Quite a few readers have reached out and asked that we do a piece on the Sembcorp Industries and Sembcorp Marine De – Merger.

It’s a very interesting deal, so I was happy to oblige.

It’s the fourth big Temasek deal in a few years – First was the CapitaLand-Ascendas deal, then Keppel Corp, then SIA’s recapitalisation, and now Sembcorp Industries – Sembcorp Marine. So Temasek has been really active these few years.

FYI we’ll share commentary on the 2020 crisis every weekend going forward, so for those of you who haven’t signed up for our mailing list, please do – its absolutely free.

It’s a weekly newsletter that goes out at noon every Sunday, and rounds up the week’s posts so you never miss anything. Sign up below (you get a free guide when you sign up):

Basics: Sembcorp Marine De – Merger from Sembcorp Industries

The de – merger deal is quite technical, but hey, that’s what Financial Horse is here for right?

Anyway, I’ll cut through all the mumbo-jumbo so you guys don’t need to read all the legal speak.

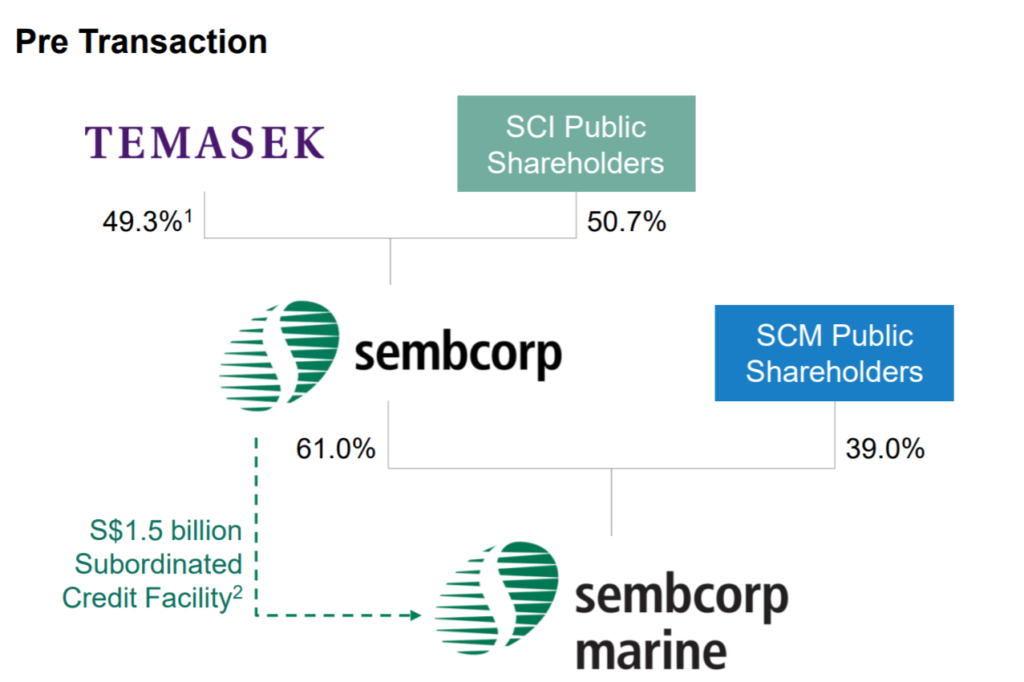

Before

This is the structure of Sembcorp Industries – Sembcorp Marine before the deal (ie. right now):

Sembcorp Industries holds 61% of Sembcorp Marine, the other 39% is held by public shareholders. Sembcorp also has a $1.5 billion loan to Sembcorp Marine.

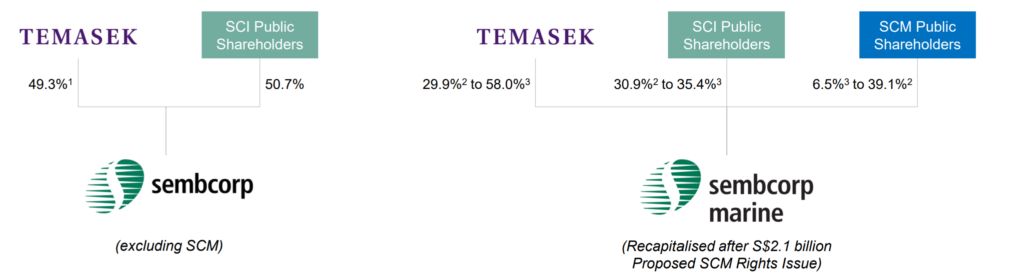

After De – Merger

After the De-Merger, this is what the structure looks like:

Sembcorp Industries and Sembcorp Marine will be separate companies, and Sembcorp Industries will no longer have a stake in it.

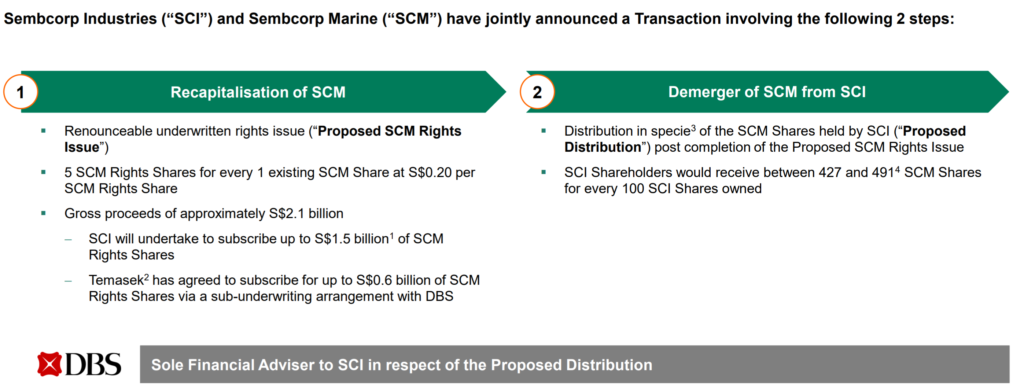

2 Step Process

The deal is executed via a 2 step process:

- Rights Issue

- Distribution in Specie

Rights Issue

Firstly, the rights issue.

This is similar to the SIA rights issue.

Basically Sembcorp Marine will do a 5 for 1 rights issue at $0.2 per share. So for every 100 shares in Sembcorp Marine, you’ll get offered 500 shares at $0.2.

At current market price, that 100 shares is worth about $50+, so you’re being asked to cough up $100 for each $50, which is quite a bit to ask from shareholders actually.

The rights issue will raise $2.1 billion in total.

Sembcorp Industries holds 61% of Sembcorp Marine so they’re on the hook for 61% of $2.1 billion (about $1.3 billion), but they will be generous and undertake to subscribe up to $1.5 billion of the new rights shares.

BTW – Sembcorp Marine will then use the $1.5 billion to repay its debt owed to Sembcorp Industries, so in a way Sembcorp Industries is just doing a debt for equity swap.

Distribution in Specie

The second part of the process is a distribution in specie.

All this means is that Sembcorp Industries will take the Sembcorp Marine shares it owns, and distributes them out to shareholders.

If you are a Sembcorp Industries shareholder, for every 100 shares in Sembcorp Industries you own, you will get about 400 shares in Sembcorp Marine (exact figure depends on how the rights issue goes, and how many shares Sembcorp Industries finally takes up).

And that’s it.

That’s how you finally achieve the de – merged structure below:

So to round it up quickly:

If you hold Sembcorp Industries (SCI)

There is nothing to do.

You just sit tight, and at the end of this deal, you will have the same number of shares in Sembcorp Industries, but you will get new shares in Sembcorp Marine (427 to 491 SCM Shares per 100 SCI Shares)

If you hold Sembcorp Marine (SCM)

You’re basically in the same position as the SIA shareholders.

You need to decide whether to take up the rights issue (5 SCM Rights Shares for every 1 SCM share – 0.20 per rights share).

Use of Proceeds

Use of proceeds will be:

- S$1.5 billion to repay the loan to Sembcorp Industries

- S$0.6 billion for working capital

Whether you like this De-Merger depends on who you are

So that’s the basics of this deal, now let’s go into some analysis.

And very simply, whether you like this deal, depends on who you are.

My personal opinion – This deal is great for Sembcorp Industries, it is not so great for Sembcorp Marine, it is great for Singapore.

Sembcorp Industries the big winner?

The market certainly feels this way, because after the deal was announced, Sembcorp Industries jumped 40%, and Sembcorp Marine dropped by 27%.

The problem here really is the Marine business. Marine is a complete disaster.

It’s been that way since the oil bust in 2015, and just when it looked like things were about to get better, we have COVID19 which is a once in a century pandemic.

Bad news for the whole world, but if you’re in the offshore&marine space, it’s really, really bad news.

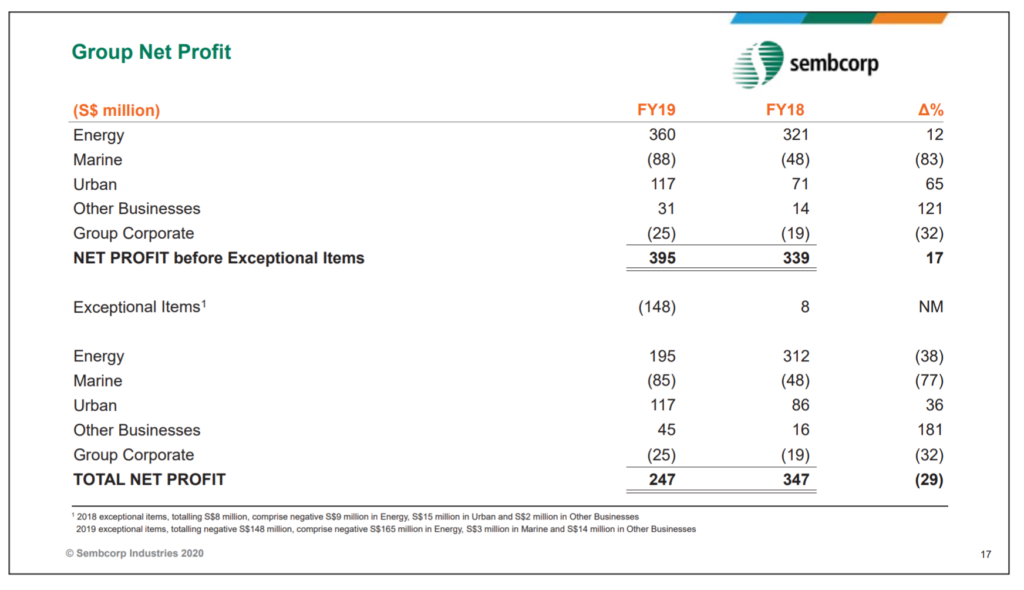

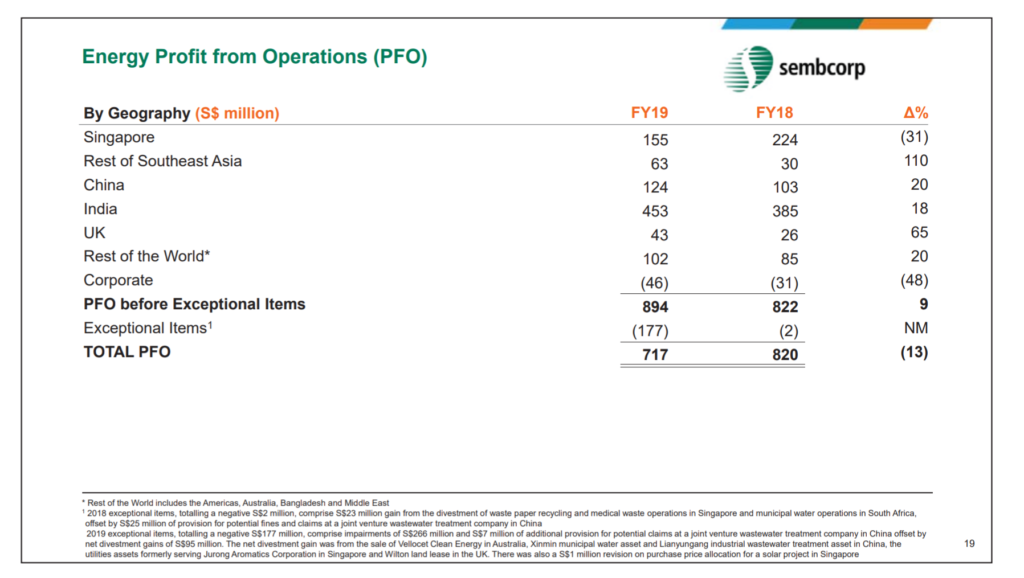

The group profit table for Sembcorp is set out below:

The Marine sector has been dragging down the entire group’s profits for a while now, and with COVID19, that’s going to get even worse.

So from a high level point of view, if you can separate the Marine business from the rest, what you’re left with is a decently profitable Energy and Urban Planning business. Once you do that, maybe capital markets will recognize the value in the company, and you get a rerating in the stock.

That’s the idea anyway, and it’s definitely worked based on the share price reaction.

Valuations

Let’s run some simple calculations.

If we take just the Energy and Urban business, that’s $477 million in earnings for FY2019.

2020 will be a tough year, so let’s just buffer in a 30% drop in earnings.

A good utilities company (eg. Cheung Kong) trades at about 10 to 11 times P/E, but Sembcorp definitely isn’t in that league.

So let’s be conservative and apply an 8 times P/E.

That will give us a share price of 1.5 (current share price is 1.95).

But don’t forget that you also get about 400+ shares in Sembcorp Marine for every 100 shares in Sembcorp Industries for free.

And if we use very conservatively the rights issue price of $0.2 per share (current share price is 0.56), that works out to another $0.8 in value per share.

So based on this very rough and conservative calculation, the “value” of a Sembcorp Industry now should be $2.3, which is the value of the Sembcorp Industry business + the value of the Sembcorp Marine shares you will get.

With Sembcorp Industries trading at $1.95 now, that’s a fair bit of upside.

What are we missing?

Of course as I like to say on Financial Horse, when a deal looks too good to be true, it probably is. It’s easy to think that we’re smarter than the market, but that’s seldom true. So we want to be extra careful with our assumptions.

And I think the key risk here is the viability of the business.

Sembcorp’s Singapore Energy business should be relatively sound because it’s a very sheltered market.

But what worries me is the Indian Energy business.

It’s a fairly big part of Sembcorp’s profits too, so it can’t be neglected entirely.

And hand to my heart, I have no clue about the Indian energy business. Is it an attractive business? Are the market dynamics a disaster? Will India have a terrible recession from COVID19? What’s the impact on Indian energy prices? No clue.

If any reader out there has knowledge on this area, please do share below, because I think this is a crucial piece of the puzzle going forward for Sembcorp Industries.

Suffice to say, if the business doesn’t hold up, the entire analysis above doesn’t make sense anymore. If we use a 4 times P/E multiple on reduced earnings, it gets us a $0.75 value for Sembcorp Industries, which adding in the $0.8 from Sembcorp Marine gets us to $1.55, way below current market value of $1.95.

Really rough calculations again, but just goes to show how a change in assumptions can completely change the analysis.

Sembcorp Marine the loser?

But what if you’re Sembcorp Marine?

You used to have Sembcorp Industries as a 61% shareholder. Now, you’re stuck with Temasek, and some public shareholders.

Will Temasek and the public be as willing to invest in the marine business as Sembcorp Industries?

Sembcorp Marine shareholders are being asked to cough up big chunks of money to recapitalize the business, but do we even know what the business will be like 2 or 3 years from now?

Huge huge uncertainty, and I truly don’t know what the future holds.

A lot of talk about how Sembcorp Marine shareholders can sell their shares to buy Sembcorp Industries. This allows them to avoid the rights issue, and they’ll still get Sembcorp Marine shares in the end via the distribution in specie. That’s one way out if you don’t want to go through the whole rights issue.

For shareholders that choose to hold on, it’s hard to see any way to not take up the rights though. The rights issue is just too dilutive.

This is Phase 1 for Sembcorp Marine

My personal view though, is that this is merely a Phase 1 deal for Sembcorp Marine.

After the De-Merger, Temasek is left with a 30% to 58% stake in Sembcorp Marine. And it really doesn’t make sense to stop there.

If I were to try and think like Temasek, I think my next move will be to wait and see my percentage ownership in Sembcorp Marine after this de-merger. And after that, to either privatise Sembcorp Marine (or acquire a majority stake), to gain decision making rights.

And finally, I will find a way to merge it with Keppel Offshore and Marine (where Temasek will be a majority shareholder after completion of the Keppel deal).

I think that just makes the most sense here.

There are real economies of scale in this business, and it doesn’t make sense to have a Keppel and Sembcorp marine arm that compete against each other on the world stage. Rather, merge them, and create a national marine giant that can more effectively compete on the world stage.

That’s also in line with the broader strategy of creating national giants within each industry.

If my view is true, then this is the beginning of a longer journey for Sembcorp Marine. And shareholders should be prepared to be in for the long haul (or you know, just flip it for a gain?).

But of course, that could just be this horse’s fantasy, so do take this with a pinch of salt, and decide for yourself if this makes sense.

Turning Point for Singapore?

The fourth big Temasek deal in the span of maybe 2 years leads me to wonder whether we are at a turning point in the Temasek business model.

It’s worked really well the past 50 years, but it’s getting to a point where the success has been emulated by our partners.

For a lot of these businesses, the key is to get cheap financing and then build scale, which a lot of other countries (especially China, can do better than us).

The world has changed since 20 years ago, and it’s inevitable that Singapore will need to evolve accordingly. Perhaps this round of deals will set the stage for a new direction for Singapore businesses. It will give us the financial cushion to pivot the business, refocus on basics, and find better ways to compete on the world stage.

Closing Thoughts: My Personal Views

Personally for me, I am not a shareholder for either company. If I were a Sembcorp Industries shareholder, I would be pretty pleased with the de-merger. Less so if I were a Sembcorp Marine shareholder.

I can definitely see why people are seeing Sembcorp Industries as a value play after this. You get the core business on the cheap, and you get the “free” Sembcorp Marine shares thrown in.

I can’t help but feel a bit skeptical though. The business hasn’t changed all that much from 1 week ago. Energy still has COVID19 to contend with, and Marine is still going to face headwinds going forward. We’re not exactly out of the woods yet.

Can a corporate transaction like this really value add? Can you make 1 + 1 = 3? Is Sembcorp Industries suddenly 40% more valuable after this?

I definitely think it’s a very clever deal, and it can be very good for both companies.

But as an investor, it’s probably not one for me. There are lots of opportunities out there at the moment, and I can afford to be picky. FYI – My full personal portfolio and personal stock watchlist are available on Patron.

So I’ll be watching on the sidelines for this one. Sure, there could be money to be made, but I’ll leave this money to other investors.

I would really love to hear your thoughts on the de-merger though. Do you like it? Are you a shareholder?

Share your comments below!

Support the site as a Patron and get access to my personal stock watch list, as well as my personal portfolio allocation.

Do like and follow our Facebook Page, or join the Telegram Channel. Never miss another post from Financial Horse!

Join our Facebook Group to continue the discussion, everyone is welcome!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Both are THE best quality investment courses available to Singapore investors out there!

FH, i am just wondering what would be the catalyst that will drive scm share price in mod to.longer term consudering all negativity surrounding marine business.

Do you think banking on privatisation or merger keppel is good bet?

That’s a good question. I think short term reflation trade / demerger excitement aside, longer term it really has to be earnings based. The marine sector simply has to improve, and short term, I find it hard to see that happening.

I think betting on corporate action is tricky because you wouldn’t know the form the corporate action would take. Short term, there’s also going to be big dilution coming from the rights issue that will weigh on the share price for SCM.

I would ask the shareholders of Sembcorp Marine to fight this. It is unfair to especially to minority shareholders. The situation is analogous to abandoning a baby when things go wrong.

Another big issue is the lie that they did nothing wrong in the Brazil fiasco. They adamantly maintained their innocence till one of their is now charged with fraud. I really question the management of these companies. Sembcorp should be solely responsible for this and pay compensation. Singaporeans who support local companies are duped into forgoing their life savings because of these fraudsters. All who had ever invested in Sembcorp Marine / Sembcorp industries should be rightly compensated for their wrong doing.

Yeah, it’s interesting to see if SCM shareholders will support this deal.

No choice, forced to be optimistic with scm. Hope US + opec+ dont keep oil price too low, and also next keppel merger can drive scm price up more than $0.44 , will be good enough.

Interesting, let’s see how it plays out.

Hi FH,

I more or less agree that SCI Singapore Business is relatively safe. I suspect their generation side will still suffer from the current SG excess capacity. However, with their local project profits & recurring waster-to-energy/Utilities income, SG business should still deliver a steady stream of profit.

For the India business, i am a little bit skeptical. Their reported India Energy Assets investment is USD4B. Their reported India income looks low vs the invested capital. The risk/reward of owning/running a coal fired thermal power plant in India is a big unknown to me. The upside – fairly limited to selling any excess capacity. Any hopes for lower running costs is a fantasy – cost improvements are largely for new technology. Having said that, India Energy demand is huge – SCI has to find new projects which are capital intensive to drive growth in this area.

How they recycle capital, invest in Energy/renewables projects and build recurring income will probably be the key to a successful SCI. Unfortunately, I don’t quite see it yet.

Hi App Shadow,

Thanks, that’s a great comment. I don’t know enough about the India business to comment, so thanks for sharing some insights. I do agree though, that short term I wouldn’t say I’m super optimistic on SCI’s earnings.

Dear Finance horse,

Great summary & good insight as always.

I have one super amateurish question regarding this deal.

The 1.5B debt that SCI is suppose to be collect from SCM is now converted into SCM shares and distributed out to SCI shareholder. Does it mean SCI NAV has dropped by 1.5M?

This deal lower the debt gearing of SCM significantly but what other effect does this have on SCI financially apart from the very good news that the lose making marine division get chop off to avoid future bleeding/loss?

Thank you

Sure, replies below!

1) Yes, technically that is correct. But SCI Shareholders will get the shares in SCM distributed to them to “compensate” for the loss.

2) Chopping off the loss making business is the main good news. This could result in rerating of the stock, and SCI will no longer need to worry about the marine business going forward.

Thank you Financial horse for answering my question so quickly. I appreciate it.

I made a typo error in my question earlier. SCI NAV will drop 1.5B after this exercise is over and not 1.5M.

Hi FH

I don’t necessarily agree with this statement “Will Temasek and the public be as willing to invest in the marine business as Sembcorp Industries?” I am not vested in SMM, so looking at it as outsider.

The way I view this, its a bailout for SMM Part 1. If Temasek does not want to invest SMM, why go this far? She can just keep status quote, anyway she already owns both SCI and SMM (indirectly through SCI). Of course it helps SCI too, so clever deal structuring. As Part 2 may need TH to take SMM private first (cough out cash) if there is antitrust resistance. Quite fluid here, several options available.

Hi Retired Uncle,

I agree that Temasek has a bigger plan for SMM, but the big question is how the subsequent restructuring will be carried out. Given how fluid it is, it could be open to Temasek to restructure it without coughing up too much cash themselves. So there’s still uncertainty for SMM shareholders.

Just a simple question, when the right issue is initiated, can it be traded in the market?

Yes, the rights are renounceable.

Incisive analysis

As someone from India, I can say that your second scenario is more likely to happen post COVID

Most of the power generated is sold to the government controlled electricity boards and these organizations are likely to be cash strapped

Delayed and deferred payments are likely although the energy demand is bound to be huge

I am not buying SCI unless it dips to at least 1.85/1.80

This might give you some margin of society

I have a very tiny holding though from 5 y ago that has not lost more than half its value

Better ways to put cash at work

My 2 cents!!

Than you for sharing your thoughts! Really appreciate hearing from someone with the inside info on India. I guess that’s another thing to be wary abot for Sembcorp! 🙂

I own SMM shares, new to this rights issue though, can I purchase a portion of the shares allocated to me? What happened to the rest? Thanks

Yes you should be able to. You will receive a document in the mail that explains your rights. Can also check with your stock broker to provide personalised advice. 🙂

hi, what are your thoughts about not just the logical merger of Keppel OM and SCM, but Keppel and SM itself? They both have an urban solutions arm for example. And for the former – would you suggest that Keppel would need to do what SC has done? A de-merger?

I think the merger would make sense, but from a cash flow stand point, probably less urgent than the margine business. Interesting, Keppel doing a de-merger could definitely be an option as well – one way to unlock shareholder value. To be honest though, there are many ways to approach the corporate restructuring, and it’s ultimately up to Temasek and the relevant board to decide which is the most suitable.