First off – I do want to say that I might not be right about this.

Buying China banks now is like buying Citibank or AIG in 2008.

You’re either going to look like Warren Buffet in 5 years, or you’re going to lose everything.

But then I figured – What’s the riskier move now:

- Buying China banks at 0.35x book value and a 7.5% yield, or

- US Growth stocks at 100 times Price/Sales into a Fed hiking cycle?

Whatever the case, I’ll share my thought process below, and I would love to hear from you.

Whether you think I’m nuts, or I’m missing something – Just let me know!

Basics: China Dividend Stocks – Too Cheap to Ignore?

If you haven’t looked at the China Dividend Stocks for a while, you’ll be amazed at the valuations.

The 4 big banks – ICBC, CCB, ABC, Bank of China, all down about 20%+ from highs.

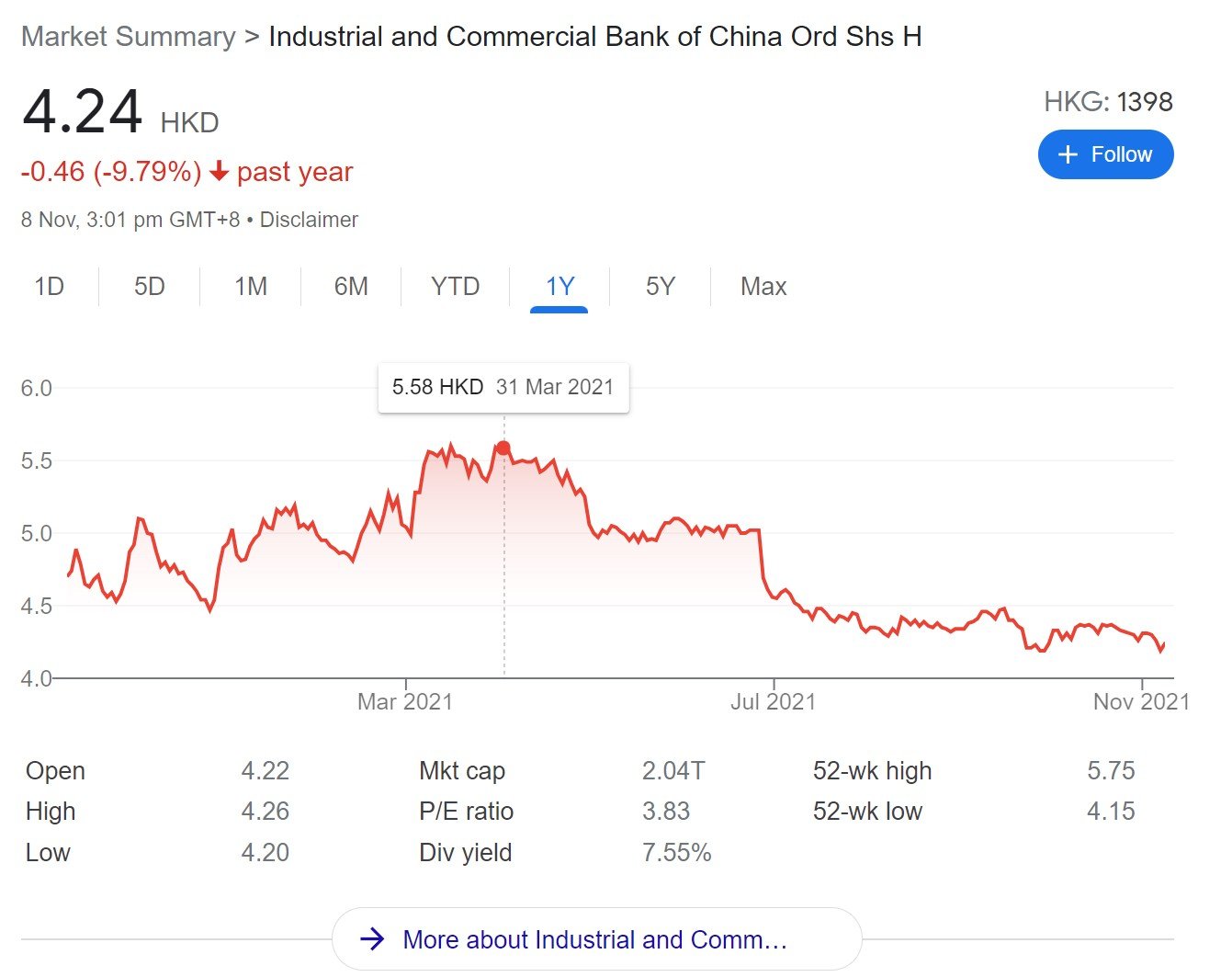

Here is ICBC, the largest bank in the world.

Trading at 7.5% dividend yield, and 60%+ discount to book value.

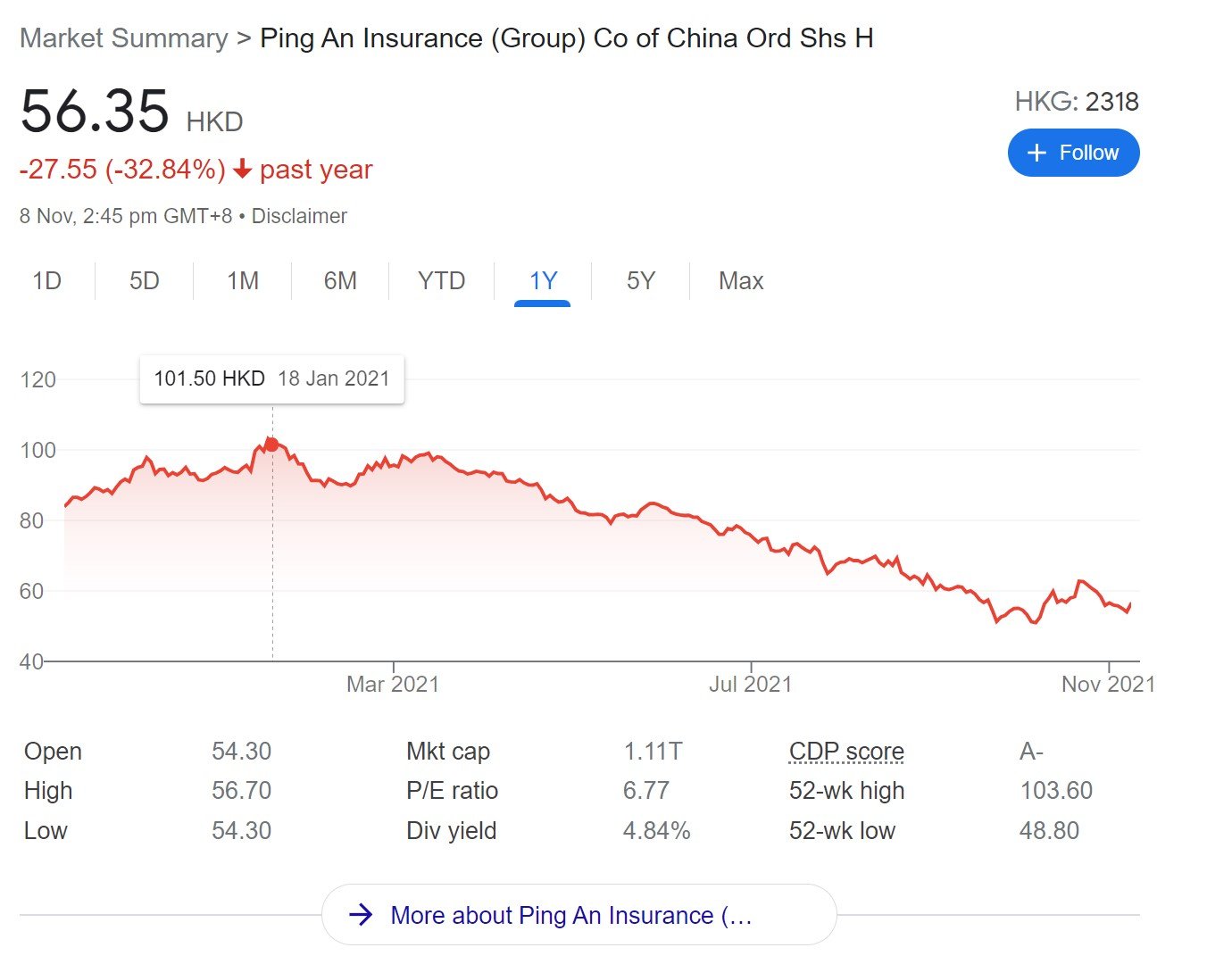

Ping An, the largest insurer in China – down 50% from highs, at a 4.84% yield.

Which is higher than some blue-chip REITs in Singapore. Don’t forget there’s no dividend withholding tax between HK and Singapore, so that full dividend goes into your pocket (there is 10% between PRC and HK though, so you pay 10% withholding tax all in).

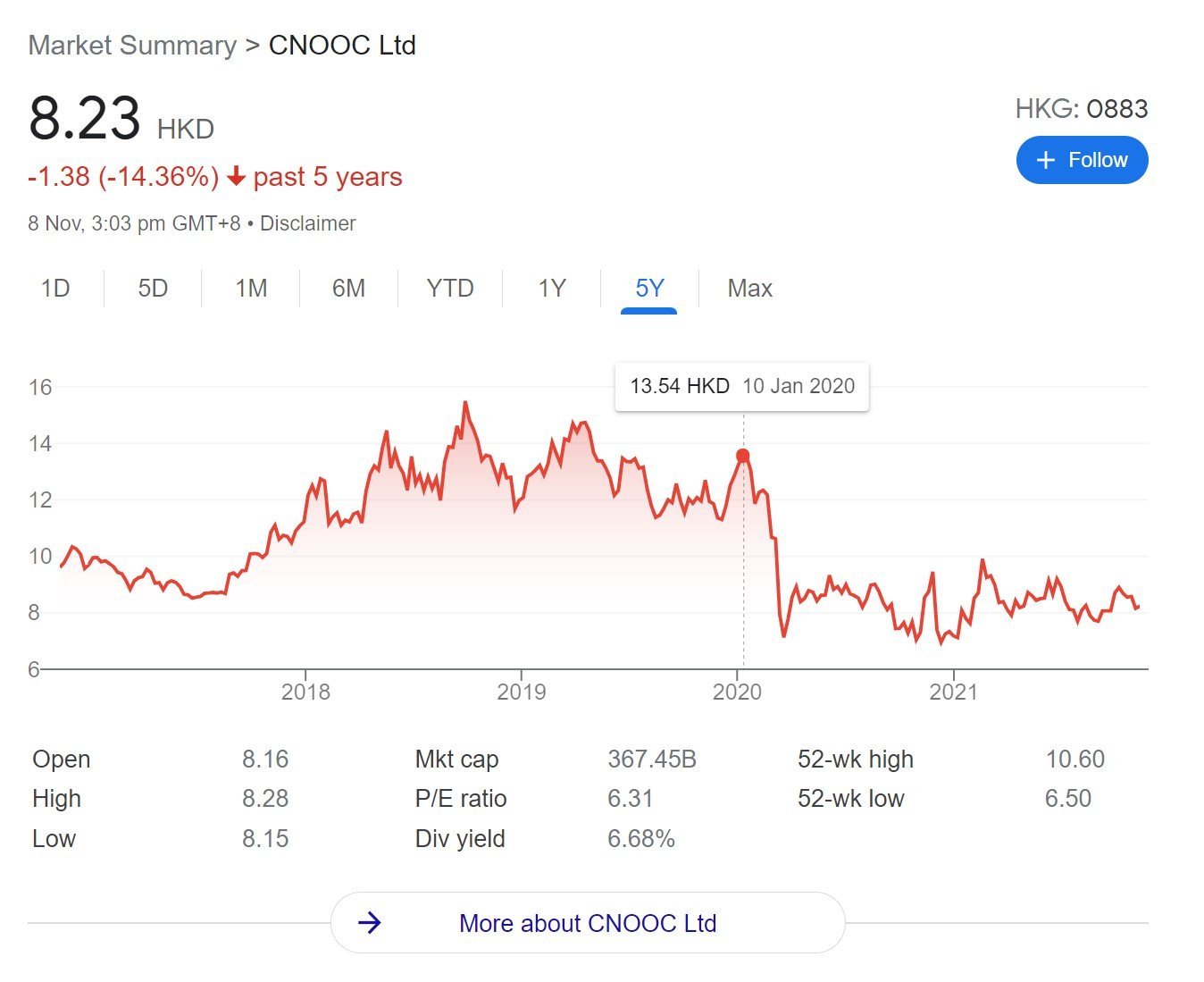

The China oil companies – Petrochina, Sinopec, CNOOC, down about 40% from highs, and trading at 6.68% yield (CNOOC).

Look at how CNOOC is down 40% from pre-COVID, and compare that to Exxon where prices have recovered to pre-COVID.

I know that there is a lot of China risk, but as investors the question is at what point do we take this policy risk to be priced in?

What do earnings look like – ICBC

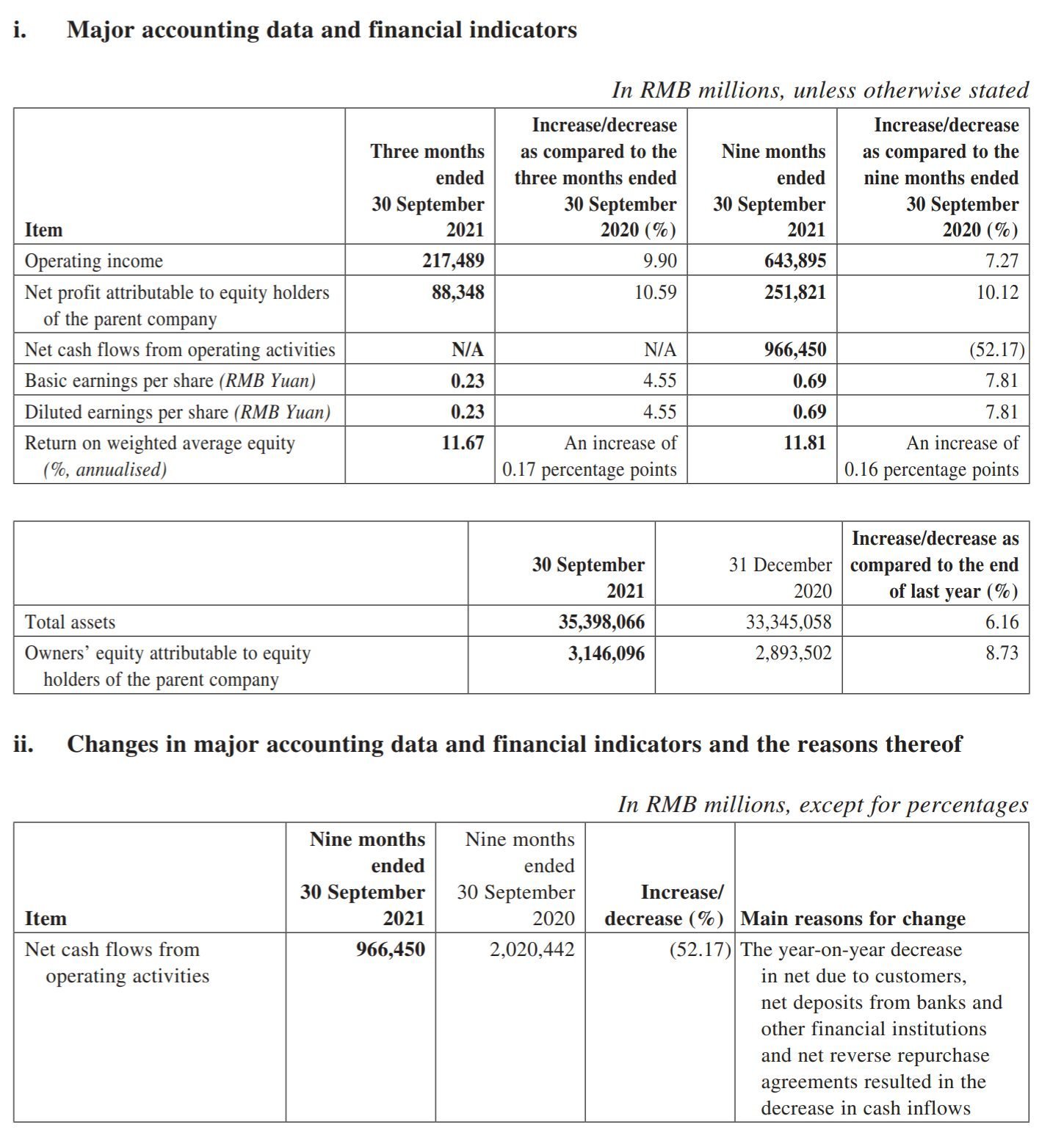

For the record, this is what ICBC’s earnings look like.

Net profit is up 10.5% year on year, EPS up 4.55%.

60%+ discount to book, and a 7.5% dividend.

But really, that’s missing the point to me. The elephant in the room is China’s real estate crisis, and China policy risk.

China’s Lehman Moment is playing out fast

We talked about Evergrande (恒大)being China’s Lehman moment. If you haven’t seen it yet, go read it as it provides important context.

Long story short – Things are getting hairy for China real estate, real fast. With echoes of 2008.

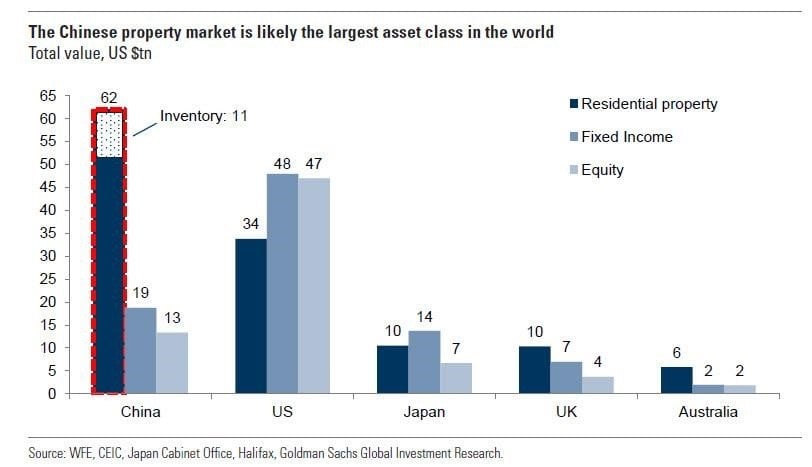

Real estate is 40% of China’s economy, and possibly more for a China bank’s loan book.

To understand if China banks are a good investment, we need to understand how the real estate cycle is going to play out.

As a Property Developer, there are 3 ways to raise money, all of which have been hit very badly:

- Sell Properties

- Borrow from a bank

- Borrow from Capital Markets

Sell Properties

Property Transaction Volume in China is down 30 – 40% year on year.

Home prices have fallen 30-40% in a year in some cities.

Homebuyers are frightened that if they buy a new property now, they may never get it because the developer goes bankrupt.

No property sales, means no cash flow for property developers.

Sure, you can sell your EV business like Evergrande, but when there’s blood in the water everyone smells it. You’re never going to get anywhere near fair market value for your assets.

Borrow from a Bank

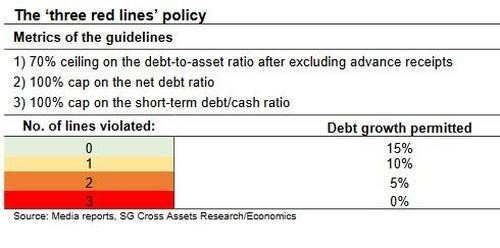

The three red lines set out guidelines on how much debt a property developer can borrow.

Most of the most indebted developers (like Evergrande) violate the three red lines, so they can’t take on additional loans from banks.

Borrow from Capital Markets

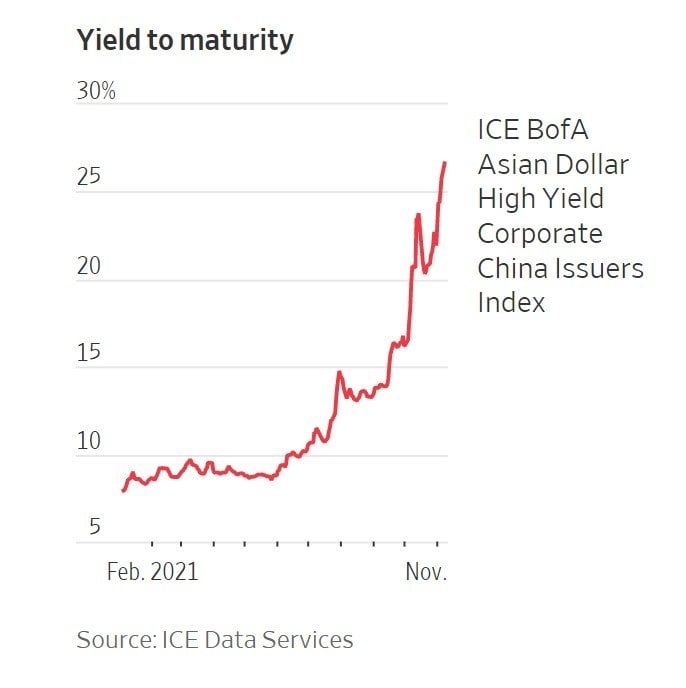

China high yield dollar bonds are trading at 20%+ now, which is getting close to 2008 levels.

China property developers are effectively frozen out of capital markets.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Contagion is spreading fast

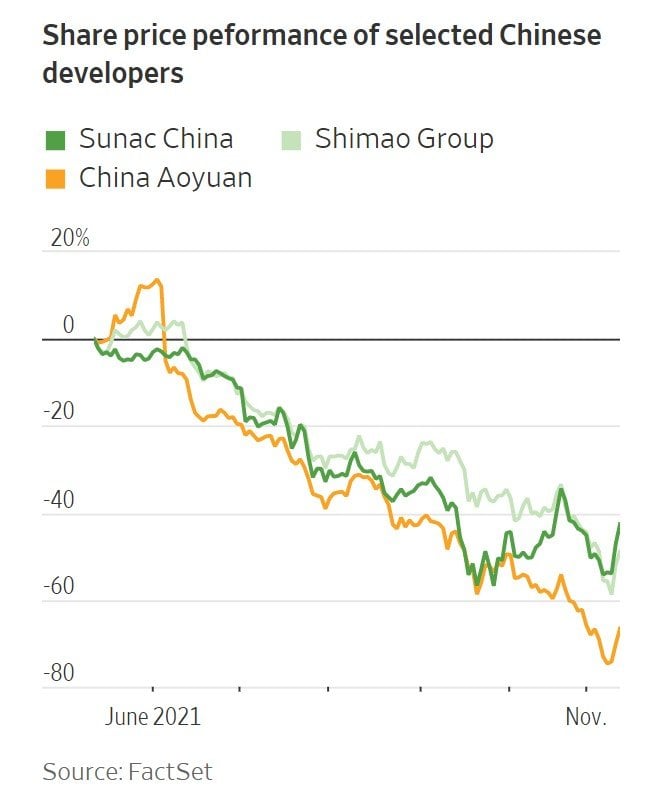

The past week saw China developer Kaisa Group Holdings default on its wealth management products, and call for trading halt in HK.

Here’s the share price performance of the other China developers:

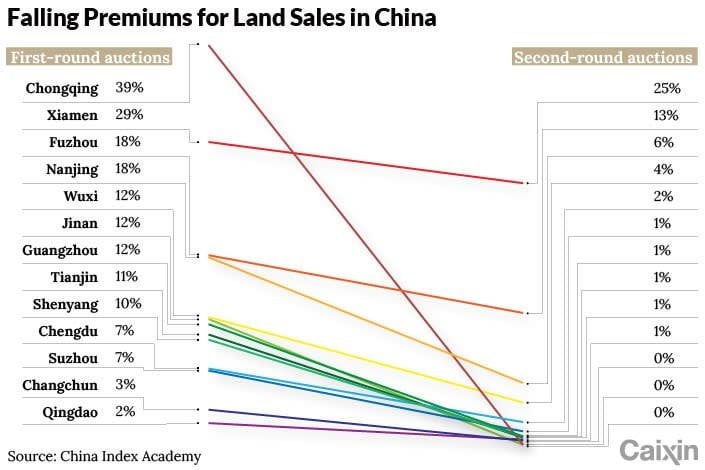

Government land auctions are also in trouble, with 27% of land parcels failing to attract buyers, and land premiums falling across the board.

Land sales are a big driver of local government income, so this will have broader knock-on effects (reducing local government spending).

In my view – there’s only one way out of this, and that’s for the CCP to step in.

Has the CCP Blinked?

It wasn’t very clear how, but this week Evergrande made payment and avoided defaulting on their bonds.

The WSJ also reports that CCP is looking to ease some of the restrictions on property developers.

Long story short – if you buy properties from another indebted developer (eg. Evergrande), the leverage taken on wouldn’t count towards your own three red lines.

This is a big move – sparked a huge rally in China real estate shares on Thursday.

If you were looking for a sign that the CCP has blinked, this might just be it.

Will this be enough?

I can’t help but feel that this isn’t enough though.

This is playing out like a classic real estate cycle.

Prices come down, people stop buying, developers have no cash flow, they are forced to fire sell, in a vicious cycle.

It’s a crisis of confidence now, and a small tweak like that may not be enough.

No official word out of Beijing, nor has the PBOC done any liquidity injections.

So even though a bailout will probably come eventually, for now Xi is happy to sit on his hands and watch everyone sweat.

Real Estate speculation is dead

Even if they do step in, my sensing is that Beijing is serious about stamping out speculation in housing. Which means that real estate growth will stay slow for a while.

From Caixin (emphasis mine):

In a Sept. 29 report, Tianfeng Securities expects real estate sales and financing to get some relief in the fourth quarter. But most experts say the thrust of Beijing’s “houses are for living” policy will not change in the long run, and it is difficult to reverse the sector’s long-term cooling.

Multiple people close to the sector told Caixin that there will not be a fundamental shift in real estate financing policy. China’s tightened management mechanism for real estate lending will stay in place as part of normalized policy, the central bank said last month in its 2021 financial stability report.

…

The central government has insisted that property not be used as a short-term stimulus for the economy, said Zou Lan, head of the financial market department at the People’s Bank of China at a news briefing on Oct. 15. The central bank asked lenders to keep credit to the real estate sector “stable and orderly,” he said.

What are the risks with China banks?

Where do I even start.

First off – the book value is a complete black box.

Go pour over the financials of ICBC – you’ll have absolutely no clue what’s on the loan book.

The asset base is $5 trillion, but if they actually call on those loans, what percentage of that can be repaid?

Secondly – China risk.

If things start blowing up, the China banks are going to be asked to step in in the name of national security.

They’ll be asked to extend loans to indebted property developers to stave off contagion, and they’ll be asked not to call on existing loans. They may even be required to buy out certain toxic assets.

And of course – real estate risk.

We talked about this above, so I won’t belabour the point. Short term, it looks like a lot of these real estate loans may go bad.

Is there implicit state guarantee?

When I was in China a few years back, I remember talking to a local fund manager.

He told me not to overcomplicate matters – and just buy the China banks / insurers / securities companies.

He acknowledged that the book value was a giant black hole, and that nobody knows their true worth.

But in his view, as long as you’re investing in one of the SOEs (like Ping An and ICBC etc), the China government would never allow them to default.

In his view, you could buy them, and collect the fat dividend year after year without fear that it would be cut. And just ignore the short term fluctuations in price.

At today’s prices, that fat dividend is 7.5%. As long as you can sell the banks at breakeven in 6 years, you’re already up 50% from dividend alone.

Look at the bigger picture

The problem is that the real estate crackdown is not an isolated incident.

It’s happening at the same time as a crackdown on China Tech, on data security etc.

All happening while China is trying to maintain zero COVID in the face of the more contagious Delta variant.

And quash domestic unrest.

That’s a lot of balls to juggle, even for the all-powerful Xi.

Buying China Banks require a leap of faith

You need to ask yourself if you believe in the China growth story, over a 10 – 20 year timeframe.

Do you believe that by 2050, China will be a global superpower, and the entire Asia-Pacific region will be dominated by China just like how America dominates the west?

If your answer is yes, I would say buy some of these SOEs, forget about them for the next few years, and just keep buying on dips. And you’ll probably make off like a bandit.

If your answer is no, then avoid China completely. The short term is very uncertain, and there are many potential paths this can take. Many of which will not end up well.

My Personal View? Are China Banks a good buy?

I know it doesn’t seem like it – but I’m an optimist at heart.

Hand (hoof?) to my heart – I think China will become a superpower by middle of this century. I just don’t know the path it will take to get there.

So I will probably add to these China dividend stocks.

At a 7.5% dividend yield for the banks, I think the risk-reward here is attractive.

This isn’t some small Thai bank we’re talking about.

The 4 big China banks (ICBC, CCB, AGC, BOC) are the four largest banks in the world. ICBC has a loan book 60% bigger than JP Morgan – the biggest American bank.

Our very own Temasek has an 8% stake in ICBC, although I don’t know if that’s a good or bad sign.

Jokes aside – I think push comes to shove, Beijing will have no choice but to bail out the sector if things get hairy. Just like how America bailed out the system in 2008.

If one can sit out the short term volatility, at some point the loan growth will return as the other sectors of the economy like manufacturing and EV continue to grow.

Which only leaves pricing, and timing.

When to start buying?

And that’s where it gets tricky.

I still think things will need to get worse before they get better.

To put it in 2008 terms, I think we’re somewhere in June 2008 (Lehman was in Sep 2008).

With bond yields at 20%+, it feels like we’re getting close to point where somebody blinks. Either the CCP relents, or bigger things start to break in the economy.

I would say that in 3 – 6 months, we either have something blow up. Or the sector starts to recover.

That said – I missed the bottom for China in Feb 2020 because I underestimated the role of policy in China.

So take my timings with a pinch of salt.

For China, you want to look for the narrative shift as your cue to start buying. Unlike the West where you look at actions.

Some of you may argue that the policy tweak by the CCP this week marked the start of the narrative shift.

Definitely possible.

It’s a tricky call though – and I’ll much rather be late and miss out on some gains, than be early and buy into a 20% decline.

Watch your risk, the upside will take care of itself

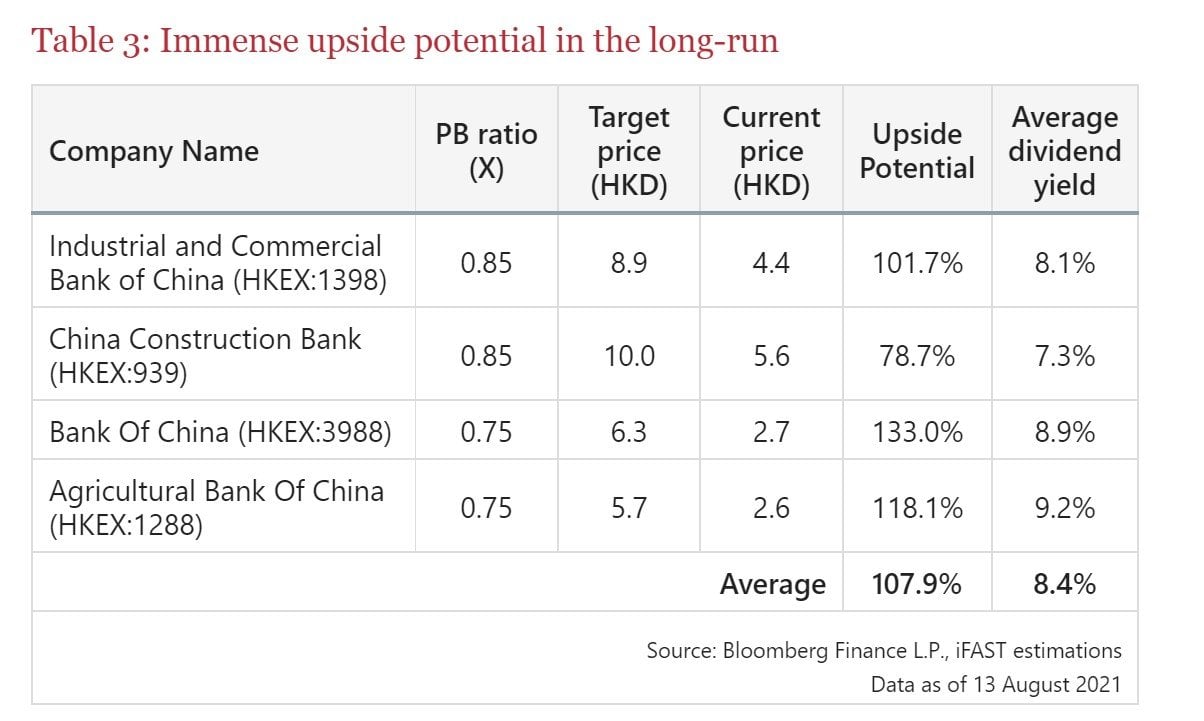

FSMOne has this chart that shows the upside potential of the 4 big China banks:

To me that’s the wrong way of approaching the issue (and also wildly overoptimistic – the banks will never go back to 0.85x book value).

In investing, you always look after your downside first, and let the upside take care of itself. Not the other way around.

Risk management wise, I’ll probably want to cap exposure to China banks at no more than 5% – 10% of my portfolio in case I’m wrong and things go south.

I also want to average in in case I’m wrong, at least until Xi’s “reelection” late next year.

Full disclosure: I haven’t started buying the China banks yet (apart from the positions I hold from a few years back). But I may start soon, perhaps as early as next week.

Do note also that I may change my decision if the facts coming out of China change, and this article won’t be updated going forward. If you’re interested my latest views and buy/sell timings are available on Patreon.

What to buy? China Dividend Stocks?

The banks are interesting to me.

The 4 big ones (ICBC – 1398, CCB – 939, ABC – 1288, BOC – 3988) are all fine.

It’s like DBS v UOB v OCBC, if the Singapore economy recovers they all go up. Personally I like ICBC and China Construction Bank, but that’s more for personal reasons.

I like Ping An too, and possibly also the oil companies. CNOOC is very cheap considering oil has recoved to $80 a barrel, and it is still at COVID lows.

China real estate might be a bit too early to touch, unless it’s via one of the offshore players like CapitaLand / Link REIT / Hang Lung / CapitaLand China Trust etc. I think real estate growth will be subdued for a while.

China Tech too, but the analysis for that is slightly different from the dividend stocks, as there are other considerations in play.

You can check out my China Stock Watch for the full watchlist – I’ll be updating it this month to include the China dividend stocks.

Closing Thoughts: China Stocks uncorrelated with Western Stocks?

After last week’s piece on Best Growth Stocks, a lot of you expressed concerns about valuations and late cycle timing.

And that got me thinking – what is the one asset class that is uncorrelated with US stocks?

Like we saw in March 2020, even things like Gold and Treasuries are no-bid in a liquidity event, when all the risk parity funds sell at the same time.

China stocks are interesting because at this point, all the momentum chasers and hot money have already exited. All the hot money is in US Growth and Crypto now.

On Wednesday when US growth was selling off on inflation fears, China tech stocks were actually rallying.

So as we head into the new Fed hiking cycle, China stocks that are down 30%-50% from highs could provide a portfolio hedge?

Who knows!

Love to hear what you think!

As always, this article is written on 12 Nov 2021 and will not be updated going forward. Latest thoughts (and my stock watch and personal portfolio) are available on Patreon.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a Free Apple stock (worth S$200) when you open a new account with and fund $2000.

Get 1 free Apple share (worth $200) you’re new to and fund $2700.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

Thumbs up again for a great post. I totally agree with the story, DBS CIO adopts a similar approach, I also hold chinese banks for the very same reasons you have listed. On the risk side, I believe the central government is more than capable to manage this. Why? Because when I look at how they handled the AFC of 97-98, this really seems like a walk in the park. Sure they might take some losses here and there, perhaps 3% NPL next year? Who knows. But seriously, 5- 7% free money every year, moving into 2022-2023 interest hike, with the VIX going crazy this year, when global equity looks more concentrated and more unstable then ever before, 5 – 7% stable guaranteed return? I’m taking it. Of course this is time horizons of 5 years and above. For those who are thinking short term, 1 – 2 years, this will not be suitable since the growth upside is limited and whatevercoins will probably outperform.

The China fund manager I was speaking to made the exact same argument.

Just take the leap of faith, collect the 7% dividend a year, and at some point the govt will bail everything out so you can probably sell at the price you bought anyway. Which leaves the dividend as pure profit.

Investing in China requires a different mindset from investing in the west. 😉

the sure way to make $ in china is to align with their strategic plans… see solar panel makers : Flat Glass, green energy : Ganfeng Lithium, CATL, BYD; Semicon : Global X China semicon ETF. If you had went big on these, you’d have made a killing, without much risks.

Agree with this. But we can’t go back in time, we need to invest in the market as it is today.

So question is – is there still money to be made in solar/EV China stocks today? Otherwise, what is the next trend to bet on?

Wait for a correction lor. What else can we do?

Although the returns going forward may not be as juicy as before. The gov needs these industries to survive and do well to meet their goals. Notice there was little or no crackdown in those industries

China banks have been in a value trap for ages -https://www.bloomberg.com/news/articles/2020-09-08/chinese-bank-stocks-lose-187-billion-in-never-ending-value-trap

1. Will this dissapear in the long-run, most likely, but here is where art is more important than science, how do you define “long-run”? 5 years, 10 years, 20 years? What about the opportunity cost you lose by not investing in say the S&P500?

2. I believe the value trap exist to account for 2 things – investors confidence in the rule of law and the data being disclosed. Unless these gaps are closed, the value trap is be persistent.

3. Sure, one can take a pun and invest in these banks and if lady luck is smiling at you, you can 2x, 3x your money. But let us also be aware of the risk that one is taking.

Yup, I don’t disagree with this. People have been talking about bad debts and a real estate crash for 20 years. There’s a reason why these things are cheap.

But the dividend is very real though, and it’s real cash in your hands while you wait for the bailout.

10 years ago ICBC was at $2, so with a long enough timeframe prices could still go up. This is China, as long as the big 4 don’t go bust, surely at some point in time loan growth will start to recover?

Kinda like going back to the 1970s and buying JP Morgan. Sure, it was a wild ride, but it eventually paid off.

i think the idea is to park your money there waiting for a chance to deploy into US when it drops anywhere from 10-30% while getting juicy dividends.

Yes, it’s strange because we just came out of the COVID recession, but the US stock market looks very late stage cycle. Going into a fed hiking cycle will be tricky, esp when the market is pricing in 2 – 3 hikes next year.

H shares have 10% dividend withholding tax. Thus if 7% div yield, will only net get 6.3%. Example: ICBC. However, if its is HK companies, no withholding tax like you mentioned in your article. Example: Hang Seng Bank.

Thanks my bad – there is 10% from the PRC to HK leg. Have corrected this. 🙂

“Don’t forget there’s no dividend withholding tax between HK and Singapore, so that full dividend goes into your pocket.”

This is not true. There is 10% dividend withholding tax if the company is indoctrinated in China (i.e. Ping An, China Banks).

Thanks my bad – there is 10% from the PRC to HK leg. Have corrected this. 🙂

I own BOC 3988HK bought through a bank in Hong Kong and have to pay 10% WHT on the dividends. In your article, you mentioned “Don’t forget there’s no dividend withholding tax between HK and Singapore, so that full dividend goes into your pocket.”

Did my bank made a mistake?

Thanks my bad – there is 10% from the PRC to HK leg. Have corrected this. 🙂

Dear FH,

Another good article from you again. 2 questions.

1) Are there any ETF that is focus on these big bank in China that we can buy instead of buying the individual banks share?

2) Are there anywhere we can read more about these big 4 china bank. for example who are their big shareholder, customer etc?

Thanks

Thanks aaa, my comments:

1) You can look at MSCI China or FXI, but they give you broad exposure to the China large caps, and not specifically China banks. I suppose there should be an ETF that focusses specifically on China’s financial sector, but I reckon liquidity will be bad – so it might be best to just buy the banks direct.

2) Yup, you can look at the annual reports / quarterly financial results. The disclosures just paint a rosy picture though, you won’t find any of the juicy stuff in there.

Yes

The CHIX ETF is a dedicated financial ETF for Chinese BFI listed at the NYSE, the charges are reasonable

I have boughtvand sold this recently

I hold all the major Chinese banks via their HK listings for about 20 plus months now

Bought them early 2020 after the epidemic started. Still underwater after recent dip despite 2 years of good dividends . The dividends are annually paid and that is around mid year

I could have sold and made money but will hold them and add again if they drop further

As usual, portion sizing is the key and they are a trade as well if you sell just before they go ex dividend

Garudadri

Thanks! Appreciate the sharing! 🙂

Interested to hear your thoughts on Ping An and the Chinese oil companies. Especially for the Chinese oil companies, what are their unit economics like? Cost of production, amount of reserves, domestic obligations etc

I just wrote a deep dive into Ping An for Patreons this week. Long story short is I like it, but the risks are very similar to that of the China banks.

China oil is very interesting, I looked at them the past week and it turns out a lot of their E&P comes from South China Sea/Africa. I would imagine the unit economics would not be good if that’s the case. Will do a deeper dive and see what I can find.

Hi FH,

Great post. If you recall, I raised the idea of China banks to you a while back and with their recent decline, it has got a lot more interesting.

Fundamentally, as you said, it all boils down to whether you believe China will thrive despite unremitting attempts at containment by the US. If so, then it is a no brainer to invest. If not, it will be a bumpy ride to say the least. Huawei, the Apple of China has been reduced from almost #1 in mobile and 5G to an also ran in just a few years so don’t underestimate this.

Nonetheless, the dividends provide a significant margin of safety over the medium to long term. I bought into Bank of China 3 years ago and with 7+% after tax dividends for 3 years, the margin of safety has grown to 20+% as the price is still above my average purchase price. So there is really no need to wait to buy at the bottom if one is planning a holding period of 10-20 years as you will essentially get your capital back within this timeframe as these banks are the literal definition of too big to fail.

Some may argue about opportunity cost but right now, HK listed shares are the lowest priced by a large margin using typical valuation metrics compared to other markets around the world. Yes, there is risk and in the next 1-3 years, no one can predict the direction. But if one believes China will survive and have a 10 year holding horizon, then this would be a rare opportunity to buy when others are fearful.

Hi CMC,

Yes – I think you just summed up the entire issue perfectly.

It really boils down to 2 issues (1) whether one believes in China long term, and (2) how to time the bottom.

(1) is ultimately a personal decision. We can debate all we want about the arguments for and against but ultimately there’s a bit of a leap of faith here.

(2) we can make educated guesses, but it will be close to impossible to time the bottom perfectly. Prices are cheap now, but they can go cheaper, or this could be the bottom. Averaging in would make sense from a risk management perspective. I missed the 2018/2019 short term bottom (during the Trump trade war) for this exact same reason too, because I was trying to time the bottom and then got too busy with life.

Hi, I believe CCP will prevent a recession at all costs as Xi’s election is coming up. As CCP has tight control over the economy, they can always use policy tools to avoid a recession. I have confidence in them seeing how they managed past crises. The economy is still growing although not as strong as before due to energy crisis, inflation, real estate and covid. One worry is their covid-zero policy, not sure what’s the long-term effect. But the question is, will these banks cut dividends since they are SOEs and may be asked to do ‘national service’? As to correlation, I think they have burst the HK stock bubble back in 2020 Dec (perhaps unintentionally as a by-product of ‘crackdown’). If you look at the charts of many tech stocks, you will notice there was strong surge towards Dec 2020 followed by sharp downturn til now which coincided with the crackdown timeline. As such I believe a lot of the funds “fled” to US and cryptos driving up the valuations even more. This year is an extraordinary one in which CCP wants to deleverage and crackdown on malpractices in the private sector.

Well all that is holding the bank stocks up is the dividend now. If they cut the dividend, there’s going to be a big crash. But I agree that it’s a possibility to bear in mind for investors.

Good point on the hot money moving from China to US, perhaps that’s what drove the US momentum stocks up even more in recent months.

The yield is tempting, but there is a lot of geo-political risk.

– Bailing out banks means recapitalising them at the expense of shareholders. Especially foreign shareholders. Look at how foreign Evergrande bondholders were treated.

– China’s economy has grown spectacularly since 2001 from favourable demographics, free trade, and a real-estate bubble. All 3 factors are now reversing. The next 20 years will not be like the previous ones.

– Any shooting over Taiwan or the South China Sea and all these shares go to zero. Could happen if the CCP sees themselves losing power due to a slowing economy.

So does a 7% yield make up for the risk of them going to zero?

Yes, that’s exactly the question. 🙂

For what it’s worth, I don’t think the CCP will wipe out foreign shareholders in a bailout. Look at US in 2008, all bondholders and shareholders escaped unscathed. The problem if you wipe them out once is that it will take years for foreign capital to come back in again. Seems to be penny wise pound foolish.

Agree on demographics, that’s a big tail risk to watch for China. They need to improve productivity and efficiency via systems and technology, faster than demographics.

FWIW – Taiwan I am less concerned about. Lots of posturing there, but I don’t see a hot war breaking out unless like you said, Xi is in real danger of losing power. Then all bets are off.

It’s China though, and this is part and parcel of investing in China. 🙂

Dont you think they can outsource low value manufacturing to other countries? Case in point: Textile making have been outsourced several years ago .

Actually dont know why you guys so scared, i have a sizeble investment in China stocks. I dont see any big risk. A lot of the risks are temporary or can be mitigated. Growth forward is likely to slow as they pursue higher quality growth instead of cheap real estate and low manufacturing. War between the 2 big powers wont break out. I mean Us and soviet didnt even dare to fight a direct war … china is unstoppable at this stage despite all efforts so far

Hmmm….for a bailout, the bank issues to the government.

Shareholders in Citibank got diluted. This article says they quadrupled their shares (https://money.cnn.com/2009/05/22/news/companies/citigroup_share_dilution.breakingviews/index.htm?postversion=2009052215). Those who made money bought *after* the bailout. And I think there was more than one bailout.

Yeah, I don’t think we get a war, everyone has too much to lose.

Actually why will go zero? If war breaks, taiwan sure lose unless there is external intervention then the outcome not so clear. Also dont forget many large Us corps derive significant revenues from china which is still the world factory. Any ‘civil war’ will cause a crash in global markets not just in HK/china since supply chains and economics are so intertwined

In any war, the world changes:

– China loses access to all shipping, any western investment, and cannot trade with any country that trades with the US. All their energy imports need to come overland, from Russia/Iran.

– If China wins the war, South Korea, Vietnam and Japan develop and test nukes. The first two have been invaded by China since WWII, and the Japanese hate them. It is a matter of survival.

You still think anyone can transfer money to/from China in this new world? Let alone trade their shares.

Why lose access to all shipping? In any case if a war breaks, the whole world loses. Hard to debate what happens. A lot of it is your own imagination 🙂 developed countries lose access to cheap and essential goods from china which is also a big pain. Shelves will be running empty worldwide. World will also lose access to TSM once taken over by china

You are right, there is no need to think about war yet, it is unlikely to happen now.

I see more risks in Us stocks than China at this point. The latter is basically unstoppable with growing leadetship in many high tech and hard tech areas and self sufficiency in chips. And also a strong military to deter invasions. All containment efforts so far have come to nought. Even Us want to reduce trade war due to inflationary pressures. Go research who loses in the trade war. In tech war , domestic companies have pressured gov to continue selling chips to china. The former is racking up debt at an alarming rate. 130% national debt to gdp. Total debt including household and corp debt are even more scary. 40% americans cannot afford $400 emergency spending living paycheck to paycheck. 70% of gdp based on consumer consumption. What happens when they cannot consume as much as before? Growing defense budget and annual deficit run in billions. Debt growing faster than economy. Basically its runaway debt with no point of return. The govt has zero interest in solving the debt problems. They just kick the can down the road. Debt interest projected to be 10% of federal budget in 2030. Basically they have to borrow $ to pay interest. Its a snowball debt. Although the whole world is “paying” for it by pegging to USD and using usd as reserves. Whether the recent bills can help I am not sure. They take years to repair and build infrastructure, too late and too little. Too much money pocketed by the cronies. China also a lot of debt but they are actively delveraging and enjoy higher economic growth. They just have to catch up in semicon and space and other tech to bring billions of growth to economy. Dont even have to invent anything new. Both are strategically decoupling from each other in certain areas. Once the decoupling is fully complete, china will be less and less dependent on Us which is quite dangerous in the sense that a growing power is abandoning a declining power which can be left to rot . Am I missing something here?

The points are all logical.. and I agree. But still too early to dismiss the US’s ability to retain power + their Allies in Asia that are scared of a rise in China. South Korea probably doesn’t want to go back to being a China vassal state, Japan raped Nanjing in the past, not sure if they are confident China wouldn’t take vengeance, Australia is an American puppet and has basically burnt bridges with China. US’s debt is unsustainable by themselves.. but could they request these other countries to share their burden? Probably. So their debt, shared among 3 Asia countries + Western puppets is probably quite manageable. Although, this probably depends on the real market pricing of their debt once the FED turns off the monetisation tap. Nonetheless, agree that China is the way to go, and they are smarter, more hardworking, and more humble than Western powers. The US showed their disgusting hands with the Plaza Accord, and China has learnt. That trick will never work again.

SK has sizeable debt itself and too small to absorb much debt. http://www.businesskorea.co.kr/news/articleView.html?idxno=80730

Japan has the largest national debt in the whole world. How are they still able to take on the debt when the day comes? Japan is basically an old man living his last days (to put it crudely, waiting to die). Its economy cannot grow anymore due to suppression from US and China eating its lunch. Its being squeezed in all directions.

Western Europe also laden with debt. Non-english speaking allies, may abandon Us. With each crisis every 10 years, the debt level rises significantly. Go look at the charts. How is sharing of debt possible?

Australia and New Zealand and other small allies, forgget it, too small. Aussie also kena decoupling from China. Its past boom was based on riding on China’s growth. Its economy growing forward is uncertain.

China just need to focus on domestic problems and follow the “Us blueprint” (minus the bad parts) to keep growing. China+Russia are friends (albeit “friends of convenience”) and who dare to touch them?

The developing countries are riding on China-led Economic Order (aka BRI and Shanghai Cooperation). Don’t you see the trend the reversal of “fortunes” (feng shui lun liu zuan)? The even bigger trend of ups and downs of empires every several hundred years?

US+allies still want to engage in arms race, raising defense budget even more.

I’m looking at facts and trends very rationally and logically. Am I wrong here?

Not to mention when a Republican president comes on stage, he may destroy all allies relations once again. LOL. This flip-flop is a f**king joke. Looks like Bidn /Democras will lose this election as the rating keeps dropping. Trump is still not giving up.

Politics of the CCP aside- I think there is too much optimism about the development trajectory of PRC. The country is navigating the middle income trap. It may never ever be a developed country – not just politically but economically. They will get old and die off before they get rich (per capita). Saying they are a superpower and will be a superpower is perhaps overstating it. The source of their only power (people) is disappearing with every year as the population shrinks. Coupled with an oppressive regime that can play emperor-god and can veer wildly from doing absolutely nothing to regulating absolutely everything at their whim and fancy gives no confidence to the world. They were the world’s factory for 30 years and made some money. But they don’t own the technology. Most of what made a Huawei phone viable was western tech and is still western tech. They just assembled it. This is a different stage of macro economic development and to think the CCP can dictate “development success” is, to put it mildly, very speculative. There are no developed communist countries in the history of the world. And they have no friends. Sure one can collect dividends for 10-20 years waiting for this to play out, but its a big risky bet.

True, I don’t disagree with this. The investment can very easily turn sour, hence position sizing is very important.

You are very biased. Look at your reply you are ignorant. Population risk is overhyped for obvious reasons. The fact is population will gradually decline but it is not so dire yet. It is not a commmunist country. It is state capitalism. They have made so many innovations: 5g,6g, hypersonics etc. you have to stand on shoulders of giants to become innovators. Everybody had to copy well first before they become innovators. Look at how western social media copy tiktok. This is just the beginning. No friends? Hello?? Middle east Gulf cooperation and BRI and Russian , not friends? China has become the largest trading partner of MOST countries globally. Look at the facts!! They are pushing out digital yuan for trade purposes. What happens 20 years down the road? It will be more widely used. I will not reply further to an ignorant fool like you. Do some research first!!!

Lol is TSM considered western tech? Who can produce the most advanced chips? Who is playing unfairly? Please look at facts and say something unbiased based on FACTS. Your dear master is suffering from millions of cases daily and labor shortages . Not to mention violence, homeless, drugs, healthcare, decaying infra, increasing wealth gap. Dementia and sleepy president . Nobody fixing the problems. Pray for them. Automation is so pervasive in china nowadays, even hotels use robots to deliver food. Population decline may actually be good so the GdP per capita goes up.

Hi FH, how about a Daiwa House Reit article? Private placements for the IPO are closing soon…thanks!

I was actually waiting for the pricing to be out to do a deep dive, but the placement tranche would be closed by then.

For now – it looks very promising though. Indicative yield of 6.5% is sound, sponsor is good, and Japan is a stable market. I think the reception should be decent for this IPO. 🙂

Great post! You’re one of the few investors who deserve attention. Most people are busy chasing 2040s earnings, glad you’re not one of them!

I started investing in Chinese SOE in mid 2021 or so. The risk/reward is so out of whack, I had to do it. The Chinese growth story hasn’t changed, just sentiment changed.

I now have roughly 33% of my portfolio in Chinese stocks like China Mobile, Yuexiu Transport, CNOOC, China Petroleum Chemical, Ping An, ICBC, CCB etc. I would never touch Chinese Tech/VIE structure, I only invest in highly cash flow positive SOEs where I have the Chinese Capitalistic Party as my business partner.

The other 66% is in tobacco stocks. My starting dividend yield of the whole portfolio is roughly 8%. I wasn’t even surprised that my portfolio surged 15% in the same timeframe the NASDAQ tanked 15% in the first month of 2022. My average p/fcf was 7.5 when I bought the stocks, now it’s closer to 9-10. Still a lot of room to go up.

I’ll keep the tobacco stocks/SOE enterprises for at least the next 10 years and expect to collect my initial investment in dividends during this timeframe and reinvest the dividends in whatever is cheap at the time. Guess the NASDAQ could be a bargain in 10 years, there will be blood on the streets, unfortunately :/

There’s very interesting! Truly appreciate the sharing.