One thing that I realised from the [Ask FH] series was that a lot of Singaporeans wanted to invest, but they weren’t sure the best way to go about doing it. Even for myself, the sheer number of investment choices on the market these days is overwhelming. Do you go with something from your pushy insurance friend, do you go with a robo-advisor, or do you get a unit trust? Which one will have the best returns going forward? And if you weren’t sure of your decision, there’s always the risk that when it underperforms, you’ll think of exiting the investment and switching to a shinier new product (and incur transaction costs).

In this article, I’m going to set out an “All Weather” investment portfolio for Singaporeans that is designed to perform well in all economic situations.

Basics: All Weather Portfolio

The “All Weather” Portfolio was first pioneered by Ray Dalio, founder of Bridgewater Associates. He did an interview with Tony Robbins where he explained how the all weather portfolio works and it’s very well done, so I’ve extracted it here:

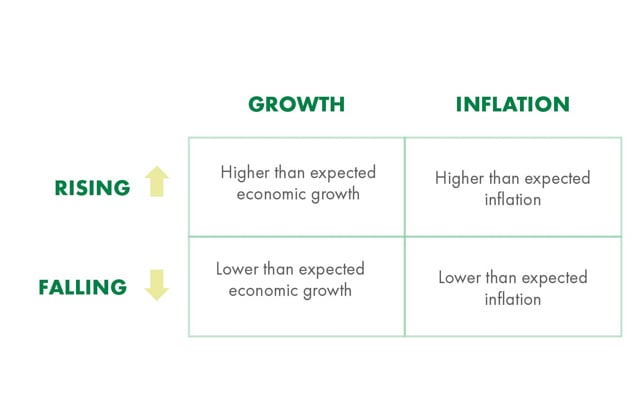

According to Dalio, there are only four things that move the price of assets:

1. Inflation

2. Deflation

3. Rising economic growth

4. Declining economic growth

And, there are only four different possible environments, or economic seasons, that will ultimately affect whether investments (asset prices) go up or down. (Unlike nature, however, there is not a predetermined order in which the seasons will arrive.)

These seasons are:

1. Higher than expected inflation (rising prices)

2. Lower than expected inflation (or deflation)

3. Higher than expected economic growth

4. Lower than expected economic growth

Because there are only four potential economic environments or seasons, Dalio says you should have 25% of your risk in each of these four categories – not 25% of your wealth in each category. That’s why he calls this approach All Weather: because there are four possible seasons in the financial world, and nobody really knows which season will come next. With this approach, each season, each quadrant, is covered all the time, so you’re always protected.

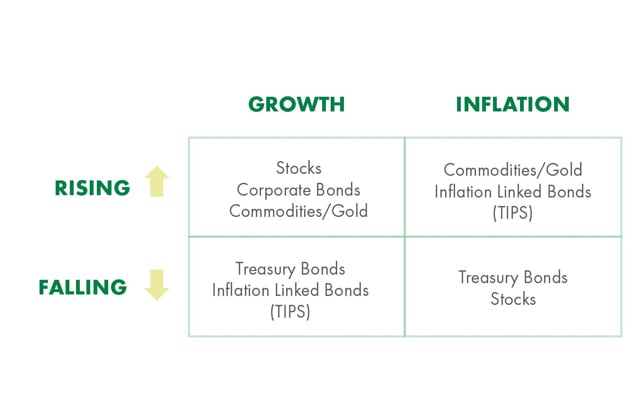

This chart breaks down which type of investment will perform well in each of these environments.

While it is invaluable to understand the principles behind Ray’s asset allocation, the challenge for investors is how to take these principles and translated them into an actual portfolio. Therefore, Robbins convinced Dalio to share a simplified version of his All Weather strategy. A strategy that the average person can execute, without any leverage, to get the best returns with the least amount of risk. It’s called the All Seasons strategy.

Why would Dalio give away the secret to his “secret sauce”? The last time Dalio would take you on as an investor you had to have $5 billion in investable assets and your initial investment needed to be a minimum of $100 million – but here he is, generously willing to help out the average investor.

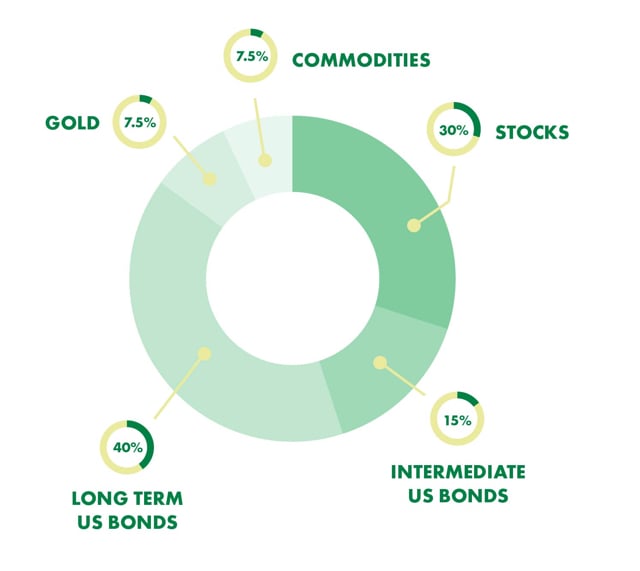

Behold the All Seasons strategy:

First, Dalio says, we need 30% in stocks — for instance, the S&P 500 or other indexes, for further diversification in this basket.

Then, you need long-term government bonds. Dalio recommends 15% in immediate term (seven- to ten-year Treasuries) and 40% in long-term bonds (20- to 25-year Treasuries). This counters the volatility of the stocks.

Finally, Dalio rounded out the portfolio with 7.5% in gold and 7.5% in commodities. As he notes, “You need to have a piece of that portfolio that will do well with accelerated inflation, so you would want a percentage in gold and commodities. These have high volatility. Because there are environments where rapid inflation can hurt both stocks and bonds.”

Lastly, don’t forget to rebalance. Meaning, when one segment does well, you must sell a portion and reallocate back to the original allocation. This should be done at least annually, and – if done properly – it can actually increase the tax efficiency.

That’s all there is to it. For the 30 year period from 1984 to 2013, this portfolio returned 9.7% annual returns, against 7.2% annual returns for a 35/65 stock/bond portfolio (47% in long-term treasuries, 18% in 10 year treasuries and 35% in the S&P 500).

All-weather portfolio (Singapore version)

| Asset class | Portfolio allocation | Singapore equivalent |

| Stocks | 30% | Stocks/REITs |

| Intermediate US Bonds | 15% | CPF Ordinary Account, Singapore Savings Bonds, US Treasuries 7 to 10 years (IEF) |

| Long Term US Bonds | 40% | CPF Special Account, Singapore Government Securities, Bond ETFs, US Treasuries 20 Year + (TLT) |

| Gold | 7.5% | Gold (GLD) |

| Commodities | 7.5% | Commodities (DBC) |

I’ve set out the Singapore equivalents above. Let’s go through them individually.

Stocks (30%)

Stocks will be Stocks or REITs. The key question here is whether to stick to Singapore stocks only, or diversify globally. I know a lot of investors are not comfortable investing in overseas stocks because they feel they don’t understand those markets, or because of forex risk. That’s actually okay, but you must be aware of the home bias, and the lack of diversification in your portfolio. Singapore stocks have done well the past 30 years because Singapore as a country has done well. If that continues in the next 30 years, your stocks will probably do well. If it doesn’t, you might be in trouble because your CPF, your employment, your house, and your savings are all denominated in SGD. It works if you’re a country as big as the US (and has reserve currency status) or China (deep domestic market, capital controls make it hard to move money out), but when you’re a small country like Singapore, and investing in the US market is as simple as opening a Saxo account and buying the S&P500, I really don’t see a reason why you shouldn’t diversify.

My proposed mix for the stock component is:

- 10% US stocks (via the S&P500, you can mix in the NASDAQ for higher risk-reward);

- 5% China exposure (via the Hang Seng Index);

- 7.5% Singapore Stocks (STI ETF, Philips Sing Income ETF, or stock pick); and

- 7.5% Singapore REITs (REIT ETF, but my preference is to pick).

If you’re absolutely not comfortable with foreign exposure, you can do 20% Singapore Stocks, and 10% Singapore REITs (REIT exposure as a percentage of the portfolio should not be too high for diversification purposes).

Noted: I had a query from a reader on why I didn’t include Europe/Japan/EM exposure, that I felt warranted an explanation. Please see my full response below:

For example, in the stock component, I didn’t include Europe/Japan/EM because I’m quite wary of their growth going forward. But if you are bullish on them, you can swap out some US/Singapore exposure, and replace it with Europe/Japan/EM. Asset allocation is by far the most important consideration for a retail investor, so as long as you keep to the asset allocation in the all weather portfolio (ie. The allocation between bonds (intermediate and long term bonds), stocks, gold etc), you should be generally okay.

That said, I’ll touch briefly on why I’m not a fan of Europe/Japan/EM:

- Europe – Europe no longer has the secular tailwinds it had during the 19th century. There was a time when Europe was the premier superpower in the world (almost all superpowers in the past 500 years save the US came from Europe). That time is long gone. Since 2012, the ECB has kept interest rates in the negative territory, and has been buying copious amounts of corporate debt. All that is going to end in 2019, and with the state of the European economy, I’m not confident their corporations can survive without this central bank life support. They’re also going through a period of political uncertainty (Brexit, Macron, and Merkel’s leaving will create a power vacuum in Germany), the Italian banking system is still on the verge of falling apart (this time there’s no Merkel to hold everything together), and chronic youth unemployment. None of this makes me bullish on the European economy, especially when compared to the US or China.

- Japan – Japan faces a lot of the problems that Europe does. Interest rates have been kept artificially low for almost 2 decades. This has given the Japanese economy a zombie-like feel, as large conglomerates are kept alive through cheap borrowings. They’ve been in and out of recessions over the past 10 years, simply because there hasn’t been that kind of “reset” of the debt cycle, where you allow the existing companies to burn and new ones to rise from the ashes. Couple that with an aging population, and huge competition from China, and you’ve got a horrible situation. Japan will never quite go away, they’re the third largest economy in the world, but the growth prospects here are not attractive, at least to me.

- Emerging Markets – Emerging Markets are too big of a category to discuss generally, because they include everything from Brazil to Argentina to Vietnam. I wasn’t bullish on EM in 2018 because the US Federal Reserve was on an aggressive rate hike cycle, which would have pressured these EM countries who borrowed heavily in US debt, and pressured their currencies as foreign investors withdrew investments (forcing them to raise interest rates to defend the currency, slowing the domestic economy). In 2019, it looks like the Federal Reserve is going to be a lot more cautious on raising rates, so EM may have a less horrible year. Unfortunately, I don’t think this EM crisis has played out fully yet, there hasn’t been that kind of bloodbath in the forex markets and an investor run in sentiment that would characterize the end of the deleveraging process.

That said, if you are bullish on either of the 3, you can always get exposure via a total stock market ETF. My approach is a more tactical one where I make certain allocation decisions based on my macro outlook. This can pay off if I’m right, but when you diversify, you lose less if you’re wrong.

Intermediate US Bonds (15%)

The tricky thing about US bonds, is the impact of withholding tax.

To illustrate – the distribution yield of IEF, a US ETF that holds intermediate term US treasuries (7 to 10 years) is 3.08%. After 30% withholding tax, that drops to 2.15%, in which case you get a better yield from a Singapore Savings bond or CPF Ordinary Account. But at the same time, US Treasuries are the deepest sovereign bond market in the world in terms of depth and liquidity, and the USD’s status as the world’s reserve currency for the foreseeable future means that it’s hard to stay away from US treasuries in an all-weather portfolio for Singaporeans. In time to come, the onshore yuan bond market may come to rival the US treasury market if the US keeps on its path of binge borrowing, but we’re not there yet. So the key is to find a balance.

| Intermediate US Bond (IEF – tracks 7 to 10 y ear UST) | CPF Ordinary Account | Singapore Savings Bond | |

| Effective yield | 2.15% | 2.5% (3.5% for first S$20,000) | 2.57% for a 10 year maturity |

| Currency | USD | SGD | SGD |

| Liquidity | Deep liquidity | Limited, only able to take out for certain situations (buying a home etc) | Not freely traded, but can be redeemed any time with pro-rata interest |

| Inverse relationship with stocks (ie. goes up with stocks fall) | Yes | No | No |

I’ve set out the unique characteristics of each asset class above, and as you can see, each has its own pros and cons. For the all weather portfolio for Singaporeans, I would propose to use purely CPF OA or Singapore Savings Bonds to form this 15%, and get exposure to US Treasuries via the long term bond component. However if you do want that UST exposure here, you can always mix it up with an Intermediate US Bond fund like the IEF, that’s absolutely fine. It’s a lower effective yield, but you get the USD exposure, and that very important capital appreciation in a financial crisis.

Long Term US Bonds (40%)

| Long Term US Treasury (TLT – tracks 20 year bonds) | CPF Special Account | Singapore Government Securities (20 year) | Bond ETF (ABF Singapore Bond Index Fund) | |

| Effective yield | 2.345% | 4.0% (5.0% for first S$60,000 in CPF) | 2.73% | 2.68% |

| Currency | USD | SGD | SGD | SGD |

| Liquidity | Deep liquidity | Unlocks only at 55 years of age. | Freely traded, but liquidity is thin | Freely traded, but liquidity is thin |

| Inverse relationship with stocks (ie. goes up with stocks fall) | Yes | No | Yes, but market is inefficient due to lack of liquidity | Yes, but market is inefficient due to lack of liquidity |

As you can see, the best bang for your buck here is CPF Special Account because of the highest yield, but it’s very tricky to use this because of the illusion of liquidity in your portfolio. You may think that you have S$100,000 in your investment portfolio, only to find in a crisis that S$20,000 of that is locked up in CPF SA and can only be unlocked at 55.

I would suggest that you count CPF SA in this component for accuracy, but limit it to no more than 10% of your portfolio. For the remaining 30%, I would suggest an even split between Singapore and US bonds. The 15% for the US part is straightforward, just buy the TLT which tracks 20 year + US treasuries.

The Singapore part is less straightforward, as it will have to be a mix of Singapore Savings bonds, Singapore government securities, Bond ETFs (eg. ABF Singapore Bond Index Fund), or whatever new long dated Temasek bond that is released and that you can get your hands on. I get that using Singapore Savings Bonds here is not ideal, but the SGD retail bond market is heavily limited in terms of options, so we’re forced to scrounge around. If you’re truly maxed out on SSB allocation, and don’t want to use SGS or Bond ETFs due to lack of liquidity, allocating more to the TLT is not a bad thing too.

You can also consider topping up your CPF SA if you’re confident that you don’t need the liquidity in the near term, because the extra yield there is very attractive.

Gold (7.5%)

I know I wrote a long article about why I don’t like gold, but we’re talking about an all weather portfolio for Singaporeans here. There are certain economic situations where massive inflation causes both stocks and bonds to fall in real value (think Venezuela or Turkey), and in such a situation, you need exposure to an asset class that has universal value. And there’s no better asset class than gold.

There are many ways to get exposure to gold, if you have a ton of gold jewellery at home you can actually just add that up and use it to form this 7.5% if you’re prepared to sell them in a crash. Otherwise, gold can be easily played via a gold ETF (GLD) or a gold savings account from any of the local bank. Check out my original gold article for more info.

Commodities (7.5%)

Commodities is included for the same reason as gold above, but for diversification (to avoid having too much money in one metal). For commodities, the easiest way is to play it via a broad, diversified ETF such as Invesco DB Commodity Index Tracking Fund (DBC), which tracks an index of 14 commodities, and has deep liquidity and AUM.

To sum up, this is what a sample all weather portfolio for Singaporeans will look like:

| Asset class | Portfolio allocation (Ray Dalio’s US version) | Financial Horse All Weather Portfolio for Singaporeans |

| Stocks | 30% | 10% S&P500, 5% Hang Seng Index, 7.5% STI, 7.5% REITs |

| Intermediate US Bonds | 15% | 15% CPF OA |

| Long Term US Bonds | 40% | 10% CPF SA, 15% Treasuries (TLT), 15% Singapore Savings Bonds |

| Gold | 7.5% | Gold (GLD) |

| Commodities | 7.5% | Commodities (DBC) |

How to use an all-weather portfolio?

- Exclude your real estate, emergency buffer.

When you’re counting your investible assets to allocate into the all-weather portfolio, don’t count your primary residence, and don’t count your emergency buffer. This is important because both should not be viewed as investment assets, they’re there to make sure you can get through your day to day life.

- Rebalance annually

The key to the all-weather portfolio is that it is designed to perform well in all economic situations. The only thing you need to do, is to rebalance. Once a year, relook at your portfolio to see if the allocation is in line with the table above, and sell/buy to keep it in line. This is to ensure that no one portion of the portfolio gets too large, distorting your risk allocation.

- Understand the value of CPF

Because almost 25% of this portfolio is in CPF, it is important to understand how CPF works, and when you can withdraw the money. CPF OA is great because it offers 2.5% risk free, and you can actually just set up an CPF Investment Account and use it to buy a ton of Singapore stocks during a financial crisis (or if you’re pressed for cash, it can pay your mortgage or pay the deposit).

CPF SA is trickier because there’s no way to take it out before 55 (assuming no changes to the policy). But because the interest rates are so good (where else can you get 4% returns risk free), there’s no getting around this. If you’re a millennial like me, we probably have a couple of decades to go before we’re unlocking this CPF SA, so it should be viewed as a 20 to 30 year bond with great returns, but no liquidity. If you’re in your 40s and 50s, you can view this as real money, because you’re very close to unlocking this, and you should plan your asset allocation accordingly.

Quick Case Study

I’ll also take a quick chance to respond to this reader:

Good day to you,

Firstly, allow me to personally thank you for all the advice you have provided to investors thus far. Reading from books has given me the knowledge to navigate the SG investment scene, but it is always greatly helpful to get insight from sites like yours. I do browse through a couple of others as well, and to be frank, I am sending a similar email to all (just so I can have different perspectives).

About myself, I am a 32-year old husband and father of a [ ]-month old infant, with another one due in [ ] months.

Through various reasons (mainly due to I was ignorant on savings and always had my parents to support me), I have only started saving 3 years ago.

So I do not have a lot to invest, and I am conservative in nature so Ray Dalio’s portfolio suggestion appeals to me. How would you suggest that I adapt his portfolio to my context? I prefer SG stocks, though I may consider looking overseas as well.

Here below is a basic summary of my financial situation:

5-room BTO flat

– took a 30 year HDB loan in 2016 ($1200/month thru CPF – 50/50 split with my wife)

– starting this year, we are saving to pay 5k (hopefully more later on) yearly in cash to cut loan down to 20 years to save on interest charges

Wage (take home): 2.4k

Emergency Buffer: 13k in CitiBank MaxiGain

Money to invest: 20k (financial aim is to expand this to about 80k in about 20 years)

With my financial aim stated as above, do you think Dalio’s portfolio (plus me favoring SG stocks) would be able to assist me in acquiring my goal?

Would appreciate your insight. Many thanks in advance, and best wishes for your financial pursuits.

Financial Horse says:

Absolutely. An all weather portfolio works here.

However, the thing about the all weather portfolio, is that because it is so diversified, it performs well in all economic situations, but doesn’t perform terribly well in any one. So there will be extended periods of time where you may underperform a pure stock index because that economic regime favours stocks. Other times you will underperform a bond index because the regime favours bonds. But what you do get, is consistent returns through all economic situations, and the next time a financial crisis comes around, your losses are not going to be as astoundingly bad as those guys who have an 80% stock portfolio.

The hardest part of the all weather portfolio to me, is just doing nothing. You have to trust that the portfolio will deliver over a long period of time, and you’re just there to rebalance it annually. A lot of people will see this portfolio underperform the S&P500 for 8 years in a row, and decide to load up on the S&P500 at elevated valuations, and that’s probably the worst thing you can do.

What the all weather portfolio does though, is free up a lot of your time from having to monitor the markets, and allows you to focus other more important pursuits in life. You can take the extra time to build a family, build your career, build a side business, and lead a meaningful life beyond just investing.

It’s not for everyone of course, there are many out there who would want to take greater risk with their investment portfolio, but even if you are one of those there’s still a lot to be learnt from the beauty of an all weather portfolio.

I also wanted to stress that this is a sample portfolio for investors. How the exact allocation will work out for you, will depend greatly on your individual risk appetite.

Till next time, Financial Horse, signing out!

Financial Horse has a set of 7 Commandments for Successful Investing, that I ask myself before making every investment, and that I will never break regardless of the situation. Enter your email below to receive a copy in your inbox!

[mc4wp_form id=”173″]

Enjoyed this article? Like our Facebook Page for more great articles, or join the Facebook Group to continue the discussion!

Hi FH,

Great piece.

I think you could adapt more from Ray Dalio’s All Weather Portfolio beside CPF.

Your suggested current All Weather portfolio seems to suit Millennials. One area where Sporean and American cultures differ greatly is property probably due to massive land bloc of US of A and our small little island of Singapore.

Asian cultures esp Spore and HKK, property as an asset class in one’s portfolio is a must esp those who have achieved those basics and having the means to acquire second or third properties to augment their wealth.

Another reason is that historically, businesses are more likely to fail or their life-cycle expended than property/land assets. Yes, S& P 500 or DoW Jones index in portfolios may live longer than any business.

Interesting, are you referring to residential property or investment properties? I did include REITs in this analysis, but you are right, an investment home would greatly skew the asset allocation. I wrote an article on this previously, perhaps some of the thought process will come in handy:

https://financialhorse.com/ideal_asset_allocation/

Hi FH

Interesting coverage on the adaptation of the All Weather Portfolio, via the Uniquely Singapore away!

I wonder if you’ve heard of yet another portfolio allocation called the “Permanent Portfolio”? The Permanent Portfolio was originally developed by Harry Browne and it supposedly achieves the objective of sufficient diversification to protect the investor through a wide variety of economic and market environments.

And its allocation cannot be any simpler: 25% stocks, 25% bonds, 25% gold and 25% cash.

Some local finance bloggers such as Dr Wealth (https://www.drwealth.com/implementing-permanent-portfolio-in-singapore/) and 15HWW (https://www.my15hourworkweek.com/2015/03/22/should-you-build-a-singapore-permanent-portfolio/) have touched on how Singaporean investors can adapt the Permanent Portfolio. In fact, I think the former has even written a book on it (it’s available in NLB library).

It would indeed be interesting if we are able to get your perspective on this portfolio allocation with similar objectives. 🙂

-Koala

Interesting! Thanks for sharing this! Some quick thoughts:

1) Allocation to gold is massive. 25% allocation to gold is ridiculous, and in most economic situations, it’s going to be a massive drag on performance.

2) 25% bond 25% bond results in the portfolio being effectively, heavily overweight stocks in terms of risk allocation, so there will be large volatility.

3) Cash (or an emergency buffer) shouldn’t be included in the asset allocation. Under this portfolio, the bond component will already provide stability and liquidity, so there shouldn’t be a need to specifically allocate another 25% to cash. Holding cash as an investment is a form of market timing, and will hinder portfolio returns.

My initial impression is that this portfolio is too simplistic, and doesn’t take into account the risk profile of each asset class. The All weather portfolio is more sophisticated in this aspect, but even then it has also been simplified for the gneral public.

https://www.investopedia.com/ask/answers/09/permanent-portfolio.asp

Although the fund was considered a successful investment for providing investors security with moderate growth, during the 1990s, the Permanent Portfolio Fund badly underperformed compared to the stock market. During that period, it was not uncommon for stocks the appreciate 20-30% annually, while the permanent portfolio rose just over 1% each year. Today, many analysts agree that Browne’s permanent portfolio relied too heavily on metals and T-bills and underestimated the growth potential of equities and bonds. (To learn more, read Major Blunders In Portfolio Construction.)

Hi FH

Thanks for sharing with us your thoughts!

Indeed – if something sounds too simple and too good to be true, then it probably is worthwhile to examine it more critically.

That said if it was indeed that effective, I’m sure it would’ve created a bigger storm amongst the investing community. 🙂

-Koala

Hi, great piece. My favourite insight is “…the all weather portfolio, is that because it is so diversified, it performs well in all economic situations, but doesn’t perform terribly well in any one” and “The hardest part of the all weather portfolio to me, is just doing nothing.”

This is very true and won’t work for many investors because we want to see returns on our investment, or at least, a history of returns in the past. It is easy to look at an index fund and see that it has generally trended upwards for the last 30 years.

For my investment time horizon, I am okay to put money for 10-20 years and not think of cashing out in the short term. Because of this, I prefer buying a low-cost index fund, held long term. More straight forward.

Warren Buffet recommends this approach for most investors. If you can track an ETF for at least 10-20 years and not think of cashing out, it would weather most bumps along the way. Historically, the trend long term has been upward.

Also, when it is downtrend, I won’t feel the pressure to cash out as much as historically, this approach has beaten many actively managed funds. 🙂 There is so much focus on choosing one popular strategy these days.. I think people forget to choose one that is suitable for themselves, their goals, time horizon, risk tolerance.

Just sharing my current portfolio: I’m 25

“Safe investments” 58%

8% physical gold and silver (in the dooms day scenario)

20% short term fixed deposits, Singapore saving bonds (pays interests 1.55%-1.95%, capital guaranteed)

30% Invest in my own business/cash for other buying opportunities (100+% returns on own biz)

“Riskier Investments” (track index funds, already diversified by its nature)

30% S&P 500 US index fund IVV

10% China Index Fund MCHI (Ray Dalio recently pointed out investing in China. In the trade war, I would wanna have my bets on both horses)

“Risky Investment/Gambling”

2% cryptocurrency/funding passion projects

What do you think?

Haha that’s quite well though out portfolio actually, I quite like it myself! 😉

What I would say, is to focus on trying to understand yourself. So for me my underlying portfolio is quite similar to an all-weather as well, but because I absolutely love thinking about and following global macro trends, this blog is my outlet, and I also keep a small portion of my portfolio to make tactical bets on global macro. I find that it helps to juice up returns, and keeps me from messing around with the rest of the portfolio.

🙂

Anyone interested to see how Ray’s All Weather portfolio performed through the COVID crisis can see the numbers here:

http://www.lazyportfolioetf.com/

Thanks for the link!