Basics: What is Financial Independence Retire Early (FIRE)

I was reading an article about Financial Independence Retire Early (FIRE) on Seedly recently.

For those who are new to the concept, FIRE is a pretty big movement globally these days. It started getting popular in the US post 2008, and has since spread to most parts of the world, Singapore included.

The core idea behind FIRE goes like this.

Save up 25 times your annual living expenses, and invest that in a diversified portfolio. Once you do that, you can spend 4% of that portfolio every year (either dividends or withdrawal) for the rest of your life, and never run out of money. And because that 4% equals your typical living expenses, you’re now financially independent, and working a day job becomes optional. You’re free to retire early, or move to jobs that interest you.

To illustrate very simply, imagine that 小明 and his wife just got married and are living in a BTO in Singapore. They are working as accountants and they absolutely hate their job. They estimate that their living expenses every year is about $50,000. They are big FIRE movement proponents, and calculate that once they save up 25 times their annual living expenses ($1.25 million), they’ll be able to spend 4% of that portfolio every year ($50,000) for the rest of their lives, and never deplete the portfolio.

They make it their goal to save up $1.25 million, and move on to the things in live that really matter to them.

The 2 key issues behind Financial Independence Retire Early (FIRE)

For FIRE to work, there are 2 key points to get right: estimating your annual living expenses, and the 4% rule.

Estimating your Living Expenses

To put it simply, you need to be able to estimate your annual living expenses accurately. In 小明’s example, he needs to be sure that the $50,000 will adequately cover his living expenses, even well into retirement. Because if his living expenses suddenly rise to $100,000, then FIRE doesn’t work so well, and he needs an alternative source of income, otherwise the portfolio will gradually deplete.

Inflation

And the biggest difficulty with estimating living expenses over a longer term period is inflation.

To illustrate – imagine that 小明 is 25 now. Using his current $50,000 living expenses and a 2% inflation rate, by the time he is 65, that annual living expenses is now $110,401. Up inflation to 3% and living expenses goes to $163,101. If it goes to 4% you’re looking at $240,000.

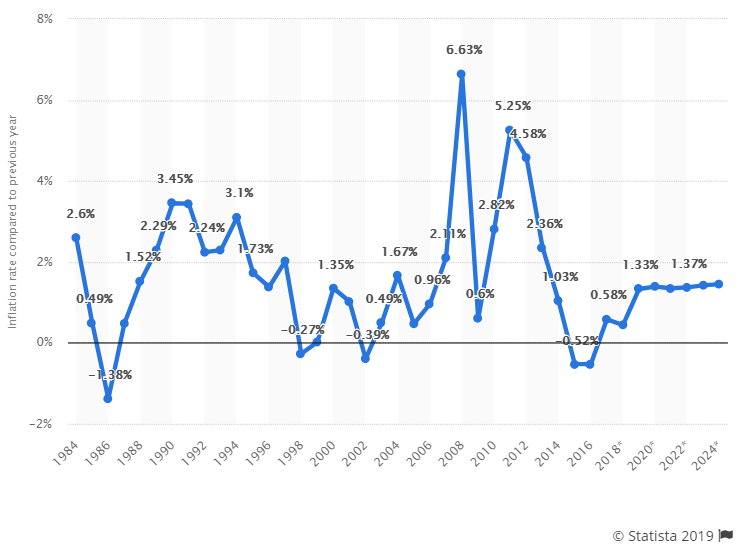

Historically speaking, inflation in Singapore has been pretty tame at about 1.7% on average, and it’s been quite low the past few years. But if you want to retire early and FIRE, you need to have a rough estimate of what inflation will look like in the coming years, which could be a tough ask.

And as seen from the chart below, inflation is lumpy. There are years when its really high (like in 08 during the GC and 2012 in the Euro debt crisis), and years when it’s really low (2015 in the oil bust). This actually has huge implications for asset allocation as we’ll see later.

The alternative of course, is to be more conservative when estimating living expenses. So if you add on a 20 to 30% buffer to your annual living expenses, and you’re able to adjust your lifestyle to one that is less expensive, this issue can probably be resolved. But if you add 20 to 30% to your living expenses, and multiply that by 25, suddenly that’s a lot more money to save for retirement.

4% rule

The second problem, and the big one, is the 4% rule.

The current FIRE movement asks you to save up 25 times your living expenses, because it estimates that you can withdraw 4% from the portfolio for the rest of your life.

And what is this magical portfolio you ask?

For the US retire early FIRE guys, they use a 60-40 stock bond portfolio split. In ETF terms, it’s broadly a 60% in the S&P500, and 40% in a medium term bond fund like the TLT.

Backtested using data since the 1870s, they’ve found that this portfolio can return 4% a year for every single rolling 30 year period, without ever depleting. In fact, it finds that most of the time, the 60-40 portfolio usually leaves behind a fairly large sum for your descendants.

One big flaw with this backtesting, is that is uses US data since the 1870s, which coincidentally was the same time when US rose to sole superpower status. Heck, you could run the same analysis for a forest in US and still find that is returns more than 4% annually. That’s what happen when you bet on a country that becomes the world’s superpower.

Asset Allocation for Singapore Investors

So the million dollar question here is. If I’m a Singapore investor, how do I construct a portfolio that returns a minimum of 4% a year, every year, for the rest of my life?

Do I go with what the US FIRE articles recommend, and use a 60-40 US stock-bond split? There are a few big problems with such a portfolio for Singapore retire early investors:

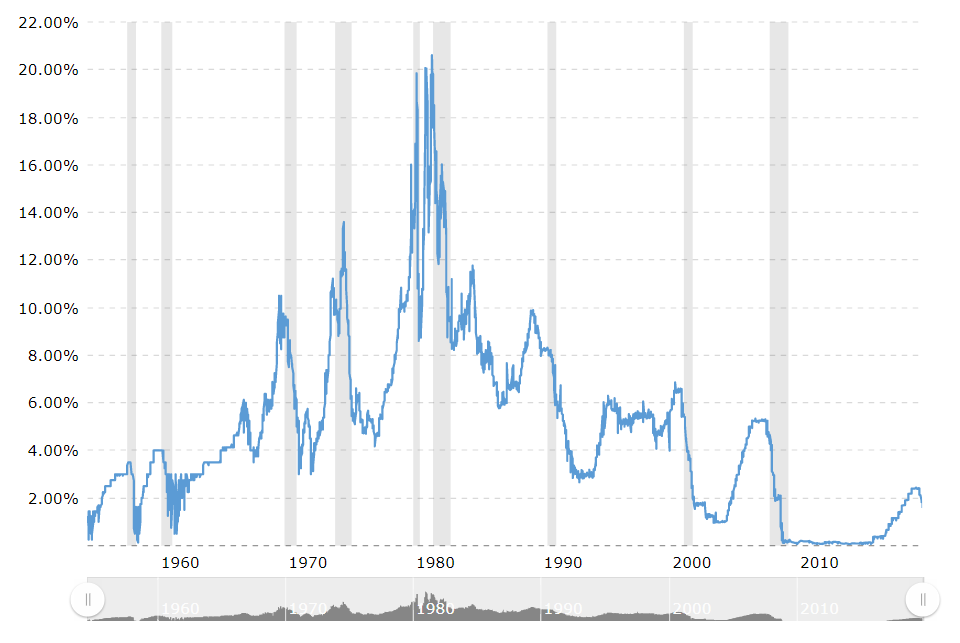

Big position in Bonds at the end of a 30 year bull market – Global sovereign debt has had a 30 year bull market. Just look at the long term interest rate chart for the US below. Interest rates peaked in the 1980s, and it’s been on a secular downtrend since. The prices of bonds trade inversely with interest rates, so anyone buying bonds since the 1980s has made a ton of money.

But investing is forward looking, so if you’re going to put 40% of your retirement portfolio in bonds right now, you need to know whether bonds are going up or down over the next 30 years. And just look at the chart below. Do you think the next move is going to be down?

60-40 underperforms in high inflation scenarios – The problem with a pure stock bond portfolio, is that it underperforms in high inflation scenarios. Without exposure to gold and commodities, when inflation in the economy is high, the stock bond portfolio will return good nominal returns, but poor real returns (inflation adjusted).

For an early retiree, FIRE proponent, this is big, because with high inflation your expenses are going up, but your portfolio may not be going up to the same extent.

Exposure to Forex Risk – As a Singaporean investor, if you follow the traditional FIRE movement’s 60-40 stock bond split, you’re probably doing something like the S&P500, and a long term treasury fund like the TLT. Because these assets are denominated in USD, you’re exposing yourself to huge forex risk.

If the SGD appreciates significantly against the USD, you could be sitting on big gains on your portfolio, but converted back to SGD, you’re still not making enough to cover living expenses.

What is the right asset allocation for a Singaporean investor?

So if Financial Horse were to retire early, how would I build my portfolio?

There are 2 main ways that I can think of: (1) an all weather portfolio and (2) active management.

The first is to use an all weather portfolio. I wrote about this a while back here, and it’s elaborated on in much greater detail in the Financial Horse course. The key idea is to use a mix of asset classes, from stocks, bonds, real estate, gold and commodities, to construct a portfolio that does well in all economic regimes, including high inflation ones.

There’s no free lunch in this world of course, so a portfolio that does well in all scenarios, doesn’t perform terribly well in any scenario. So you’re sacrificing portfolio returns, for stability and peace of mind.

The other way, is active management. So you’ll keep up to date with broad economic trends, and move assets around to juice up your performance. If you think inflation is going to go up, you’ll sell some bonds and use that to buy gold. You also read Financial Horse regularly to keep up to date with investing trends. That’s the rough idea.

And if you’re good about it, your returns can be fantastic, you may be able to return well in excess of 4%, and live a lavish lifestyle in retirement.

The downside, is that you need to spend lots of time keeping up to date with markets, even after retiring early. It’s okay if you’re a financial nut like I am, but I get that not everyone’s idea of retiring early is keeping track of financial markets on a regular basis. For those of you, you can either go with the all weather portfolio, or outsource your financial management to a third party manager.

If you go with the latter, you need to be really sure that your manager will be able to deliver the returns you need (you could also outsource it to a few different managers if you have enough funds).

Neither approach is perfect however, and to me, this is the biggest flaw with the retire early FIRE movement. Most FIRE article out there simply gloss over the asset allocation point. But in reality, building a portfolio that can return 4% for the rest of your life, for Singapore investors, is more easily said than done.

Singapore is too small an economy to survive on its own, so if you just buy the STI ETF, you’re making a huge bet on the future of Singapore, and if it doesn’t pan out retirement life may not be cushy. If you allocate to other big global markets like US and China, you get potentially higher returns, also higher potential risks.

How to find the right balance in asset allocation, to me, is the crux of the issue for early retirees (FIRE) in Singapore.

Note: Exclude the house you live in

And don’t forget that when running calculations for FIRE, you need to exclude your primary residence. You should only be counting assets that generate cash, and your primary residence is for you to live in, not earn money.

I know many people who plan to sell their house and downgrade to something smaller when they get older, so for those of you, you can probably add in a portion of the house value. There are many who plan on living in a fancy house forever though, so it really depends on your goals in life.

Closing Thoughts: FIRE in Singapore

The Financial Independence Retire Early (FIRE) movement was born in the US earlier this decade. A lot of them were tech professionals who made a ton of money in tech (eg. Early Google / Amazon employees), and then decided to retire early and run blogs.

It’s also no coincidence that the FIRE movement is hugely popular after a 10 year bull run in the stock market. Anyone who started on this retire early movement 10 years ago, could pretty much put his money into 1 or 2 ETFs and watch the money go up 2 to 3 times.

Now the point of this article isn’t to dump cold water on the whole retire early movement. I think it’s a fantastic goal to work towards and can be a great motivator. No, the point of this article is to highlight that retiring early is a lot more nuanced than most people are making it out to be.

The past 10 years were good for investors.

But if you want to retire early, you’re going to need to live through about another 40 years of financial markets. And a lot of things can happen in 40 years.

Any other issues that I missed? Share your comments below!

Looking for a comprehensive guide to investing? Check out the FH Complete Guide to Investing for Singapore investors.

Support the site as a Patron and get market and stock watch updates. Big shoutout to all Patrons for their support!

Like the Financial Horse Facebook Page and join the Facebook Group (Singapore) or Facebook Group (China) to continue the discussion!

Hi, FH, good article, and one I’ve been pondering on for a while. Not so much on whether it would work, but what it would take for it to work. What do you think about using Endowus as an all weather portfolio?

Haven’t looked into them too closely to be honest. Perhaps you could share some thoughts on why you’re considering using them as an all weather? From what I recall, they’re using Dimensional Equity funds and Pimco Bonds right? The lack of allocation to gold/commodities will make it tricky to function as an all-weather.

Hi, thanks for the reply. My apologies, I meant “as a part of”. I am currently allocating a small portion of my cash monthly to Endowus’ funds. Am keen to see how the funds perform. It’s nearly idiot- proof. Haha. The large majority however, are still into actively managed stocks and bonds.

I am curious to see how they perform as well!

I think 4% rule is inflation adjusted, meaning every year the amount withdrawn goes up as per inflation, so that 小明 is maintaining his lifestyle at 55k constant dollars.

What do you mean by inflation adjusted? Do you mean that the portfolio generates 4% real returns every year?

If so then yeah I agree, but building a portfolio that generates 4% real returns vs 4% nominal returns are very different asks, and require different approaches.

Interesting point, thanks for raising this thought.

The 4% rule is indeed inflation adjusted.

Developed by William Bengen, a financial planner from MIT, the 4% Rule study offers this: a retiree can take 4% of their initial retirement assets, and increase that amount every year to account for inflation, assuming a 50% to 75% portfolio allocation to stocks.

See original paper. http://www.retailinvestor.org/pdf/Bengen1.pdf

Thanks for sharing this!