Update: Balloting Results are out! View them here.

As you already know by now, the latest series in the Astrea bonds – Astrea VI, is out.

Very, very hot stuff with lots of coverage in the media, so I wanted to share my views as well.

Basics: What is the Astrea series of Bonds?

The Astrea series of bonds is basically a set of bonds secured by private equity (PE) Funds.

Think about it this way.

You take 35 different PE Funds.

You put them all together into a $1.5 billion portfolio.

And you borrow $600 million secured against this $1.5 billion portfolio.

That’s really what the Astrea VI bonds are.

Before this, there was the Astrea IV (4.35%) and Astrea V (3.85%), so Astrea VI is the latest in this set.

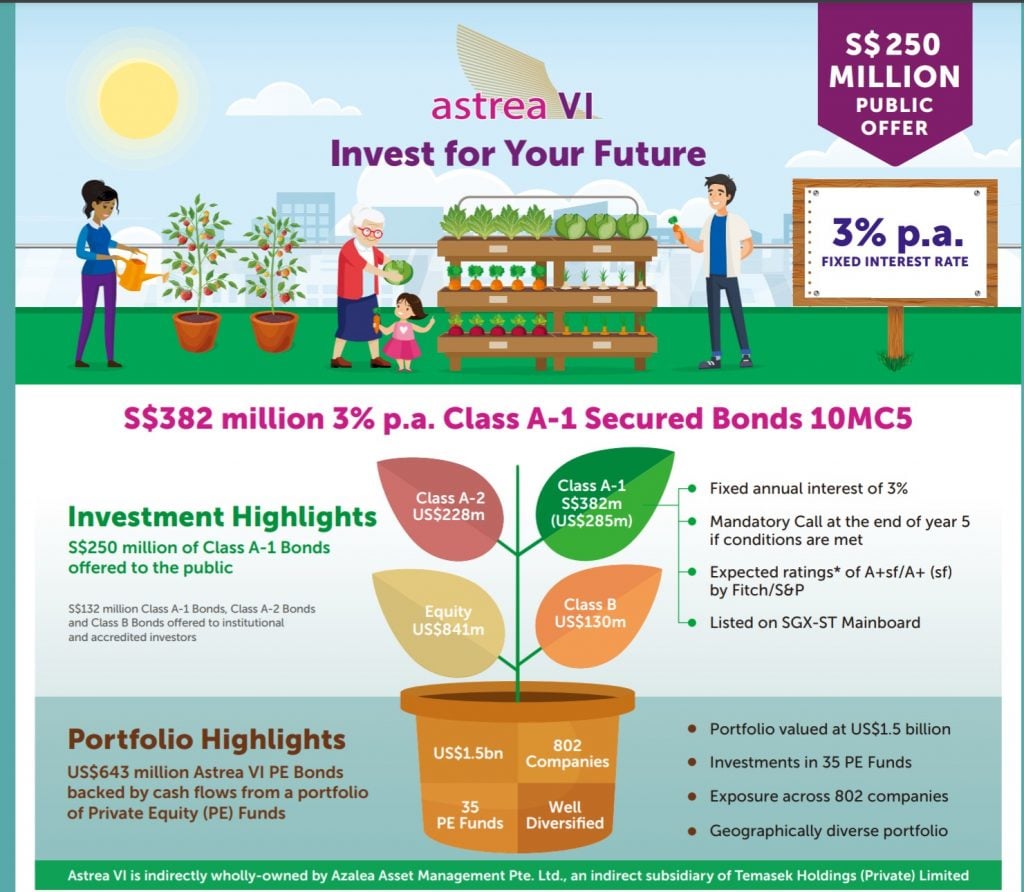

Key Features of Astrea VI Class A-1 Bonds

Retail investors only get access to the Class A-1 Bonds, which are the highest and safest tranche available.

Key features are:

- 3.0% interest paid twice a year (18 March and 18 September each year)

- Bonds last for 10 years

- If certain performance conditions are met, the bonds will be redeemed after 5 years, and there is a bonus payment of 0.5%

Don’t forget to join our Telegram Channel and Instagram!

[mailmunch-form id=”928667″]

Is the 3% yield on Astrea VI attractive?

|

Series |

Date |

Yield |

10 year SSB at the time |

Yield spread vs 10 year SSB |

|

June 2018 |

4.35% |

2.43% |

1.92% | |

|

June 2019 |

3.85% |

2.13% |

1.72% | |

|

Astrea VI |

March 2021 |

3.0% |

1.15% |

1.85% |

Now I know a lot of you think that the 3.0% yield is low.

But let’s not look at it on an absolute basis, because yields are relative.

We need to look at it versus the risk-free rate, which is the 10-year Singapore Savings Bond.

And when you look at it in that way, the 3.0% is a whole 1.85% higher than the 10-year SSB at 1.15%.

Compared to Astrea IV and Astrea V, the yield spread is generally in line with the previous bonds.

So frankly, the yield is still pretty attractive compared to what you can get on the open market, at this level of risk.

Even if you go out there and buy Astrea IV/V on the open market today, your yield to maturity won’t be as good as Astrea VI.

Default Risk

The million-dollar question – what is the chance of default for Astrea VI?

This part can be a bit technical, so if you want to skip through it, feel free to jump to the conclusion to this section.

The structure for Astrea VI is very similar to Astrea IV and Astrea V.

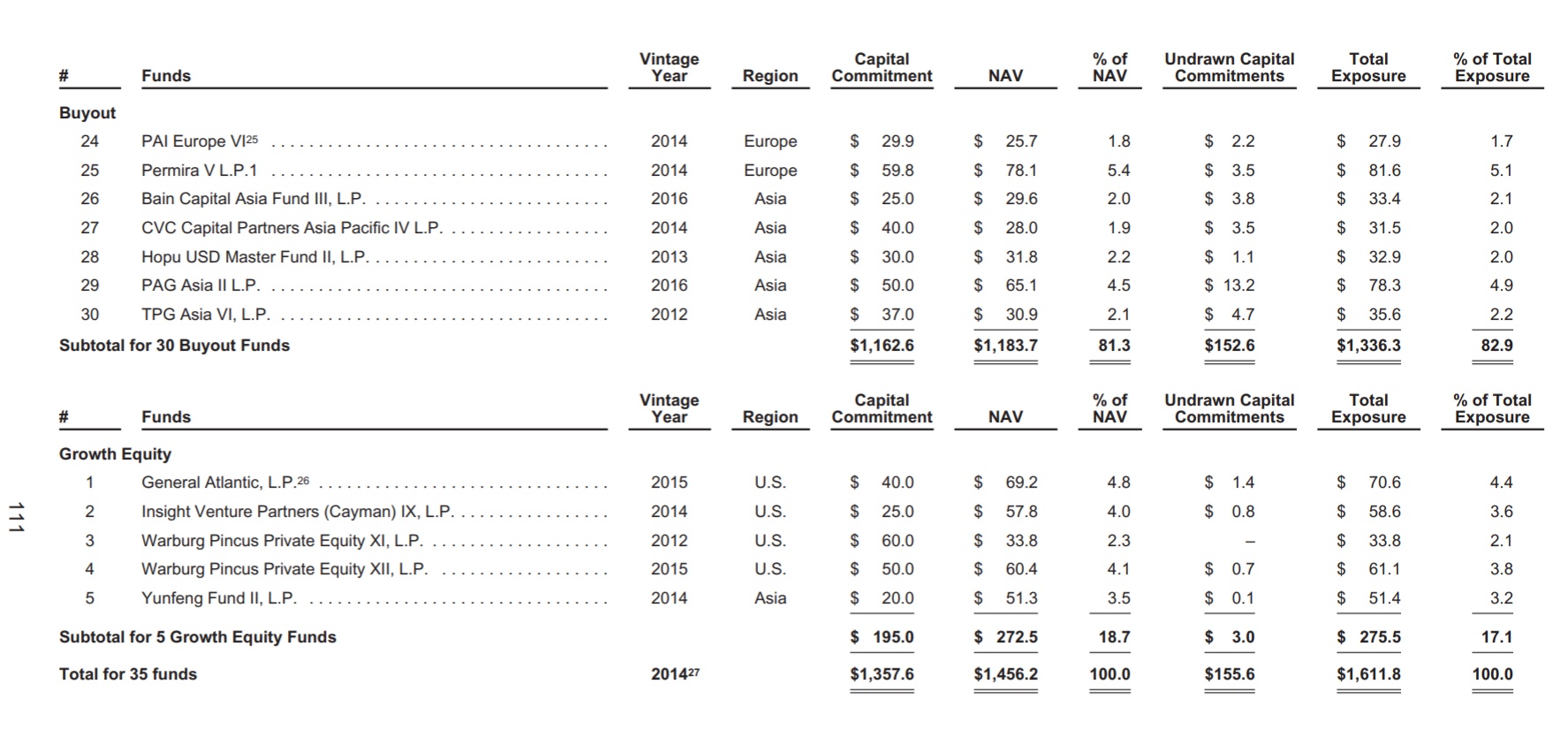

What are the underlying assets?

So the underlying is 35 different PE funds as set out below.

The funds are broadly diversified, with US Buyout funds being the biggest chunk.

Top 3 GPs are Bain, Warburg Pincus, TPG, basically the big names in private equity.

Average vintage is 5.8 years which is good.

PE is like wine, so the older it is the better it is.

Older funds are more stable and more likely to generate cash flow. Good stuff if you’re a bond holder.

What are the safeguards in place for Astrea VI?

Basically, there are 5 big safeguards for Astrea VI:

- 35% LTV for Class A-1 Bonds

- Reserves Account

- Sponsor Sharing

- Maximum LTV Ratio

- Credit Facility

35% LTV for Class A-1

Think about it this way.

You buy a house for $10 million. You borrow $3.5 million from the bank.

As long as the house does not fall in value by more than 65%, the bank will not lose money.

The Astrea PE Bonds are the same, only you are the bank lending the money.

Class A-1 and Class A-2 rank equally, so you’re looking at 35% LTV for Class A bonds.

Barring a 65% drop in value of the underlying PE Funds, the bonds *should not* default.

Reserves Account

Debt investors will know this as the waterfall payment.

But really – it’s just a fancy way of saying that all the money generated from the underlying assets needs to be paid in a specific order.

Back to the house example, imagine that the bank now requires that all rental income from the houses, or all proceeds from the sale of the houses, needs to be paid in a specific order.

Astrea is required to pay all moneys in the following priority:

- Key expenses

- Interest on the bonds

- Into a reserve account every 6 months at a fixed rate, that will be used to redeem the bonds after 5 years.

- Remaining expenses

Only after these payments are made, will the “owner” of the houses (the Sponsor Azalea), be entitled to receive any moneys from the equity tranche.

Long story short – this is a good thing as it is additional protection for Astrea VI bondholders.

Sponsor Sharing

Any amount that is paid to the Sponsor in the equity tranche will also be split 50-50, with 50% of it going into the Reserves Account, which is then used to redeem the Class A-1 bonds after 5 years.

Maximum LTV Ratio

Astrea VI has a max LTV Ratio of 50%. Once the gearing of Astrea VI crosses 50%, this clause will kick in, and the Sponsor will not be entitled to any cashflows until the Reserve Account has been topped up to the amount to redeem the Class A-1 bonds.

Credit Facility

Essentially, DBS has given Astrea a loan, that can be drawn on at any time to provide emergency liquidity.

This can be used to pay expenses, and interest on the bonds, but it cannot be used to redeem the bonds themselves.

That’s all very nice FH, but will these bonds default?

Long story short, my view on Astrea VI is similar to Astrea IV / V:

The default risk here is very low.

There are a lot of structural safeguards in place, that together with the 35% LTV, make default risk low.

But of course, it is not zero risk.

If the risk is zero the yield would be 1.15% (10-year SSB)

I think for these bonds to default, we really need to see the PE Funds collapse in value by 50% or more.

And bear in mind these are PE Funds from the big boys like TPG, Bain, WP etc.

If these funds half in value, we’re probably looking at Great Depression Part II.

In that Scenario – Even if you park your money in the stock market, you’re not going to be spared.

Only the USD / gold / Treasuries will hold its value in that scenario.

Astrea VI is NOT backed by Temasek

This is important to note.

Temasek owns 100% of Azalea, who owns 100% of Astrea. Astrea then issues these bonds.

But if anything goes wrong, Temasek is NOT on the hook here.

The protection comes from the 5 points we talked about earlier, there is no “Temasek Guarantee” here.

So again – there are a lot of safeguards in place, but Temasek guaranteeing Astrea VI is not one of them.

Liquidity / Price on the secondary markets

I extracted the price charts for Astrea IV and Astrea V below.

2 key takeaways:

- Both are trading very well on the open market, at about 5% premiums

- Trading liquidity is very poor (but at least there is some liquidity)

Will they trade well on the open market? Is there risk of capital loss on secondary markets?

Someone, and I kid you not, asked this at the Live Q&A to Astrea’s management.

The question basically was – How will Astrea VI trade on the open market after listing. Does the price go down such that I suffer capital losses?

Obviously, the reply was that they had no clue.

And to be fair, this is a legitimate concern.

As shared last week, I do expect us to be in a rising yield environment for 2021. This will continue until such time as the Feds come in with some kind of operation twist or yield curve control (or not, if you disagree with me).

If yields go up, bond prices come down, so there is a possibility that these Astrea VI bonds trade underwater.

I don’t have a strong view on how Astrea VI trades post-IPO.

Based on Astrea IV/V’s yield to maturity, Astrea VI should see a small bounce on IPO.

But whether they trade down in the coming months, I frankly have no easy answer here.

The liquidity on these things are so low that anyone trying to dump them can easily move the market.

So I genuinely cannot rule out that possibility that Astrea VI trades below par for short periods on the open market.

This is a risk to note if you’re buying in.

Trading Liquidity is low

And again – trading liquidity is very low.

As low as 11 lots a day for Astrea V.

If you want to sell these in a hurry, you probably need to price below market to get them done.

Don’t expect instant liquidity here.

How attractive Astrea VI is depends on your opportunity cost

Let’s put it this way.

If the money doesn’t go into Astrea VI, where would it go instead?

If the money goes into stocks or REITs, then I think stick with stocks / REITs. Those probably give a better investment return.

We’re moving into a more inflationary scenario with economic growth picking up, so I wouldn’t allocate money away from stocks / REITs into low yielding bonds like these.

But if the money is going into a DBS Multiplier or money market fund, then Astrea VI is a very solid choice. The 3% just offers a very attractive risk-reward compared to anything cash can offer at the moment.

Will I be subscribing?

I think I will actually.

I have a whole bunch of funds sitting around in DBS Multiplier, Endowus Cash Smart, and Syfe Cash just earning what 1.4% a year?

For a small bit of extra risk, I’m easily doubling the return here to 3.0%.

So yes, I think I will allocate a portion of my cash into Astrea VI.

It cannot be too big as a proportion of my cash though, because Astrea VI is not liquid as we’ve seen, and it may take some time to get the money back.

In times of exceptional stress like March 2020, these bonds can and will trade below par.

But as long as I have sufficient liquid cash on hand, and I can wait a few days to a few weeks to access the cash here, I think Astrea VI works for me as a place to park cash.

That’s just me though – you need to decide whether the same analysis applies for you.

How likely am I to get Astrea VI?

I’ve extracted the balloting tables for Astrea IV and Astrea V below:

Astrea IV

Astrea V

Basically, the sweet spot is around $11,000, which gets you about a $5000 to $6000 allocation.

This gives you the most bang for your buck.

The next jump requires you to apply for about $40,000, and you only get $1000 more in allocation.

Almost everyone that applies will get something.

Temasek (or Astrea) does it intentionally this way – so that everybody who applies gets some, but nobody gets a lot.

Of course – this is based on historical performance from Astrea IV/V. They may decide to switch things around this time.

How to apply for Astrea VI?

Application is already open, and it closes on Tuesday 16 March at noon.

If you’re keen don’t forget to “press button” before then.

You can apply via ATMs, Internet Banking, or Mobile Banking.

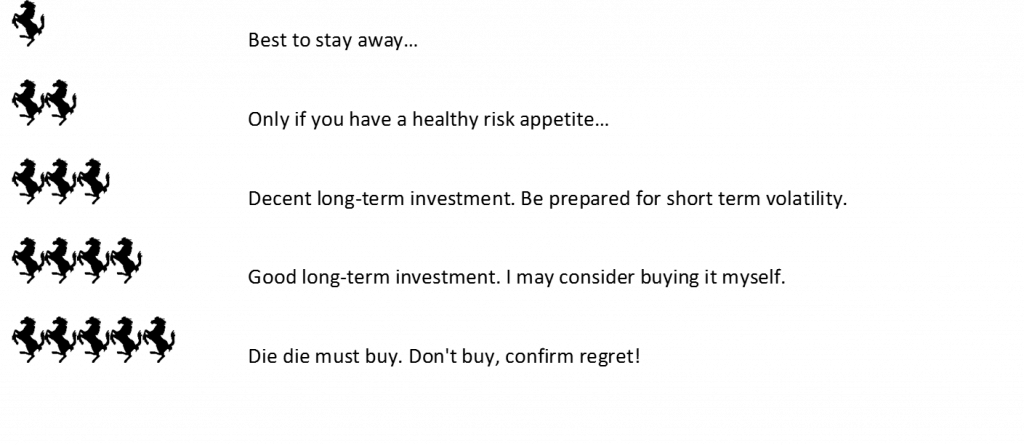

Closing Thoughts: 4 Horses for Astrea VI

The Astrea IV bonds was the first and only investment product to have a full 5/5 Horse Rating from me, since Financial Horse came into being.

I don’t think Astrea VI is on the same level, because frankly, I really would have wanted to see a higher yield.

I know that yield spread is the same as the previous bonds, but 3% just doesn’t have the same kick to it. I mean 3% is just 0.5% more than my CPF-OA!

But there’s no denying that Astrea VI just offers a fantastic risk-reward profile, unmatched by anything in the market right now.

Seriously – I just don’t think there’s any product out there with a similar risk-reward.

Anyway, Astrea VI is a 4 horse rating for me, and full disclosure – I will be subscribing for Astrea VI as well.

Love to hear your thoughts – will you be subscribing for Astrea VI?

Astrea VI – Financial Horse Rating

Financial Horse Rating Scale

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Both are THE best quality investment courses available to Singapore investors out there!

Dear FH,

Thank for the write up. I appreciate it.

Quick question. I am aware that we cannot use SRS fund to subscribe to this bond at launch. However, after the initial launch, will we be able to use SRS after this bond start to trade on SGX?

Thank you

Sorry for the late reply. Yes I believe you can.

Thank you for replying. Much appreciated.

No problem, glad it helps!

Wanted to highlight that Astrea VI is slightly below $1 now (19May22).

Yes, with the rising interest rates this isn’t totally unexpected. Fixed income in general has been selling off.