A lot of you have asked me for my views on CapitaLand Investment recently.

The “New CapitaLand” IPOed on 20 September at $2.95, and since then it’s soared to an all time high of $3.52.

Is there something that we’re missing here? Why does the market love this stock so much?

Is CapitaLand Investment a good investment right now?

Basics: What is CapitaLand Investment (SGX: 9CI)

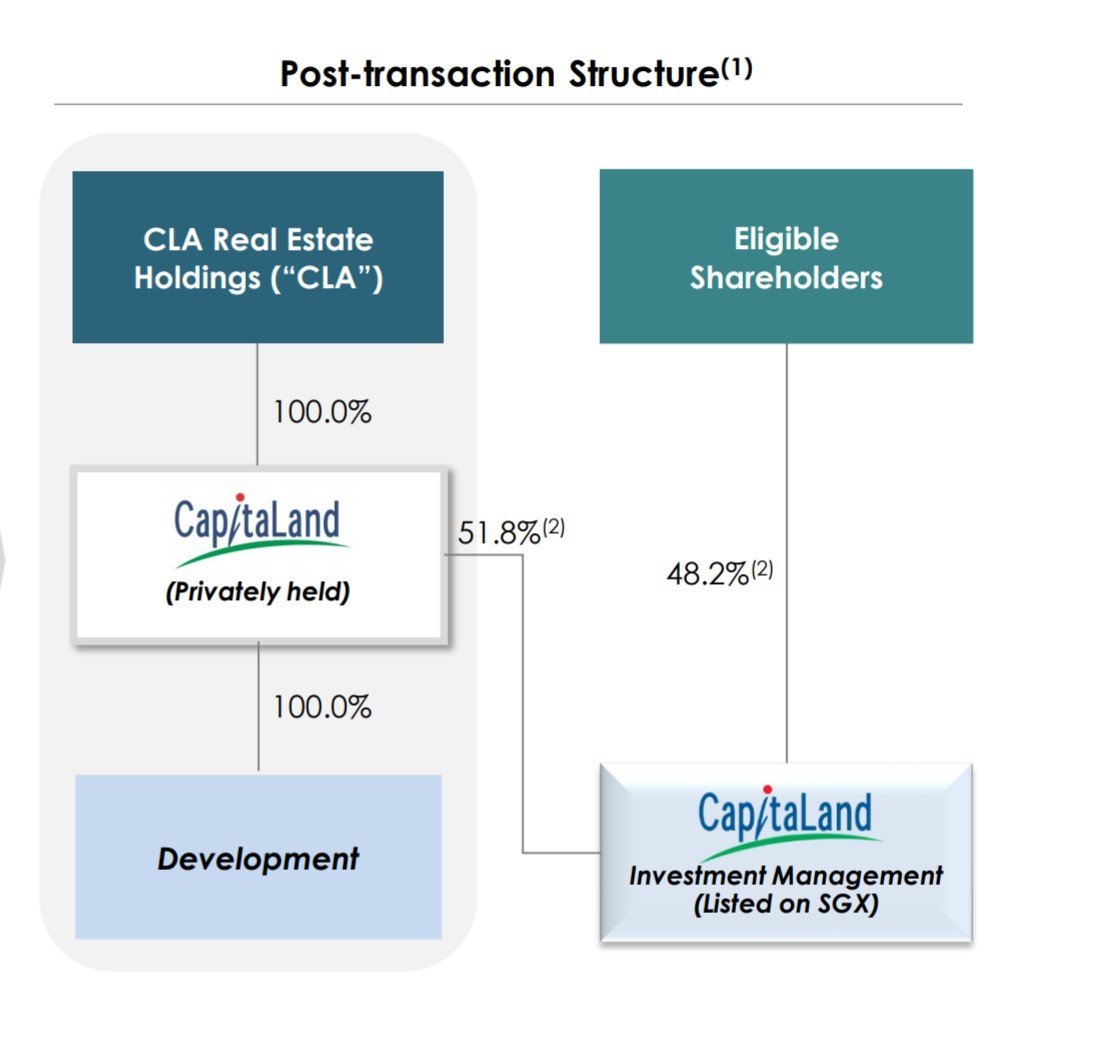

In March 2021, CapitaLand announced that they were privatizing the development business at a hefty premium.

The development business would be privately held, and only the investment arm would be listed on the SGX.

The market loved the news, and the stock rallied almost 20% after the news was released.

Well – fast forward 6 months, and the restructuring was finally completed in September. The new CapitaLand Investment listed on 20 September at $2.95.

And promptly soared to $3.52.

It’s since corrected to $3.34 though, potentially opening up an interesting opportunity.

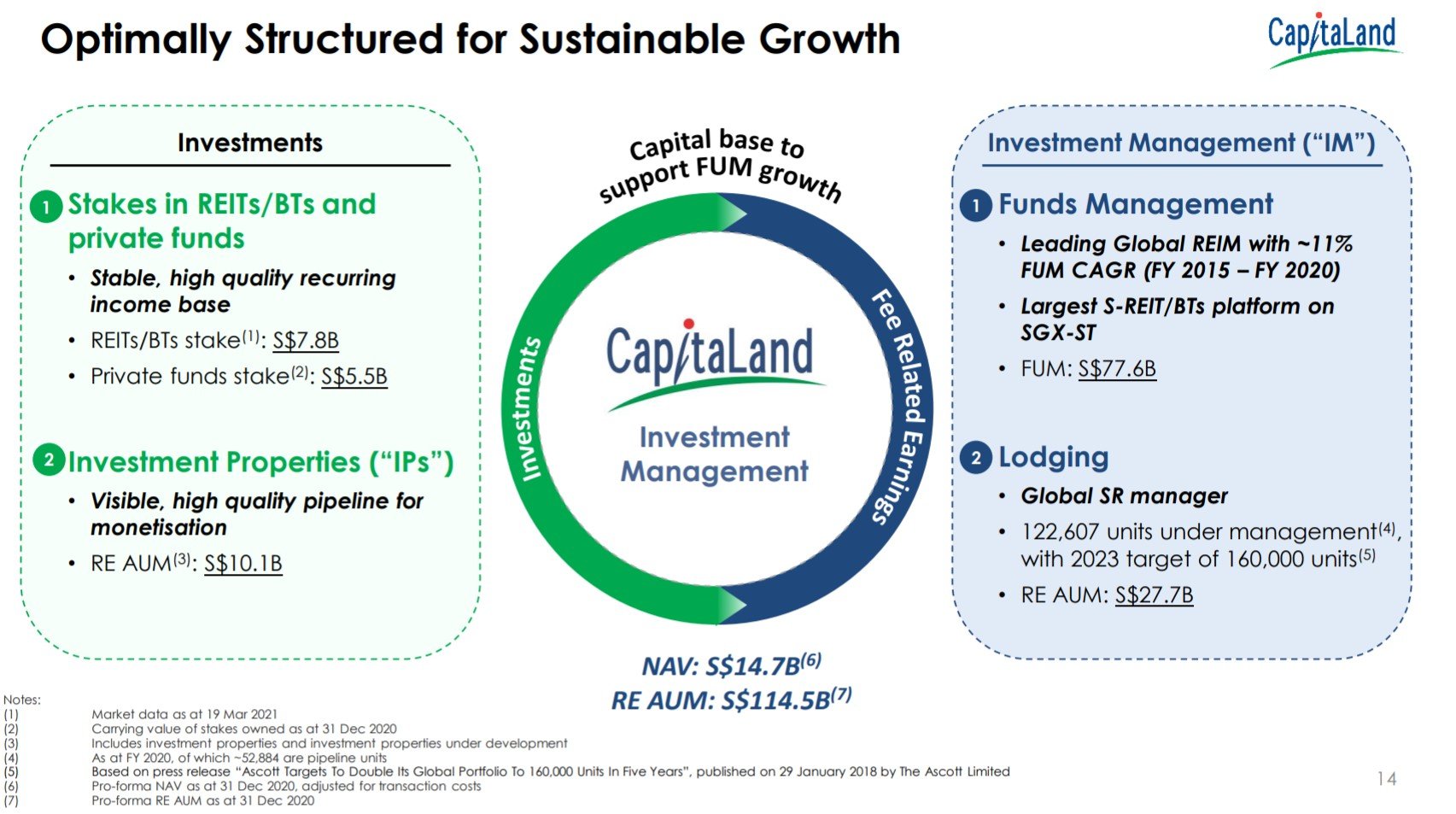

What does CapitaLand Investment hold?

What the new CapitaLand Investment holds is:

- The listed CapitaLand / Ascendas REITs:

- CapitaLand China Trust

- CapitaLand Integrated Commercial Trust

- CapitaLand Malaysia Mall Trust

- Ascott REIT

- Ascendas REIT

- Ascendas India Trust

- The unlisted private Funds (eg. the Raffles City Funds)

- The mature Investment Properties (eg. Jewel, Ion Orchard, Galaxis)

- The hospitality business (Ascott)

- The REIT Managers and Fund Managers

Let’s discuss each piece individually.

Sum of the Parts Analysis – CapitaLand Investment

Listed CapitaLand / Ascendas REITs

These are the existing stakes that CapitaLand Investment holds in the listed REITs.

The stakes are worth $6.1 billion on the open market today using latest prices as at 30 September:

Stakes are worth less because of inefficient tax holding structure?

Some of you may point out that CapitaLand holding the stakes is less valuable than retail investors holding them directly.

The reason why is because of tax treatment.

If CapitaLand holds the REITs, they pay corporate tax on the distribution profits. If you as an individual hold the REITs, you pay no tax on the distribution.

You can also argue that if CapitaLand decides to dump their stake on the open market, they’re never going to get the market price because it’s so dilutive.

I mean, just take a look at Keppel REIT’s share price recently.

Both are fair points.

So let’s be super conservative and apply a 15% discount to the stakes in the listed REITs.

That cuts it down to $5.185 billion.

The Unlisted Funds (eg. the Raffles City Funds)

The unlisted funds are a bit more tricky.

Back in March 2021, CapitaLand valued the private funds stake at $5.5 billion.

A big chunk of this is in China, so you can argue that the value has gone down because of Evergrande and the China slowdown.

Knowing how the institutionals value their properties though, I’ll probably bet my money that the valuations they are using for the funds are on the conservative side.

It’s the same reason why every time a REIT sells a property, they sell it at a big premium to the last valuation. It’s always easier to mark it up then down, so no fund manager wants to put too aggressive a valuation that he needs to mark it down in time.

So for this, I’m happy to take it at book value – $5.5 billion.

Mature Investment Properties

The mature investment properties held by CapitaLand Investment are set out above (Top 15).

Big names like ION Orchard, Raffles City Chongqing, CapitaSpring, Jewel, Galaxis etc.

The total value is $10.1 billion.

The problem though – is that we don’t know CapitaLand’s stake in them.

Looking at the list above, it probably averages to around 60% stake in the Top 15 properties, but we have no clue what the numbers look like outside the Top 15.

So I decided to be extra conservative here, and I assumed a 30% ownership of the Investment Properties, which is probably on the very low side.

Assuming 30% – this works out to $3.03 billion.

REIT + Funds + Investment Properties is 79% of CapitaLand’s Market Cap

If you add up the stakes of the (1) Listed REITs, (2) Private Funds, and (3) Investment Properties (assuming 30% stake), we get $13.7 billion.

That’s a whopping 79% of CapitaLand’s current market cap ($17.38b).

What makes up the remaining 21%, or $3.6 billion?

Remaining 14% or $3.6 billion?

It’s the stuff on the right hand side – the Hospitality Business (Ascott) and the Funds Management Business.

Hospitality Business (Ascott)

To be really honest – I don’t like the hospitality business.

I just think the better way to play hospitality is by owning the online travel platforms – the AirBnBs, Booking.com, Meituan etc.

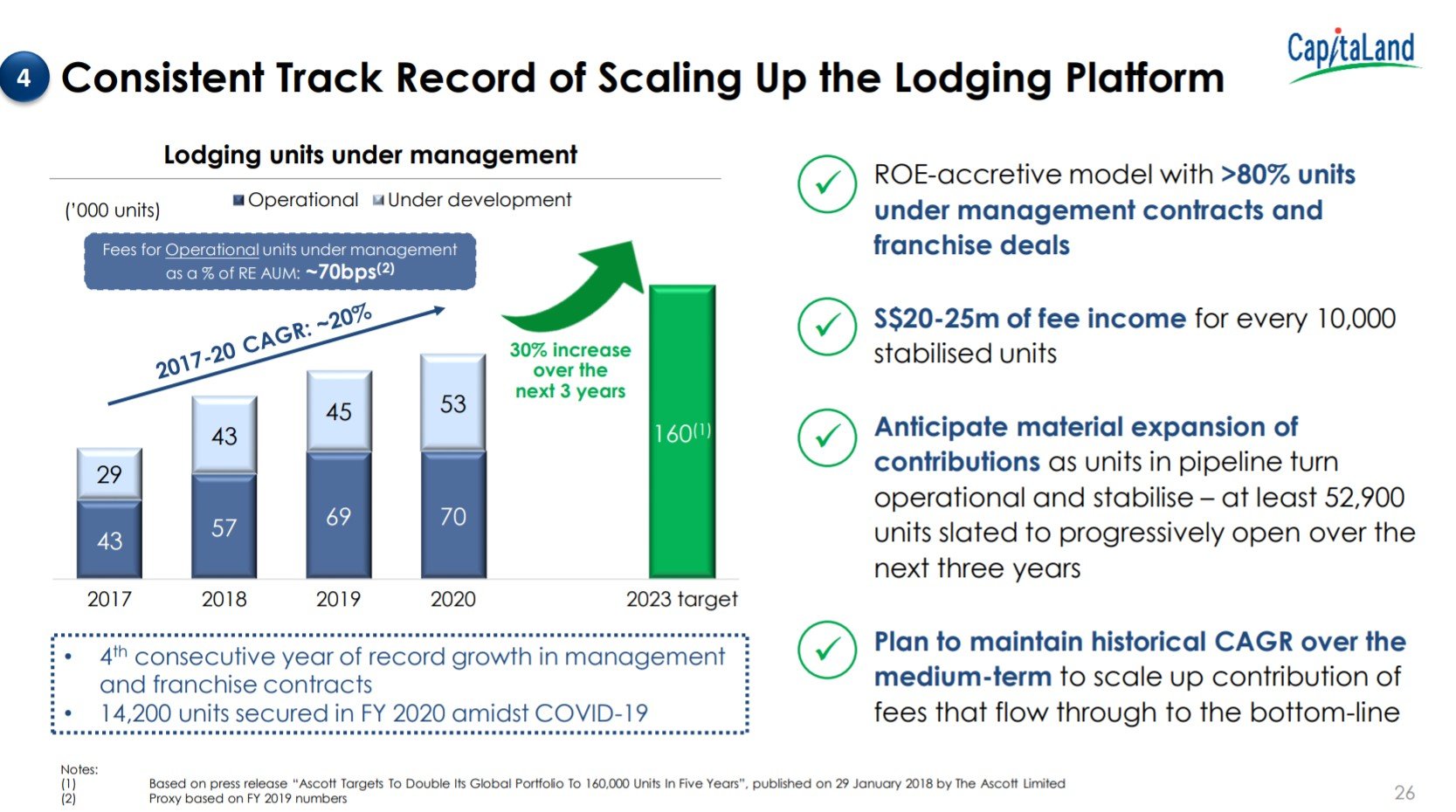

That said, the business does have 70,000 units today, and looking to grow to 160,000 by 2023.

At the very least, there has to be some value in the Ascott business.

REIT Manager / Fund Manager

This part of the business I really like though.

You know how every REIT pays a percentage based fee to the REIT manager to “manage” the REIT?

And each time the REIT buys a property they have to pay an “acquisition fee” to the REIT manager?

Yeah… CapitaLand Investment owns the REIT manager for all the Ascendas and CapitaLand REITs.

That’s just very solid, very stable income.

This business is a gold mine.

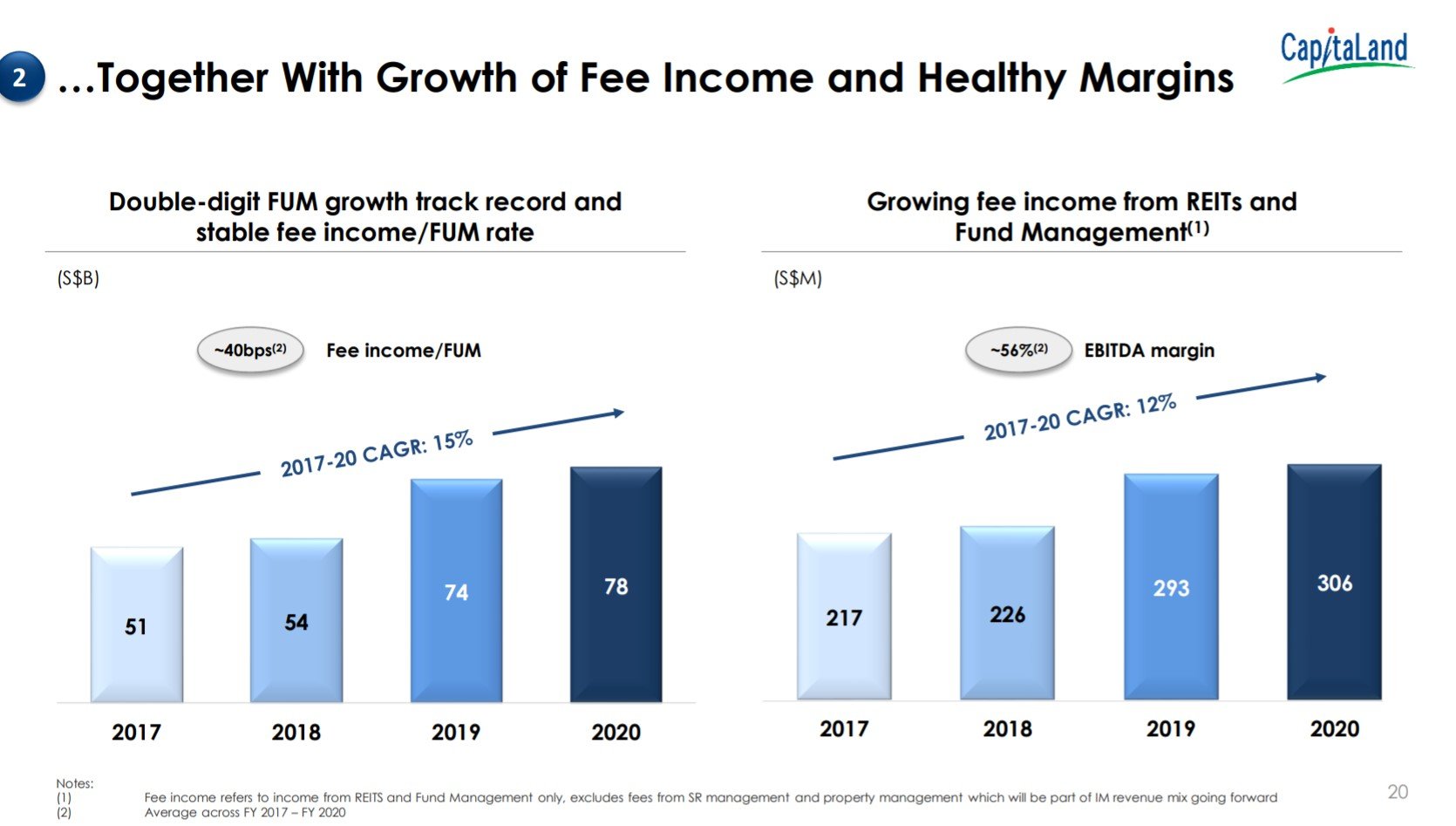

Most fund managers are valued at about 15 times earnings.

Let’s just be extra conservative and use 12 times earnings.

If we use the 2020 earnings of $306 million, this business alone is worth $3.6 billion.

So FH… You’re telling me I can get the Ascott business for free?

Using my numbers above – the Ascott + Fund Management Business is worth $3.6 billion.

If the Fund Manager business is worth $3.6 billion by itself, then you’re essentially getting the Ascott Business for free.

And like we discussed, there clearly is some value in this business.

This isn’t like SPH’s print media where they had to pay $100 million to get rid of it.

So yeah… I’m starting to get why the market likes CapitaLand Investment.

BTW – we share commentary on Singapore Investments every week, so do sign up for our mailing list.

Don’t forget to join our Telegram Channel and Instagram (or our Reddit Community)!

[mc4wp_form id=”173″]

CapitaLand Investment’s Book Value

I’m just going to cross check my numbers against the book value.

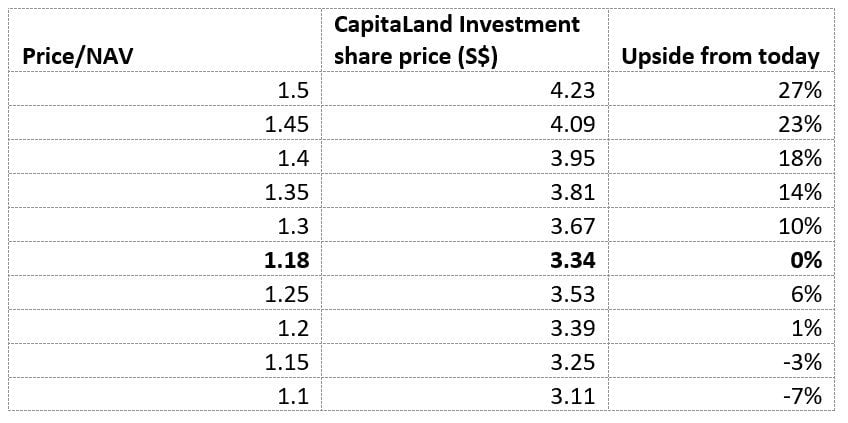

Official book value (NAV) for CapitaLand Investment is $2.823.

At current price of $3.34, that 1.18x book value.

What is the right multiple for CapitaLand Investment?

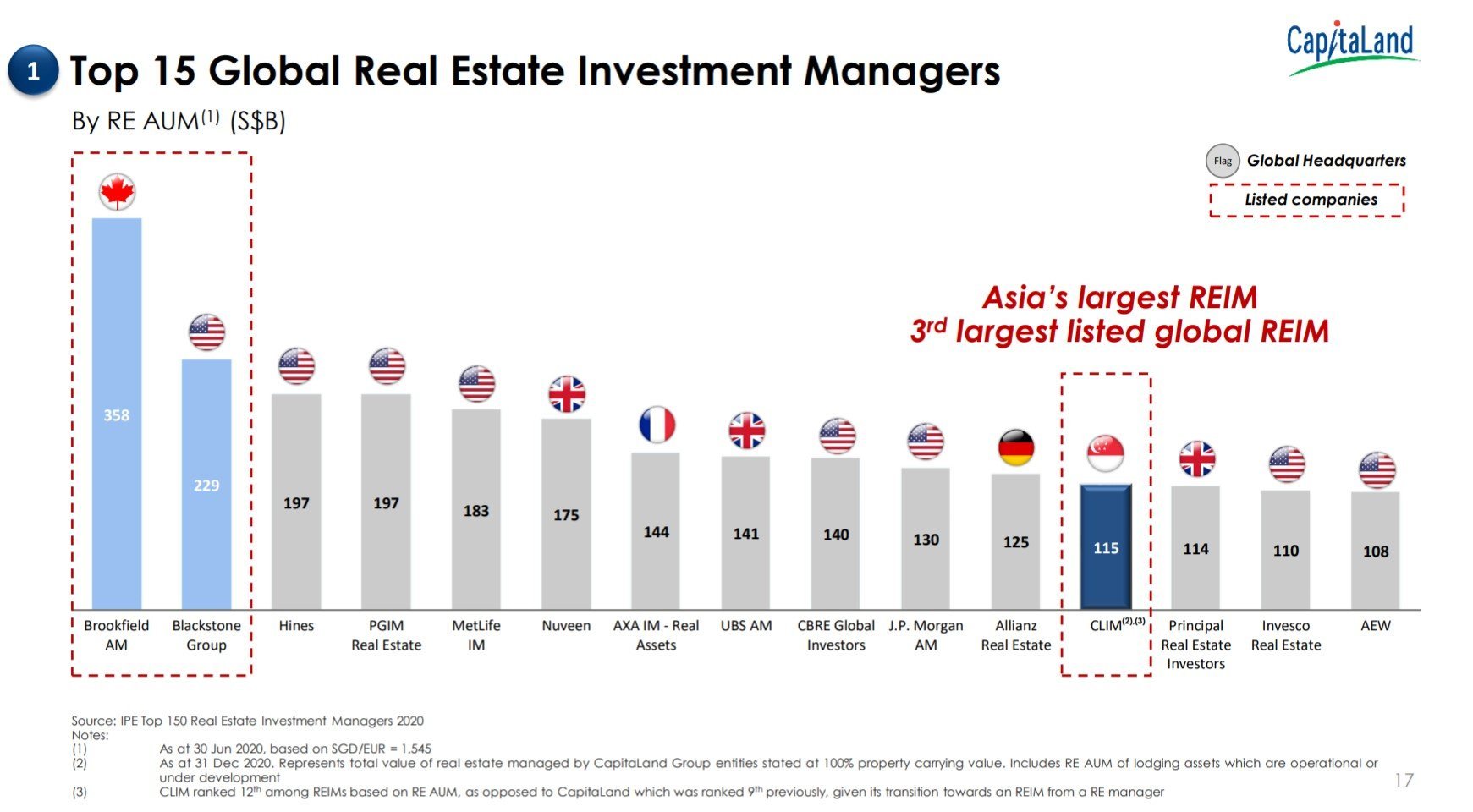

CapitaLand Investment is the 3rd largest listed real estate investment manager in the world.

To compare against the market leaders:

- Brookfield Asset Management – 2.43x Book Value, 30x Price/Earnings

- Blackstone – 9.16x Book Value, 18x Price/Earnings

Now for obvious reasons both Brookfield and Blackstone have much bigger fund management arms than CapitaLand, so the comparison is not apples to apples.

But it does give you an indication of how highly the market values the fund management business, that CapitaLand is trying to expand into.

CapitaLand is looking to grow the Fund Management business

Just look at the recent hires for an idea of the direction:

The first is Simon Treacy who is appointed as the CEO of the private equity real estate division and will be in charge of growing CLI’s private equity real estate business.

The other is Patrick Boocock who will take on the role of CEO of private equity alternative assets to grow the group’s unlisted asset portfolio.

Both men come with good credentials. Mr Treacy was the managing director, global chief investment officer and head of US equity for BlackRock’s (NYSE: BLK) real estate division, while Mr Boocock was previously the managing partner and head of Asia at Brookfield Asset Management (TSE: BAM.A).

It’s clear that CapitaLand wants to growth their fund management / private equity real estate business.

Translating the vision into execution is not easy, but current valuations are not demanding. So if CapitaLand can pull it off, there’s a fair bit of upside here.

Sensitivity testing of CapitaLand

To give you an idea of the upside (or downside)

Here’s how much you can make (or lose) if there is a rerating in the multiples:

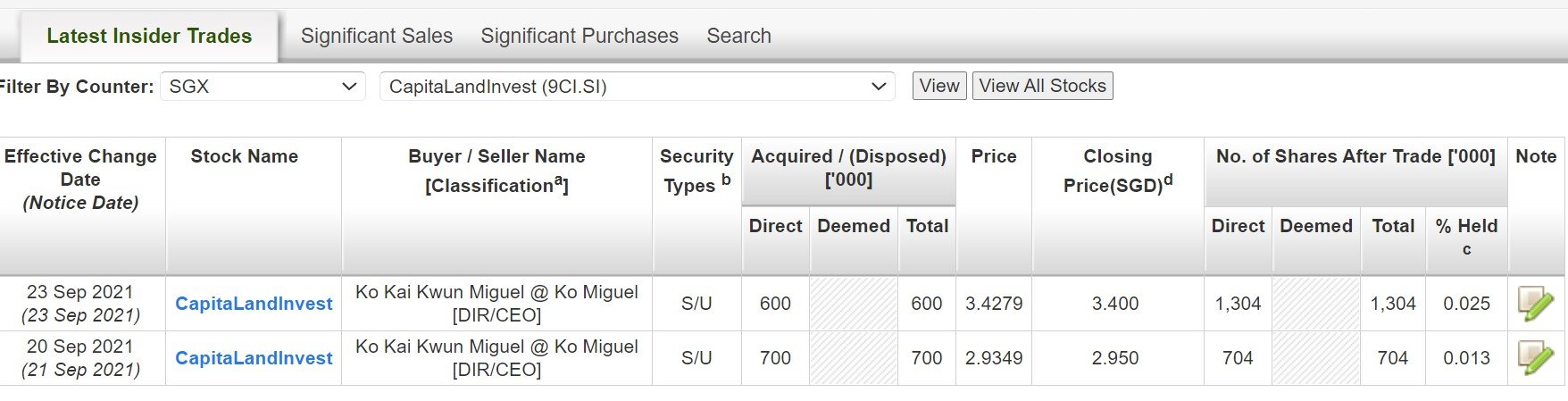

CapitaLand Investment chairman Ko snaps up $2 million worth of shares on trading debut day

Interestingly – the new Chairman Miguel Ko snapped up $4.06 million worth of CapitaLand Investment Shares after IPO.

Miguel Ko used to be Chairman of Ascendas Hospitality Fund Management and Ascendas Hospitality Trust Management, and before that Chairman and President of Asia Pacific Division at Starwood Hotels & Resorts, and Deputy Chairman and Chief Executive Officer at CDL Hotels International.

So he’s been in the real estate circles for a while, and the fact that he’s putting money where his mouth is is a very solid vote of confidence for the new CapitaLand Investment.

Technicals of CapitaLand Investment

The technical are surprisingly strong too – with the rally in late September coming on very strong volume.

Will I buy CapitaLand Investment $3.3?

Full Disclosure – I am vested in CapitaLand Investment.

I was a shareholder in the previous CapitaLand, so after the restructuring I continue to hold my stake.

And I actually really like this stock.

Using my very conservative numbers above – you’re essentially getting the entire Ascott Hospitality business for nothing.

Which means there is a very nice margin of safety priced into the stock.

My concern though is twofold – (1) China slowdown, and (2) Lack of longer term catalyst.

China Slowdown

CapitaLand Investment has an almost 40% exposure to China real estate.

With all that is going on with Evergrande, China real estate growth looks tricky.

I covered Evergrande in detail here and here, so I won’t belabour the point.

Long story short – my base case is for a broader slowdown in China real estate growth in the near term.

Which may weigh on CapitaLand Investment short term.

Lack of longer-term catalyst

All Singaporean retail investors know this feeling.

You buy into a Temasek company, full of hope and promise.

Valuations look good, long-term strategy is solid.

Then the stock goes nowhere… for 5 years.

The problem with the Singapore market is that sometimes… nothing happens.

A cheap stock can stay cheap for a long time, and without a catalyst, it just goes sideways.

My fear with CapitaLand is that longer term, investors may get bored with the stock, and then it just sits there doing nothing.

And all I would get is my dividend.

For now, the market reaction to CapitaLand Investment is very strong, so let’s hope this doesn’t happen.

Let’s cut to the chase FH, will you buy CapitaLand Investment $3.3?

Probably not today.

I already hold a position, and I don’t see an immediate need to add to the stock (Full Portfolio available on Patreon).

Short term, the macro does look very tricky.

Interest rates are going up, monetary policy is tightening, inflation pressures are picking up.

And with rate of growth slowing, and China Evergrande playing out, there’s quite a few headwinds for global markets right now.

The last few weeks have already shown some weakness in the market, and I do think there is a real possibility of a correction in the months to come.

So I do want to keep some powder dry during this period. FYI my full stock watch and portfolio are available on Patreon.

So simple answer – I like CapitaLand Investment, but I already have a position, and I don’t see a need to rush to add given the global macro.

That said, from a fundamental, valuations point of view, I really like CapitaLand Investment. Valuations are cheap, the real estate portfolio is solid, and the vision is sound.

This is a solid 4 Horse rating for me.

Love to hear what you think! Do you like the new CapitaLand Investment?

Financial Horse Rating – CapitaLand Investment

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a Free Apple stock (worth S$200) when you open a new account with Tiger Brokers and fund $2000.

Get 1 free Apple share (worth $200) you’re new to MooMoo and fund $2700.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for highly competitive FX and commissions.

Check out our review on Tiger Brokers and MooMoo.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide on the best buying platforms here.

As always, this article is written on 1 October 2021 and will not be updated going forward. Latest thoughts (and my stock watch and personal portfolio) are available on Patron.

Join our Reddit community at r/SingaporeInvestments.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Both are THE best quality investment courses available to Singapore investors out there!

Thanks for the nice analysis, FH! Do you know what the current dividend yield is? It matters because if it goes sideways for 5 years, this will determine if you are paid while waiting.

Problem is that we don’t know the true yield because they havent officially paid a dividend yet, nor did they announce the payout policy. Based on some rough numbers assuming a 40% payout ratio, it should be about 3%.

Ascendas Reit had completed acquisition for the remaining 75% stake in Galaxis from Capitaland on 30 June 2021 by the way????.

Do u think the P/B ratio will be at least 2x in the long term horizon (3 years) ?

Side note : I was planning to buy on the opening day 20th Sep 2021 but nvr do so because of China Evergrande news????.

You’re right, thanks for pointing this out!

2x looks quite aggressive haha, considering ~80% of it is real estate investment. Don’t think it’ll get that high unless they execute flawlessly on the FM Biz. More likely a low 1.x PB longer term, but with additional gains from growth of the underlying real estate prices?

Yup, agreed with what you said. Hopefully they are able to capital recycling on their investment pipelines worth 10.1bn to grow their FUM????and hopefully AUM also can????????.

They have confirmed the payout ratio is 30% of their earnings…I can see some issues with Mr Horse analysis up there….

Thanks for the heads up, might have missed that one.

Sure – let me know what issues there are and we can work to improve the analysis. 🙂

This is the only Sgx listed property stock that I will pass on to the next gen. ????

I saw some one wrote it’s worth $5+. Can remember the details.

I see current price/book value is 1.38 in SGX website, may I know why you got 1.18? Thanks.

It was from their most recently announced NAV of 2.8. I suppose this number could be out of date though, as per comments above they have sold Galaxis so the NAV may be adjusted down.