So… the next T-Bills auction is on 12 Oct (Thursday).

After last auction’s T-Bills came in at a whopping 4.07% yield.

I think it’s safe to say that investor interest in this T-Bills auction is going to be very strong.

Will we see interest rates stay at 4.07%?

Are T-Bills still worth buying vs other options like Fixed Deposit or Singapore Savings Bonds?

Let’s dive in.

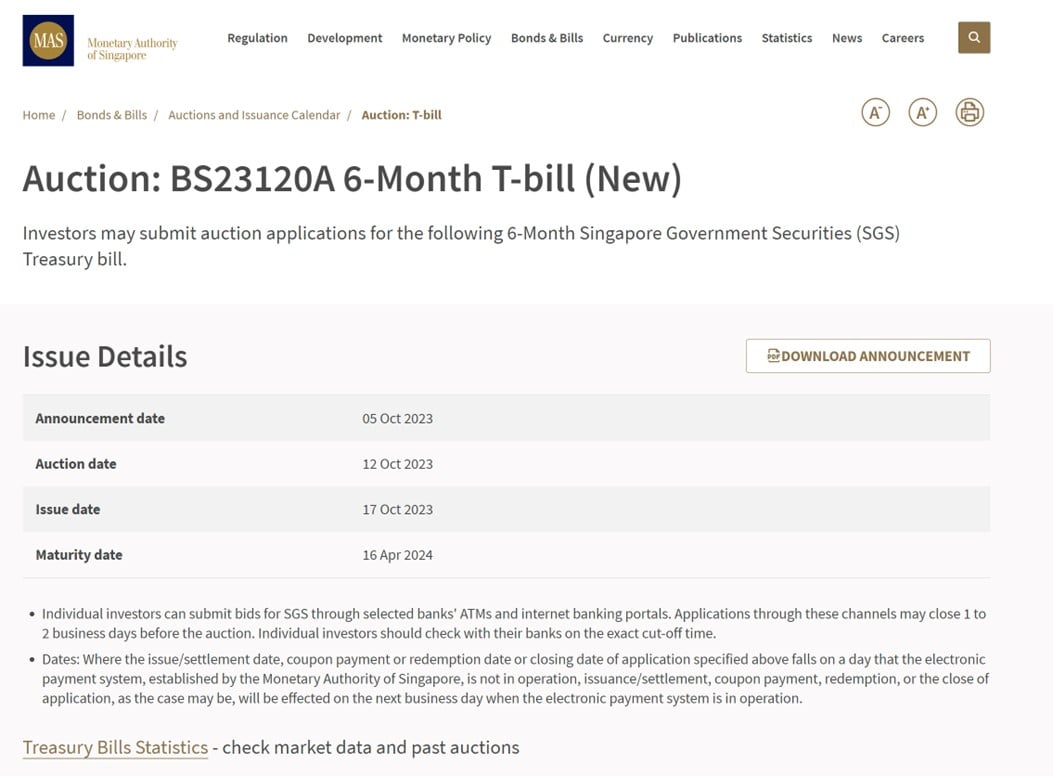

Next T-Bills auction is on 12 Oct (Thursday) – (BS23120A 6-Month T-bill)

First off – next 6 months T-Bills auction is on 12 Oct 2023 (Thursday).

If you’re applying in cash do apply by 9pm on 11 Oct 2023 (Wed)

For CPF-OA you’ll want to get it done by 10 Oct.

What is the estimated yield on the next 6-month T-Bills auction? (BS23120A 6-Month T-bill)

T-Bills trade at 3.97% on the open market

In the latest auction debrief I gave 2 possible explanations of why T-Bills yields jumped from 3.75% on the open market to 4.07% at the auction.

It was either:

- Freak Result – The auction was a freak result due to a sharp drop in demand, and the actual fair value of T-Bills is 3.75%

- Market pricing not accurate due to poor liquidity – Due to poor trading liquidity, the 3.75% market pricing was inaccurate. Fair value is 4.07%, and it took the T-Bills auction to achieve price discovery

I suggested the way to tell which of the above was accurate – was to look at how T-Bills trade after the auction date.

If it stayed at 3.75% then we’ll know it was (1).

If it jumped to 4%ish then we’ll know it was (2).

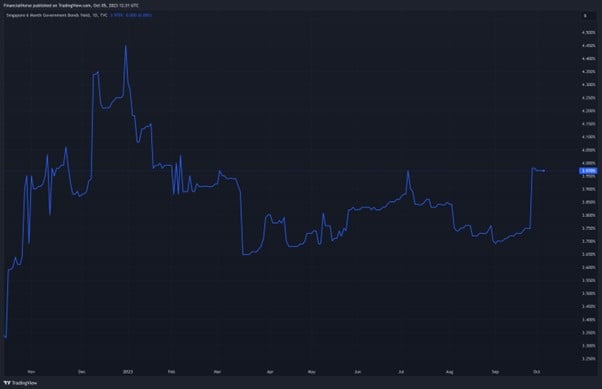

As it turns out – this was the move in 6 month T-Bills on the open market.

6 month T-Bills yields jumped to 4%ish (3.97% today), which suggests that (2) is correct.

This is a good sign – suggests that T-Bills yields may stay high this auction.

But… T-Bill trading liquidity is incredibly thin

That being said, trading liquidity for the T-Bills is incredibly thin.

I extracted the daily candle chart for the 6 month T-Bills below, and you see how few trades are actually done on the open market.

So I would caution against placing too much reliance on market pricing on T-Bills – there just isn’t sufficient trading liquidity for true price discovery.

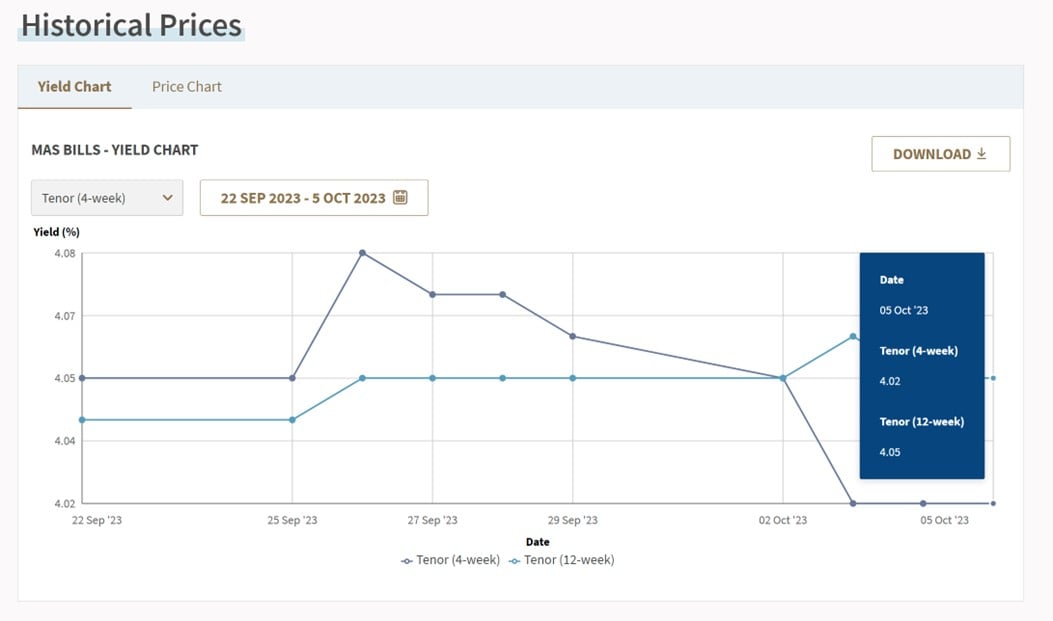

12-week MAS Bills flat at 4.04%

The institutional only 12-week MAS Bills have been flat the past month or two – at 4.05%.

Sharp moves in MAS Bills are a good indicator of the trend for T-Bills.

So as of now, MAS Bills are not showing any big changes in yields either way.

If you are submitting a competitive bid I do suggest taking a quick look at the latest MAS Bills pricing before you apply.

If there is a sharp move up or down – that could suggest a similar trend for T-Bills (can access it here).

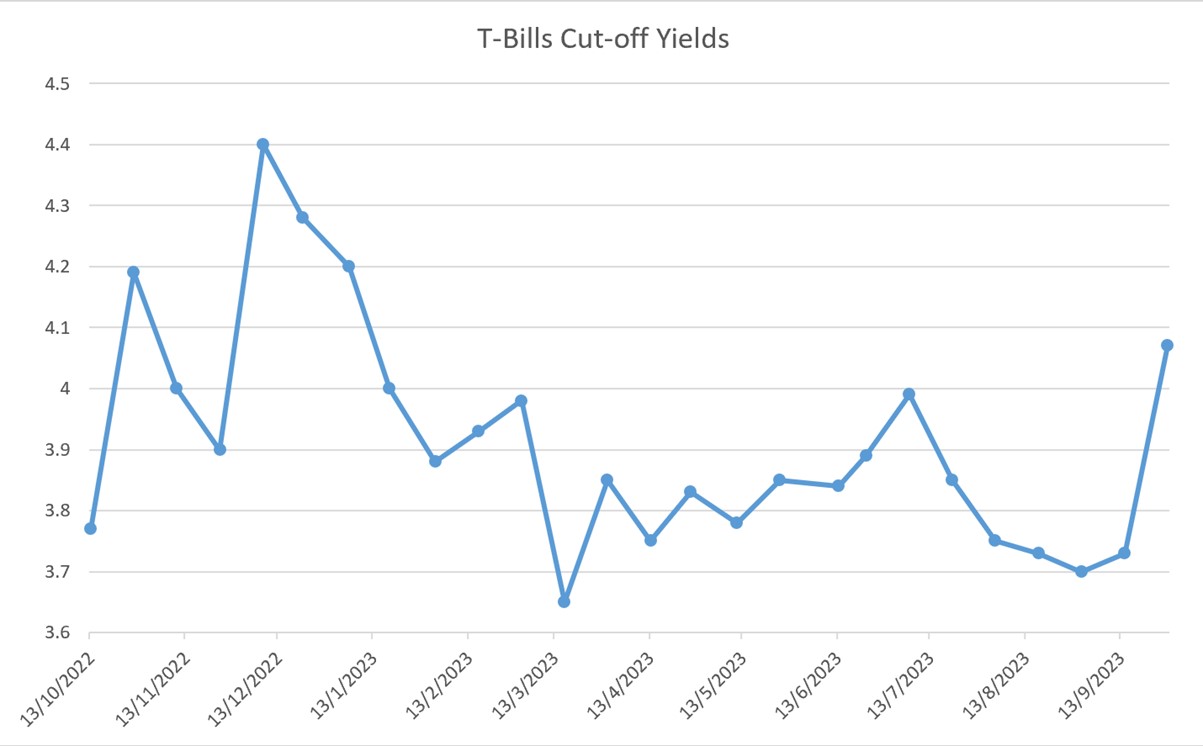

T-Bills yields jumped the previous auction to 4.07%

As most of you know by now – T-Bills yields jumped the previous auction.

Going from 3.73% up to 4.07%.

The second highest yield of 2023.

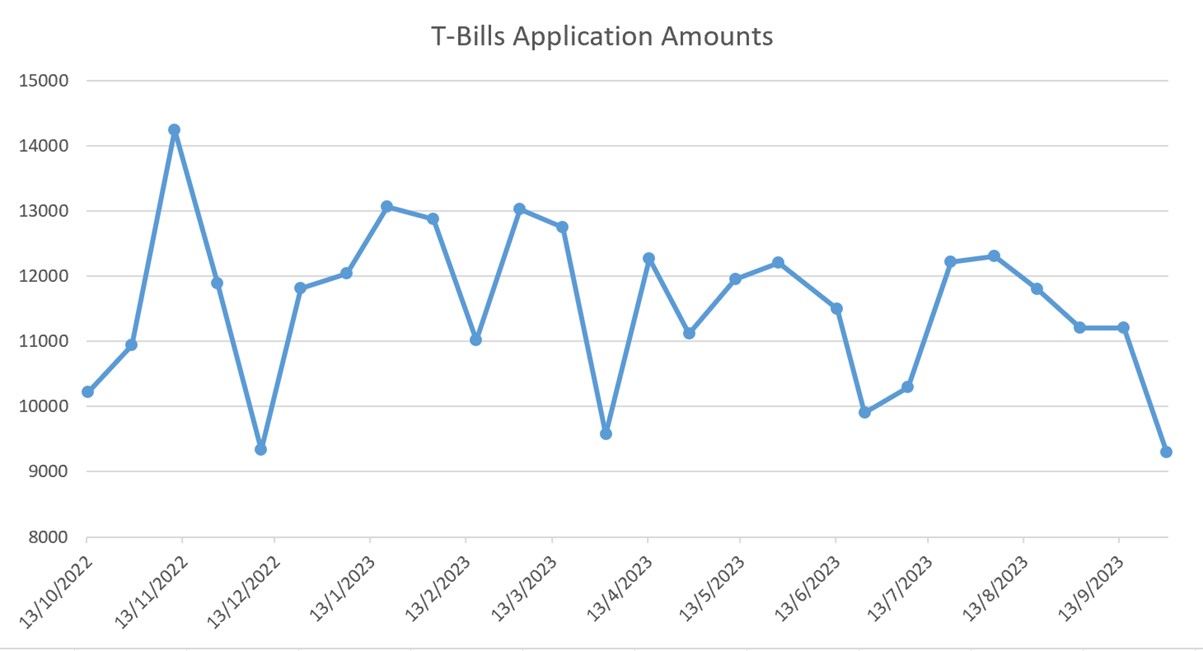

While demand for T-Bills plunged

A big part of this was due to the plunge in T-Bills application amounts.

Demand dropped 17%, from $11.2 billion to $9.3 billion.

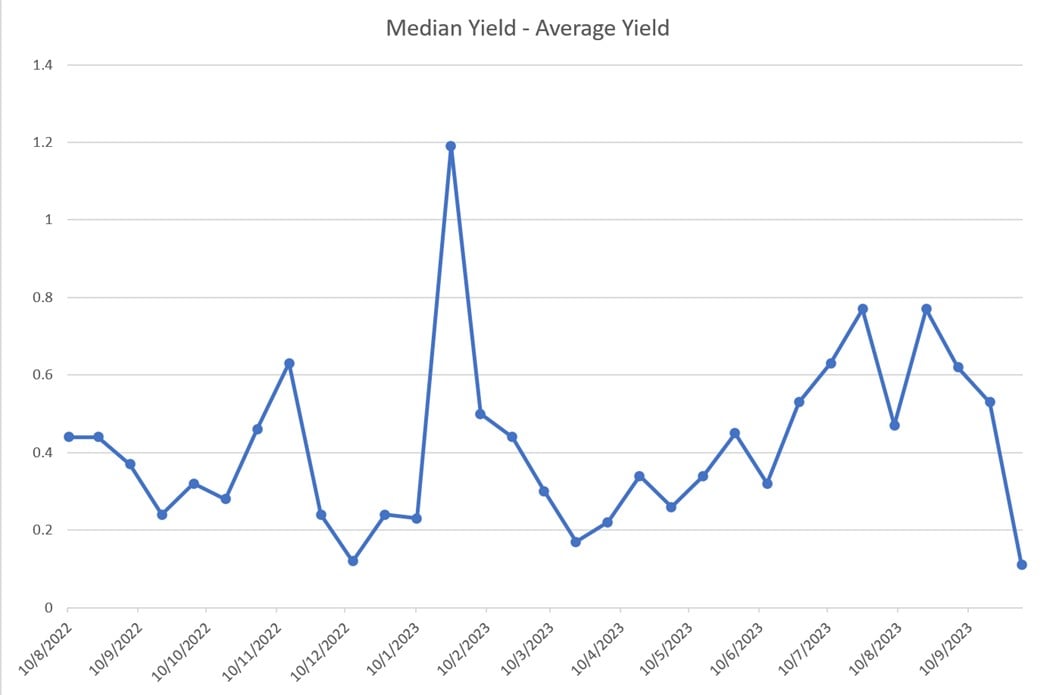

Median Yield – Average Yield narrowed – less “lowballers”?

You can see this reflected in the spread between the median yield and average yield.

To illustrate what this is:

Imagine you have 100 bids.

The median yield, is if you arrange all the bids from small to high, and take the yield of the 50th bid.

While average yield, is adding up the yields of all 100 bids and dividing by 100.

So average yields are skewed by lowball bids, while median yields are not.

To put it simply – the bigger the spread between the median yield and average yield, the more “low-ballers”.

And the most recent auction, this spread between the median yield and average yield was even lower than the lows hit in Dec 2022 (where yields shot up to 4.4%).

This meant very few “low-ballers”.

Now why this is the case is not so straightforward to answer.

But you’ll note that the spread has a big correlation to demand – in that the spread narrows in auctions where demand is low.

So it’s a bit of a chicken and egg.

Will this repeat the next T-Bills auction?

But I digress.

The million dollar question is – Will this repeat the next T-Bills auction?

Will demand remain low, and the number of low-ballers remain low, such that yields stay high?

What happened the last time the spreads were this low?

The last time the spread between median and average yield was this low was Dec 2022 – when yields soared to 4.4%.

In that case, in the next auction:

- Demand increased from $9.3 billion to $11.8 billion (26% increase)

- Spread between median and average yield went up from 0.12 to 0.24

- Yields dropped from 4.4% to 4.28%

If we go by this logic – then the next T-Bills auction should see higher demand and more low-ballers.

And yields should go down, but probably not plunge.

But I mean, that’s a really big if right there.

Estimated yield of 3.90% – 4.10% on the 6-month T-Bills auction? (BS23118S 6-Month T-bill)

Putting all this together.

The fact that yields remain high on the open market.

The fact that we’re likely to see a surge in demand the next T-Bills auction.

I would say yields *probably* come in lower than 4.07%, but *probably* still in the 3.9ish – 4ish range.

I would go with an estimated yield of 3.90% – 4.10% on the next T-Bills auction.

For obvious reasons though – there is significant uncertainty because you just can’t predict with certainty how investors will bid.

As always, I encourage investors to submit a competitive bid (just in case there is a freak result and yields drop a lot).

And submit as close to the deadline as you can, so you can take a look at where market pricing is at that time before deciding on your bid.

Are T-Bills still worth buying vs Singapore Savings Bonds or Fixed Deposit or Savings Accounts?

Singapore Savings Bonds are a decent buy – and will get better

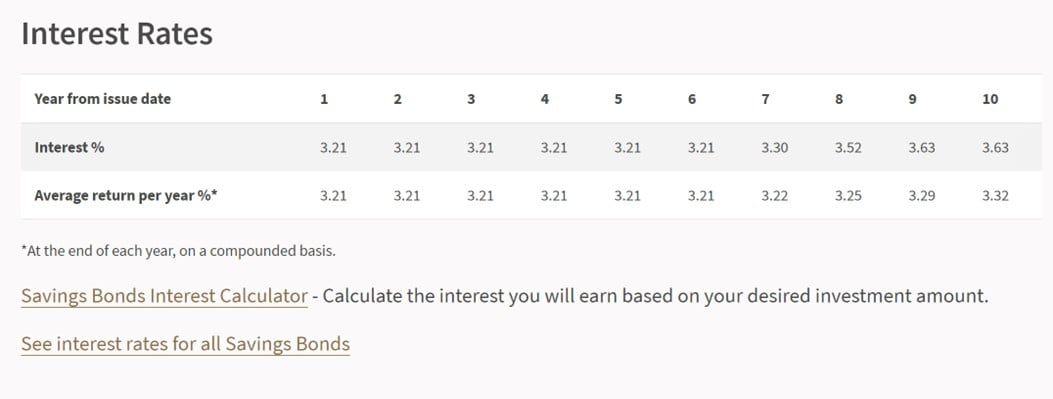

I just want to put it out there that this month’s Singapore Savings Bonds are very, very decent.

You’re locking in 3.21% yield for the next 6 years, stepping up to 3.32% over 10 years.

That’s risk free yield locked in for 10 years, and you can get the money back anytime with no capital loss.

Considering CPF-OA pays 2.5%, to be able to get 3.32% risk free for 10 years is very attractive.

What’s more – Singapore Savings Bonds yields track the 10 year SGS yields.

And the 10 year SGS yields this month is likely to be higher than last month’s.

If so – next month’s Singapore Savings bonds are going to be even more attractive, as an alternative to T-Bills.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great charts & insights on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

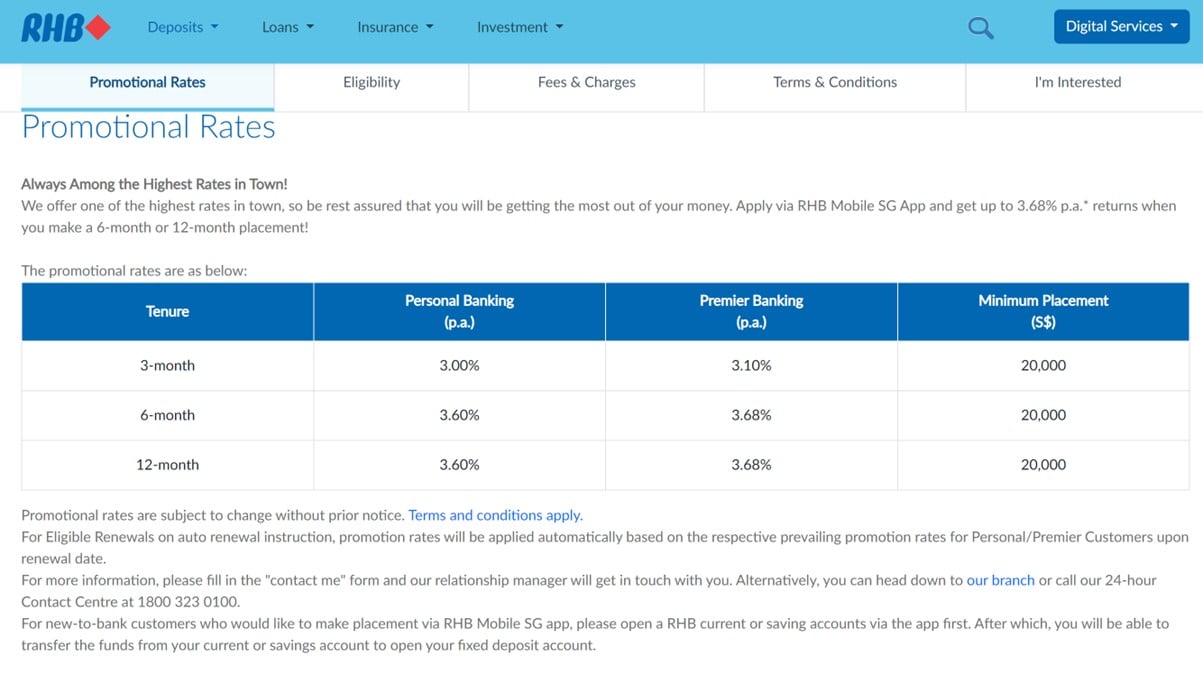

RHB Bank Fixed Deposit – 3.68%

The best Fixed Deposit option I could find today is RHB at 3.60% for 6 months.

Minimum of $20,000, that steps up to 3.68% if you are premier banking.

So if you don’t want to buy T-Bills, this is probably the next best thing.

Are T-Bills still worth buying vs Singapore Savings Bonds or Fixed Deposit?

Generally speaking I would say if you want the highest short term yield, T-Bills are better than Fixed Deposit.

But if you already have a lot of cash in short term instruments and want to lock in something for a longer duration, Singapore Savings Bonds (SSBs) are a great diversifier.

SSBs are likely to get even better next month though, so I leave it for individual investors to decide if you want to apply now and wait for the next month – I will share further thoughts on this in another article.

Am I applying for T-Bills?

Yes I am.

I’ve been applying for almost every T-Bills auction this year (I roll whatever excess cash I have into T-Bills for the highest yield).

I have a chunk of cash from an OCBC Fixed Deposit yielding 4.08% that just matured, and I will look to roll them into T-Bills next week.

But T-Bills don’t offer good liquidity because they cannot be easily sold before maturity.

So I do maintain a chunk of liquid cash in a mix of:

|

Instrument |

Approx Yield |

Maximum |

|

UOB One |

5% |

$100,000 |

|

Singapore Savings Bonds |

3%+ |

$200,000 |

|

MariBank Account |

2.88% – 3.5% |

$75,000 |

In the past I also tried GXS and Chocolate Finance (see my review on Chocolate Finance), but these days the bulk of spare cash goes into a mix of the 3 above.

MariBank Account (SDIC Insured, by Shopee)

I did a full review on MariBank Account recently, which is the bank by Shopee (Sea Ltd).

Long story short:

- SDIC Insured

- 88% yield

- Withdraw anytime, no lockup

- No minimum amount (maximum of $75,000)

It’s simple, fuss free, and SDIC insured, what’s not to like?

Do note there is an option in MariBank that allows you to invest in money market funds for a higher yield (Mari Invest).

The money market fund is a special tie up between MariBank and Lion Global – the Lion-MariBank Save Plus Fund.

Trailing yield is about 3.2 – 3.5%, and 60% of the funds are invested in MAS Bills, which makes this a lower risk product (but not risk free).

The main highlight in my view is that unlike other money market funds where the cash only comes back on T+1, with Mari Invest any amount up to $10,000 can be sold and withdrawn immediately.

Basically Mari Invest is offering the bridge loan up to $10,000 to cover the T+1 withdrawal timing, which I really like – to the extent that I put the full $10,000 in.

Whatever the case, I would love to hear what you guys think

Are you applying for the next T-Bills auction?

How are you allocating your cash these days?

This article was written on 6 Oct 2023 and will not be updated going forward.

For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do sign up as a Patreon.

WeBull Account – Get up to USD 2000 worth of shares

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 2000 free fractional shares.

You just need to:

- Sign up for a WeBull Account here

- Fund any amount

- Hold for 30 days

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Investment Research Tools

I use Trading View for my research and charts. Get $15 off via the FH affiliate link.

I also use Koyfin for fundamental and macro research. Get a 10% discount via the FH affiliate link.

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Best investment books to improve as an investor in 2023?

Check out my personal recommendations for a reading list here.

The content here is for informational purposes only and should NOT be taken as legal, business, tax, or investment advice. It does NOT constitute an offer or solicitation to purchase any investment or a recommendation to buy or sell a security. In fact, the content is not directed to any investor or potential investor and may not be used to evaluate or make any investment. Do note that this is not financial advice. If you are in doubt as to the action you should take, please consult your stock broker or financial advisor.

Hi FH, I have 2 questions:

1. If I remember correctly, you invested your CPF OA in T Bills. Has it matured? And if yes, were you able re-invest in T bills again without losing interest as a result of the rollover (I mean, I still find it difficult to calculate the loss of CPF interest depending on whether the money is withdrawn beginning of the month and end of the month and how to manage the rollover when the T bill matures so that I won’t lose interest.)

2. I have:

a. SSB GX23010Z (average return yr1-3=2.95% p.a., yr4=3.02%, yr5=3.09%, yr6=3.13%, yr7=3.16%, yr8=3.19%, yr9=3.23%, yr10=3.26%

b. SSB GX23050W (average return yr1-7=3.03%p.a., yr8=3.04%, yr9=3.06%, yr10=3.07%).

I’m thinking of redeeming one of them to buy the SSB to be issued in Dec 2023 (I’m counting on SSB rates getting even better for the Dec issue). I need to sell it this month, get the cash in Nov, then buy new SSB. But not sure how to figure out which one to sell. Can you please show me how to think about this? Thank you!

Hi Blue Blur, my comments below:

1. You need to rollover in the same month if you don’t want to lose another month’s interest. I dont believe I managed to do it with the most recent T-Bills (CPF-OA).

2. I’ll do a full article on SSBs, and will answer this question in greater detail as a case study. Basically you think about how long you are likely to hold the SSBs for, and optimise for that duration. So if you think you will only hold 3 years, then you might as well redeem the (a) first and enjoy the higher short term rates from (b).

I would say a bird in hand is worth 2 in the bush. 10 years is a very long time!