So… SPH had a monster of a rally last week.

It went from $1.05 to $1.25, a massive 20% increase.

Quite a few of you have asked for a review of SPH Holdings.

SPH Holdings is a really interesting media-property hybrid, and I was really excited to do a deep dive.

And boy… did they not disappoint.

Note: The research for this article, and most of the charts here, are sourced from ShareInvestor Webpro. It’s a great way to quickly perform research on Singapore stocks, far more comprehensive and flexible than other options like Yahoo Finance.

You can learn more in my review on ShareInvestor Webpro here.

Basics: What is SPH?

SPH Holdings, or Singapore Press Holdings, started out as a media company.

They own all the big newspapers in Singapore – Straits Times, Lianhe Wanbao, New Paper, Berita Harian etc.

As they matured, they took all that cash flow and plowed it into property. Because what else would you do with all that money right?

So today, SPH is a company of 2 halves.

There is a (1) media business that owns the newspapers (monetises via subscription and ads), and (2) a property business. They also have other investments (M1 being a notable example), but this isn’t big enough to move the needle.

Financial Results of SPH

FY2020 financial results are set out above, and they’re really interesting. Basically:

- The media business is a disaster, with revenues down 22.8% year on year

- The property business is resilient (or as resilient as it can be in COVID-19)

Let’s discuss both separately.

SPH’s Media Business

Ad revenue – Will it recover post COVID, or is it dead forever?

UOB Kay Hian has a great writeup on this:

The media segment print ad revenue dropped 32.9% yoy in its worst annual decline as advertisers scaled down on marketing budgets due to the disruption of the pandemic. The hit to advertising spending is broad-based, including digital ads, which declined 6.2% on a yoy basis. We note a slight reduction in the decline for 4QFY20 as compared to the previous quarter, though the drop remains significant in nature.

Management noted a lagged effect in advertising revenue recovery, as the general economy had recovered during previous business cycles, given the discretionary nature of advertising spending. However, the structural challenges faced by print media could impede such an occurrence this time around.

Newspaper used to be the best business to be in

In the good ol days (before the internet), owning a newspaper was just about one of the best businesses you could start.

The business model went like this:

- Start a newspaper

- Sell them cheap / give them away, and make sure everyone reads your paper

- Sell ads to advertisers

- Raise ad prices

Before the internet, if an advertiser wanted to reach their target audience, a newspaper was probably the best option available.

You had guaranteed circulation and readership amongst the target audience.

And newspapers have strong network effects – once you get ad revenue you can spend money on better content, increasing readership, further increasing ad revenue.

So newspapers tend towards monopolies – giving them massive pricing power. They can charge whatever rate they wanted and advertisers would pay.

The rise of the internet

Then of course, the internet came along.

If you’re an advertiser today, and you want to get a message out to your consumer, you have alternatives:

- Google Search Ads

- Google Display Ads

- Facebook Ads

- Instagram Ads

- Influencer Marketing

Now the key difference with “old school” marketing is that modern marketing allows for hyper targeting.

Let’s say you’re a bag shop selling to young professional ladies.

With newspapers, maybe you can pick between Business Times or Straits Times. But at the end of the day you just pay for the ad. Everybody who reads the newspaper will see it, not just the young professional ladies. So that’s inefficient.

Whereas with modern marketing, you can go to Google / Facebook and hyper-target only your specific audience. Maybe females in the 25 – 34 age group, with a certain education background.

That’s been an absolute gamechanger for the advertising industry.

And advertisers love it.

Can’t put the genie back in the bottle

You can’t put the genie back in the bottle for this one.

Print advertising spend was already dying pre-COVID, and COVID merely accelerated these trends, in a big way:

What can SPH do?

So you know that advertising revenue for print media will decline going forward, because of the rise of the Googles and Facebooks.

The latest tech earnings show that – total advertising spend has plunged, but Google and Facebook are still doing really well. Advertisers have pulled all their offline ad spending and moved them onto Google/Facebook.

So what can SPH do?

The way that Financial Times / New York Times etc responded, is that they shifted away from ad revenue, and towards a subscription model.

SPH is definitely trying something similar as well, and it’s showing results.

Can this offset the decline in Ads?

At the end of the day though, ad revenue at 30% is much bigger than subscription revenue at 16%.

So the key question – Will the rise in subscription income offset the fall in ad revenue?

Only time will tell, but my gut feel is that it won’t.

The core media business will probably decline for years to come, before finding a bottom eventually (if at all). The rise of the internet has completely upended this business model, and frankly, I don’t see a way back.

These days, anyone can create a publication – you get everyone from Mothership to a small blogger, each with their own ultra-niche audience.

Big newspaper like Straits Times will still be around, but I don’t think they ever go back to the kind of dominance they had in the past.

The world has changed.

BTW – we share commentary on the COVID crisis every weekend, so please sign up for our mailing list, it’s absolutely free.

It’s a weekly newsletter that goes out every Sunday, and rounds up the week’s posts so you never miss anything.

Don’t forget also to join our Telegram Channel!

[mailmunch-form id=”928667″]

SPH’s Property Business

The other big part of the SPH business is property, which comes from 2 parts:

- 63% ownership of SPH REIT

- Student Accommodation and Aged care business (100% owned by SPH)

Don’t underestimate that 63% of SPH REIT.

Based on latest prices that’s worth $1.4 billion. Which btw, is a whopping 70% of SPH’s current $1.9 billion market cap.

The property business has been as resilient as you would expect in this COVID pandemic.

With all the government support and stimulus, it actually has performed better than the media business.

We had a brief look at SPH REIT recently and I thought it was a generally ok REIT, but nothing to shout about.

I think current market pricing (0.8x book value) is on the high side though.

Student Accom, Aged Care

SPH has branched out into Student Accommodation and Aged Care (for old folks) recently. According to the reports, they’re doing decently well.

Truth be told, it’s still a very small part of the business, and not meaningful just yet.

The 2 core businesses here will be media and SPH REIT.

Does SPH have core expertise in property?

My main concern with SPH being in property though, is that they don’t have that kind of specialized real estate expertise that the real players have.

You know, the BlackRock/Blackstone, CapitaLand, Mapletree etc.

Real estate is a scale business, and SPH’s real estate portfolio is tiny. They will find it hard to attract talent, source for good deals (without overpaying), attracting investors etc.

So I’m not convinced that SPH’s real estate portfolio will justify a premium valuation.

Sum of the Parts Valuation – SPH

Which is a great time to jump into valuations.

DBS Research values SPH at $1.09 based on a sum of the parts valuation:

We value SPH’s core newspaper and magazine operations at S$0.16/share based on discounted cash flow (DCF) model, SPH’s property business and other investments at S$1.89, and net debt at S$0.96.

UOB’s number is $1.61 before conglomerate discount. They applied a 30% discount which takes it to $1.12.

FH Valuation of SPH

I agree with UOB’s valuations of the property business, which is $2.26.

UOB gave the newspaper business a $0 valuation, which to be honest, I don’t think is fair because there still is value there. It is the number one newspaper in Singapore after all, and generates half of the revenue for SPH.

I will use DBS’s $0.16 value of the newspaper business (based on DCF analysis).

Less off the debt, and you get a final sum of the parts valuation of SPH of $1.77

At current price of $1.23, that works out to 0.7x book value.

Compare that against a best in class real estate player like CapitaLand which trades at 0.6x book value now, and SPH doesn’t look super attractive.

I could just buy CapitaLand and Google and get best in class exposure to real estate and media, at cheaper valuations and stronger growth prospects.

Any potential catalyst?

So the reason for the 20% jump last week, was because of rumours of a “restructuring” to “unlock shareholder’s value”.

When queried by SGX, SPH replied that:

Singapore Press Holdings Limited (“SPH”) regularly evaluates all opportunities across its portfolio with the objective of enhancing shareholder value, which may from time to time involve discussions with various parties and stakeholders. There is no assurance that any transaction will materialise or that any definitive or binding agreement will be reached. SPH will, in compliance with applicable rules, make further announcements as appropriate.

Which basically is saying nothing.

But there’s seldom smoke without fire, and my gut feel is that there’s probably some restructuring being discussed right now, and we’ll likely see it in the coming months.

Balance Sheet – SPH

A couple more points to look at then I’ll share holistic views.

Balance sheet is pretty strong, so that’s not a big concern.

Dividend – SPH

Dividend yield in the past sat at around 3%+, with an 80% payout ratio.

That’s not sustainable when the core business is in trouble, and reminds me a lot of Singtel.

The focus now is on cash conservation, so dividend has been slashed.

Trailing yield for SPH is 2% now.

SPH Shareholders

Contrary to popular belief, SPH is NOT a Temasek backed company.

They are mostly held by public shareholders.

The media laws prevent a foreigner from controlling SPH’s media business (for national security).

So the potential for restructuring is limited. The core media business will always be held by SPH.

Buyback – SPH

Much like a lot of the other companies we looked at, very active buyback during the March to April period, then stopped after.

Note: ShareInvestor WebPro is a great and very cost-effective way to do analysis like this – beats trawling through the SGX announcements one by one. If you do such analysis regularly, well worth checking it out. Our review on WebPro (and Promo Code) here.

Insider Trades – SPH

Nothing notable from insider trades, mostly directors getting their director’s remuneration in shares.

Going into property may have been the right move

Interestingly, I find that SPH is in a very similar situation to Singtel.

In the past, they had an absolutely dominant business. Best in class, strong monopoly, and insane cash flow.

But what do you do with all that cash generated?

The core business is already mature, so reinvesting it doesn’t make sense.

With Singtel, they took the money and diversified geographically.

So if SPH did the same, it would be equivalent to buying a newspaper business in Australia or South East Asia. That’s tricky though, because media is very sensitive, and it’s not easy to buy another country’s newspaper.

So SPH diversified into another business.

And of all the businesses out there, real estate is probably the easiest one to go into. As long as you buy good properties, don’t overpay, you generally do decently.

So in hindsight, I don’t actually see a lot that SPH could have done differently.

The core media business was always doomed once internet came about, and there was very little that could be done to prevent it. Diversifying the business probably makes the most sense.

Closing Thoughts: Would I buy SPH?

That said, we’re investors, and we’re in this business to make money.

My personal view is that SPH is about fairly valued right now.

There could be some upside short term as this reflation trade plays out, or as and when the restructuring news is announced.

But as a long term investor, I find it hard to be excited about SPH.

The real estate business is not best in class, so it makes little sense to me when a behemoth like CapitaLand is at a cheaper valuation and has much higher quality properties (Raffles City China, stakes in CICT, Ascendas REIT, etc).

The media business is okay, but it definitely is in secular decline. It will stabilize eventually, but really tough to say when and where.

The answer’s clear for me though, I will not invest in SPH. I just don’t see a place for it in my portfolio.

If I wanted real estate exposure I would go with the REITs / a player like CapitaLand. If I wanted media exposure I would go with Google or Facebook where the future lies.

Interestingly, I actually do own REITs, CapitaLand, Google and Facebook (full portfolio on Patron). Which I find a much better combination.

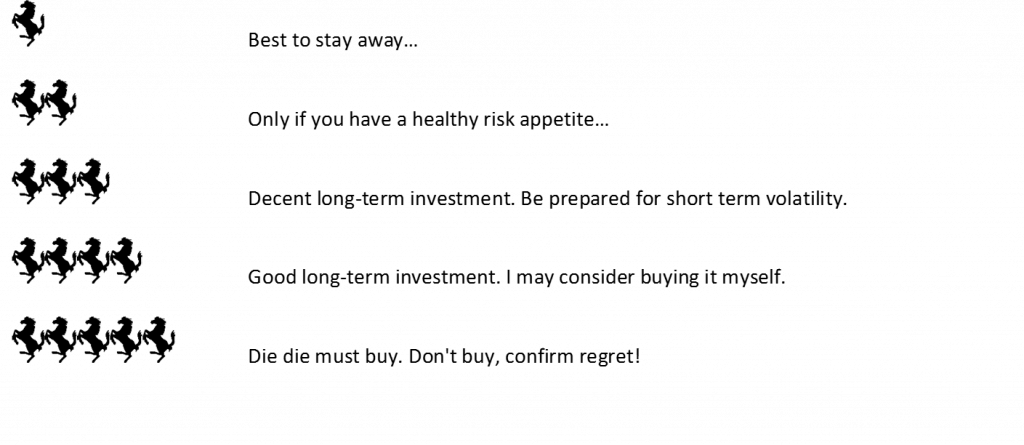

SPH is a 2 horse rating for me.

Financial Horse Rating – SPH

Financial Horse Rating Scale

As always, this article is written on 27 Nov 2020 and will not be updated going forward. Latest thoughts (and my stock watch and personal portfolio) are available on Patron.

Share your comments below!

Support the site as a Patron and get access to my personal stock watch list, as well as my personal portfolio allocation.

Do like and follow our Facebook Page, or join the Telegram Channel. Never miss another post from Financial Horse!

Join our Facebook Group to continue the discussion, everyone is welcome!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Both are THE best quality investment courses available to Singapore investors out there!

Great read! I’m curious if you have any thoughts on why CapitaLand is trading at 0.6x P/B, which to me seems rather undervalued by the market?

Yeah there’s a bit of a conglomerate discount. But SPH at 30% discount and CL at 40% discount? I would go with CapitaLand any day. 🙂

Thanks for the thoughtful, understandable, and actionable write up! You should do one for cloudflare. I find it hard to understand their biz model as it’s quite technical.

Haha they are basically a mix between a CDN and a Security platform. Their reverse proxy tech is really, really interesting. Very little alternatives in the market. 🙂

But yeah, it is pretty technical, you will need some background knowledge of how the internet works to understand Cloudflare.

yes pls do one on them!

Dead. You are very polite / kind by not talking about the weakness in the property investment in student hostels in UK. Even at $1, I wont buy.

Yeah I am not a buyer at $1 too. 🙂

I think sph need a better ceo…