them) is this:

- The Singapore business is competitive. Expect to see declines in mid single digits.

- The Australia business is okay, but nothing to shout about. Expect low single digit growth.

- For the other markets (Indonesia, Phillipines, Thailand and India), Singtel merely takes up equity stakes in the respective local companies. Accordingly, Singtel doesn’t have day to day management of these companies, and much will depend on how well the company is run by the respective management teams. Forex movements come into play as well.

Given how broadly diversified Singtel is, it’s hard to look at the performance of all the various business units across all geographies and clearly say that Singtel is a winner, or a loser. My personal thoughts though are these:

I don’t like the Singapore telco business over the next 12 months. With TPG Telco coming in, and increased competition from the mobile virtual network operator (MVNO, basically companies like Circles.Life that leverage on existing infrastructure), I expect margins to decline going forward.

I don’t know much about the Australian business, but looking at the numbers coming out from there, it seems nothing to be overly excited about. Low single digit growth is about it.

The regional business troubles me as well. There’s been a lot of competition in the respective local markets these days. Perhaps the telco operator that Singtel is betting on will win. But perhaps not as well. At the same time, there’s been a lot of adverse currency movement coming out from emerging Asian markets due to Trump and trade war fears, so Singtel’s earnings when restated in SGD are not going to look good.

Dividend

In FY2017, Singtel paid a 20.5 cents dividend, which using Friday’s share price of S$3.31, works out to a 6.2% trailing yield. Not too bad indeed, that’s almost like a REIT!

Going forward, management has stated that:

Barring unforeseen circumstances, it expects to maintain its ordinary dividends at 17.5 cents per share for the next two financial years and thereafter revert to the payout ratio of between 60% to 75% of its underlying net profit.

At 17.5 cents, that works out to a 5.3% forward yield. It’s still quite attractive though.

The FY2017 dividend was a payout of 81% of net profit, and its forward dividend is about 60% to 75% of net profit. It’s definitely more sustainable than the numbers coming out from M1 or Starhub, lower payout ratio, and Singtel has the added bonus of having a more diversified income base.

Personally I think this 5.3% yield is sustainable going forward. However, it’s important not to get too fixated purely on yield alone. Singtel’s share price has fallen 15% the past year, which is basically 3 years worth of dividends lost at one go. This isn’t like a REIT where at the end of the day, you’re still owning real estate. With share price declines, sometimes they may never recover to the P/E multiple they once had.

What I dislike

Industry Singtel is operating in

There’s a saying from Warren Buffett that I feel is really apt here: “When a management with a reputation for brilliance tackles a business with a reputation for bad economics, it is the reputation of the business that remains intact.”

I like everything that management has done with the company. They know that in the long run, the Singapore market is not sustainable, so they expanded into Australia, Indonesia, Thailand, Philippines, India etc. They also pay a nice juicy dividend to keep shareholders happy, and are pretty prudent about keeping payout ratios sustainable.

But none of these change the fact that at the end of the day, Singtel is a telco company. 96% of their earnings comes from legacy telco businesses, things like subscription for a broadband connection, a monthly phone line etc. In this digital age, an internet connection is basically a commodity. If I terminate my Singtel subscription and switch to M1 tomorrow, there is absolutely no impact to me from a consumer point of view (leaving aside things like price). These days, the money to be made lies further up the value chain, in the companies that are leveraging on the internet to provide services. So Google, Facebook, Amazon, Alibaba, these guys are making the big bucks and juicy margins, while the Singtels and Verizons of the world are stuck providing a basic utility. It’s an absolutely horrible place to be in for any company.

I have little doubt that Singtel’s management is fully aware of this as well. They are touting their efforts to build up Group Digital Life, which provides value added services such as video streaming and data analytics, in the hopes that one day it can be a significant revenue contributor. The numbers look good, 100% growth year on year, but at the end of the day, it only contributes about 4% of revenue. Whether it can grow fast enough to make up for the core business remains to be seen.

So if we leave aside all the new ventures for now, what we are left with, is a telco company with core businesses in Singapore and Australia, and large stakes in regional telcos. And in the longer term (10 to 20 years timeframe), that’s just not very attractive to me.

Singapore Business

At the Singtel Investor Day 2018 – Q&A, Singtel had this to say (as reported by DBS Research):

What’s Singtel’s view on topline growth in Singapore? Mobile revenues are likely to decline over the course of FY19, with the entry of TPG. Over the medium term, Singtel believes that 4-players cannot survive independently and there will be room for consolidation in the market. Singtel’s IoT strategy is primarily focused on the enterprise segment, which is expected to account for ~75-80% IoT revenues of Singtel.

That’s absolutely spot-on to me. I have my own theories on why the government wanted to open up the telco space to TPG, but that’s a topic for another day. From a pure economics standpoint, I don’t see any way 4 players can survive in the Singapore telco market. The pie just isn’t big enough. Eventually, either M1 or Starhub is going to get bought out, and we’ll be left with 3 players again. Perhaps then margins can start to improve. But in the meantime, all existing players are going to see increased competition, and declining revenue.

But this is all in the short term. In the longer term, I still believe that telco operations will become increasingly commoditised, and existing players will lose pricing power. And don’t forget that Singapore’s telco market is far more developed than the other countries Singtel is operating in. Over time, I expect a similar story to play out in those countries as well.

Expansion into new sectors may not bear fruit

The one saving grace I can think of, is Singtel’s efforts into Group Digital Life. If Singtel can find a way to diversify their income away from its core telco operations, and diversify into higher value add businesses like video streaming, then the entire equation will change. Unfortunately, this is a huge if. In this space, you are now competing with global behemoths like Alibaba, Tencent Holdings, Google, Amazon, Microsoft etc. Perhaps Singtel can find a way to carve a niche out for itself. As an investor, I prefer not to speculate. If and when that happens, I will re-evaluate my thesis on Singtel.

Sum of parts analysis

DBS Research ran a sum of the parts (SOTP) analysis on Singtel and concluded that this worked out to S$3.70 per share (for newer investors, a sum of the parts analysis determines what individual business units would be worth if Singtel is broken up and spun off individually or acquired by another company).

Now I don’t doubt DBS Research’s numbers at all. I think a S$3.70 SOTP fair value sounds about right. Unfortunately the thing I have learnt about SOTP analysis is that sometimes it’s just that. Just because your SOTP numbers show that the company is 10% overvalued does not mean that the market will ever respect that. The share price can trade at an undervalue for many years while the core business stagnates, and eventually your SOTP numbers catch down to the market price. Was the SOTP analysis right or was the market right? In reality, it doesn’t even matter because you can’t realise the gains on your investment.

Closing Thoughts

When I started my research into Singtel, I had very high hopes for the company. A regionally diversified, Temasek backed company trading at a 5.3% forward yield? Where do I sign up?

Unfortunately the truth of the matter is far more complicated than that. I have a lot of reservations about investing in this company. I don’t like the near term outlook, and I don’t particularly like the long term outlook. I suppose an argument can be made that Singtel should be viewed as a defensive, utility stock. But what I want from such stocks are virtual monopolies. Singtel’s Singapore business is getting increasingly competitive, and I expect the same to happen to its regional ventures as well. The 5.3% dividend is likely sustainable for the next few years, but what about 10 years out, 20 years out?

I did a recent analysis into Netlink Trust (check it out here), and I really liked what I saw. Netlink has a virtual monopoly on fibre infrastructure in Singapore, huge barriers of entry to deter any potential competitor (massive capex costs to compete) and stable cash flow due to its monopoly and regulated environment. And it’s trading at a 6% yield.

If I really wanted a telco play, I would actually pick Netlink Trust over Singtel. It’s about everything I want from a defensive, utility stock. (Full disclosure: I bought Netlink Trust during the recent dip, and may add on price weakness)

It’s hard to give a Financial Horse rating for this one, but I’ll probably settle on 2.5 Financial Horses. I really like what management has done with the company, with its regional diversification, 5.3% yield, and its investments into new ventures. But I just don’t like the industry it is operating in. If I really had to invest in Singtel, I would probably want a 6% yield as a margin of safety, which assuming a 17.5 cents dividend, works out to S$2.91 per share. At its current price of S$3.31, that’s a long way to fall.

Financial Horse – Singtel Rating

![]()

Rating Scale:

Financial Horse has a set of 7 Commandments for Successful Investing, that I ask myself before making every investment, and that I will never break regardless of the situation. Enter your email below to receive a copy in your inbox!

[mc4wp_form id=”173″]

Enjoyed this article? Like our Facebook Page for more great articles, or join the Facebook Group to continue the discussion!

Thanks for the comprehensive review.

As you correctly pointed out “the money to be made lies further up the value chain, in the companies that are leveraging on the internet to provide services”. I look forward to Singtel doing more more partnerships (even becoming a shareholder) with “Alibaba, Tencent Holdings, Google, Amazon, Microsoft”, which unfortunately have been lacking for many years.

Thanks for the comment. I do agree that Singtel needs to find a way to diversify their income stream. The million dollar question is how to do this.

We’ll return article. I will like to explore the potential of Enterprise Business as it has been contributing significantly in Singapore. They are trying to do the same in Australia. If it succeeds, it will form a robust and stable contribution to its bottom line. Telcomsel has been a huge contributor in the past years except recently due to competition. Can it regain its market dominance in Indonesia. On balance, I feel that your well research piece may have been a little biased on the downside.

Thanks for sharing your thoughts. I might not have touched on Enterprise Business too much in my article, but the arguments that this is increasingly a commoditised business with little pricing power would hold true to some extent. But we shall see…

A very detail write up. I do suspect that Singtel will drop further within the next few months. But over the long run of 3 years and above, I do expect it to increase.

I am vested in this counter.

There seems to be a lot of strong retail support for this counter. Only time will tell who is right. Good luck with your investments, and thanks for dropping by! 🙂

interesting.. from your previous article, you mentioned its not worthwhile to compare PE for netlink. instead FCF should be used instead.

what would be the FCF comparision for ST vs Netlink? (would it be apple to apple if we compare it this way?)

i am vested in both. but i am deciding which one to add more, due to the current price weakness.

Unfortunately not. Netlink is a BT, so a REIT like analysis has to be used for Netlink (ie. FCF, not PE). Sintel is an operating company, so a company like analysis has to be used (ie. PE ratios, EV/EBIDTA etc). The nature of the corporate structures are different unfortunately. Netlink is also a pure Singapore play, while Singtel is a regional play.

To add, with a company, the management can invest in new areas of growth to diversify their income stream. With a BT/REIT, you’re basically stuck with the underlying assets, whether its real estate or fibre assets. If the underlying assets are no longer income generating or not as relevant, it can be very hard to diversify.

what would be a peer comparision for netlink?

That’s tricky, there’s no real equivalent to netlink in terms of asset class. The closest I can think of is something like Parkway life REIT, with its long term leases and built in step up rents.

Very good article. Thanks for the insight. I wanted to add more Singtel shares, but after reading the article I have a second thought. Netlink May be better option.

One question: how can I search for 5 rated stocks in your site.

Hello and welcome to Financial Horse! I think Singtel is still an okay buy in the medium term, it’s the near term and longer term that concern me.

I haven’t added that function to the site yet. But to answer your question, the only 5 rated stock I have so far is Astrea IV Bonds (the temasek bonds). Those were at IPO prices though, they’re gone up a fair bit on the open market. 🙂

https://financialhorse.com/astrea-bonds/

Thanks for the analysis. I own some Singtel share. You mention that “96% of the revenue comes from legacy telcos business”. How did you get this figure? The group enterprise business have contributed significantly to profit and they are not part of them “legacy telcos”. It offerings include Cybersecurity (via 100% owned Trustwave), IT services and DC.

I took all the SBUs other than Group Digital Life. It’s a good point now that you mentioned it. Cybersecurity is about 3.4% of their latest quarterly revenue, so perhaps the number should be somewhere in the low 90s. I’m not so sure if I would count IT services as a non-legacy business though.