Introduction

I saw a question on the Seedly Facebook Group recently that really got me thinking:

“Hi everyone, I would like to find out which mode of investment stands a higher chance to make money? Robo advisor or conventional methods like financial advisor? I’m looking at 10% annually.”

Immediately, a couple of points jumped out at me. Firstly, the historical, multi-decade return for equities is about 7%. 10% is simply unachievable without taking outsized risks that opens you up to complete loss of your initial capital. Secondly, a person who can achieve a 10% return consistently should no longer be running a robo or be working as a financial advisor, he should be running Blackrock or Berkshire Hathaway.

Yet the question with Robo advisers stuck with me. Why do so many people think that a robo adviser can achieve a 10% return when even the best hedge fund managers struggle to hit 8% annualised returns? Was there something I was missing? I decided to take an in-depth look at these robo-advisers.

Given that Stashaway recently raised US$5.3 million Series A funding, I decided to start with them.

Important Note: For a more recent take comparing all Robo Advisors in Singapore, please go here.

StashAway Referral Link

If after this article you want to give StashAway a try, you might as well use this referral link that I got from StashAway’s CEO. You get 50% off your fees for the first SGD 50,000 invested for 6 months. That’s about S$94 saved on fees, so if you’re going to check out StashAway, you might as well just use this promo code.

StashAway Referral Link

Basics: StashAway / Robo-Advisers

StashAway is a Singapore based Robo-Adviser (the other big ones are AutoWealth and Smartly). How StashAway works can be summarised into the following:

- When signing up for an account, you answer a number of questions about your age, income, savings and investment profile.

- You then pick a savings goal, from the options below (eg. General investing or Plan for Retirement).

- StashAway will recommend an asset allocation for you. You can choose if you want a more aggressive or more conservative plan, but beyond that you can’t control the asset classes or allocation.

- Once satisfied, you transfer in a lump sum payment, and set up a monthly transfer. StashAway will convert all the SGD into USD, which it then uses to buy US ETFs.

- StashAway will do automatic rebalancing to ensure that you keep to the asset allocation.

- All dividends received are automatically reinvested in the allocation chosen for you.

- There is no lock-up period, you can exit at any time. Once you give them notice, they will sell all your holdings and return you the cash net of expense

What I dislike

Actually my number one gripe with StashAway is their asset allocation strategy.

StashAway has a very professionally done “White Paper” that details their strategy, and it has a number of really pretty charts. I was highly impressed at first, until I started thinking about the implications of this strategy.

StashAway touts their:

“Economic Regime-based Asset Allocation™. It’s our proprietary investment strategy that harnesses economic trends to maximise your returns at the risk level that feels right to you.”

It’s all nice and pretty, but to simplify their investment strategy massively, there are 2 investment techniques: Asset Allocation, and Re-optimisation.

1. Asset Allocation (Risk Parity Strategy)

Asset allocation is how StashAway determines the initial portfolio allocation. It’s an adaptation of the risk parity (without leverage) or all weather portfolio strategy, which is defined by Investopedia as

“Risk parity is a portfolio allocation strategy using risk to determine allocations across various components of an investment portfolio. The risk parity approach to portfolio management centers around efficient market theory to optimally diversify an investment portfolio among specified assets.”

The thinking is that certain asset classes such as stocks and bonds are negatively correlated. When stock prices go up, bond prices decline. When stock prices decline, bond prices go up in a flight to safety. By holding a portfolio of assets weighted by risk, this reduces volatility in the good times, and significantly cuts down on losses in the bad times. This is the core concept behind the typical 60-40 stock bond strategies that we always hear about.

I entered my personal details into StashAway and they recommended the following asset allocation (based on a 30 year old single male, approx. S$120,000 income)

Default Recommended

Portfolio Composition: 54.5% – Growth, 45.5% – Protective

Asset Allocation

| FIXED INCOME | TICKER | WEIGHT | |

| iShares 10-20 Year Treasury Bond ETF | TLH | 3.17% – 4.75% | |

| iShares 20+ Year Treasury Bond ETF | TLT | 9.50% – 14.26% | |

| iShares TIPS Bond ETF | TIP | 11.88% – 17.82% | |

| Vanguard Intermediate-Term Government Bond ETF | VGIT | 10.30% – 15.44% |

| US EQUITIES | TICKER | WEIGHT | |

| Consumer Discretionary Select Sector SPDR Fund | XLY | 11.88% – 17.82% | |

| Consumer Staples Select Sector SPDR Fund | XLP | 3.17% – 4.75% |

| CASH | TICKER | WEIGHT | |

| Cash | SGD | 0.80% – 1.20% |

| HYBRID | TICKER | WEIGHT | |

| SPDR Bloomberg Barclays Convertible Securities ETF | CWB | 11.88% – 17.82% |

| COMMODITIES | TICKER | WEIGHT | |

| SPDR Gold Trust | GLD | 7.52% – 11.28% |

| EUROPEAN EQUITIES | TICKER | WEIGHT | |

| SPDR Euro STOXX 50 ETF | FEZ | 2.54% – 3.80% |

| ASIA EX JAPAN EQUITIES | TICKER | WEIGHT | |

| iShares MSCI All Country Asia ex Japan ETF | AAXJ | 7.37% – 11.05% |

My problem with this risk parity strategy is the outsized allocation to bonds. For my profile, StashAway chose a 40+ % allocation to US Bonds, and 60% global equities, commodities and convertible securities. Even the most aggressive plan I was able to select (by dialling everything up to maximum, and confirming I acknowledge the risks) has a 23% allocation to bonds. This is the case regardless of what plan you pick, and what profile you enter. A significant portion of your portfolio always goes into US Bonds.

The problem with this massive allocation to US Bonds is that:

Witholding Tax

All dividends/income is subject to a 30% withholding tax, which is just crazy. Why would I pay 30% tax on all my income to the US Government when I can just invest in Singapore bonds? It is crazy enough that I will discuss this in further detail later.

30 year bond bull market

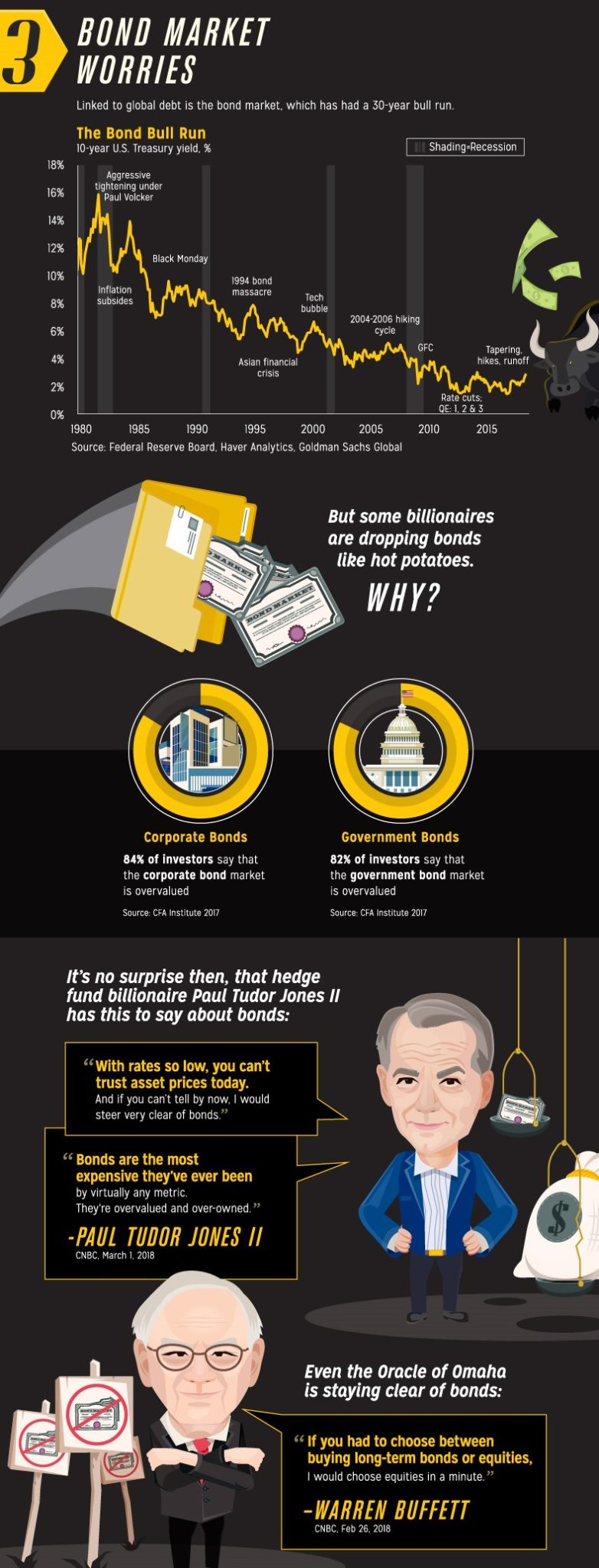

At this point in the economic cycle, I am highly worried about the future of bonds. Visual Capitalist has an amazing infographic on this below, which can be summed up as follows. Bonds have been in a 30 year bull market (note this is not like stocks, which are only in a 10 year bull market). Interest rates have been falling systematically from 12% in 1980 to about 2% today, and it is negative in some countries around the world such as Europe/Japan. For bond prices to go up, yields have to drop. When yields are 2% to negative, there is nowhere for yields to go but up, which results in massive falls in bond prices.

There are also some great quotes from Paul Tudor and Warren Buffet on how overvalued bond prices are, on a historical basis.

CPF

The whole idea of a 40% allocation to bonds, under a portfolio allocation theory, is to smooth out your returns in a down cycle. This theory was written by ang-mohs, who do not have a mandatory CPF contribution. My own take is that Singaporeans have a huge amount of money stashed away in CPF (OA, SA, SRS and Medisave). These are government guaranteed, risk-free investments at a 2.5% plus interest rate, which coincidentally is about the same returns on the US Bonds that StashAway would put my money into.

For Singaporeans, our CPF can serve as a pseudo-bond portfolio, which means that in my investments, I should be going mostly equities and high yield products such as REITs to maximise returns. By allocating a significant chunk of my investible assets into bonds, I am inadvertently taking an overly conservative position.

2. “Reoptimisation”

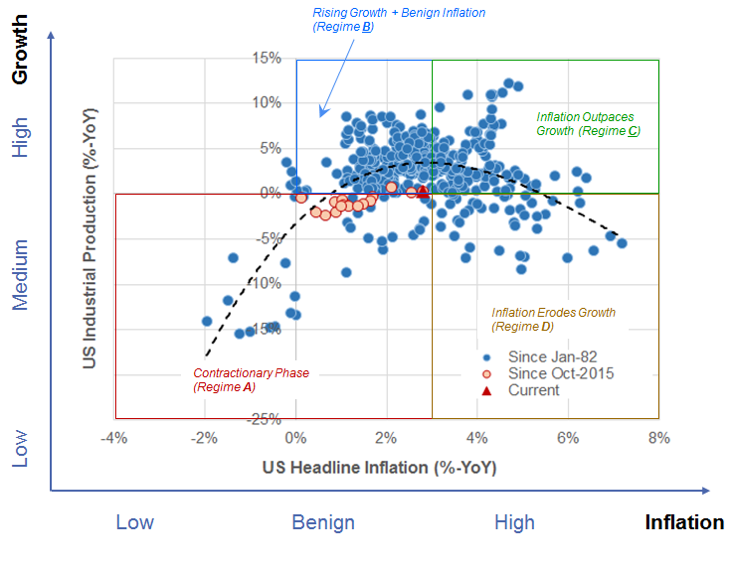

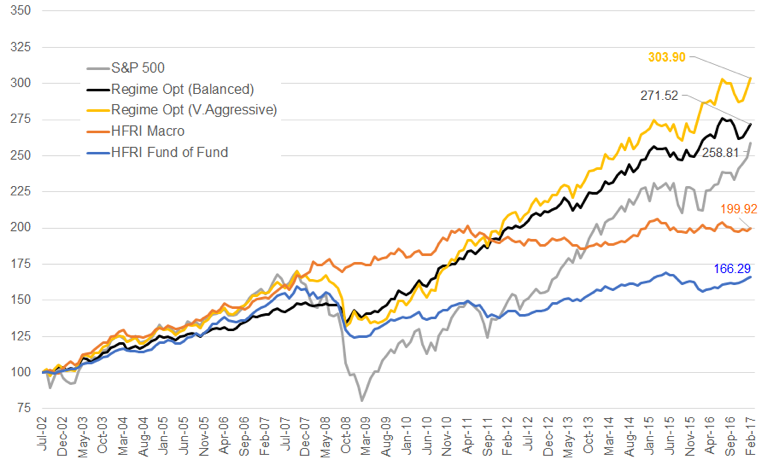

Re-optimisation is where it gets even dicier. StashAway claims that they can split all economic regimes into 4 broad categories as set out below. Based on the economic regime we are currently in (which they determine by looking at economic fundamentals), they will adjust your asset allocation accordingly.

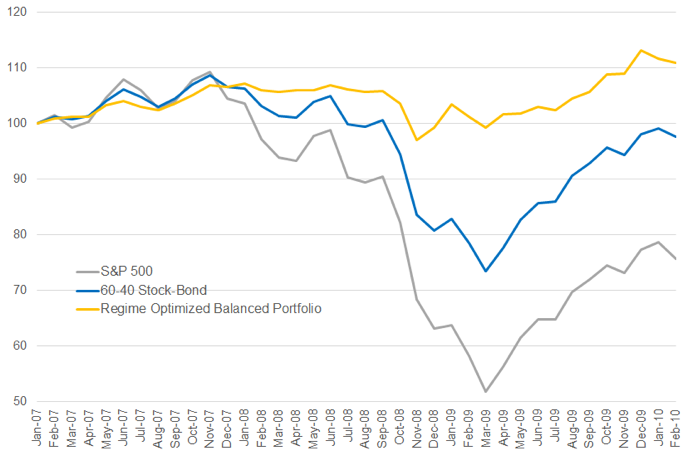

The claim is that by doing so, they can significantly reduce the downside in a financial crisis. Now, Financial Horse is a sceptical horse by nature, so when I see charts like the below, I almost never believe them unless I can test them myself. A number of issues jump out at me.

Proprietary Technique prevents independent backtesting

Firstly, StashAway’s investment technique is proprietary software that is not released to us. We have zero information as to how they decide which economic regime we are in, and how they will adjust asset allocation accordingly. Without this information, there is no way to independently verify their claims, or to question the assumptions made.

History never repeats itself

Given that StashAway has had the time to study all the economic fundamentals leading up to the previous Financial Crisis, they could have well designed a model that would effectively identify the financial crisis and pre-empt it. Accordingly, if the Financial Crisis were to repeat, the StashAway technique would truly outperform the index. The problem then, is that History never repeats itself. Each financial crisis is unique, and set off by different triggers. What techniques worked to allow StashAway to pre-empt the previous financial crisis may not necessarily work in the next financial crisis.

Holy Grail

A lot of really smart hedge fund managers and professors have spent their careers trying to minimise downside in a financial crisis, yet they almost always suffer massive losses when the crisis does materialise. The market is devilishly complex, and when too many people adopt similar strategies, it actually neturalises the effectiveness of the strategy. Has StashAway discovered the Holy Grail here? Perhaps.

What are they doing with my money?

Which leads me to another concern. I am investing in a robo-adviser because I do not trust hedge funds and their active management, which more often than not results in underperformance versus an index. Why is StashAway implementing this “proprietary” automatic re-optimisation of my portfolio, that can tweak it beyond my original asset allocation? And why do I have zero information on what goes into this re-optimisation?

It feels a lot like a pseudo active management. And unfortunately without knowing what goes into their model, I really cannot comment on how effective it would be. To put my money in StashAway would require an implicit belief that their proprietary model will outperform.

3. Withholding Tax

As mentioned above, all dividends and bond payments are subject to a 30% withholding tax. StashAway knows this as well, as stated on their FAQs:

Do my dividends get taxed?

All dividends of US-listed securities are subject to 30% dividend withholding tax and the QII (Qualified Interest Income) rule. The latter rule applies to US domiciled funds, especially US government bonds, of which some of the dividend withholding taxes can be claimed back. Our broker will do this on your behalf.

This is absolutely ridiculous. Why would I pay 30% withholding tax on all US bond payments, when I can just invest in an equivalent Singapore/Asian bond portfolio and keep the extra 30% to myself? In my personal Financial Horse portfolio, I use US equities purely for growth stocks (foreign investors are exempt from capital gains tax), and for dividend or income plays, I stick purely to Singapore stocks / REITs.

By using US bonds, you are exposing yourself to massive US tax liability, which is tax-inefficient. If you really had to do a 60-40 equity bond allocation, you could always consider using a Singapore/Asian bond ETF as a replacement.

Update: I wrote a recent article that explains how US withholding tax works. Do check it out if you need more info on this topic.

4. Fees

Over multi-decade periods, any amount of fees really adds up. Don’t forget, StashAway invests in US ETF, so not only do you pay the management fee for the ETF, you also pay StashAway’s fees.

StashAway’s fees are set out below.

Our pricing structure

| Total Investment (SGD) | Annual Fee Rate (Incl. GST) |

| First $25,000 | 0.8% |

| Any additional amount above $25,000, up to $50,000 | 0.7% |

| Any additional amount above $50,000, up to $100,000 | 0.6% |

| Any additional amount above $100,000, up to $250,000 | 0.5% |

| Any additional amount above $250,000, up to $500,000 | 0.4% |

| Any additional amount above $500,000, up to $1,000,000 | 0.3% |

| Any additional amount above $1,000,000 | 0.2% |

On a hypothetical S$100,000 portfolio, this works out to be 0.675%, or 675 dollars a year. It may seem miniscule, but any amount of fees really affects the power of compounding. As a rough illustration, assuming a 6% annualised return on your S$100,000 portfolio, the effect of a 0.675% fees is S$10,00 after 10 years and S$100,000 after 30 years. After 50 years, a 0.675% fee is the difference between a S$1.3 million portfolio and a S$1.8 million portfolio.

| Returns | At 6% returns a year | At 6% returns a year, with 0.675% fees |

| After 10 years | S$179,084 | S$168,081 |

| After 20 years | S$320,713 | S$282,515 |

| After 30 years | S$574,349 | S$474,856 |

| After 40 years | S$1,028,571 | S$798,147 |

| After 50 years | S$1,842,015 | S$1,341,541 |

Note: I understand this calculation is a bit simplistic because as the portfolio size grows, the annual fees drop. However, this does provide a rough gauge on the impact that a small amount of fees can have on the power of compounding.

5. What if they change their business model?

As a young investor, my investment timeframe is 30 to 40 years. That’s a really long period of time, and a lot of things can change in the interim. Is it a stretch to wonder if StashAway would still be around after 40 years, or if their business model, or their management will change?

Over such extended periods, it’s not impossible to think of a situation where StashAway changes their fee structure, or their redemption mechanics, or their investment strategy, or perhaps even close down. When you are investing your money with someone else, there is always an element of uncertainty.

It’s not a huge risk, but a point to note nonetheless.

What I liked

Given the lengthy exposition above, you would have thought that I hate this robo-adviser. But I don’t. There’s a lot to like about it. In Part II of this article, I will set out what I liked about StashAway, and my Financial Horse rating.

Read Part II.

Enjoyed this article? Like our Facebook Page for more great articles!

Financial Horse has a set of 7 Commandments for Successful Investing, that I ask myself before making every investment, and that I will never break regardless of the situation. I share this with all my email subscribers at absolutely no cost. Sign up for the newsletter now!

[mc4wp_form id=”173″]

Hi Financial Horse, would like to point out that the auto re-optimization option offered by stashaway can actually be disabled

Interesting. If so then actually the difference between StashAway and AutoWealth will come down purely to asset allocation and insolvency risk. This puts them a lot closer, and I would think picking between the two will come down ultimately to personal preference.

Have you consider a review on Smartly ?

Yes, I would definitely consider doing an article if there was something new that I had missed. However I did feel that my previous articles on Robo advisers should have covered most of the issues on this topic. Did I miss anything? Let me know and I would be happy to do a revised post.

Recently, CIMB and UOB has introduced also RoboAdvisor, unsure if the strategy that implements are favourable. Not sure if you could have a review, i’m about to start applying StashAway until i read your post. Hmm..Looking for alternative again, look forward your recommendation (hope the referral commission will not put up any bias). Thanks.

Hi Win, welcome to Financial Horse!

Thanks for pointing this out, I am actually in the process of researching for a new article to compare the existing robos with OCBC’s new robo invest. I’ll include CIMB and UOB in this analysis as well. Targetting to get it out in the next few week. 🙂

Hi, looking forward to your article on OCBC’s roboinvest!

I’m hoping to have one out by this weekend!

[…] view on robo-advisor and StashAway, I recommend checking out this comprehensive review by Financial Horse and […]

Hi Financial Horse, if you switch off the auto-optimisation, then how should the asset allocation be? Isnt auto optimisation a good thing?

It’s hard to say without knowing exactly how their auto optimisation works. If they get it right, then absolutely its a good thing. If not, it could do more harm than good. 🙂

[…] too seduced by sexy words like “algorithm” or “re-optimisation” though. I’ve come across critics of Stashaway’s investment methodology on the internet, so I’d take it all with a pinch of […]

hi..does not investing in us domiciled etfs attract us estate tax of 40 percent

Yes, that’s correct.