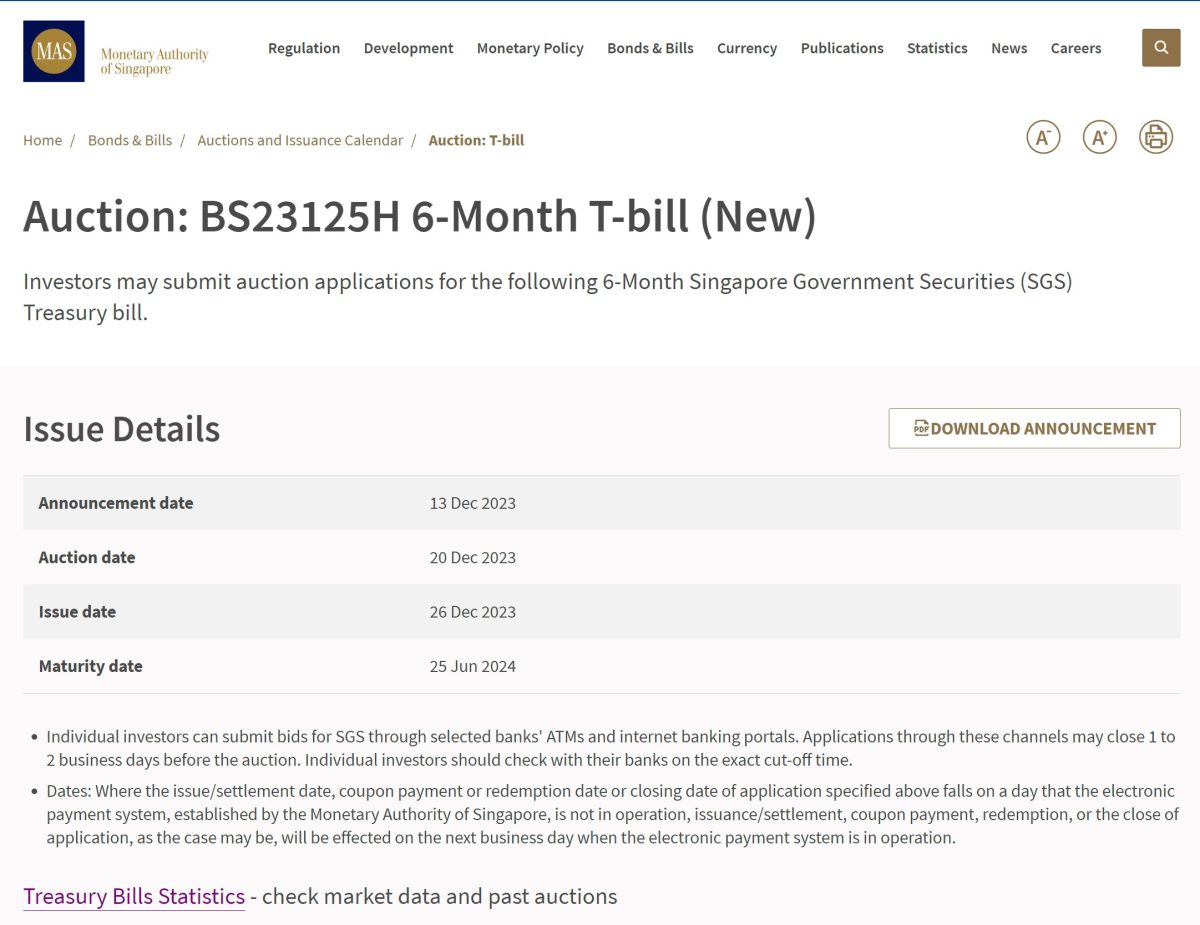

Now the next T-Bills auction is on 20 Dec.

Unfortunately, after closing as high as 4.07% a few auctions ago.

T-Bills yields have since dropped to 3.74%.

US interest rates have also plunged of late – the US 10 year yield dropping from 5% to below 4% this week.

Jerome Powell this week also seemed to confirm the market’s view of 2024 interest rate cuts – only question being how many cuts we see.

Put it all together and it doesn’t really look bullish for T-Bills yields – and will T-Bills interest rates drop further?

Next T-Bills auction is on 20 Dec (Wed) – (BS23125H 6-Month T-bill)

First off – next 6 months T-Bills auction is on 20 Dec (Wed).

Note that this is Wednesday, instead of the usual Thursday.

This means that:

- If you’re applying in cash do apply by 9pm on 19 Dec (Tue)

- If you’re applying using CPF-OA do apply by 18 Dec (Mon)

What is the estimated yield on the next 6-month T-Bills auction? (BS23125H 6-Month T-bill)

I’ll split the analysis up into 2 parts.

From a (1) fundamentals perspective (economic growth, inflation, global interest rates etc), and a (2) technical perspective (supply-demand).

From a (1) Fundamentals perspective:

T-Bills trade at 3.73% on the open market

6-month T-Bills are trading at 3.73% on the open market.

But… T-Bill trading liquidity is incredibly thin

But we’ve seen the past few auctions that trading liquidity on the T-Bills is so thin – that actually the market pricing is not that indicative.

You’ll find that the market pricing actually takes its cue from the latest T-Bills auction.

The past few auctions where the T-Bills auction yield diverged materially from market price (whether up or down).

It was actually market price that adjusted to the latest T-Bills auction yield, rather than the other way around.

So I would caution against placing too much reliance on market pricing on T-Bills – there just isn’t sufficient trading liquidity for true price discovery.

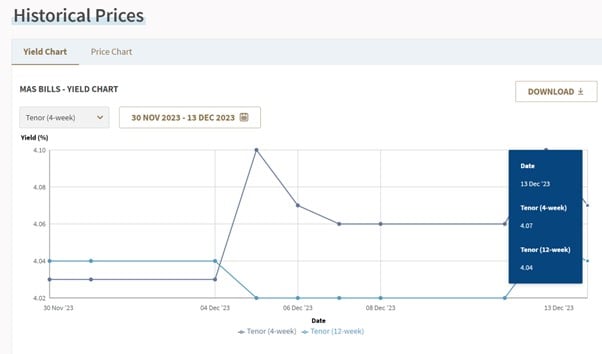

12-week MAS Bills flat at 4.04%

The institutional only 12-week MAS Bills have been flat the past month or two – at 4.04%.

Sharp moves in MAS Bills are a good indicator of the trend for T-Bills.

So as of now, MAS Bills are not showing any big changes in yields either way.

If you are submitting a competitive bid I do suggest taking a quick look at the latest MAS Bills pricing before you apply.

If there is a sharp move up or down – that could suggest a similar trend for T-Bills (can access it here).

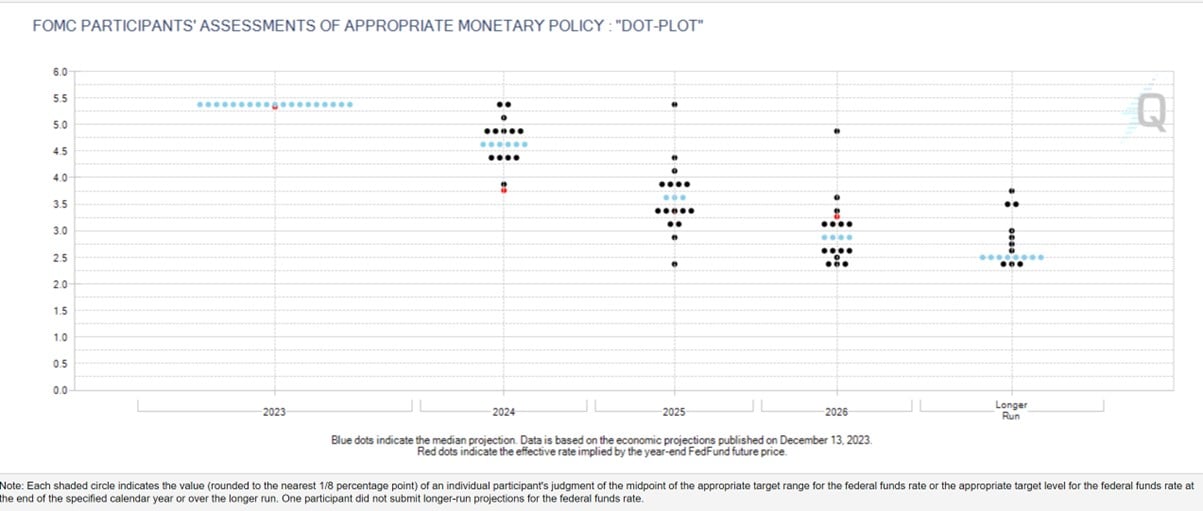

BUT – Interest rates expectations have plunged, confirmed by Jerome Powell this week

It’s fairly clear by now that the Feds are done with rate hikes (July was the last hike).

The question now is how many rate cuts we will see in 2024.

This is the latest Fed dot plot, member themselves see anywhere from no rate cuts to 6 rate cuts:

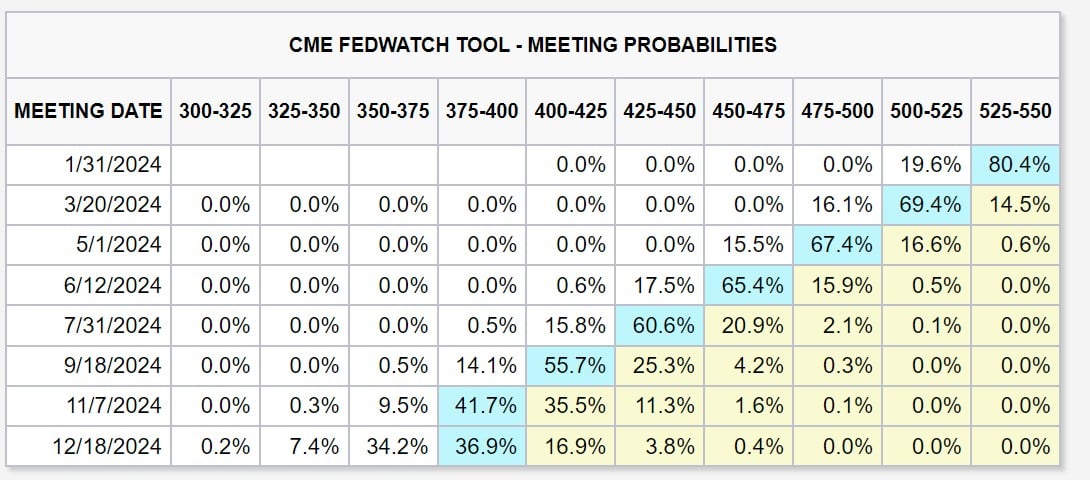

While the market is pricing in a total of 6 rate cuts in 2024 – starting as early as March 2024.

Historically speaking, the Fed usually pauses 6 – 12 months before starting to cut.

Given July 2023 was the last rate hike of the cycle, the timing of interest rate cuts in 1H 2024 does seem to be in the rough ballpark.

Whatever the case, this does not bode well for T-Bills yields.

US Interest Rates have plunged

This is the US 2 year yield – from 5% a few weeks back to 4.35% this week:

The plunge is even more stark with the US 10 year yield – from 5.0% to 3.98% this week:

From a Technicals, supply-demand perspective

From a more micro perspective, what matters is the supply-demand dynamics.

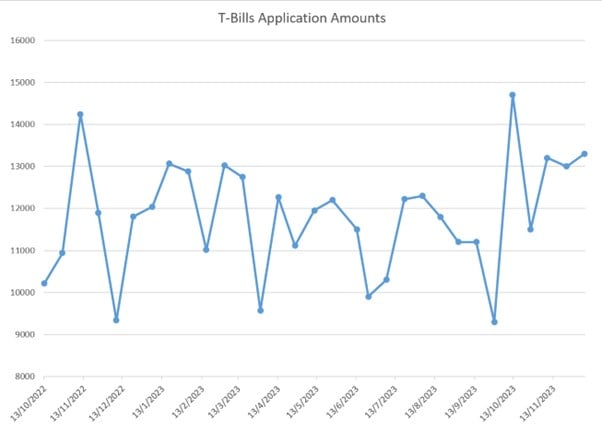

Demand for T-Bills increased the previous auction to $13.3 billion (vs $13.0 billion)

In the latest T-Bills auction, demand for T-Bills increased slightly to $13.3 billion (vs $13.0 billion the previous auction).

This is not great – as it shows demand stabilising at record levels.

You can see how current levels of T-Bills demand is around the highest it has been in all of 2023:

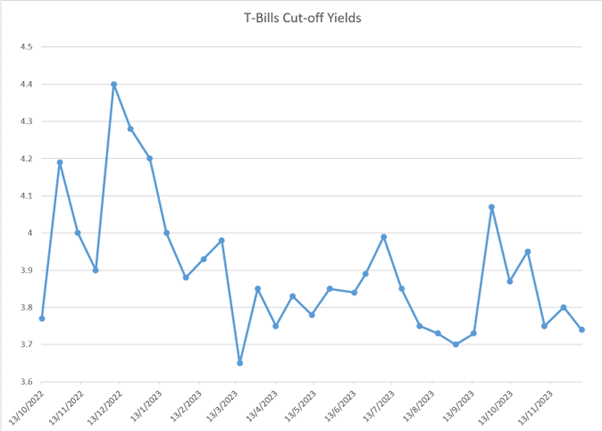

This caused T-Bills yields to drop to 3.74% (vs 3.80% the previous auction)

This led to a drop in T-Bills yields to 3.74% (3.80% the previous auction).

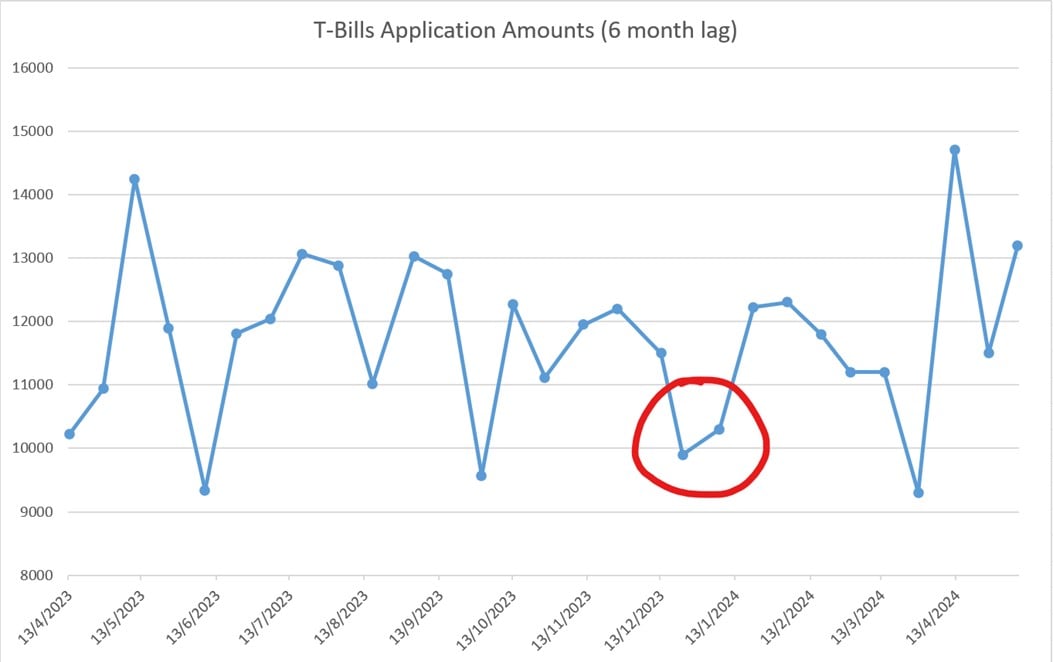

What about T-Bills demand from 6 months ago?

Some of you have requested for a chart showing T-Bills demand from 6 months ago.

The thinking is that if T-Bills demand was very high 6 months ago, it stands to reason that a lot of that money would be maturing today – contributing to higher T-Bills demand.

I’m not entirely sure if I agree with that line of reasoning.

Because regardless of T-Bills demand, the T-Bills supply doesn’t change.

So if I didn’t get T-Bills 6 months ago, chances are I would have placed it into another instrument (unlikely to be 6 month duration), so the predictive ability of this data may not be high.

Whatever the case, I have plotted T-Bills Application Data with a 6 month lag below.

You can see how 6 months ago, T-Bills demand dropped quite sharply.

Going by this logic, T-Bills demand should drop, which doesn’t really tally with recent data (showing a stabilisation at record levels of demand).

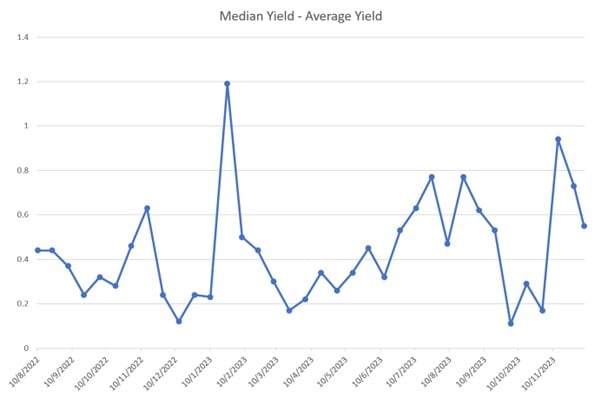

Median Yield – Average Yield spread jumped – a lot of “lowballers”?

To illustrate what this is:

Imagine you have 100 bids.

The median yield, is if you arrange all the bids from small to high, and take the yield of the 50th bid.

While average yield, is adding up the yields of all 100 bids and dividing by 100.

So average yields are skewed by lowball bids, while median yields are not.

To put it simply – the bigger the spread between the median yield and average yield, the more “low-ballers”.

And with the most recent 2 T-Bills auction before this, spreads completely blew out – close to the highest in 2023.

In the latest auction – spread have come down slightly, but still remains very much on the high side.

This indicates that there is still a lot of inelastic demand for T-Bills out there.

Investors are so desperate to get their hands on T-Bills that they are just submitting low-ball bids, to ensure they get an allotment.

Even if this skews yields to the downside.

Estimated yield of 3.65% – 3.80% on the 6-month T-Bills auction? (BS23125H 6-Month T-bill)

Let’s put it all together.

Market is now pricing in up to 6 interest rate cuts in 2024.

This is reflected in a sharp drop in US interest rates both at the short and long end.

Meanwhile demand for T-Bills remains at record levels, and spread data indicates that bidders are submitting low-ball bids to ensure an allotment.

Given all of the above – I’m not that optimistic for yields at this next T-Bills auction.

I would probably go with an estimated yield of 3.65% – 3.80% on the next T-Bills auction.

Should you submit a competitive or non-competitive bid for T-Bills?

I usually encourage investors to submit a competitive bid (just in case there is a freak result and yields drop a lot).

And submit as close to the deadline as you can, so you can take a look at where market pricing is at that time before deciding on your bid.

But I know some investors really don’t like competitive bidding.

In which case non-competitive bidding is probably fine as well (saw close to full allotment the previous auction).

But do note that with non-competitive, if there is a freak result and yields drop to 3.0%, you are still forced to buy.

What yield to submit with competitive bidding for T-Bills?

Some of you have asked how to approach competitive bidding for T-Bills.

Apparently there are others out there who are advocating for submitting ridiculously low bids like 1.5% just to ensure you get an allotment.

I don’t really agree with that kind of reasoning, and if everyone were to do that you’ll see T-Bills close are ridiculously low yields.

I would say to think about the minimum yield you are prepared to buy the T-Bills.

Let’s say any yield below 3.60% and you would prefer to just go with fixed deposits or money market funds.

Then a competitive bid around the 3.60% range may make sense.

Don’t forget that you can submit multiple bids.

So you can submit a bid for $20,000 of T-Bills at 3.60%, and another $10,000 at 3.75%.

This effectively allows you to buy more T-Bills if yields close high, and yet still get some if yields close low.

Are T-Bills still worth buying vs Singapore Savings Bonds or Fixed Deposit or Savings Accounts?

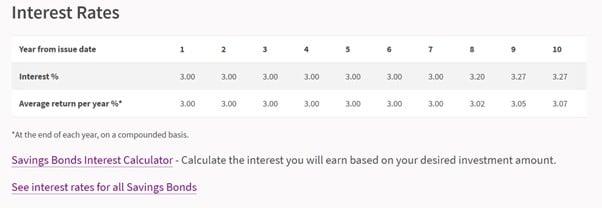

Singapore Savings Bonds are not an attractive buy

Because of the sharp drop in 10 year interest rates this month.

Singapore Savings Bonds are not as attractive as they were last month – and likely to drop further next month.

You’re looking at about 3%ish first year yield.

Personally I have enough Singapore Savings Bonds for now, and I’m going to be skipping this month’s Singapore Savings Bonds.

Although investors who want to lock in yields can consider SSBs as an alternative to T-Bills.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

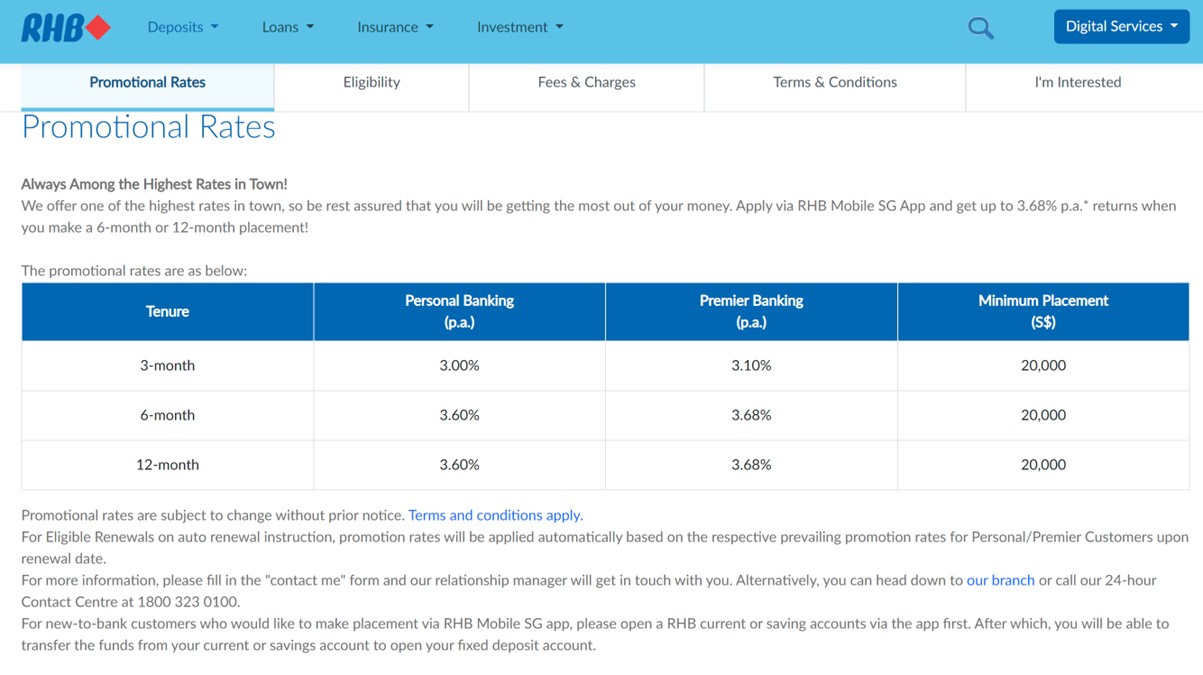

Best Fixed Deposit option instead of T-Bills? RHB Bank at 3.68%

The best Fixed Deposit option I could find today is RHB at 3.60% for 6 months.

Minimum of $20,000, that steps up to 3.68% if you are premier banking.

So if you don’t want to buy T-Bills, this is probably the next best thing.

Money Market Funds pay about 3.6% – 4.2% yield (better than T-Bills?)

With the drop in T-Bills yields, money market funds are actually looking pretty attractive yield wise.

Mari Invest, which is the money market fund solution via Mari Bank in a tie up with Lion Global, pays about 3.6% – 4.3% (exact yield fluctuates over time due to the nature of the instrument).

Whereas Fullerton SGD Cash Fund pays about 3.6% – 3.8%.

Money Market Funds are technically not risk free though – so this is a big point to note.

The benefit though, is that you can get your money back with T+1 liquidity, which is a big plus vs T-Bills.

Note also that Syfe Cash+ Guaranteed pays 4.0% for 3 months, and 3.9% for 6 months, which is likely higher than T-Bills rates. But like Money Market Funds, it is technically not risk free (and money is locked up for the duration unlike MMFs).

Picking between T-Bills vs Singapore Savings Bonds vs Fixed Deposit vs Savings Accounts vs money market funds?

I would say if you want the highest short term yield, T-Bills are probably your best bet if you want something risk free.

The drawback with T-Bills is the (1) lack of liquidity, and (2) short duration of 6 months.

So you can’t put all your money in T-Bills too.

If you want liquidity, money market funds are a decent option, and currently offer yields very competitive (potentially higher) than T-Bills. But money market funds are not risk free.

Singapore Savings Bonds are not as attractive anymore after the drop in 10 year interest rates, but still a viable option if you want to lock in yields long term.

Where am I parking my cash for liquidity?

Apart from T-Bills, I’ve been parking my cash in a mix of the following for liquidity:

|

Instrument |

Approx Yield |

Maximum |

|

UOB One |

5% |

$100,000 |

|

Singapore Savings Bonds |

3%+ |

$200,000 |

|

MariBank Account |

2.88% – 3.5% |

$75,000 |

|

Mari Invest (or other Money Market Fund) |

3.6% – 4.3% |

No maximum (not risk free) |

Maribank (2.88%) vs GXS (2.68%) or Chocolate Finance (4.5%) for cash

In the past I also tried GXS (2.68%) and Chocolate Finance (4.5%) for cash.

But MariBank by Shopee has higher yields (2.88%) than GXS while being SDIC insured so it’s a no brainer.

The 2.88% offer has also been extended to 31 March 2024.

While Chocolate Finance is technically not risk free (4.5% on $20,000), so I hesitate on putting too much in as well.

Maribank Promo Code for FH Readers (extra $10 Shopee Voucher)

For those keen on Maribank.

Maribank very kindly reached out to offer an exclusive promo code for FH Readers

Sign up for a Mari Savings Account (using the promo code “MARI28FH”) and get a $10 Shopee voucher with no min spend.

Full disclosure that I don’t get any benefit from you guys using this code, so the benefit is all yours. ????

The Maribank Savings Account pays 2.88% on up to $75,000, with no minimum amount, no hoops to jump through, and SDIC insured.

Pretty much a no brainer if you have spare cash and want to generate a higher yield without any lockup or any requirements to fulfil.

Promo ends 31 Dec 2023, Full T&Cs here.

Am I applying for T-Bills?

I have a lot of T-Bills that just matured this week.

I will likely roll some of that money into new T-Bills.

Where yields fall is a big question mark, so I will use competitive bidding to avoid any freak results.

If yields come in below a certain level, I might be better off just parking the funds in a money market fund instead.

Love to hear what you think though – will T-Bills yields drop further? Are you applying for T-Bills?

This article was written on 14 Dec 2023 and will not be updated going forward.

For my latest up to date views on markets, my personal REIT and Stock Watchlist, and my personal portfolio positioning, do subscribe for FH Premium.

WeBull Account – Get up to USD 5000 worth of shares (Best promo of 2023 – Now Extended)

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now (Best Promo of 2023)

You can get up to USD 5000 free shares.

You just need to:

- Sign up for a WeBull Account here

- Fund any amount (get 5 free shares)

- Hold for 30 days (get 5 free shares)

OCBC Online Equities Account – Trade on 15 global exchanges, all via the OCBC Digital Banking App!

Did you know that can you trade shares on your OCBC Digital Banking App?

With an OCBC online equities account, you can buy stocks, local ETFs, REITs, bonds and more directly through your banking app.

Even better? Enjoy reduced commission rates of just 0.05% for buy trades on SG, US and HK market until 31 December 2023.

Everything on one app! Fuss-free funding, with access to 15 global exchanges

For SGD trades, you can fund and settle automatically via your OCBC account.

And for FX trades, you can settle using the foreign currency held in your OCBC Global Savings Account.

This means fuss-free trade settlement and minimising forex costs – saving you time and money.

Start trading with your OCBC Online Equities Account here!

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Investment Research Tools

I use Trading View for my research and charts. Get $15 off via the FH affiliate link.

I also use Koyfin for fundamental and macro research. Get a 10% discount via the FH affiliate link.

Portfolio tracker to track your Singapore dividend stocks?

I use StocksCafe to track my portfolio and dividend stocks. Check out my full review on StocksCafe.

Low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Best investment books to improve as an investor in 2023?

Check out my personal recommendations for a reading list here.

Hi FH, may I ask your opinion on a matter: I have a sum of money for a major purchase 3-4 years later. Considering how seemingly chaotic the world is now (Ukraine Russia war, Hamas Israel conflict, and the foreseeable interest rate cuts), and I’m not very investment savvy. I have some equity unit trusts and some fixed income unit trusts for retirement (longer term horizon). But if I need the money 3-4 years later, which is the better option?

1. Buy this month’s SSB at 3% for first 4 years?

2. Keep buying and renewing this sum in 6-month t bills for 3-4 years?

3. Is 3-4 years long enough/safe enough to invest this sum in equity unit trusts?

4. Are short duration fixed income unit trusts (like Nikko AM Shenton Short Term Bond SGD) reliable options?

5. Or can also consider longer term fixed income unit trusts?

6. Or can consider a combination of some of the above options?

I think the key when I saw this was your own disclaimer than you are not very investment savvy.

If you’re not savvy, equity markets may be a bit too risky for the given timeframe.

I would probably say a mix of the risk free options of T-Bills and SSBs. If you want a bit more risk, can add some allocation to the short term bond funds with 3 – 4 year durations (can buy via Syfe or Endowus).