Temasek Bonds are back!

The last time we saw these Temasek bonds was back in 2018 with 2.7% yielding 5 years bond, and they sold like hot cakes.

So when I heard about the new Temasek T2026-S$ 1.8% 5 year Retail Bonds, I was very excited to do a deep dive.

Are they any good, are they worth buying? Let’s find out!

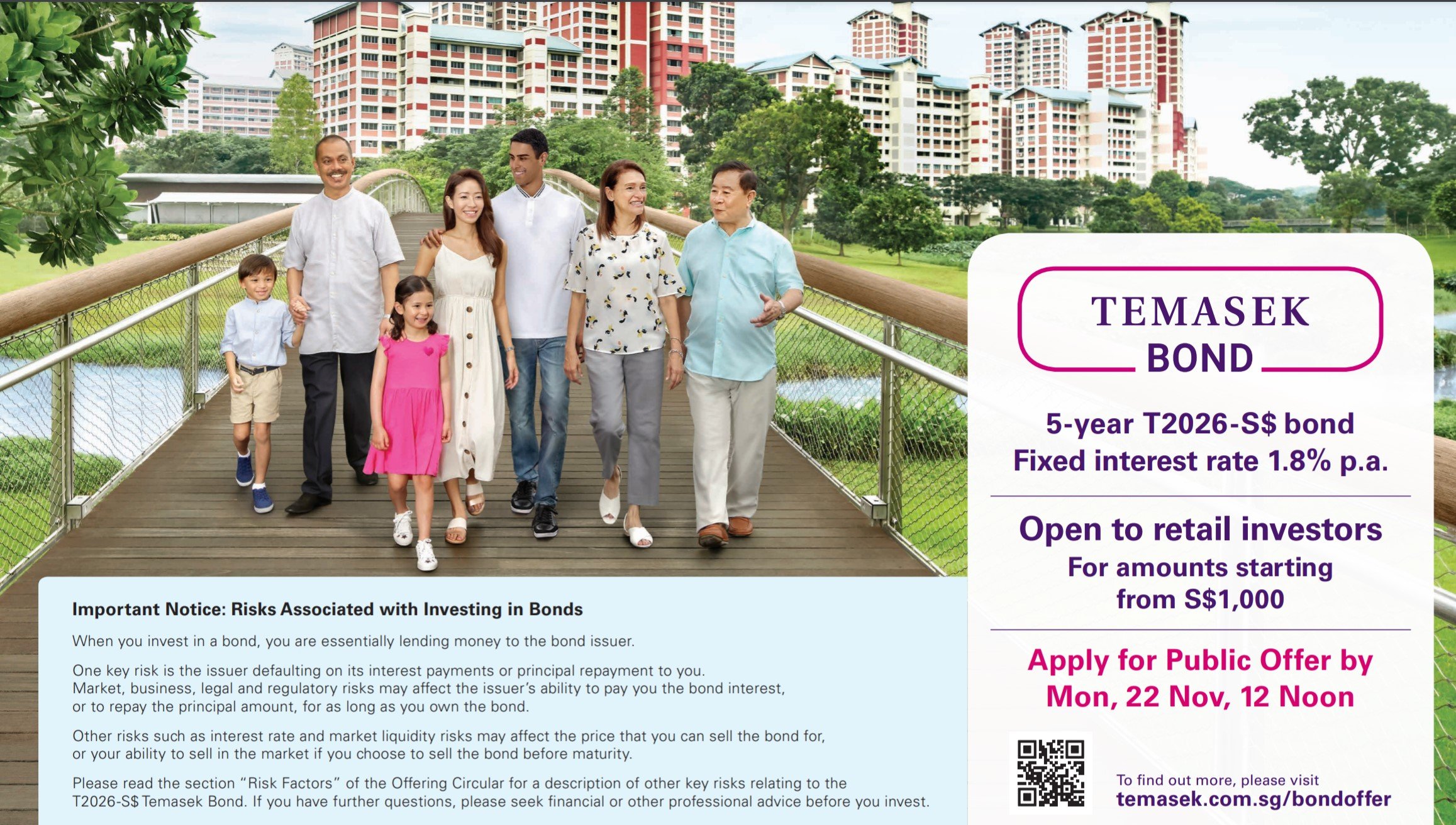

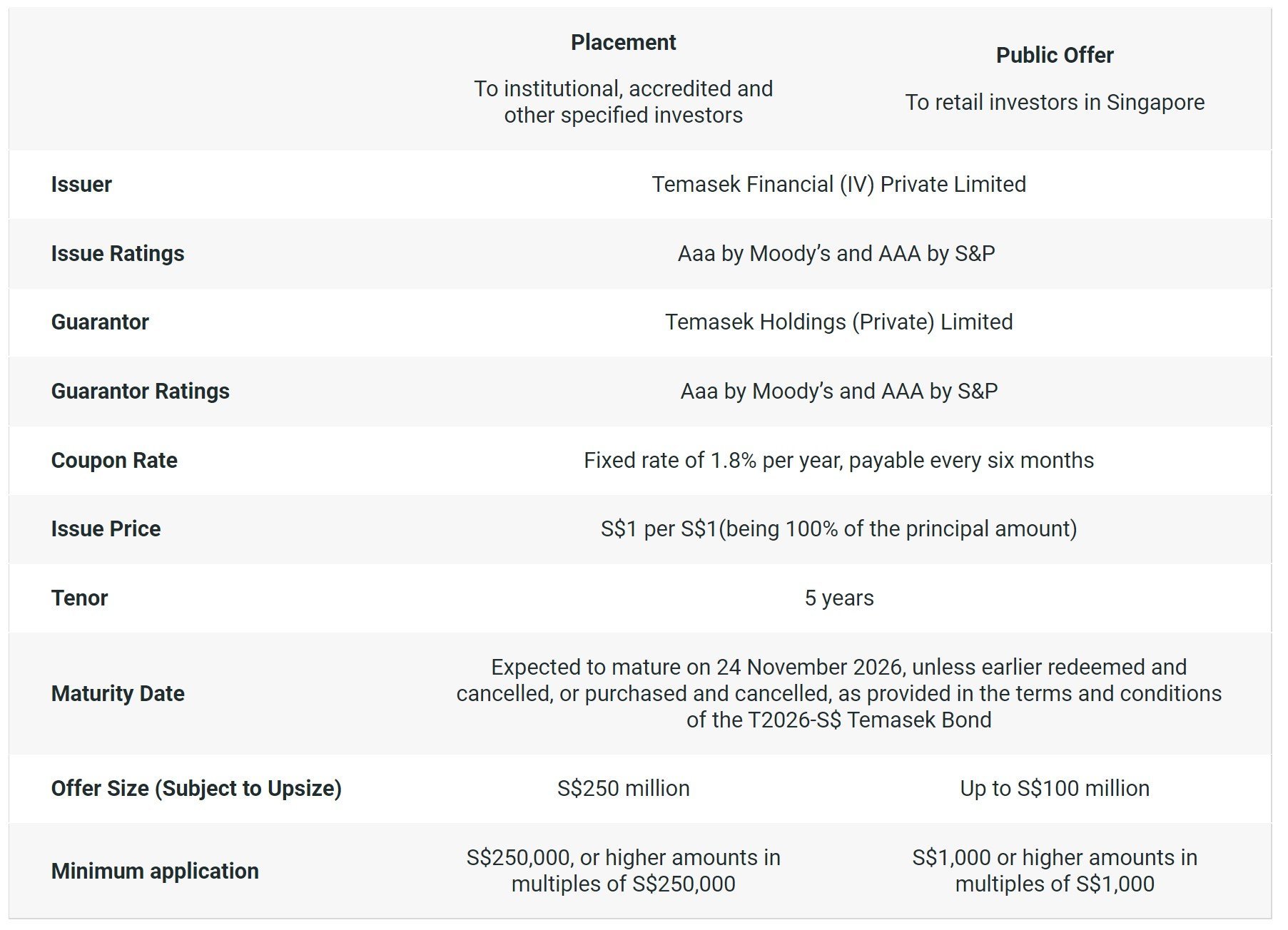

Basics: Temasek’s 1.8% 5 year T2026-S$ Bonds

I’ve extracted the key details below.

Basically, these Temasek Bonds are:

- Issued by a Temasek subsidiary but guaranteed by the Temasek Parent – Temasek Holdings (Private) Limited

- 1.8% coupon per year, payable every six months

- 5 years duration, maturing on 24 November 2026

- Freely Traded (can be bought/sold) on the SGX

- Public Offer of S$100 million

- Minimum application of S$1,000, in multiples of S$1,000

For those who are familiar with the 2018 Temasek Bonds or the Astrea Bonds Series, this is pretty similar.

What is the Risk of Default on these Temasek Bonds?

Okay the million dollar question – What is the risk of default?

I took this from the Temasek Website (emphasis mine):

“The T2026-S$ Temasek Bond to be issued by Temasek Financial (IV) Private Limited, a wholly-owned subsidiary of Temasek, is a 5-year bond which pays an annual coupon of 1.8%.

Temasek Holdings (Private) Limited is the Guarantor, which fully guarantees all payments of interest due, and the full repayment of the principal amount at maturity in 2026.

There is no certainty that the Guarantor will always remain solvent and able to fulfil its obligations under the guarantee.”

There’s a lot to unpack there.

But to put it very simply – These Temasek Bonds are guaranteed by Temasek.

Temasek Holdings (Private) Limited, which is the parent Temasek entity, will full guarantee all payments – both the interest and principal.

As long as you hold these Temasek Bonds for 5 years until maturity on 24 November 2026, the only risk you are taking on is the risk of a default by Temasek.

What is the chance of a default by Temasek?

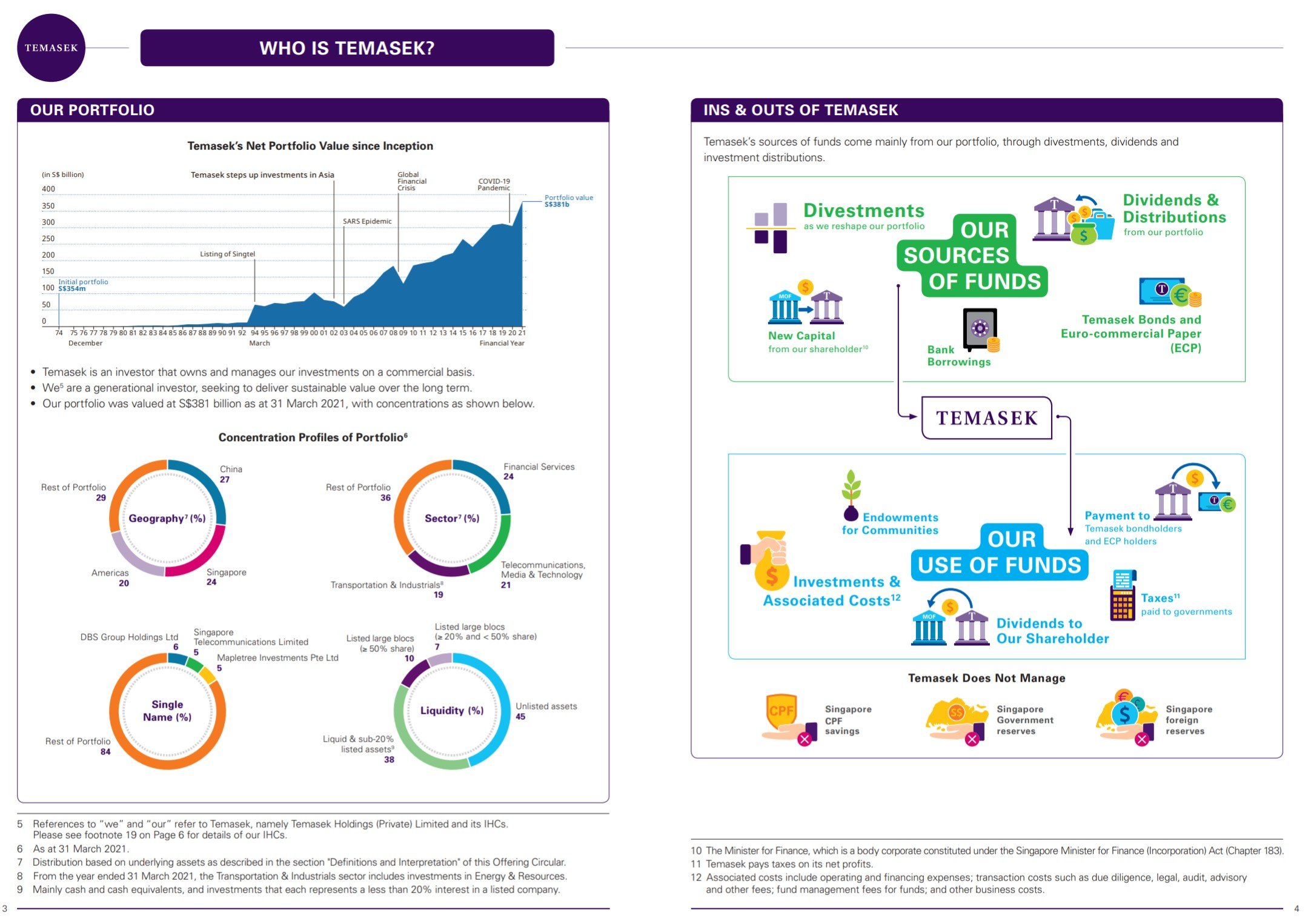

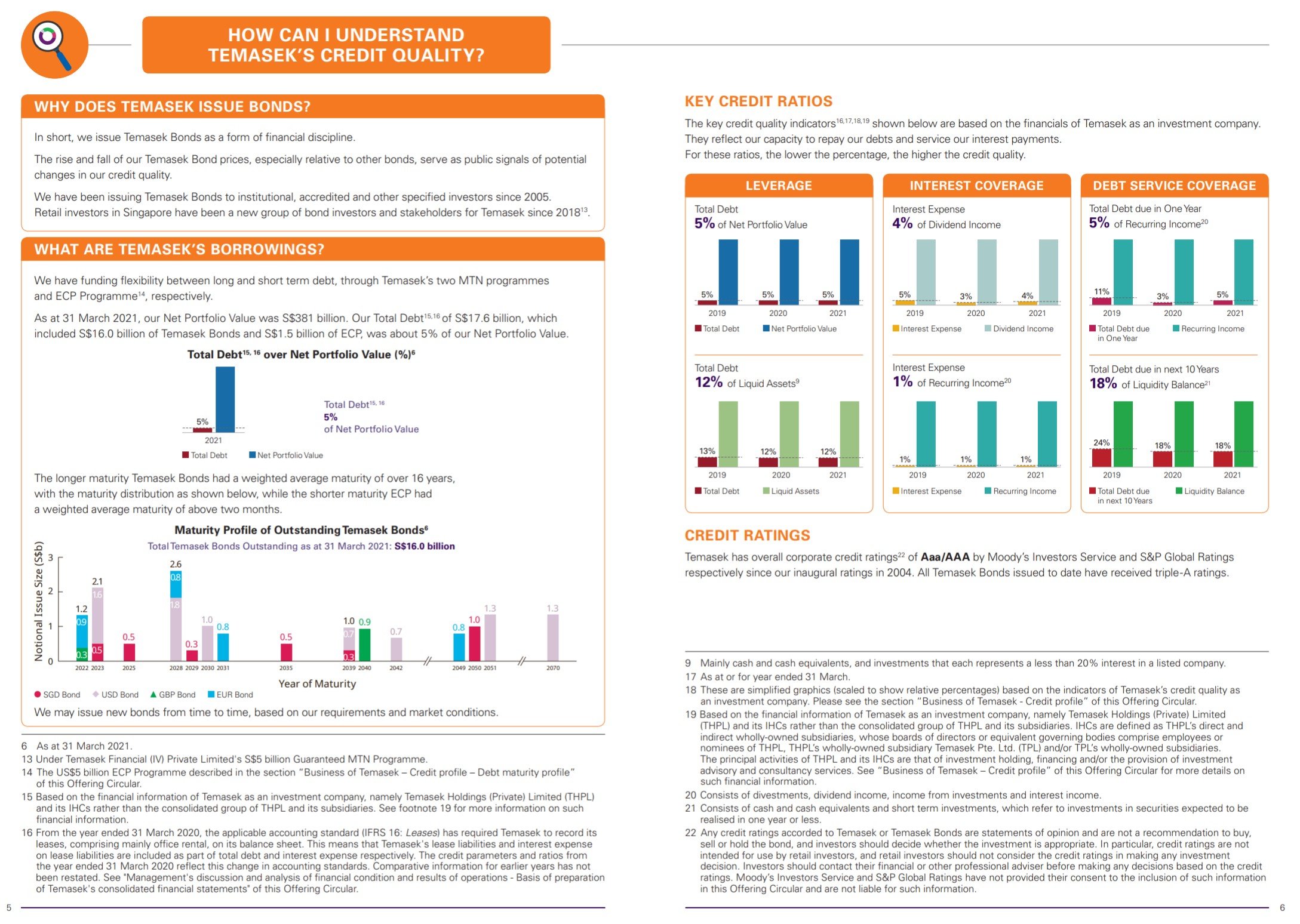

I extracted a bunch of charts below on Temasek’s portfolio and credit quality.

For what it’s worth, Temasek is rated Aaa/AAA by Moody’s and S&P respectively, which is the highest level of credit rating.

But who are we kidding.

This is Temasek we’re talking about.

If you’re a Singaporean, you probably already have your own views on Temasek, and nothing I say is going to change that.

Of course, nothing in life is risk free, and I get that there is a small chance Temasek can go bankrupt.

But frankly, in the view of these humble horse, this is as close to zero risk at it gets.

Is the 1.8% Yield on the Temasek Bonds good?

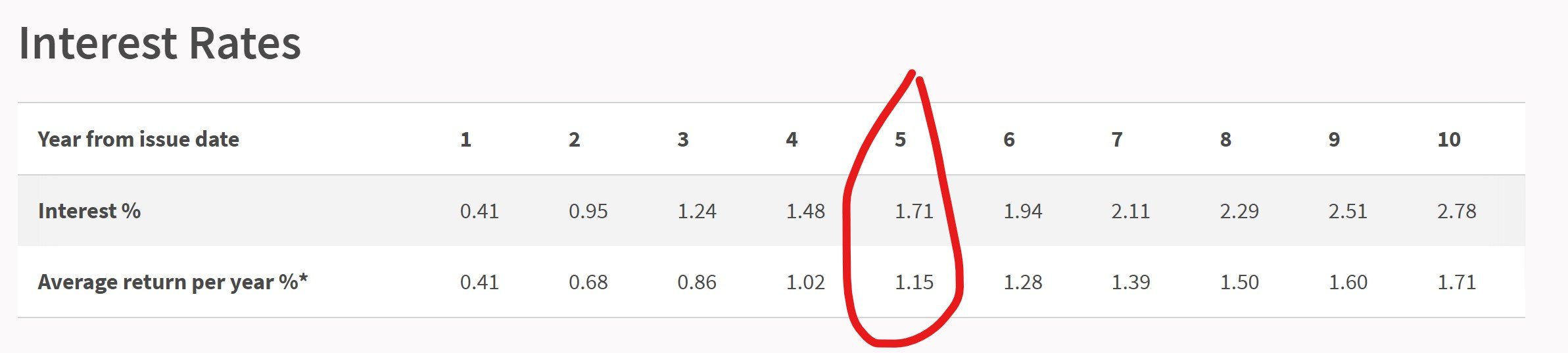

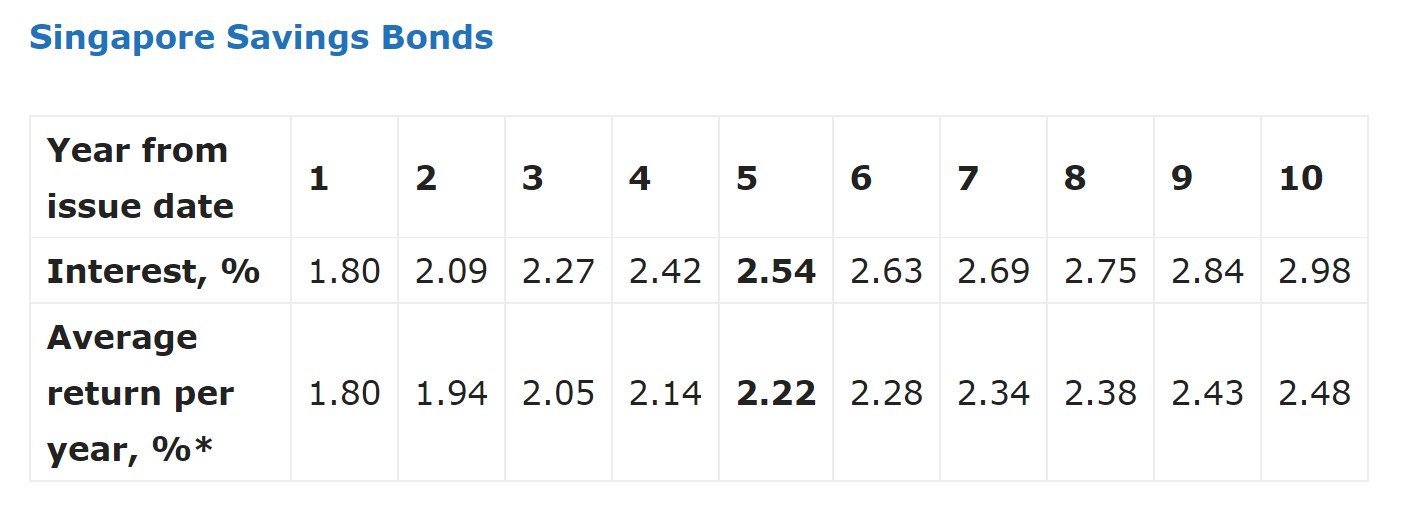

A 5 year Singapore Savings Bond will yield 1.15% if you hold it for 5 years.

At 1.8% yield, these Temasek Bonds are being offered at a 0.65% premium to the risk free rate, which is frankly quite attractive.

To put things in perspective, the 2018 Temasek Bonds were offered at 2.7%, which was only a 0.48% premium to the risk-free back in 2018.

So if you view it this way, the current 2021 Temasek Bonds are more attractive than the 2018 Temasek Bonds.

Rising Interest Rates may mean Capital Losses

From the Temasek Website:

The T2026-S$ Temasek Bond may be traded on the Singapore Exchange (SGX-ST) at market price.

Temasek does not guarantee its market price or liquidity.

What they are trying to say, is that if you decide to sell these Temasek Bonds on the SGX before November 2026, then the price you get is subject to the price a buyer would pay for them.

And for this, Temasek has no control.

When interest rates go up, the price of a bond goes down.

Which means that if interest rates go up between now and 2026, you may face capital losses if you’re trying to sell these Temasek Bonds on the SGX.

Are Interest Rates likely to go up?

That’s where things get a bit tricky.

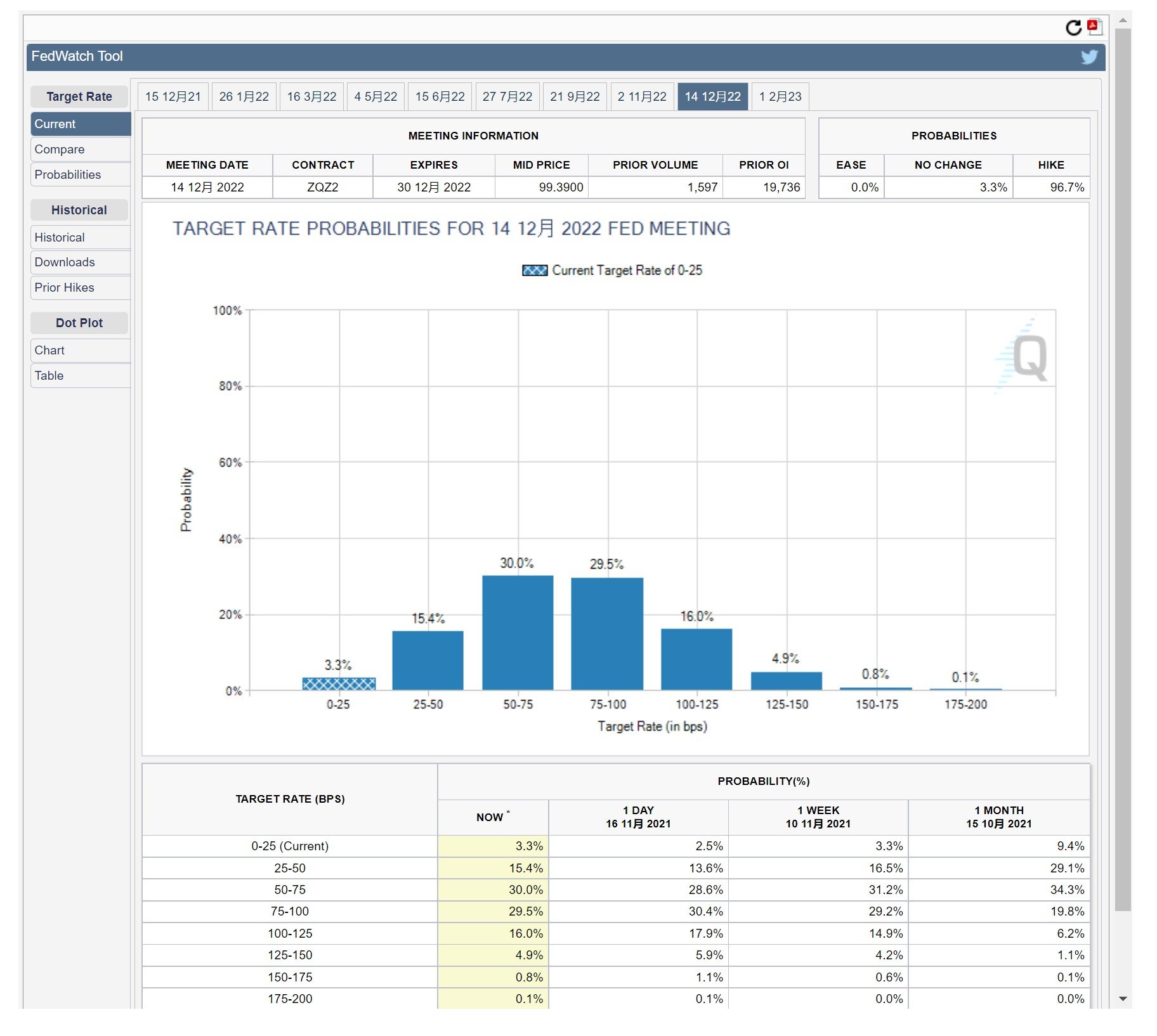

Inflation is starting to become a big problem globally, and the market right now is pricing in 2 – 3 rate hikes by December 2022.

My personal view is that short term, say 1 – 2 years out, interest rates are going up.

This is a big difference from 2018 when the Temasek Bonds were issued towards the later stages of the hiking cycle, when the Feds were starting to wrap up their rate hikes.

This time around in 2021, we’re sitting at the start of the Fed Hiking cycle.

So you may argue that to tempt investors to buy these bonds in 2021, a higher risk premium is required. Hence the 0.65% premium versus 0.48% back in 2018.

And that’s fair.

But the long and short of it is this – If you plan to sell in the next 1 – 2 years, whether you can get your full principal back will depend on how aggressive the US rate hikes are.

Granted it’s unlikely to be a big loss (probably 2 – 3%), but still something to note nonetheless.

Of course, the option is open for you to hold them until Nov 2026 and get your full principal back with no losses, but for those who need the cash urgently that wouldn’t work.

So if you’re subscribing for these Temasek Bonds – it’s worth thinking about whether you plan to sell them next year, or whether you’re going to hold to maturity.

Liquidity on the Temasek Bonds

Spoiler alert – Liquidity on these Temasek Bonds is likely to be incredibly poor.

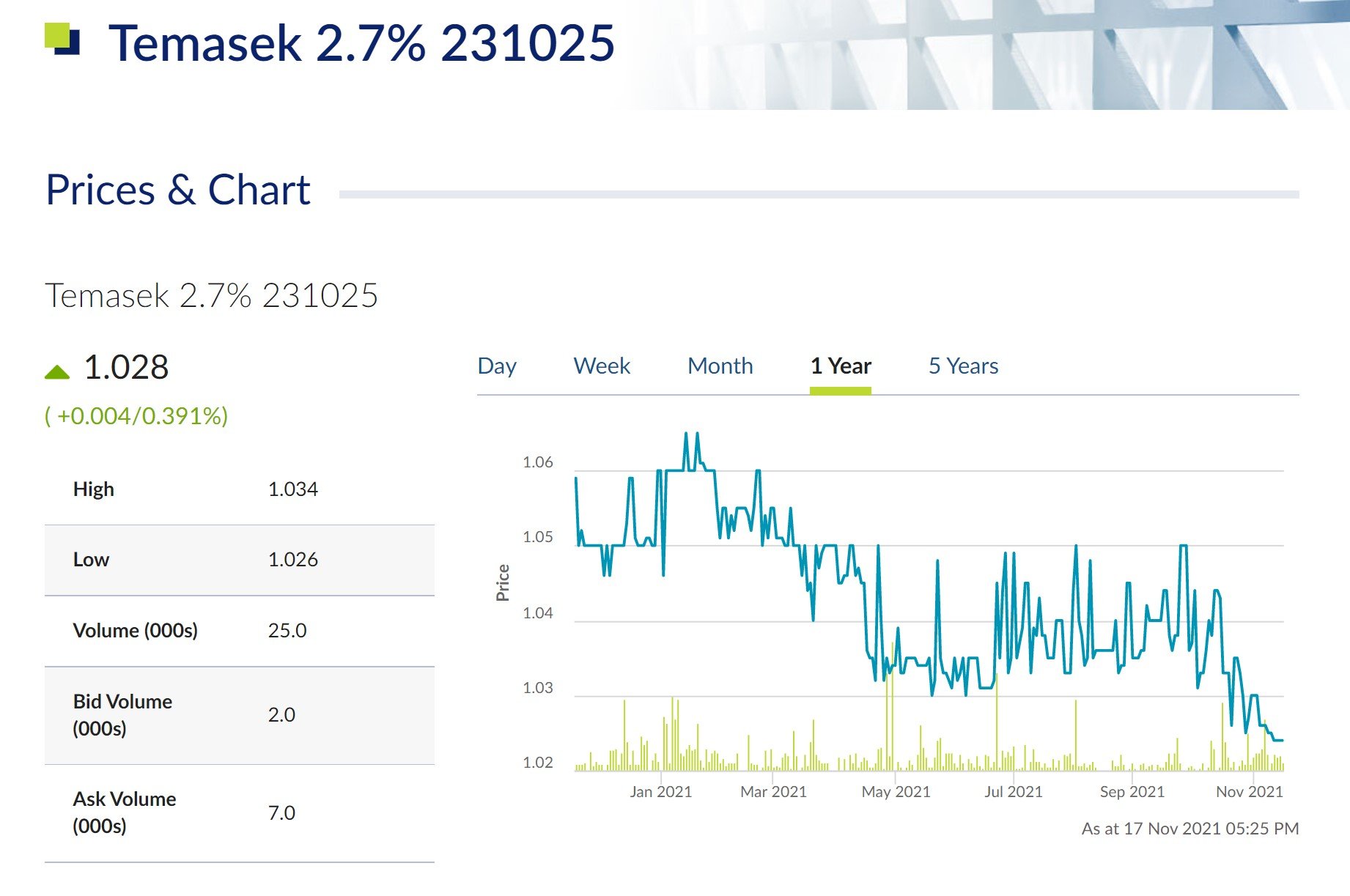

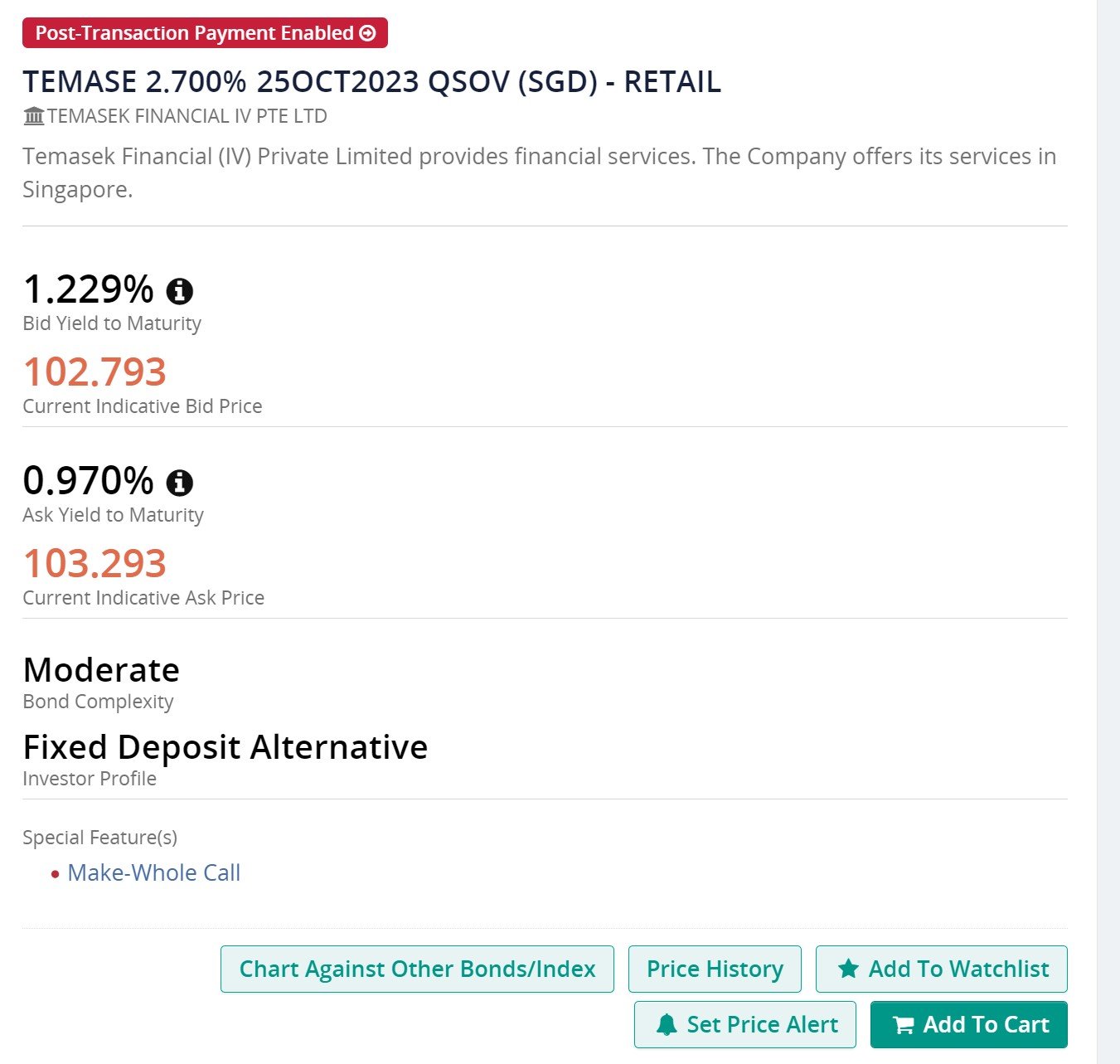

I pulled up the 2018 Temasek 2.7% Bonds, and trading liquidity is an abysmal 25,000 units a day.

I mean that’s just Sahara Desert level of liquidity.

Don’t forget that the 2018 Temasek Bonds had a $300 million public offer, which is 3 times that of the current $100 million public offer.

Big one to take note of.

If you need the cash and need to sell these Temasek Bonds into a rising interest rate market, you might need to price it at a discount to find a buyer.

Look at the bid-ask spread on the 2018 Temasek Bonds. You could drive a Tesla through that spread.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

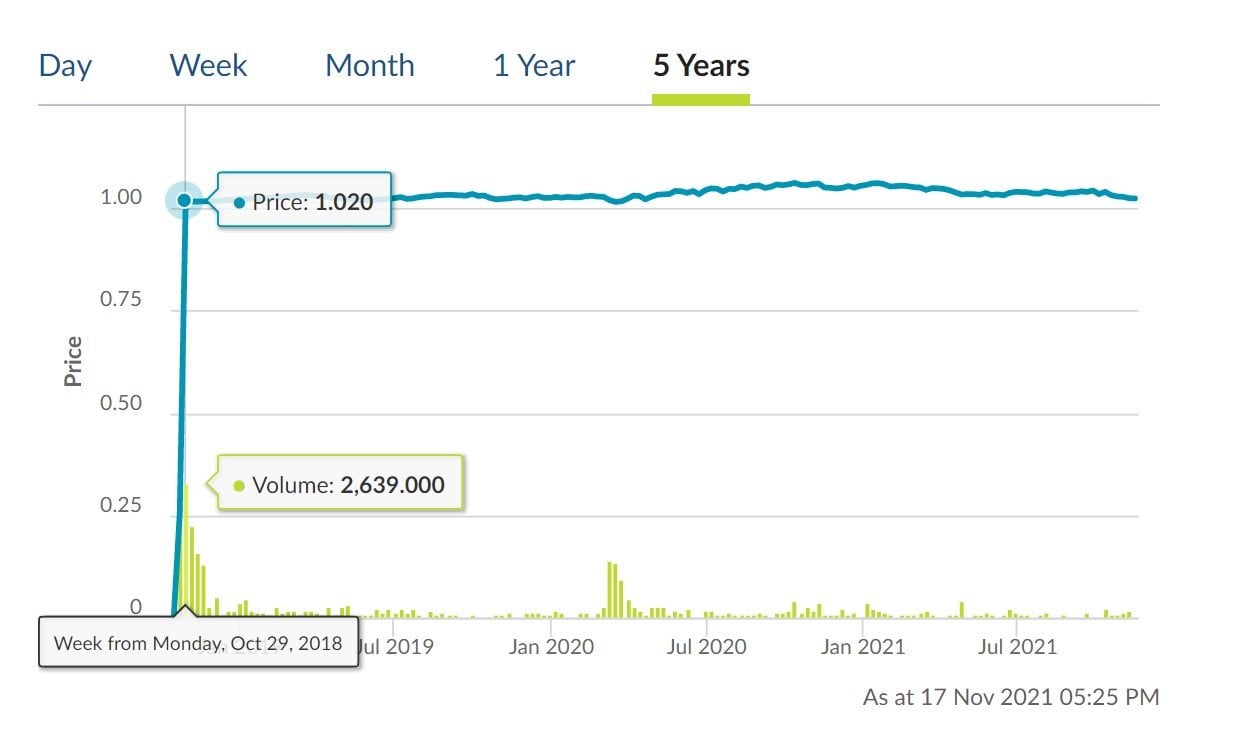

How did Temasek’s 2018 Bond do? 2.7%, 5 years duration (T2023-S$ Temasek Bond)

Temasek’s 2018 bonds did very well.

On day one it had a nice 2% pop, and it traded at between 1.02 – 1.05 for much of its life.

Big point to note is that the Temasek 2018 Bonds were issued towards the tail end of the interest rate hike cycle.

This time around the 2021 Temasek Bonds are issued into a rate hiking cycle, so they may actually trade below par if rate hikes are aggressive.

What are the chances of getting these Temasek Bonds IPO?

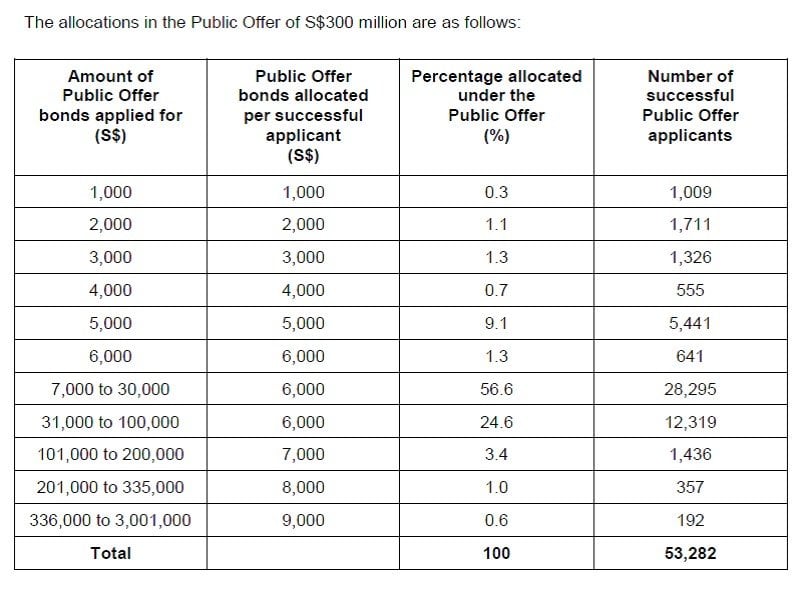

The public offer for the 2018 Temasek Bonds was $300 million and it was 8 times oversubscribed

This time around in 2021, the Public Offer is only one third the size at $100 million.

You could argue that interest rates are significantly lower this time so demand will be lower, but I think the reduced offer size will more than offset it.

So I think these Temasek Bonds will be very hot, and don’t expect to get a big allocation.

How will Temasek allocate these Temasek Bonds if Oversubscribed?

From the Temasek website (emphasis mine):

“We aim to allocate the T2026-S$ Temasek Bond to as many retail investors as possible if it’s oversubscribed.

This is similar to how we had allocated the T2023-S$ Temasek Bond issued in 2018 to all valid applicants in the Public Offer.

We will finalise the exact allocation based on the valid applications received. “

So it’s like the 2018 Temasek Bonds and Astrea Bonds Series, where they try to give it to as many retail investors as possible.

Based on the 2018 Temasek Bonds allocation:

- Everybody applying $6,000 and below got their full allocation

- Everybody applying $6,000 to $100,000 was allocated $6000

- Anyone applying $101,000 to $200,000 got $7,000… seriously?

You can check out the balloting table below:

Balloting Strategy in 2021?

Using the 2018 results, $6,000 is the sweet spot to apply for.

But if you’re serious about getting these 2021 Temasek Bonds, I would say just apply for $10,000 to be on the safe side.

Would I subscribe for these Temasek Bonds?

I like these Temasek Bonds, and from a pure investment perspective I think the 0.65% risk premium in this market is fantastic considering these are basically risk free.

That said – I’m probably going to skip them.

The reason why is because I have most of my cash reserves sitting either in CPF (earning 2.5%), or in Singapore Savings Bonds from back in 2019 (earning 2%). Full Portfolio can be viewed on Patreon if you’re keen.

The rest of my liquid cash is earning maybe 1%+, but I need to use them in the coming months.

Any cash that I put into these Temasek Bonds I would probably want back in the next 1 – 2 years.

That would expose me to short term interest rate risk, bid-ask spread, and transaction fees when I sell.

All for 1.8% a year, on maybe $5000 if I’m lucky.

It’s probably more effort than it’s worth for me.

Who is likely to subscribe for these Temasek Bonds?

That said, for retirees with a lot of cash stuck in the bank earning 0.5% fixed deposit, I think these are a pretty good buy.

There is literally no other product on the market right now that would give you a similar return, at this level of risk.

You can argue that the 1.8% yield is too low, but unfortunately that’s just the environment we’re living in today.

Anything 3%+ and above in this climate and you’re probably going to be taking on a real risk of default.

Allocation too small to be meaningful?

A lot of you raised this concern with the Astrea Series of Bonds as well.

Namely that a $6,000 allocation to the Temasek Bonds isn’t meaningful from a portfolio standpoint, and you’re better off not getting any.

And I completely get it.

If you have a $1 million dollar stock portfolio and $200,000 liquid cash, having $6,000 stuck in these Temasek Bonds paying $108 a year is more trouble than it’s worth.

I think that’s a perfectly legitimate concern, and if you’re one of these you may be better off just putting your money in a money market fund or fixed deposit, and hope that interest rates go up in 2022.

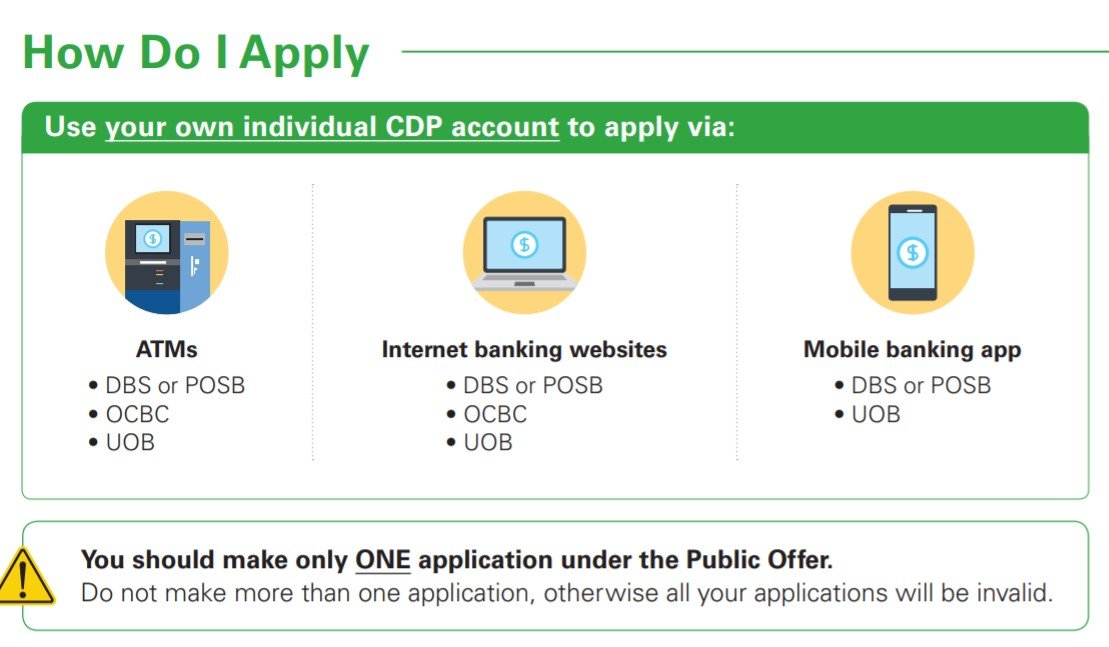

How to Apply for the Temasek Bonds?

Application closes at 12PM on Monday, 22 November, so do apply for the Temasek Bonds soon if you’re keen.

Application process is similar to any other IPO, you can do it via Internet Banking or ATM for any of the 3 local banks:

- DBS or POSB

- OCBC

- UOB

Minimum application is S$1,000 or higher amounts in multiples of S$1,000.

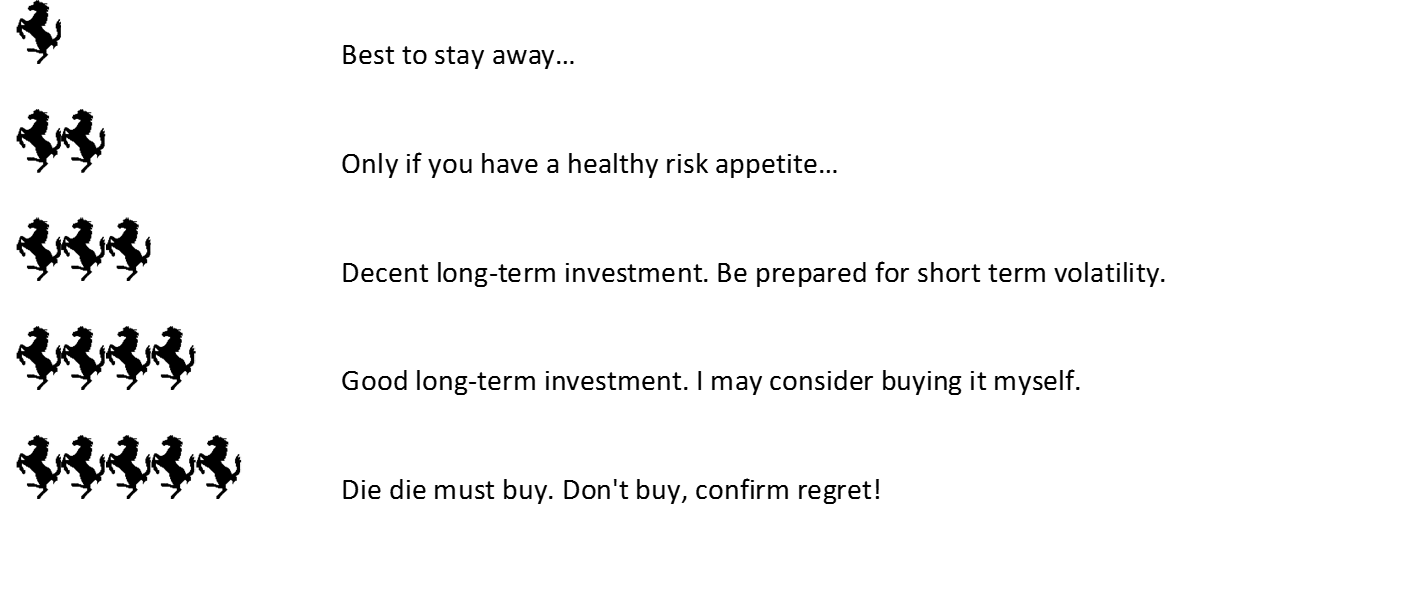

Closing Thoughts: 4 Horse Rating for the Temasek Bonds

From an investment perspective, I think these Temasek Bonds are close to perfect.

0.65% Premium to the Risk Free, for bonds that are as close to risk-free as you can get in this climate.

There’s basically no other investment product in the market that comes close.

The problems with the Temasek Bonds are due to factors beyond their control: (1) poor liquidity on the SGX, and (2) rising interest rate climate.

As investors though, we do still need to take this into account, because those have very real effects in the real world.

So because of this, the Temasek’s 1.8% 5 year T2026-S$ Bonds are a 4 Horse Rating (out of 5) for me.

They’re great, but not perfect.

Love to hear what you think!

Temasek’s 1.8% 5 year T2026-S$ Bonds – Financial Horse Rating

Financial Horse Rating Scale

As always, this article is written on 19 Nov 2021 and will not be updated going forward. Latest thoughts (and my stock watch and personal portfolio) are available on Patron.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a Free Apple stock (worth S$200) when you open a new account with and fund $2000.

Get 1 free Apple share (worth $200) you’re new to and fund $2700.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

Thinking about flipping on 1st day of trading to make some quuck bucks.

What do you think ?

Allocations are not likely to be big though. Let’s say you are lucky and get 5,000, and it pops 2%, that works out to $100 before transaction fees.

If it pops 1% then it’s just $50 which barely covers transaction fees.

5 years is too long to get the principled amount and interest. Assuming anytime if i sell will be lower than what i invested. I would rather invest in buying cardano ada instead with these $6000. Assuming i bought at usd 2 per coin and sold at usd 5. The profit could be sgd 8000.

Well the risk profile of both are very, very different. 😉

For those who need something risk free to replace cash, these Temasek Bonds could be an option.

For default risk, 0.0001% – debt is only 10% of total asset. Very conservative.

Will definitely be over subscribed several times again. Where do we find a AAA rated bond paying 1.8% now and explicitly guaranteed by Temasek? I had already apply yesterday and don’t expect much. The last one, I applied for $51K and only get a miserable $6K. Lol. Temasek mah. This time if I can get $10K is good enough.

For flipping, the profit after brokerages is miserable unless you can get a big allocation which is unlikely. Why bothering? I treat it as spare cash with nowhere to go, just buy and forget. I get it, FH will tell me about opportunity costs. I get it.

For price, I think it’s unlikely to drop below par unless there is a deep global crisis. The supply is just too little. If it drops to par, I guess institutions especially insurance companies will go in and swept all they can. I will join in but the window will be short.

Above are just my views. I may be wrong.

Interesting point on this never going below par. I suppose if you assume that the cycle high for interest rates this time around is below 2%, then you’re right these Temasek bonds may never go below par.

The next 1 – 2 years are going to be very tricky though. Depending on how inflation plays out, I’m expecting significant rates volatility going forward. I expect 2022 to be a very different political environment in relation to how to address inflation.

I’m inclined to agree with you, but can’t rule out the possibility of a more hawkish Fed to combat inflation. In any case for those who hold long term this is not an issue. And I kinda agree with you that the amount is so small anyway, insurance companies can easily come in and buy out all the float if it trades below part.

Great points though, really appreciate the sharing.

Always welcome.

Agree that Fed and interest rate is key for the bond market but it’s not everything. Maybe I didn’t spell it well. It may drop below par, but only for a very short time because that’s where lots of money will get diverted to due to extreme fear. When everything got sell off, where will the money go to?

Oh I get what you mean. Yes I agree with this.

Too much hype on interest rate lately by media after the China Tech hype burst. I get it, they need to do business and make profit. But is it really so scary?

Dear FH,

You mention in your article that this is more suitable for retiree with lots of spare cash.

Just a thought. In this case, would it not be better for these retiree to put these spare cash into their CPF account which is equally risk free and attract higher interest?

Best regards

Well CPF has quite specific rules on when you can withdraw the money, so not everyone may be comfortable with that just for an additional 0.7% pa return. 🙂

Yes agree. Too many restrictions and can change anytime. Do note the sequence of withdrawal too. If one meets the FRS and still have spare, he has to empty his SA first.